Footnote of the Week: Among Insured Tax Credit Deals, Many Have Coverage Levels of 110% or Higher

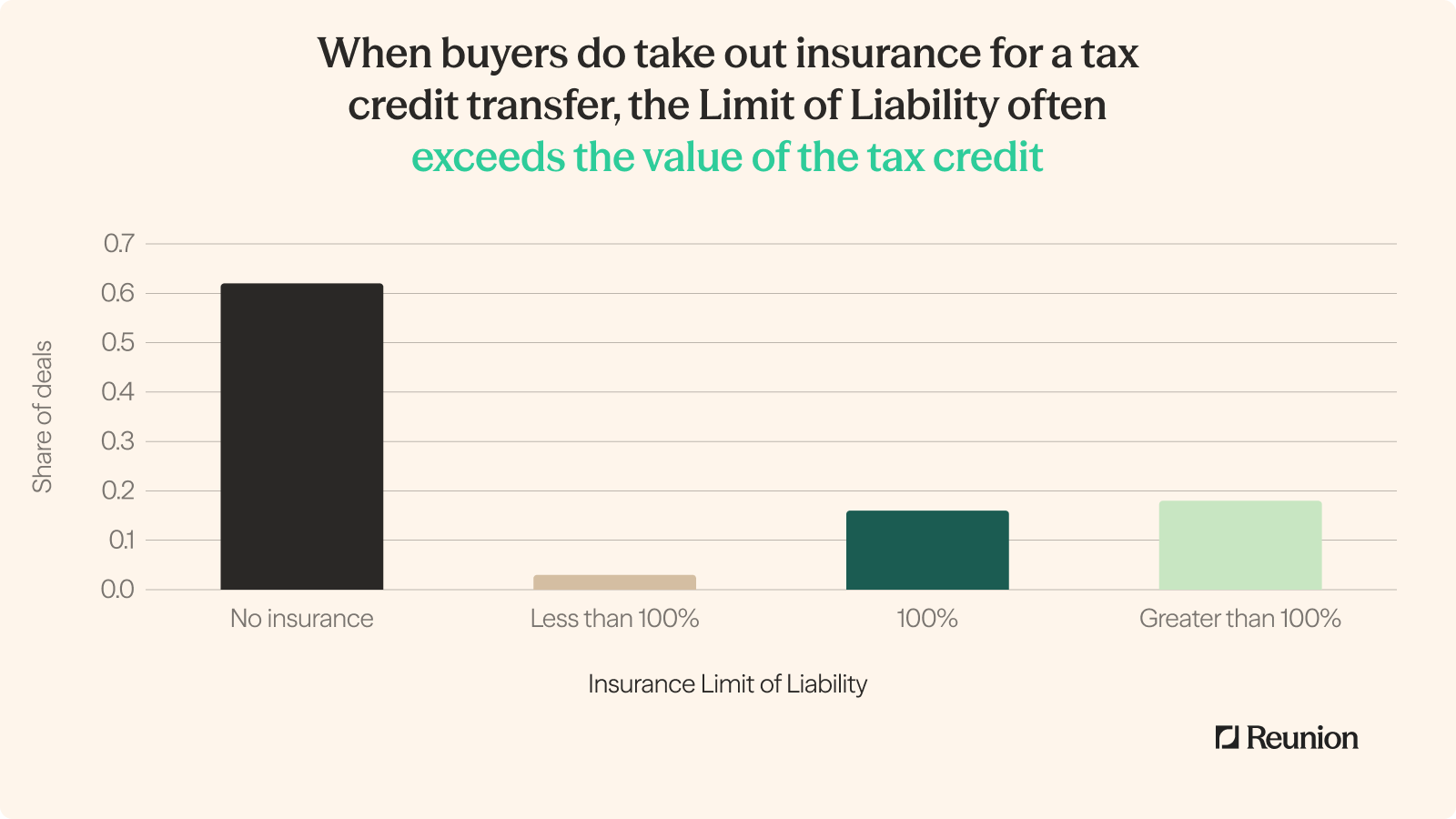

For transactions that include insurance, our data reveals that the Limit of Liability often exceeds the face value of the tax credit.

In discussions of energy tax credit transfers, much of the focus goes to headline numbers like pricing, deal sizes, and types of credits. A less discussed element that can make or break a deal is tax credit insurance. The demand for tax credit insurance, which is designed to protect the value of tax credits in the event of an IRS challenge, has grown significantly since the start of transferability.

Since Reunion began facilitating tax credit transfers in 2023, about 40 percent of our transactions have included tax credit insurance coverage. As shown in the colored bars below, most of this insurance coverage has had a Limit of Liability equal to or greater than 100%. Conversely, the black bar represents the roughly 60 percent of deals that did not include insurance, suggesting cases in which the tax credit seller could provide a sufficiently strong indemnification, or the parties were comfortable with the risk-reward of the credits being transferred.

The pattern of Limits of Liability commonly exceeding 100% is noteworthy, and implies that many tax credit buyers want protection from second-order risks such as penalties and legal fees that could arise from a disallowance or recapture. To gauge the upper range of these Limits of Liability, we dug into the tax credit type that we’ve seen insured most frequently: §48 investment tax credits.

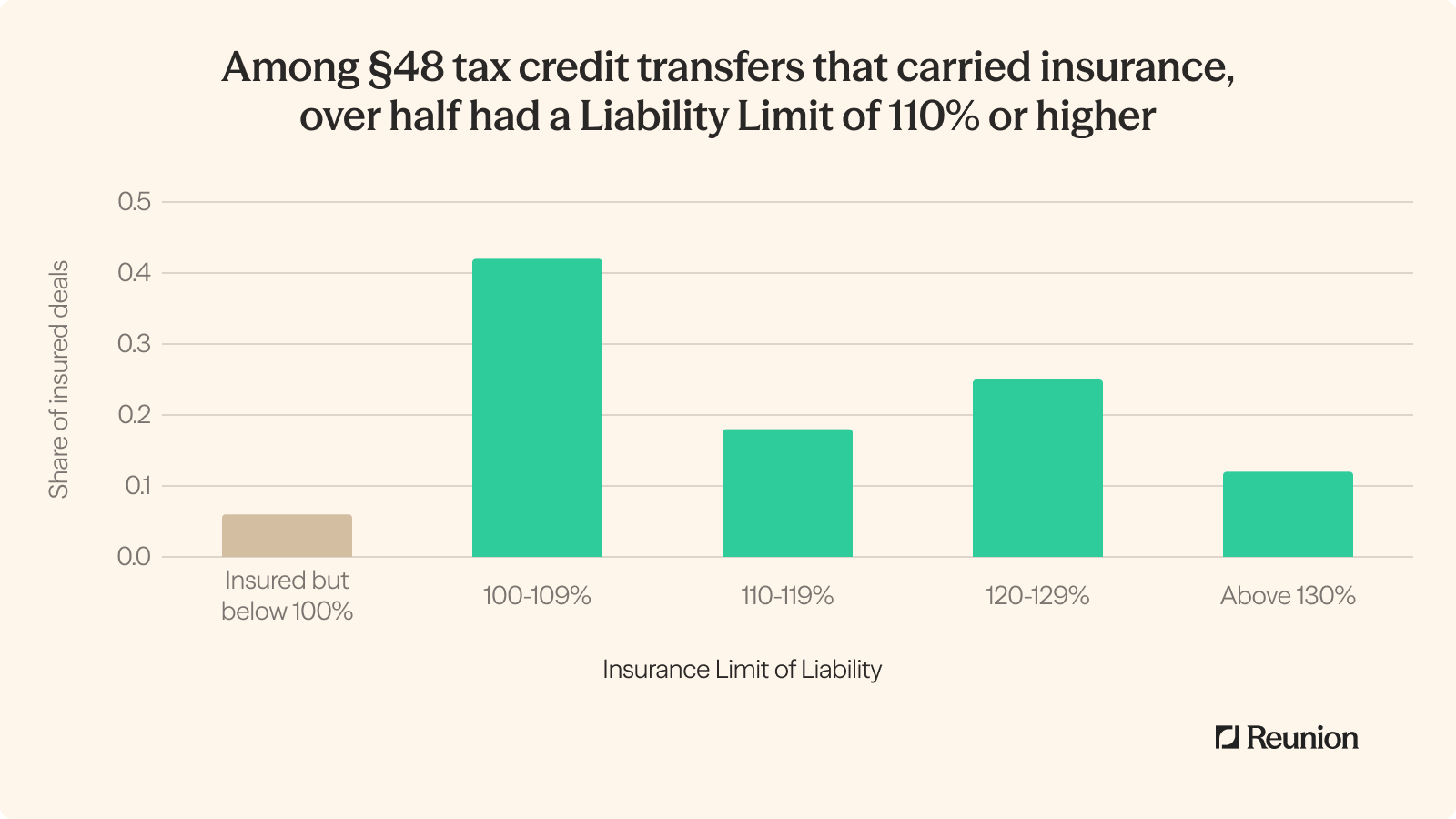

For §48 transfers, the Limits of Liability have pushed markedly higher than face value – with a little over half of insured deals hitting 110% or higher, and multiple deals establishing Limits of Liability greater than 130%. (The small share of deals with a liability limit below 100% are primarily distributed or residential energy assets; this coverage is designed to support a partial loss, rather than a less likely portfolio-wide loss event.)

While tax credit insurance isn’t warranted on every deal, it plays an important role in enabling tax credit transfers among risk-sensitive buyers, especially when the seller is not investment grade. Our analysis suggests that relatively high Limits of Liability are supported by the market, and may give buyers access to a wider range of tax credit opportunities.