How an investment grade seller unlocked the IG premium for ITCs

Case Study

§48 ITC

Q1 2025

Reunion guided a Fortune 500 energy company's first tax credit sale to close in 45 days at the premium end of the ITC market.

Overview

A Fortune 500 energy company with an investment grade (IG) credit rating came to Reunion with $45M in §48 ITCs and a clear goal: maximize cash proceeds without a drawn-out process.

Reunion had market intelligence which suggested that an investment grade seller could command a premium in the market if matched with the right buyer — and we ran a process that delivered.

$0.95

Gross price

3 Days

To agree on key terms

Reunion Market Monitor

See the real-time tax credit transfer pricing, terms, and market intelligence that helped this seller close.

Market intelligence

A first-time seller with a clear goal

The deal

§48 ITC

2025

$40–50M

§48 Investment tax credits

Utility-scale battery storage

Deal structure

An investment-grade §48 ITC transfer structured around a single high-capacity counterparty.

The seller

- Fortune 500 energy company

- Over $100B in annual revenue

- Publicly traded

- Investment grade credit rating

- First tax credit transfer

The seller’s objectives

- Maximize cash proceeds

- Close with a single counterparty who could take $40M+ of tax credits

- Minimize execution timeline and risk

Sourcing the ideal buyer from a vetted pool

How Reunion's market intelligence identified the right match at a premium price from a pool of 50+ vetted buyers.

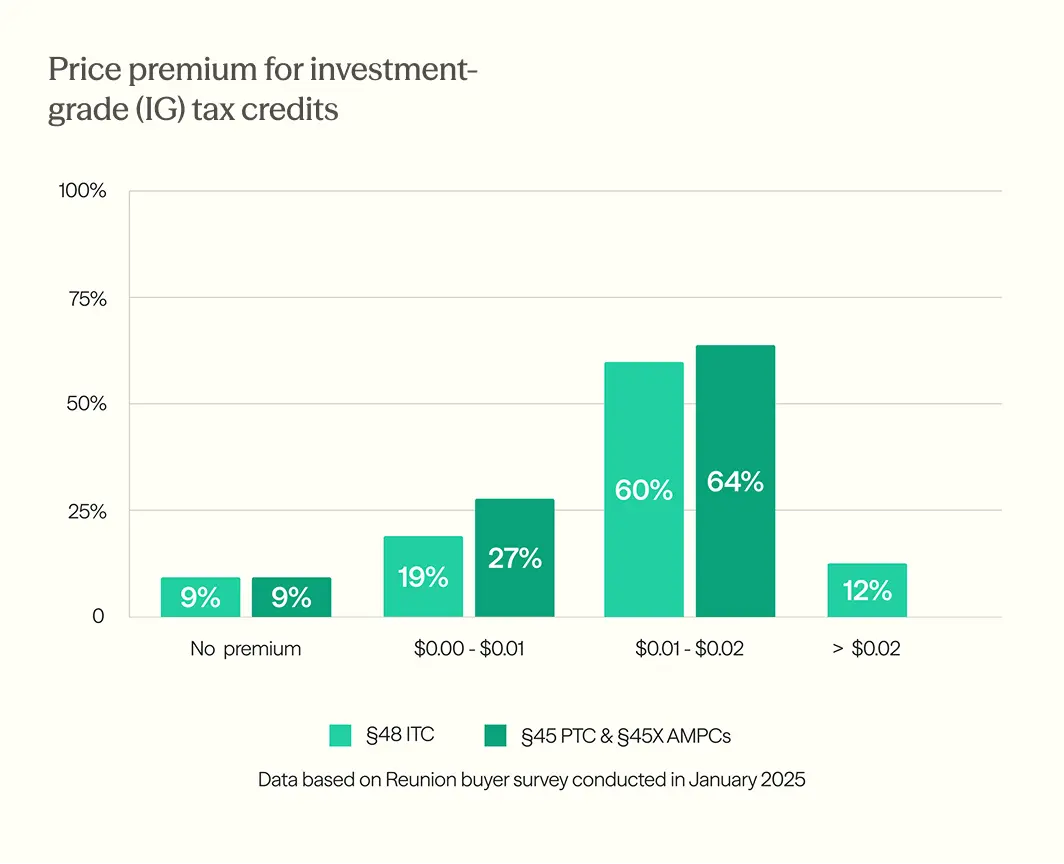

Reunion Market Monitor revealed key insights about IG tax credits and pricing:

- ~20% of dollarized demand across Reunion's vetted buyer pool requires an IG counterparty

- Nearly 60% of transaction-ready buyers are willing to pay $0.02+ premium for IG tax credits, regardless of credit type, technology, or volume

As such, Reunion ran a buyer discovery process based on:

- Investment grade focus: Buyers who specifically required an investment grade seller

- Fiscal-year filers: Buyers with a March fiscal-year close, often overlooked by other sellers because they were “out of market” relative to the calendar-year cycle

The result

A 130-year-old American company ($2B+ annual revenue, fiscal-year filer) was identified as the ideal counterparty and met the seller’s $0.95 ask.

See the real-time tax credit transfer data that helped source the right buyer.

Orchestrating a 45-day transaction close

How Reunion aligned terms early and prepared the parties to move fast.

Aligned early on critical terms

Pricing

Positioned $0.95 as a market-clearing price upfront to buyers to avoid a protracted bidding process

Tax credit insurance

Identified a buyer willing to forego insurance per the seller’s desire, accepting the IG parent company's indemnification instead

Volume contingency

Agreed upfront on a deal structure that included pricing tiers outside the $40M–$50M target range, so the cost segregation report wouldn't trigger renegotiation

Ensured buyer transaction-readiness

- Ran a tax credit workshop with internal stakeholders

- Confirmed CFO had agreed to terms and delegated signing authority to VP of Tax

- Confirmed Treasury had $60M cash on standby

- Verified advisors were lined up: primary and backup law firms identified, two Big 4 firms engaged for diligence

3 Days

To align on key commercial terms

7 Days

From term sheet to diligence memo

45 Days

From term sheet to close