Denis Cook

March 5, 2026

How Big Is the Transferable Tax Credit Buyer Market, and How Fast Is It Growing?

The first of five data-driven posts exploring how companies are participating in the transferable tax credit market.

For Buyers

For Sellers

Section 6418 of the Inflation Reduction Act created a new market for companies to purchase clean energy tax credits – a mechanism that previously didn't exist in U.S. tax code. Two years in, we took a look at the buyer universe to understand its size and composition.

How Many Companies Have Publicly Disclosed Transferable Tax Credit Purchases?

As of early March 2026, 119 public companies – approximately 8.4% of the ~1,400 largest U.S. public companies – have disclosed purchasing transferable tax credits in SEC filings.

Reunion analyzed over 6,000 public filings across approximately 1,400 of the largest U.S. public companies to quantify buyer participation. ASU 2023-09, a new accounting standard in effect for fiscal years beginning after December 15, 2024, requires more granular tax disclosures by public companies and makes credit purchases easier to verify.

The above count reflects human-verified disclosures in 10-K, 10-Q, 20-F, and 40-F filings filed since January 1, 2025. The 119 verified purchasers span 30+ states and 11 industry sectors. They range from Fortune 100 corporations to regional banks.

How Fast Is the Transferable Tax Credit Market Growing?

Across the nearly 1,000 public companies in our dataset that filed annual disclosures in both 2024 and 2025, we found that the share of firms disclosing tax credit purchases rose from 4.9% in 2024 to 8.5% in 2025 – an increase of approximately 74%.

Growth was broad-based across sectors and company sizes, though it was particularly pronounced among smaller taxpayers. Companies with under $200M in annual tax expense doubled their purchase rate. Participation is broadening thanks to more standardized deal structures, increases in credit supply, and clarified IRS guidance.

Why This Matters

The transferability provision of the IRA fundamentally expanded the buyer community beyond the small group of traditional tax-equity investors that historically participated in clean energy finance. Any corporation with federal tax liability can now purchase credits directly, and the filing data shows they are doing so in increasing numbers. The 119 verified purchasers represent only publicly disclosed transactions. The actual buyer count, including private companies and transactions below disclosure thresholds, is almost certainly larger.

For the next post that explores tax credit purchase rates by company size and effective tax rates, click here.

Reunion maintains a database of public companies that have disclosed transferable tax credit purchases, available to entities buying or selling credits, and provides exclusive access to the underlying SEC data to existing buy-side and sell-side clients of Reunion. Reach out to your Reunion contact for access.

Data Notes

Analysis Period: February-March 2026

Universe: ~1,400 largest U.S. public companies

Filings Reviewed: 10-K, 10-Q, 20-F, 40-F filed since January 1, 2025

Methodology:

- Credit Classification: Many filings reference transferable credits without specifying type. These are classified as clean energy credits since transferability is generally tied to Section 6418.

- Sample Composition: Of approximately 1,400 companies, roughly 1,000 had filed both 2024 and 2025 reports during the analysis window. The remainder had not yet filed 2025 reports or had 2024 filings published before data collection began.

- Data Quality: An AI-assisted process was used to scan filings. All identified purchasing activity was then human-verified at the company level.

Connor Danik

February 20, 2026

Section 45Z Proposed Regulations Are Out — What Changed?

On February 3, 2026, the Department of Treasury and the Internal Revenue Service (IRS) issued proposed regulations for the Clean Fuel Production Credit.

For Buyers

For Sellers

On February 3, 2026, the Department of Treasury and the Internal Revenue Service (IRS) issued proposed regulations for the Clean Fuel Production Credit (§45Z). The proposed regulations were published in the Federal Register on February 4, 2026, and are generally consistent with the prior guidance issued.

Noted below are key changes and additions, as well as clarifying or confirmatory guidance that was issued in the proposed regulations.

Jump to a section:

Sold for use in a trade or business

A taxpayer is eligible for the 45Z credit only if it produces transportation fuel and subsequently sells it to an unrelated person (i) for use by such person in the production of a fuel mixture, (ii) for use by such person in a trade or business, or (iii) such person sells such fuel at retail to another person and places such fuel in the fuel tank of such other person. The proposed regulations confirm that the term “sold for use in a trade or business” includes sales of fuel to an intermediary or reseller. The definitions in Section 3.03(7) and the "Appendix - Draft Text of Forthcoming Proposed Regulations" of Notice 2025-10 previously defined the term to mean fuel sold for “use as a fuel” in a trade or business. After stakeholders raised concerns that this language could prevent sales for resale, the proposed regulations removed the “use as a fuel” requirement from the definition of “sold for use in a trade or business.” The proposed regulations also conforms the definition for “sold for use in a trade or business” with the meaning under Internal Revenue Code Section 162.

Safe Harbor Certificates

The proposed regulations introduce two new safe harbors for substantiating the emissions rate for a transportation fuel as well as substantiation for qualified sales. For non-SAF transportation fuel, taxpayers may substantiate an emissions rate determined under the 45ZCF-GREET model by obtaining a certification in substantially the same manner required for sustainable aviation fuel (SAF) under proposed regulation §1.45Z-5. For qualified sales, taxpayers may obtain from the purchaser a certificate in substantially the same form as described in proposed regulation §1.45Z-4(g)(3)(ii). However, a key requirement is the taxpayer must obtain the certificate from the purchaser prior to or at the time of sale (or, for multiple sales, before or at the first covered sale). In addition, the proposed regulations state the Purchaser agrees to provide the person liable for tax with a new certificate if any information in the certificate changes.

Related Party Sales

The proposed regulations adopt a broader related-party “look-through” rule. Under Notice 2025-10, a taxpayer that is a member of a consolidated group is treated as selling fuel to an unrelated person if another member of the group (the related person) ultimately sells the fuel to an unrelated person. Under the broader related-party rules, a taxpayer that is not a member of a consolidated group is also treated as selling fuel to an unrelated person if and when a related person sells the fuel to the unrelated person.

Energy Attribute Certificates & Incrementality

Certain taxpayers may purchase energy attribute certificates (EACs) such as renewable energy certificates (RECs) to reduce their carbon intensity score and resulting emissions rate. The proposed regulations confirm that when incorporating EACs into the 45ZCF-GREET model, rules similar to final regulation §1.45V-4(d) apply. When applying the rules for purposes of the 45ZCF-GREET-Model, the facility is considered placed in service in the first taxable year it produces transportation fuel. The proposed regulations require the EAC-generating facility (or if the EAC facility uses carbon capture and sequestration technology) to have a commercial operations or placed in service date no more than 36 months prior to the first day of the taxable year in which the 45Z facility first produced transportation fuel.

Emissions Rate Table

The proposed regulations clarify that the applicable emissions rate table establishes the emissions rate for a fuel if the emissions rate table includes both the type and category of that fuel. The applicable emissions rate table for a taxpayer is the first publicly available emissions rate table that is in effect during the taxpayer's taxable year of production. However, if an allowed methodology is updated with respect to an included type or category of fuel and is publicly available after the first day of the taxable year of production (but still within such taxable year), then the taxpayer could choose to treat such updated version as the most recent version of such methodology. If an emissions rate table does not initially include a type or category of fuel but an allowed methodology is updated to add such type or category during the calendar year, then that fuel type or category will be considered included in such emissions rate table, and an impacted taxpayer must use this version as its the first publicly available version that includes its type and category of fuel.

Facility Ownership

The proposed regulations confirm the taxpayer is not required to own the qualified facility and credit eligibility is tied to the production of transportation fuel at a qualified facility and subsequent qualified sale.

Timing of Sale

The proposed regulations confirm that production of a transportation fuel may occur in a prior taxable year than the taxable year in which the qualified sale of the fuel occurs, but that a qualified sale may not occur before the date the fuel is produced.

Double Crediting

Code §45Z(d)(5)(A)(iv) states transportation fuel means a fuel which “is not produced from a fuel for which a credit under this section is allowable.” The proposed regulations clarify that the first transportation fuel in the production chain qualifies for the §45Z credit. However, a fuel could still qualify for the §45Z credit if its production process uses a transportation fuel solely as a process fuel or other non-primary-feedstock input.

Feedstock

The proposed regulations confirm that transportation fuel produced after December 31, 2025, must be exclusively derived from a feedstock that was produced or grown in the United States, Mexico, or Canada.

Negative Emissions Rate

Except for transportation fuel in which its primary feedstock is derived from animal manure, the proposed regulations confirm that the emissions rate may not be less than zero for any transportation fuel produced after December 31, 2025.

Indirect Land Use

The proposed regulations confirm that the emissions rate should exclude any emissions attributed to indirect land use change for transportation fuel produced after December 31, 2025.

Production

The proposed regulations clarify that the term production must involve substantial processing by the producer and does not include instances in which a person engages in minimal processing such as creating a fuel mixture or otherwise engaging in activities that do not result in a chemical transformation. For example, this definition of production would exclude any person that removes conventional or alternative natural gas (CANG) from a pipeline, compresses it further after removal, and then sells such further compressed CANG; compression of CANG that is already interchangeable with fossil natural gas would also not meet the proposed definition of production.

Carbon Capture Equipment

The proposed regulations confirm carbon capture equipment will be considered a part of the qualified facility if the equipment contributes to the lifecycle GHG emissions rate of the transportation fuel, which includes emissions from all stages of the fuel’s production and use, including feedstock production and transportation, fuel production and distribution, and use ofthe finished fuel.

Undenatured Ethanol

There was an open question if undenatured ethanol would qualify as transportation fuel as the previous guidance only referenced denatured ethanol. The proposed regulations clarify that undenatured fuel ethanol that meets the qualifications of ASTM D8651 for blending with gasoline and that has an emissions rate that is not greater than 50 kilograms of CO2e per mmBTU meets the definition of non-SAF transportation fuel.

Suitable Use

Code §45Z(d)(5)(A)(i) specifies transportation fuel means a fuel which “is suitable for use as a fuel in a highway vehicle or aircraft.” The proposed regulations clarify that actual use as a fuel in a highway vehicle or aircraft is not required.

Written or electronic comments must be received by April 6, 2026 and a public hearing will be held on May 28, 2026. Taxpayers may rely on the proposed regulations as long as they rely on them in their entirety and in a consistent manner.

Katherine Westcott

February 19, 2026

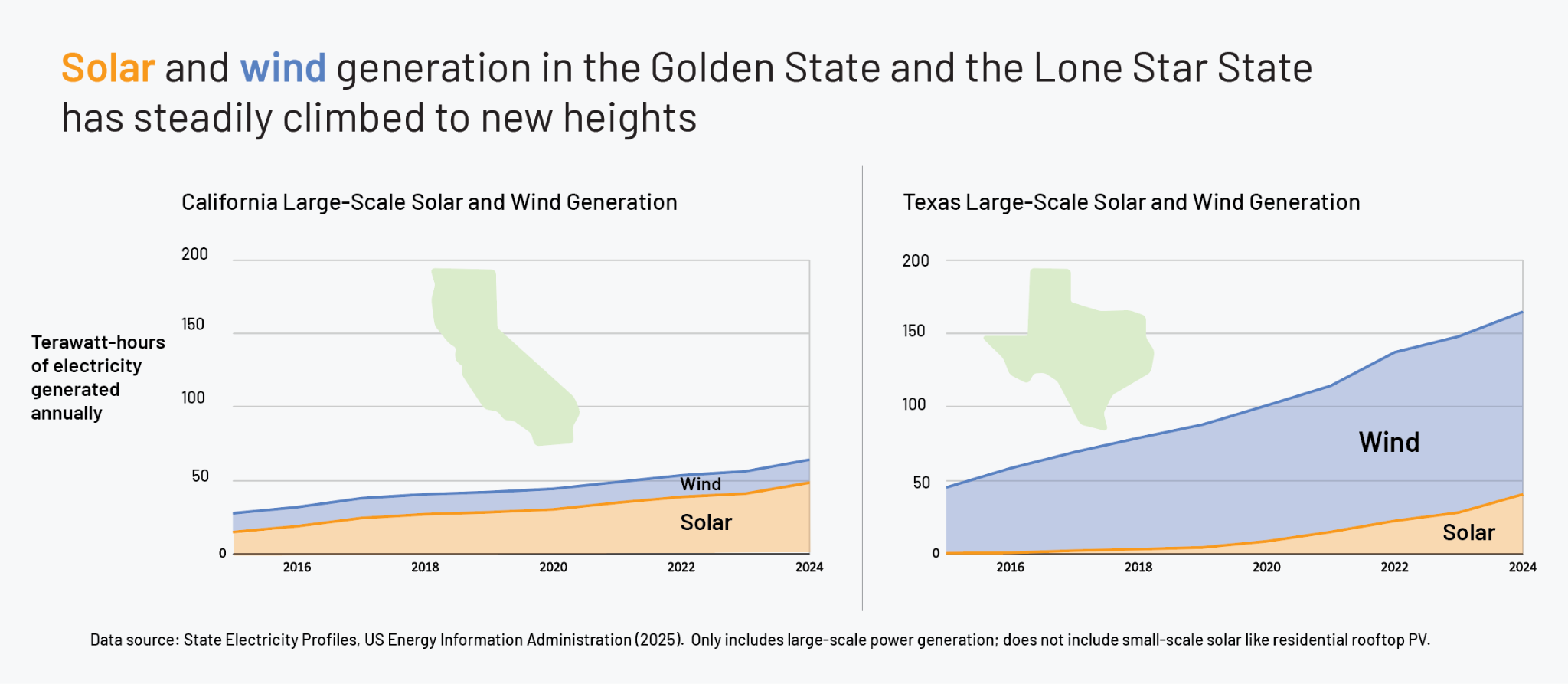

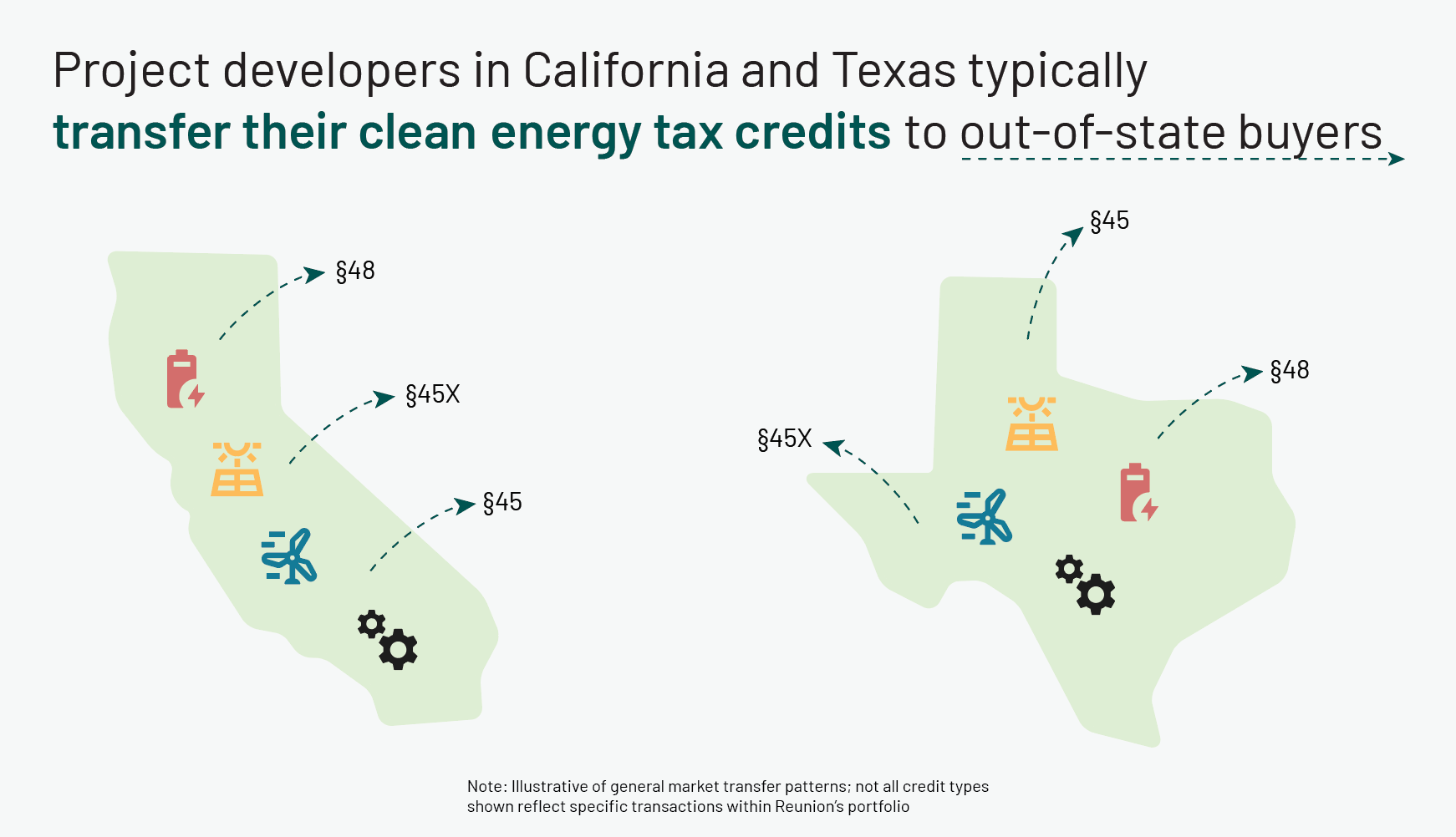

Footnote of the Week: California and Texas have a Common Export — Transferable Energy Tax Credits

We calculate that in more than 90% of cases, project developers and manufacturers in California and Texas ultimately transferred their tax credits to out-of-state buyers.

For Buyers

For Sellers

When it comes to clean energy in America, California and Texas are a central part of the story. The Golden State leads the nation in installed solar power, while the Lone Star State claims second place. Meanwhile, Texas produces far more wind power than any other state. The charts below track the remarkable year-on-year growth in electricity production from large-scale solar and wind in the nation’s two most populous states. (California’s vast adoption of rooftop solar isn’t presented here, but tells a similar growth story.)

This expansion of renewable power has occurred alongside the rise of other innovations in these states – including energy storage and manufacturing of clean energy components (e.g., solar modules and battery cells).

Reunion’s portfolio of work has included numerous clean energy deals in California and Texas – ranging from wind turbines to fuel cells to batteries. Since these projects generate transferable tax credits, we were curious to what degree these credits have been transferred to in-state entities versus out-of-state entities.

We calculate that in more than 90% of cases – across many technology types and deal types (§45 production credit, §45X manufacturing credit, and §48 investment credit) – project developers and manufacturers in California and Texas ultimately transferred their tax credits to out-of-state buyers. We inferred buyers’ location from the address of their corporate headquarters. (Note: Our assessment makes an allowance for the reality that a portion of Californian and Texan buyers acquire in-state credits in a manner that is neither visible to nor transacted via Reunion’s platform.)

The frequent export of tax credits may seem surprising at first glance for California and Texas, given that many Fortune 1000 companies are headquartered in those states and likely have the tax appetite to purchase transferable credits. However, the interstate movement of these tax credits is a positive validation of their transferable nature – which was designed to accelerate the deployment of clean energy nationwide, and is making good on that promise through a geographically flexible framework.

Katherine Westcott

February 5, 2026

Footnote of the Week: Among Insured Tax Credit Deals, Many Have Coverage Levels of 110% or Higher

For transactions that include insurance, our data reveals that the Limit of Liability often exceeds the face value of the tax credit.

For Buyers

For Sellers

In discussions of energy tax credit transfers, much of the focus goes to headline numbers like pricing, deal sizes, and types of credits. A less discussed element that can make or break a deal is tax credit insurance. The demand for tax credit insurance, which is designed to protect the value of tax credits in the event of an IRS challenge, has grown significantly since the start of transferability.

Since Reunion began facilitating tax credit transfers in 2023, about 40 percent of our transactions have included tax credit insurance coverage. As shown in the colored bars below, most of this insurance coverage has had a Limit of Liability equal to or greater than 100%. Conversely, the black bar represents the roughly 60 percent of deals that did not include insurance, suggesting cases in which the tax credit seller could provide a sufficiently strong indemnification, or the parties were comfortable with the risk-reward of the credits being transferred.

The pattern of Limits of Liability commonly exceeding 100% is noteworthy, and implies that many tax credit buyers want protection from second-order risks such as penalties and legal fees that could arise from a disallowance or recapture. To gauge the upper range of these Limits of Liability, we dug into the tax credit type that we’ve seen insured most frequently: §48 investment tax credits.

For §48 transfers, the Limits of Liability have pushed markedly higher than face value – with a little over half of insured deals hitting 110% or higher, and multiple deals establishing Limits of Liability greater than 130%. (The small share of deals with a liability limit below 100% are primarily distributed or residential energy assets; this coverage is designed to support a partial loss, rather than a less likely portfolio-wide loss event.)

While tax credit insurance isn’t warranted on every deal, it plays an important role in enabling tax credit transfers among risk-sensitive buyers, especially when the seller is not investment grade. Our analysis suggests that relatively high Limits of Liability are supported by the market, and may give buyers access to a wider range of tax credit opportunities.

Denis Cook

January 8, 2026

ASU 2023-09 should highlight adoption of IRA clean energy tax credits

ASU 2023-09, Improvements to Income Tax Disclosures, requires public and private companies to provide a more detailed tax rate reconciliation in their financial statements. Participation in the transferable clean energy tax credit market should become more clear.

For Buyers

For Sellers

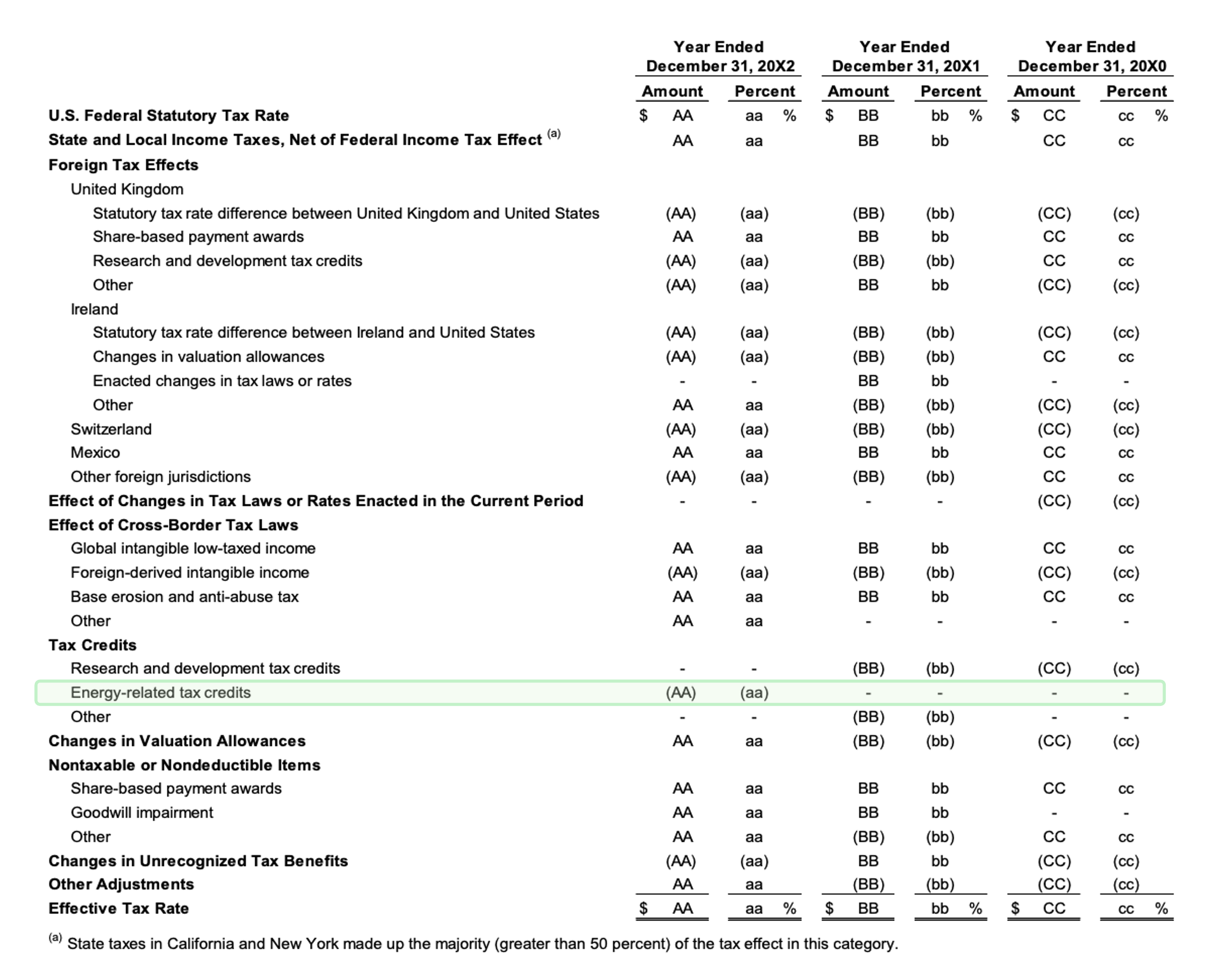

Overview of ASU 2023-09

Accounting Standards Update (ASU) 2023-09, Improvements to Income Tax Disclosures, represents the FASB’s latest effort to modernize and enhance income tax disclosures under ASC 740, with a clear emphasis on improving transparency around effective tax rate drivers and cash taxes paid.

For corporate tax professionals, the update is less about changing tax accounting and more about significantly expanding what must be explained – and supported – in the tax footnote.

At its core, 2023-09 requires companies, public and private, to provide a more robust and structured explanation of why their effective tax rate differs from the statutory federal rate. The rate reconciliation must now be presented in a tabular format that includes both dollar amounts and percentages, and reconciling items must be categorized using prescribed groupings such as state and local taxes, foreign tax effects, tax credits, valuation allowance changes, and changes in tax laws.

When reconciling items exceed a quantitative threshold – generally 5.0% of the tax at the statutory rate – further disaggregation is required, often by nature or jurisdiction. The result is a more decision-useful, but also more data-intensive, reconciliation.

When do the disclosure updates go into effect?

ASU 2023-09 applies to public business entities (PBEs) and non-PBEs. Simplistically, a PBE is a public company, while a non-PBE is a private company.

The new requirements within ASU 2023-09 go into effect at different dates, depending on the type of entity:

- PBEs: Annual periods beginning after December 15, 2024 – generally, calendar year 2025

- Non-PBEs: Annual periods beginning after December 15, 2025 – generally, calendar year 2026

Impacts on transferable tax credit investments

ASU 2023-09 does not change the accounting for transferable tax credits, but it will make their financial statement impact more visible through enhanced income tax disclosures.

Most notably, tax credits that materially reduce tax expense will need to be more clearly reflected in the effective tax rate reconciliation. Under the new standardized categories and quantitative thresholds, significant transferable credits are likely to be disclosed as a separate reconciling item rather than being aggregated within broader “credits” or “other” categories, increasing transparency around their role in lowering the effective tax rate.

The new income taxes paid disclosure also affects companies that utilize transferable credits. Because these credits often reduce cash taxes owed, companies may report low or minimal taxes paid in certain jurisdictions. ASU 2023-09 requires income taxes paid, net of refunds, to be disaggregated by federal, state, and foreign jurisdictions, with separate disclosure for significant jurisdictions, making the disconnect between tax expense and cash taxes paid more apparent.

Finally, while the ASU is disclosure-focused, it may drive additional documentation and controls around transferable credits. Companies should expect greater scrutiny of the nature, materiality, and sustainability of tax credit investments, as well as more robust explanations in the tax footnote regarding how those credits affect both the effective tax rate and cash tax profile.

Sample income tax disclosure

ASU 2023-09 includes a “sample rate reconciliation between income tax expense (or benefit) and statutory expectations.”

Companies that have disclosed a transferable tax credit purchase

Reunion maintains a list of public companies that have disclosed a transferable tax credit purchase through an SEC filing. We invite you to request access to the evolving list.

Alex Melehy

December 29, 2025

What Are the Prevailing Wage and Apprenticeship (PWA) Requirements for Clean Energy Tax Credits?

The IRA's Prevailing Wage & Apprenticeship (PWA) requirements are the gateway to the full 5x clean energy tax credit multiplier. Projects that comply unlock credits worth five times the base rate; those that don't forfeit up to 80% of their potential value.

For Sellers

To create a robust market for well-paying clean energy jobs, the Inflation Reduction Act (IRA) radically transformed the economics of clean energy project development by introducing Prevailing Wage and Apprenticeship (PWA) requirements.

For developers, EPCs, and tax equity investors, PWA compliance is not just an administrative checklist—it is the key to unlocking project viability. Projects that comply with PWA requirements receive a tax credit that is five times greater than the base rate. Conversely, failing to meet PWA standards means forfeiting up to 80% of a project's total potential credit value.

Here is the definitive breakdown of what PWA compliance entails, which tax credits are impacted, and the specific thresholds developers must navigate.

The Two Pillars of PWA

PWA is divided into two distinct components: prevailing wage requirements and apprenticeship requirements.

1. Prevailing Wage Rules

All laborers and mechanics employed by the developer, contractors, or subcontractors must be paid a minimum prevailing wage specified by the U.S. Department of Labor (DOL). Prevailing wages must be paid during the construction of the facility, as well as during any alteration or repair work for a set number of years after the project is Placed in Service (PIS) (the number of years depends on the credit type**)**. It is important to note that workers do not have to be paid prevailing wages for basic maintenance work, which is “routinely scheduled and continuous or recurring.” Examples of basic maintenance are regular inspections of the facility, regular cleaning and janitorial work, regular replacement of materials with limited lifespans such as filters and light bulbs, and the calibration of any equipment.

2. Apprenticeship Requirements

The apprenticeship rules fall into three strict categories:

- Labor Hours: A specific percentage of total construction labor hours must be performed by qualified apprentices. For projects beginning construction in 2024 or later, this requirement is 15% (compared to 12.5% for projects started in 2023).

- Ratio Requirement: Contractors must adhere to daily apprentice-to-journeyworker ratios as prescribed by the associated registered apprenticeship program (the program that apprentices are sourced from).

- Participation: Any contractor or subcontractor employing four or more laborers or mechanics must hire at least one qualified apprentice.

Crucially, apprenticeship requirements do not apply after a facility has been placed in service. Post-PIS compliance applies only to prevailing wages for alterations and repairs.

Which Credits Are Subject to PWA?

Of the 11 clean energy tax credits eligible for transfer, 10 are subject to PWA requirements. The sole exception is the §45X Advanced Manufacturing Production Credit, which is entirely exempt from PWA rules.

PWA Exemptions: The BoC and 1 MW Thresholds

There are two primary ways a project might be exempt from PWA requirements entirely:

- Beginning of Construction (BoC): Projects that successfully established beginning of construction before January 29, 2023, are strictly exempt from PWA rules, except for §48C and §45Z credits.

- The 1 Megawatt (MW) Threshold: Under §45 and §48 (and their tech-neutral replacements, §45Y and §48E), projects with a maximum net output of less than 1 MW (measured in alternating current) are automatically exempt from PWA.

Quick Reference: PWA Duration by Tax Credit Type

Depending on the tax credit, prevailing wage requirements extend well into the operational life of the asset.

Because retroactive PWA compliance is exceptionally difficult and expensive, clean energy developers and EPCs must implement structured tracking from day one. By utilizing purpose-built compliance software and subject matter experts, developers can automatically flag noncompliance, cure underpayments, and secure bankable compliance reports that protect their 5x credit multiplier.

Denis Cook

December 10, 2025

Reunion's Q3 2025 Transferable Tax Credit Pricing and Markets Update

Reunion’s Q3 Market Monitor print highlights moderate tax credit pricing declines, but continued market maturation

For Buyers

For Sellers

Reunion recently released our Q3 Market Monitor update, including forward-looking pricing estimates through Q4 of this year.

Overall, our data highlights two seemingly divergent trends: (1) softened demand for 2025 tax credits alongside (2) increased market maturity and liquidity.

To better understand this dynamic, this note examines six key trends from our data:

- Pricing: 2025 tax credit prices have declined compared to 2024 levels, primarily due to the OBBBA

- Market dynamics: Sections 45U and 45Z are becoming increasingly popular production credits

- Transaction timing: 10% of 2024 tax credit transfers closed in Q3 2025

- Prevailing wage and apprenticeship (“PWA”): Credits that are PWA exempt because of beginning of construction (“BoC”) exemption are vanishingly rare

- FEOC: FEOC will become a key purchase consideration, with upward pricing for credits with low FEOC risk

- Credit adders: Adoption of bonus credit adders continues to expand for ITCs, but remains muted for PTCs

Pricing

2025 tax credit prices have declined compared to 2024 levels

Across virtually all credit types and deal sizes, 2025 pricing declined relative to 2024 levels. This trend has been particularly pronounced in Q3 and Q4. In 2024, prices rose from Q3 to Q4 as buyers competed for increasingly limited supply. In 2025, the trend reversed, with pricing generally softening over the same period.

Investment-grade (“IG”) supply continues to command a premium – ITCs from IG sellers, for example, continued to trade one to three cents above these median levels in late 2025.

*Section 48 ITC pricing is exclusive of residential solar and biogas. Reunion maintains separate pricing series for these technologies.

The following chart compares estimated Q4 2025 to actual Q4 2024 data. This year’s Q4 data is based on deals closed through November and terms sheets executed through the publication date of this note.

*Section 48 ITC pricing is exclusive of residential solar and biogas. Reunion maintains separate pricing series for these technologies.

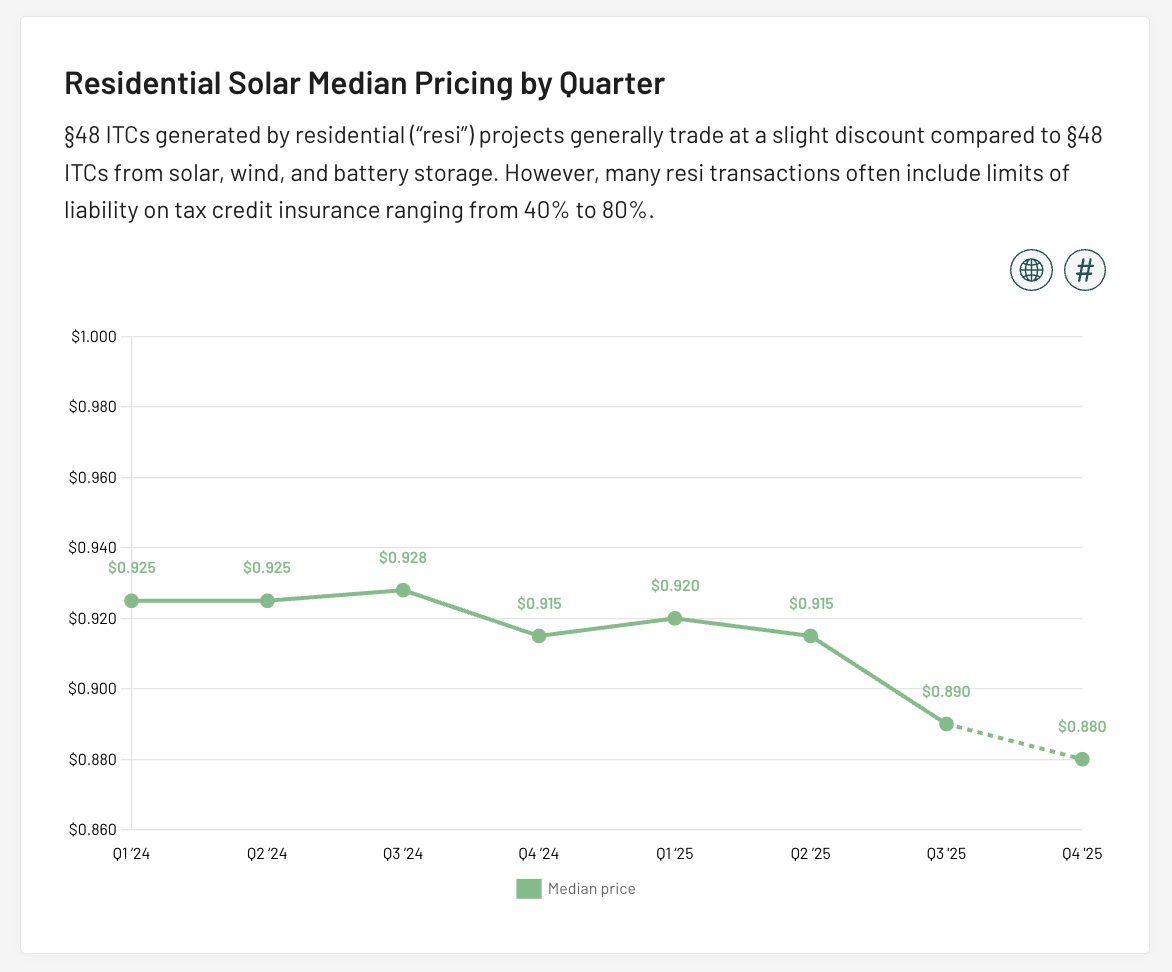

Residential, or “resi,” solar experienced marked price declines throughout 2025 as well. (Reunion maintains separate pricing series for ITCs from resi solar and biogas. We do not include resi and biogas deals in our market-wide Section 48 ITC pricing above.) Looking across 2024 and 2025 vintages, median prices fell from $0.928 in Q3 2024 to an estimated $0.88 in Q4 2025.

When understanding resi prices, it's important to recall that buyers and sellers often negotiate the limit of liability ("LOL") on resi tax credit insurance policies, which flows through to headline pricing. A major resi solar developer, for example, offered a further discount of two cents for an LOL of 40% versus 100%.

While “headline” declines in prices have been modest on a percentage basis, the flow through to cash tax savings has been significant

A corporate taxpayer who purchased a $50M tranche of Section 48 ITCs Q3 2024 and am equivalent $50M tranche of Section 48 ITCs in Q3 2025 would have benefited from an additional $500,000 in cash tax savings – a 14.3% increase.

Tax credit pricing declines in 2025 have largely been driven by impacts of the OBBBA

In the months leading up to the Bill’s passage on July 4, the tax credit market slowed as buyers hesitated to make meaningful commitments without clarity on the final legislation. Many feared that 2025 tax credits might be retroactively repealed and chose to wait for assurance that existing credits would be respected before proceeding with transactions.

The Bill provided clarity that both current- and future-year tax credits will be respected, but the OBBBA itself had a significant downward impact on corporate tax liabilities. Dozens of corporations that were expecting $50M or $100M+ in tax liability no longer had the appetite to purchase 2025 credits.

Today, many companies are still working to understand how OBBBA will affect their final 2025 tax liability – and have delayed purchasing credits as a result.

We expect lingering OBBBA-related impacts on 2026 tax liabilities. As of the publication of this note, Reunion is conducting our year-end tax credit buyer survey, and early feedback suggests that corporations are anticipating reduced 2026 tax liabilities of 10% to 30% against an assumed “non-OBBBA” baseline. Varying degrees of impact tend to cluster in sectors that are particularly sensitive to tax law changes. We’ll publish our year-end buyer report in early 2026.

Although 2026 aggregate demand may be down compared to this non-OBBBA baseline, we are seeing a significant number of taxpayers moving early on 2026 credits. These taxpayers generally fall into two camps:

- Strategic: Companies proactively seeking investments over $50M

- Opportunistic: Companies seeking investments with outsized discounts

We will incorporate pricing for 2026 tax credits in our Q1 2026 Market Monitor release.

Market dynamics

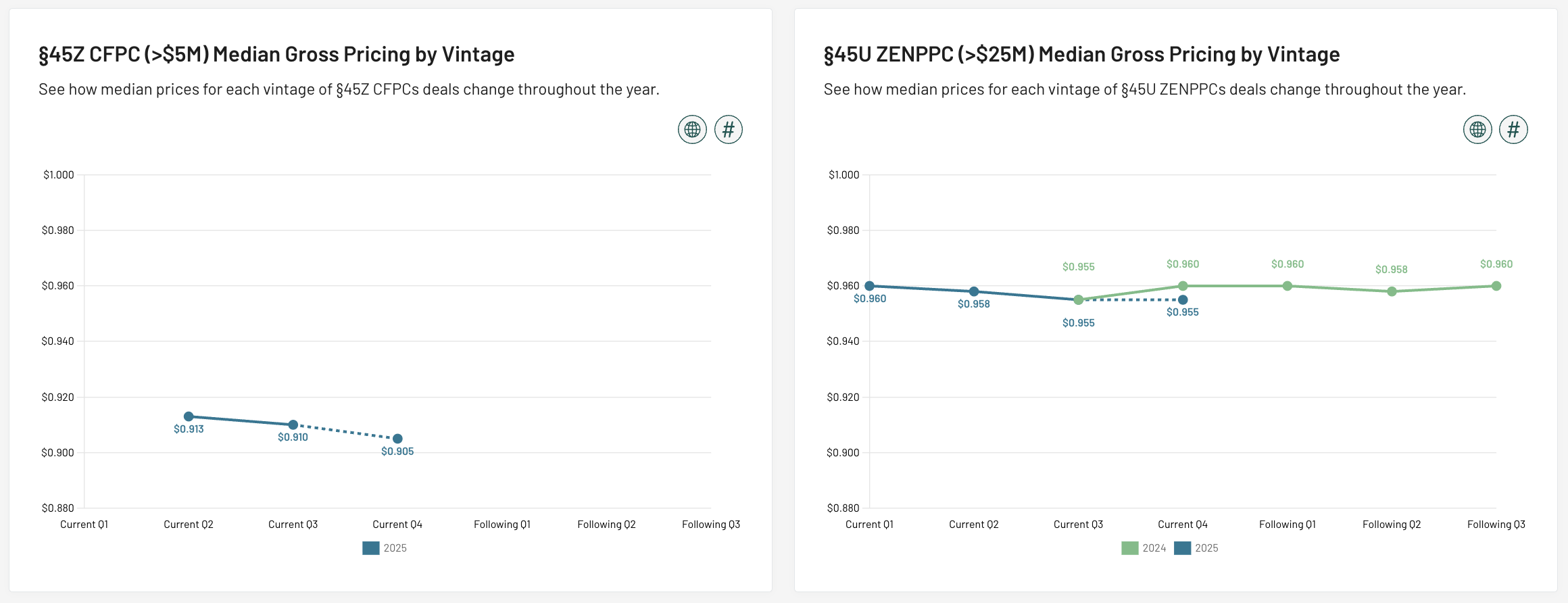

Section 45U nuclear and Section 45Z clean fuels are becoming increasingly popular production credits

In the second half of 2024, a handful of Reunion’s corporate clients explicitly prioritized Section 45U zero-emission nuclear power production credits (“ZENPPCs”). However, the majority of production credit-focused buyers focused on Section 45 PTCs.

As we approach the end of 2025, we have observed that many production credit-focused companies now view 45U ZENPPCs and 45 PTCs with roughly equivalent interest. From a pricing perspective, 45U nuclear credits are among the most stable.

A similar pattern is emerging around Section 45Z clean fuel production credits (“CFPCs”). An increasing number of corporate buyers are actively targeting 45Z credits due to two key factors:

- Risk/return: Section 45Z clean fuel credits are trading in the high $0.80s to low $0.90s, depending largely on the purchase size, presence of tax credit insurance, and the seller’s financial strength. Although this pricing generally aligns with Section 48 ITCs, Section 45Z CFPCs are not subject to recapture.

- General business credit (“GBC”) ordering: Tax credit carrybacks have become more popular, and an effective carryback strategy must account for the credit-ordering rules reflected in IRS Form 3800. Compared to Section 48 ITCs, Section 45Z CFPCs are more advantageous for a carryback from a credit ordering perspective.

To reflect this growing interest, we are now publishing pricing series for both 45U and 45Z credits. Our 45U pricing goes back to 2024, while 45Z begins in 2025 (when the credit first became available).

Although demand for 45Z credits is growing, prices have moderated slightly throughout 2025. We believe this reflects supply dynamics: since the 45Z credit only became available this year, a preponderance of sellers entered the market in the latter half of this year, generally offering full-year tranches of 2025 credits.

Looking ahead to 2026, we expect, and have already begun to see, 45Z deals structured around quarterly payments, akin to many Section 45 PTC transactions. Strips should become increasingly common, too.

The Treasury and the IRS have not yet issued final guidance for either of these credits, though this has not been a gating factor for most buyers. 45Z, in fact, is among the credits that received favorable treatment under the OBBBA.

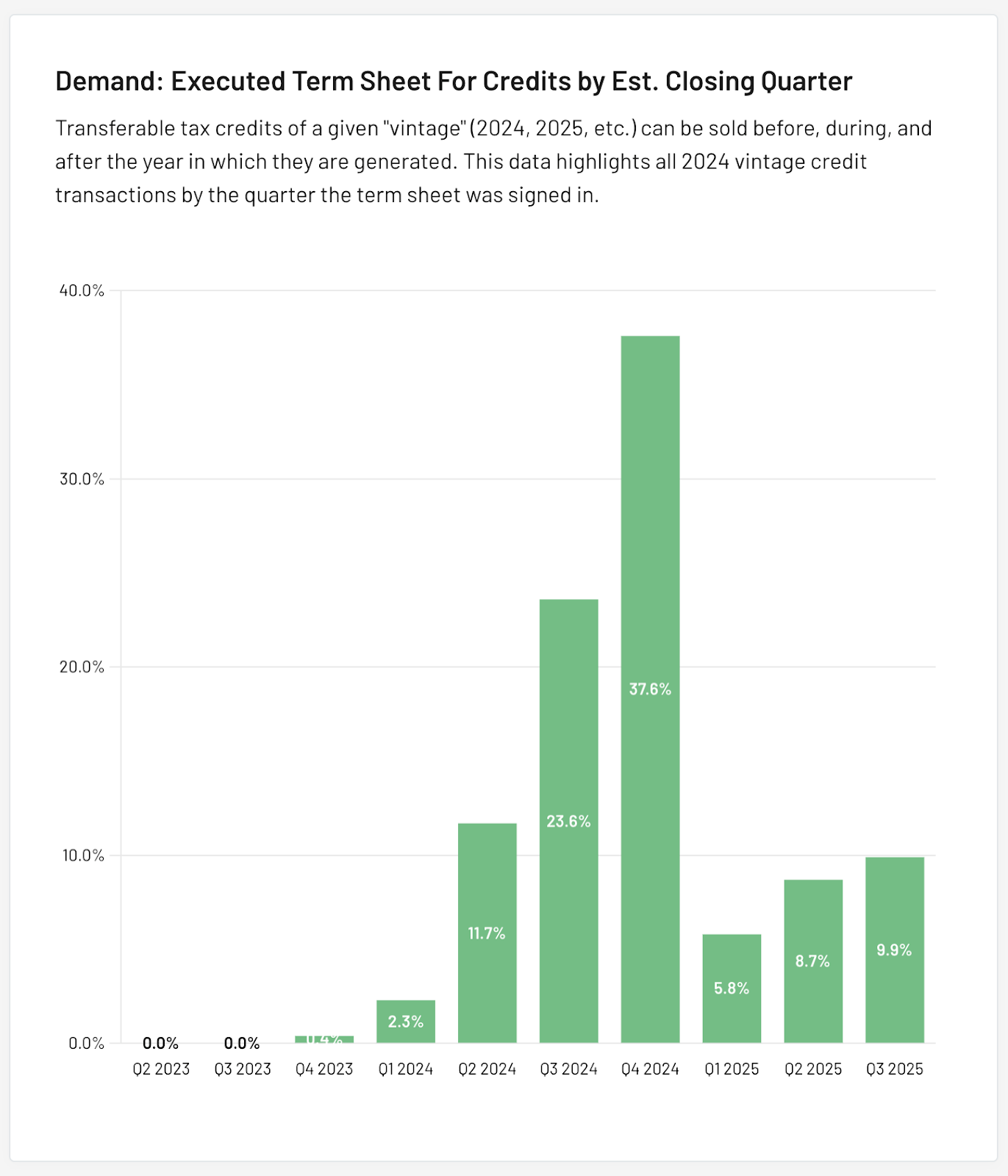

10% of 2024 tax credit transfers closed in Q3 2025

Nearly 10% of all transfers involving 2024 credits took place in Q3 2025 – concentrated heavily in September and the first half of October, just ahead of the extended filing deadlines for both partnerships and C-corporations, respectively. This is measured by notional deal volume.

For many buyers, these “before-the-buzzer” transactions were structured around a carryback strategy, allowing them to request a refund simultaneously with the filing of their 2024 return.

Other deals were driven by the desire to fully utilize remaining tax capacity under the 75% statutory credit offset cap.

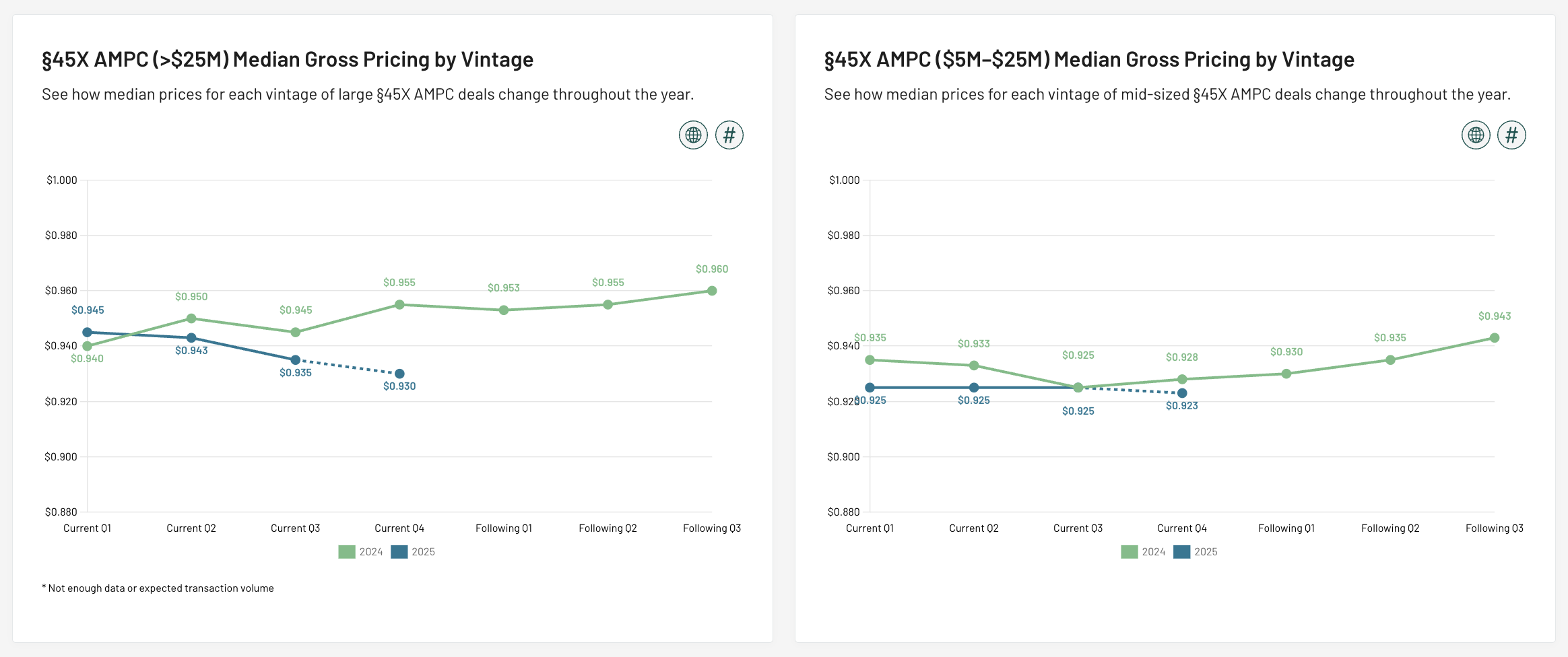

Regardless of the buyer’s underlying motivation, sellers generally benefited from premium pricing. Section 45X transactions for the 2024 vintage, for example, traded at the top of their range in Q3 2025 – "Following Q3" for the 2024 trend line – for both large and small deals.

PWA

Credits that are PWA exempt because of beginning of construction (BoC) dates are vanishingly rare

In the early days of the transfer market, buyers often sought tax credits that were exempt from prevailing wage and apprenticeship (PWA) requirements in an effort to avoid an incremental due diligence burden. Projects that either began construction before January 29, 2023 or have a capacity of less than 1 megawatt are generally exempt from PWA rules.

In 2023, nearly all available credits on Reunion’s platform fit that profile: by credit value, 95% of Section 48 ITCs and 100% of Section 45 PTCs were PWA-exempt due to BoC timing. Fast-forward to the 2026 credit vintage, and the landscape has essentially reversed.

Projects with a capacity under 1 MW, such as residential solar, remain exempt from PWA requirements, as do certain other credit types (e.g., 45X credits).

Only 1% of 2026 Section 48 ITCs and 29% of Section 45 PTCs remain PWA-exempt due to BoC timing.

The 29% exemption figure for 2026 Section 45 PTCs may give buyers an overly optimistic impression. Much of this volume is already committed through multi-year strips or tied up by existing buyers holding rights of first refusal. As a result, PWA-exempt PTCs that are broadly available may carry a pricing premium and clear the market quickly.

FEOC

FEOC is becoming a key purchase consideration, resulting in premium pricing for credits with low FEOC risk

In 2024, buyers specifically requested credits that were exempt from PWA requirements. We are starting to see a similar trend emerging with respect to Foreign Entity of Concern (FEOC); buyers are prioritizing “legacy” Section 48 ITCs and Section 45 PTCs that qualify as FEOC-exempt. We expect legacy credits to trade at a premium price compared to similar credits (e.g., 48E and 45Y) that require compliance with FEOC rules.

We expect demand for increasingly scarce "legacy,” FEOC-exempt Section 48 and Section 45 tax credits to drive pricing higher.

Credit adders

Adoption of bonus credit adders continues to expand for ITCs, but remains muted for PTCs

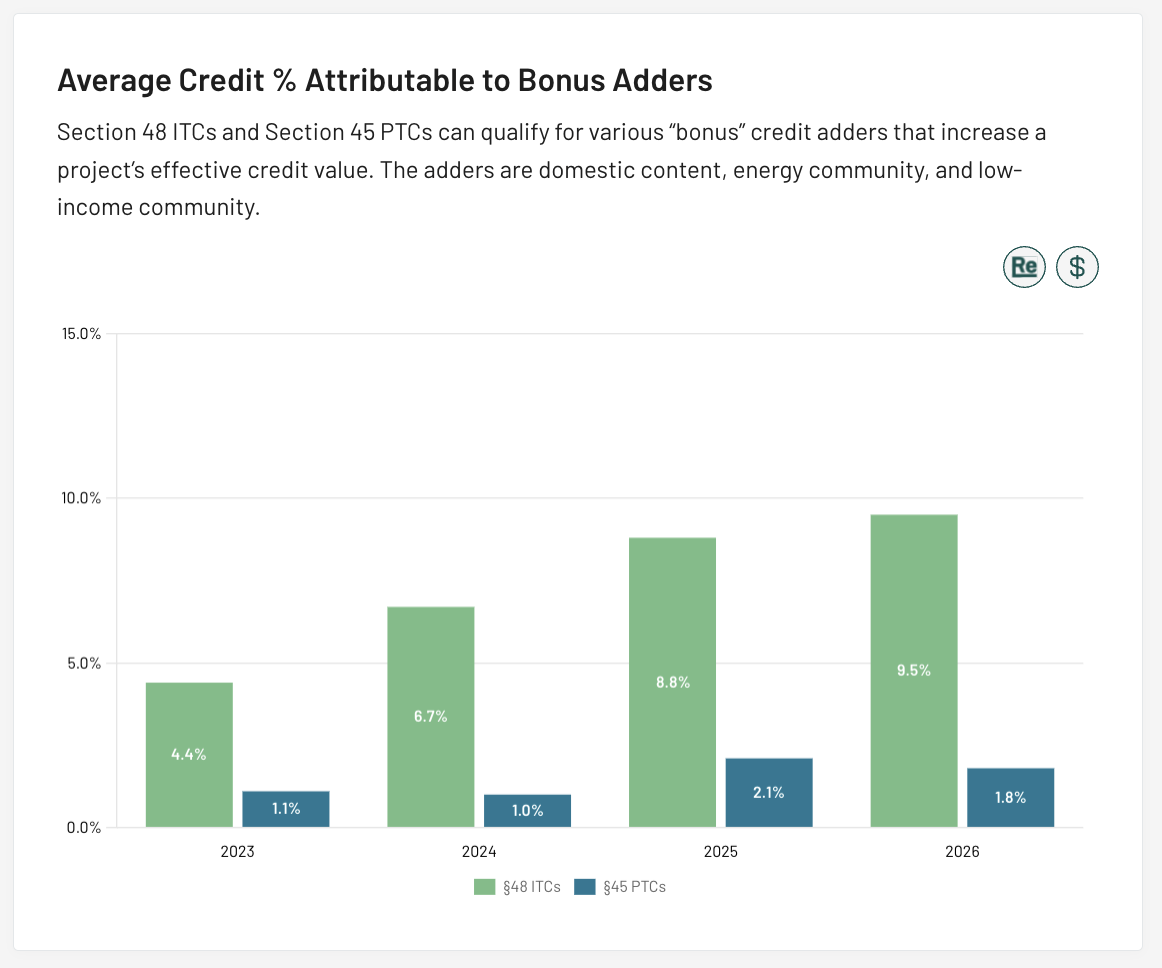

Section 48 ITCs and Section 45 PTCs can qualify for various “bonus” credit adders that increase a project’s effective credit value.

Since 2023, average ITC credit amount above the 30% baseline (assuming PWA compliance), have risen from 4.4% to 9.5%, indicating that most developers are now effectively incorporating at least one credit adder.

From a buyer’s perspective, Section 48-eligible projects without a bonus credit adder have become relatively scarce.

Section 45 PTCs, by contrast, show a different pattern. Average PTC rates above the base credit amount have remained relatively flat from 1.1% in 2023 to 1.8% in 2026. This stability is expected, however, because many Section 45 PTCs originate from projects that pre-date the Inflation Reduction Act’s introduction of bonus credit adders.

Access Reunion's Q3 Update to Market Monitor

Explore the latest pricing trends, transaction data, and market dynamics shaping the transferable tax credit market.

Alex Melehy

December 8, 2025

What Happens If You Fail PWA Compliance? Penalties, Recapture, and the Real Cost of Non-Compliance

Failing to meet PWA requirements under the IRA can cost developers up to 80% of their tax credit value, with cure penalties ranging from $5,000–$10,000 per worker for wage shortfalls to $50–$500 per hour for apprenticeship gaps.

For Sellers

Under the Inflation Reduction Act (IRA), PWA compliance isn't just a regulatory checkbox—it's the mechanism that lets you claim 5x your project's base tax credit amount. Most developers know this in theory, but few appreciate just how costly non-compliance actually is in practice. Below, we break down the penalties, recapture risks, and deal friction that come with falling short.

The 80% Cliff: Losing the 5x Multiplier

Projects that meet both prevailing wage and apprenticeship requirements qualify for a 5x credit multiplier. Miss either one, and you forfeit up to 80% of the credit you planned on. On a $100 million project claiming the §48 ITC, that's $24 million in lost credit value. And if the failure surfaces during the recapture period, the IRS can potentially claw that amount back from the tax credit buyer.

The IRS Correction and Penalty Framework

The good news: if a prevailing wage underpayment or apprenticeship gap comes to light, the IRS doesn't automatically knock your credit down to the base rate. You get a 180-day window after a final IRS determination to make corrections. The bad news: those cure provisions are steep.

- Prevailing Wage Shortfalls: You must pay affected workers the back-wages owed, plus interest at the federal short-term rate (per §6621) plus 6%, along with a $5,000 penalty to the IRS per worker for each year of underpayment. If the IRS finds the failure was due to "intentional disregard," the back-wage obligation triples and the penalty jumps to $10,000 per worker.

- Apprentice Labor Hours Gaps: Every hour short of the apprentice labor hours requirement costs $50—or $500 per hour if the IRS deems it intentional disregard. To put that in perspective: on a 100,000-hour project requiring 15% apprentice labor, a complete apprenticeship labor hour failure could mean $750,000 in penalties.

- Apprentice Participation Shortfalls: Any contractor or subcontractor with four or more laborers or mechanics on the project must employ at least one qualified apprentice. If they don't, the penalty is calculated by dividing that contractor's total labor hours by the number of laborers and mechanics they had on the project, then multiplying by $50 per hour ($500 for intentional disregard). This one is assessed at the contractor level—so a single large sub that never brings on an apprentice can rack up serious exposure even if the project-wide apprentice labor hour percentage looks fine.

Real-World Deal Friction: The Cost of Incomplete Reports

IRS penalties aside, poor PWA tracking creates real deal friction. In Reunion's transaction database, deals with a PWA diligence requirement close more than two weeks slower on average than those without one.

The usual culprit? Incomplete certified payroll reports. In one recent transaction Reunion facilitated, buyer's counsel spent weeks picking apart gaps in the PWA data, eventually pushing the compliance report to a post-closing obligation—resulting in lost leverage for the seller that could have been avoided entirely.

Why "We'll Figure It Out Later" Doesn't Work

A lot of developers assume they can piece together their records after construction wraps. In practice, retroactive compliance is far harder and far more expensive. Forensic reconstruction of wage data from messy records can run $150,000–$200,000 in accounting fees, compared to roughly $40,000 when tracked from the start (depending on project size and contractor count).

The takeaway: treat certified payroll data as a hard dependency, not a nice-to-have. A purpose-built PWA compliance provider can flag issues in real time, get ahead of back-pay or penalty exposure, and keep your 5x multiplier intact from day one.

Mahon Walsh

December 5, 2025

A guide to quick refunds for tax credit buyers

Form 4466 quick refunds help tax credit buyers recoup their investment months sooner

For Buyers

In brief

A quick refund under IRC §6425 allows a corporation that has overpaid its estimated income taxes – perhaps due to buying tax credits – to get cash back before filing its full tax return. By filing IRS Form 4466 shortly after year-end (and before the regular return due date), eligible corporations can recover overpayments – so long as the excess exceeds both $500 and 10% of expected tax liability. For tax credit buyers in particular, quick refunds are a powerful cashflow tool, accelerating the economic benefit of credits by months compared to the standard refund process.

Quick refunds allow corporations to recover overpaid estimated taxes early

Under IRC §6425, a “quick refund” allows a corporation that has overpaid its estimated federal income tax to request an “adjustment” of its estimated income tax prior to filing its full annual return.

Corporations may request a quick refund by filing IRS Form 4466 (see the full Instructions for Form 4466).

Quick refunds have become a common mechanism for corporations purchasing tax credits to more quickly realize the benefit of their investment in the event that they overpaid their estimated tax.

Quick refunds accelerate cash recovery from tax credit purchases

If a corporation has overpaid estimated tax due to a tax credit transaction in their current tax year, the quick refund returns the overpayment much faster than the conventional refund process. This allows the corporation to more quickly realize the benefit of their investment.

Benefits are particularly pronounced for corporations who purchase credits in the months immediately preceding or following the close of their tax year. As a quick refund can only be requested after the end of a given tax year (see §6425(a)(1)), corporations purchasing tax credits in the months surrounding the end of their tax year may more quickly request and receive a quick refund.

A quick refund, however, yields benefits for any corporation that has overpaid their estimated tax, regardless of the timing of their tax credit purchase.

Eligibility depends on the size of the estimated tax overpayment

Corporations that have overpaid their estimated income tax in the current tax year are eligible for a quick refund under Form 4466. Take a company that has an estimated 2025 tax liability of $100M, which it pays in quarterly estimated tax payments of $25M each. Let’s assume that the company purchases $40M of tax credits, reducing their estimated tax liability to $60M.

- After their Q3 estimated payment date, they will have paid $75M in estimated taxes, which is an overpayment of $15M

- After their Q4 estimated payment date, they will have paid $100M in estimated taxes, which is an overpayment of $40M

If the corporation is in an overpayment position, they can file for a quick refund using Form 4466. To qualify, the overpayment must be:

- Greater than 10% of expected tax liability for the year AND

- Greater than $500

Form 4466 must be filed shortly after year-end

Corporations must apply for a quick refund after the end of their tax year (e.g., December 31 for calendar-year tax filers) but before the 15th day of the fourth month thereafter and their income tax return filing (Form 1120) for that year. Thus, a calendar-year filer would submit Form 4466 between January 1st and April 15th.

Form 4466 instructions state, “An extension of time to file the corporation’s tax return will not extend the time for filing Form 4466”, so corporations must file Form 4466 before their non-extended tax filing deadline, even if they extend. In other words, a corporation with a December year-end that extends their tax return filing date must still submit Form 4466 before April 15th. Practically speaking, corporations should file a quick refund request as soon as possible after their tax year-end to maximize cashflow benefit.

The corporation must also file a copy of the previously filed Form 4466 with its income tax return.

Refunds are typically issued within 45 days

The IRS is required to process a Form 4466 request within 45 days. The IRS may review elements of the filing, so corporations should be prepared to provide any requested information promptly to avoid delays in receiving the refund.

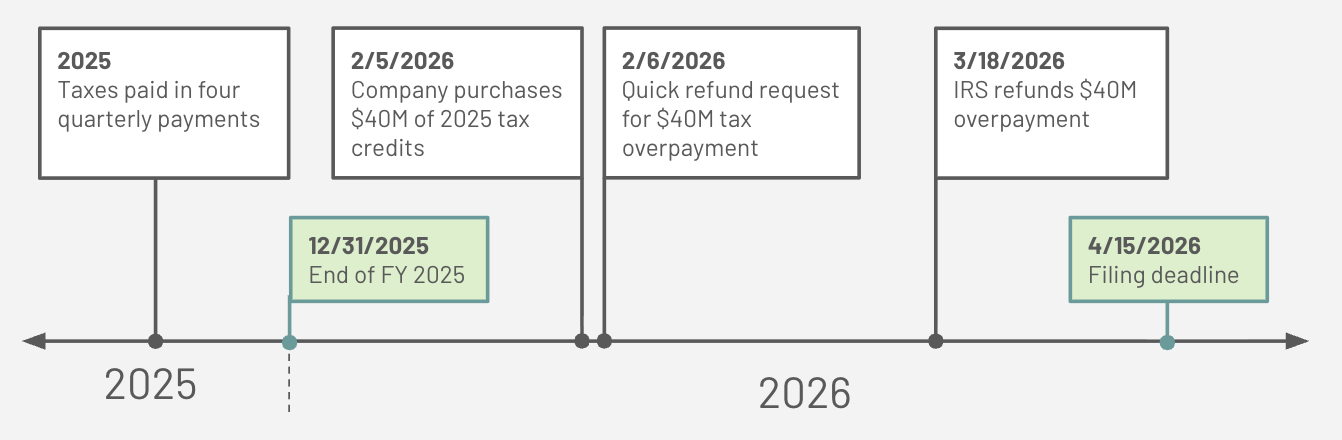

Here is a sample quick refund timeline for a calendar-year filer with a filing deadline of 4/15/26:

- The company has a 2025 estimated tax liability of $100M, which it already paid in four quarterly payments of $25M

- The corporation purchases $40M of Section 48 ITCs on 2/5/2026 for $36M. The corporation has now overpaid their 2024 taxes by $40M.

- The corporation submits Form 4466 on 2/6/2026, requesting a quick refund of their $40M overpayment

- The corporation receives $40M from the IRS on 3/18/2026, realizing their cash savings of $4M

Reunion Accelerates Investment Into Clean Energy

Reunion’s team has been at the forefront of clean energy financing for the last twenty years. We help CFOs and corporate tax teams purchase clean energy tax credits through a detailed and comprehensive transaction process.