Reunion’s Q3 2025 Transferable Tax Credit Pricing and Markets Update

Reunion’s Q3 Market Monitor print highlights moderate tax credit pricing declines, but continued market maturation

Reunion recently released our Q3 Market Monitor update, including forward-looking pricing estimates through Q4 of this year.

Overall, our data highlights two seemingly divergent trends: (1) softened demand for 2025 tax credits alongside (2) increased market maturity and liquidity.

To better understand this dynamic, this note examines six key trends from our data:

- Pricing: 2025 tax credit prices have declined compared to 2024 levels, primarily due to the OBBBA

- Market dynamics: Sections 45U and 45Z are becoming increasingly popular production credits

- Transaction timing: 10% of 2024 tax credit transfers closed in Q3 2025

- Prevailing wage and apprenticeship (“PWA”): Credits that are PWA exempt because of beginning of construction (“BoC”) exemption are vanishingly rare

- FEOC: FEOC will become a key purchase consideration, with upward pricing for credits with low FEOC risk

- Credit adders: Adoption of bonus credit adders continues to expand for ITCs, but remains muted for PTCs

Pricing

2025 tax credit prices have declined compared to 2024 levels

Across virtually all credit types and deal sizes, 2025 pricing declined relative to 2024 levels. This trend has been particularly pronounced in Q3 and Q4. In 2024, prices rose from Q3 to Q4 as buyers competed for increasingly limited supply. In 2025, the trend reversed, with pricing generally softening over the same period.

Investment-grade (“IG”) supply continues to command a premium – ITCs from IG sellers, for example, continued to trade one to three cents above these median levels in late 2025.

*Section 48 ITC pricing is exclusive of residential solar and biogas. Reunion maintains separate pricing series for these technologies.

The following chart compares estimated Q4 2025 to actual Q4 2024 data. This year’s Q4 data is based on deals closed through November and terms sheets executed through the publication date of this note.

*Section 48 ITC pricing is exclusive of residential solar and biogas. Reunion maintains separate pricing series for these technologies.

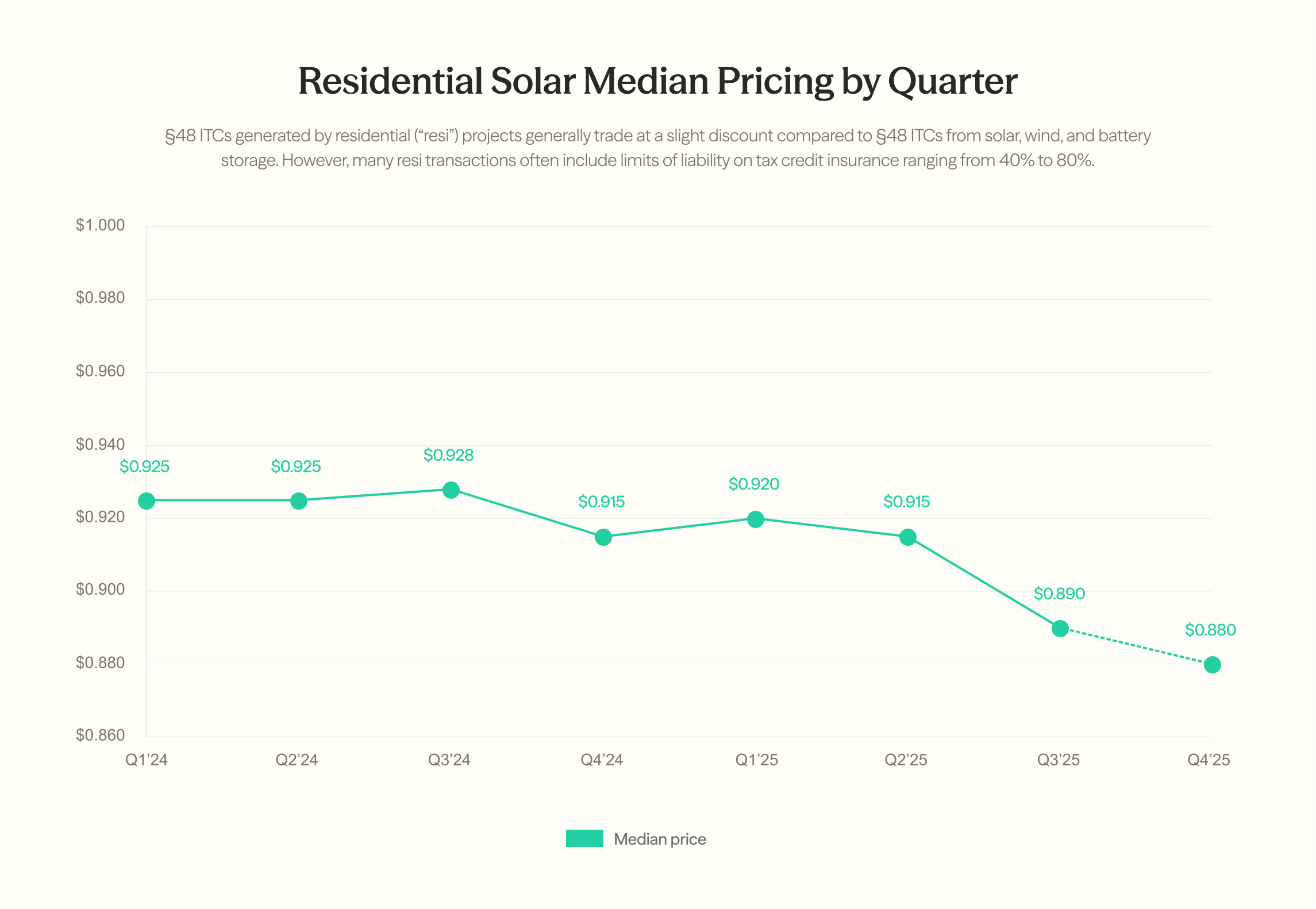

Residential, or “resi,” solar experienced marked price declines throughout 2025 as well. (Reunion maintains separate pricing series for ITCs from resi solar and biogas. We do not include resi and biogas deals in our market-wide Section 48 ITC pricing above.) Looking across 2024 and 2025 vintages, median prices fell from $0.928 in Q3 2024 to an estimated $0.88 in Q4 2025.

When understanding resi prices, it's important to recall that buyers and sellers often negotiate the limit of liability ("LOL") on resi tax credit insurance policies, which flows through to headline pricing. A major resi solar developer, for example, offered a further discount of two cents for an LOL of 40% versus 100%.

While “headline” declines in prices have been modest on a percentage basis, the flow through to cash tax savings has been significant

A corporate taxpayer who purchased a $50M tranche of Section 48 ITCs Q3 2024 and am equivalent $50M tranche of Section 48 ITCs in Q3 2025 would have benefited from an additional $500,000 in cash tax savings – a 14.3% increase.

Tax credit pricing declines in 2025 have largely been driven by impacts of the OBBBA

In the months leading up to the Bill’s passage on July 4, the tax credit market slowed as buyers hesitated to make meaningful commitments without clarity on the final legislation. Many feared that 2025 tax credits might be retroactively repealed and chose to wait for assurance that existing credits would be respected before proceeding with transactions.

The Bill provided clarity that both current- and future-year tax credits will be respected, but the OBBBA itself had a significant downward impact on corporate tax liabilities. Dozens of corporations that were expecting $50M or $100M+ in tax liability no longer had the appetite to purchase 2025 credits.

Today, many companies are still working to understand how OBBBA will affect their final 2025 tax liability – and have delayed purchasing credits as a result.

We expect lingering OBBBA-related impacts on 2026 tax liabilities. As of the publication of this note, Reunion is conducting our year-end tax credit buyer survey, and early feedback suggests that corporations are anticipating reduced 2026 tax liabilities of 10% to 30% against an assumed “non-OBBBA” baseline. Varying degrees of impact tend to cluster in sectors that are particularly sensitive to tax law changes. We’ll publish our year-end buyer report in early 2026.

Although 2026 aggregate demand may be down compared to this non-OBBBA baseline, we are seeing a significant number of taxpayers moving early on 2026 credits. These taxpayers generally fall into two camps:

- Strategic: Companies proactively seeking investments over $50M

- Opportunistic: Companies seeking investments with outsized discounts

We will incorporate pricing for 2026 tax credits in our Q1 2026 Market Monitor release.

Market dynamics

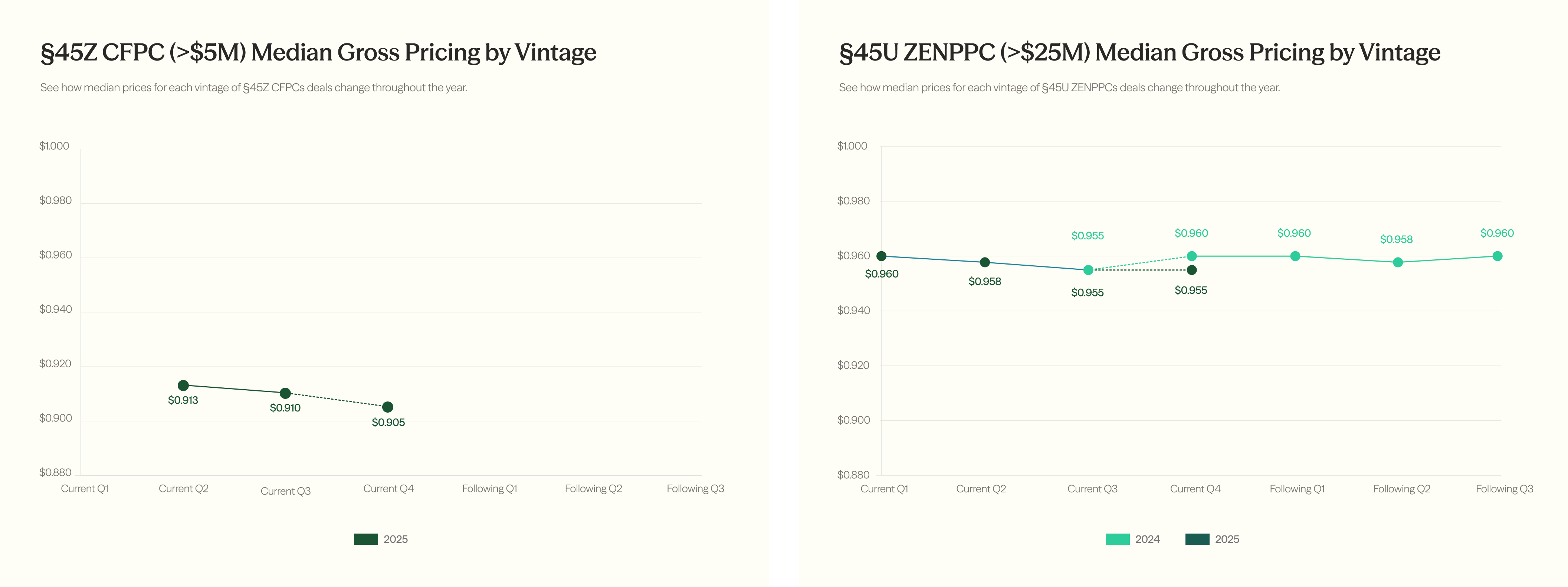

Section 45U nuclear and Section 45Z clean fuels are becoming increasingly popular production credits

In the second half of 2024, a handful of Reunion’s corporate clients explicitly prioritized Section 45U zero-emission nuclear power production credits (“ZENPPCs”). However, the majority of production credit-focused buyers focused on Section 45 PTCs.

As we approach the end of 2025, we have observed that many production credit-focused companies now view 45U ZENPPCs and 45 PTCs with roughly equivalent interest. From a pricing perspective, 45U nuclear credits are among the most stable.

A similar pattern is emerging around Section 45Z clean fuel production credits (“CFPCs”). An increasing number of corporate buyers are actively targeting 45Z credits due to two key factors:

- Risk/return: Section 45Z clean fuel credits are trading in the high $0.80s to low $0.90s, depending largely on the purchase size, presence of tax credit insurance, and the seller’s financial strength. Although this pricing generally aligns with Section 48 ITCs, Section 45Z CFPCs are not subject to recapture.

- General business credit (“GBC”) ordering: Tax credit carrybacks have become more popular, and an effective carryback strategy must account for the credit-ordering rules reflected in IRS Form 3800. Compared to Section 48 ITCs, Section 45Z CFPCs are more advantageous for a carryback from a credit ordering perspective.

To reflect this growing interest, we are now publishing pricing series for both 45U and 45Z credits. Our 45U pricing goes back to 2024, while 45Z begins in 2025 (when the credit first became available).

Although demand for 45Z credits is growing, prices have moderated slightly throughout 2025. We believe this reflects supply dynamics: since the 45Z credit only became available this year, a preponderance of sellers entered the market in the latter half of this year, generally offering full-year tranches of 2025 credits.

Looking ahead to 2026, we expect, and have already begun to see, 45Z deals structured around quarterly payments, akin to many Section 45 PTC transactions. Strips should become increasingly common, too.

The Treasury and the IRS have not yet issued final guidance for either of these credits, though this has not been a gating factor for most buyers. 45Z, in fact, is among the credits that received favorable treatment under the OBBBA.

10% of 2024 tax credit transfers closed in Q3 2025

Nearly 10% of all transfers involving 2024 credits took place in Q3 2025 – concentrated heavily in September and the first half of October, just ahead of the extended filing deadlines for both partnerships and C-corporations, respectively. This is measured by notional deal volume.

For many buyers, these “before-the-buzzer” transactions were structured around a carryback strategy, allowing them to request a refund simultaneously with the filing of their 2024 return.

Other deals were driven by the desire to fully utilize remaining tax capacity under the 75% statutory credit offset cap.

Regardless of the buyer’s underlying motivation, sellers generally benefited from premium pricing. Section 45X transactions for the 2024 vintage, for example, traded at the top of their range in Q3 2025 – "Following Q3" for the 2024 trend line – for both large and small deals.

PWA

Credits that are PWA exempt because of beginning of construction (BoC) dates are vanishingly rare

In the early days of the transfer market, buyers often sought tax credits that were exempt from prevailing wage and apprenticeship (PWA) requirements in an effort to avoid an incremental due diligence burden. Projects that either began construction before January 29, 2023 or have a capacity of less than 1 megawatt are generally exempt from PWA rules.

In 2023, nearly all available credits on Reunion’s platform fit that profile: by credit value, 95% of Section 48 ITCs and 100% of Section 45 PTCs were PWA-exempt due to BoC timing. Fast-forward to the 2026 credit vintage, and the landscape has essentially reversed.

Projects with a capacity under 1 MW, such as residential solar, remain exempt from PWA requirements, as do certain other credit types (e.g., 45X credits).

Only 1% of 2026 Section 48 ITCs and 29% of Section 45 PTCs remain PWA-exempt due to BoC timing.

.png)

The 29% exemption figure for 2026 Section 45 PTCs may give buyers an overly optimistic impression. Much of this volume is already committed through multi-year strips or tied up by existing buyers holding rights of first refusal. As a result, PWA-exempt PTCs that are broadly available may carry a pricing premium and clear the market quickly.

FEOC

FEOC is becoming a key purchase consideration, resulting in premium pricing for credits with low FEOC risk

In 2024, buyers specifically requested credits that were exempt from PWA requirements. We are starting to see a similar trend emerging with respect to Foreign Entity of Concern (FEOC); buyers are prioritizing “legacy” Section 48 ITCs and Section 45 PTCs that qualify as FEOC-exempt. We expect legacy credits to trade at a premium price compared to similar credits (e.g., 48E and 45Y) that require compliance with FEOC rules.

We expect demand for increasingly scarce "legacy,” FEOC-exempt Section 48 and Section 45 tax credits to drive pricing higher.

Credit adders

Adoption of bonus credit adders continues to expand for ITCs, but remains muted for PTCs

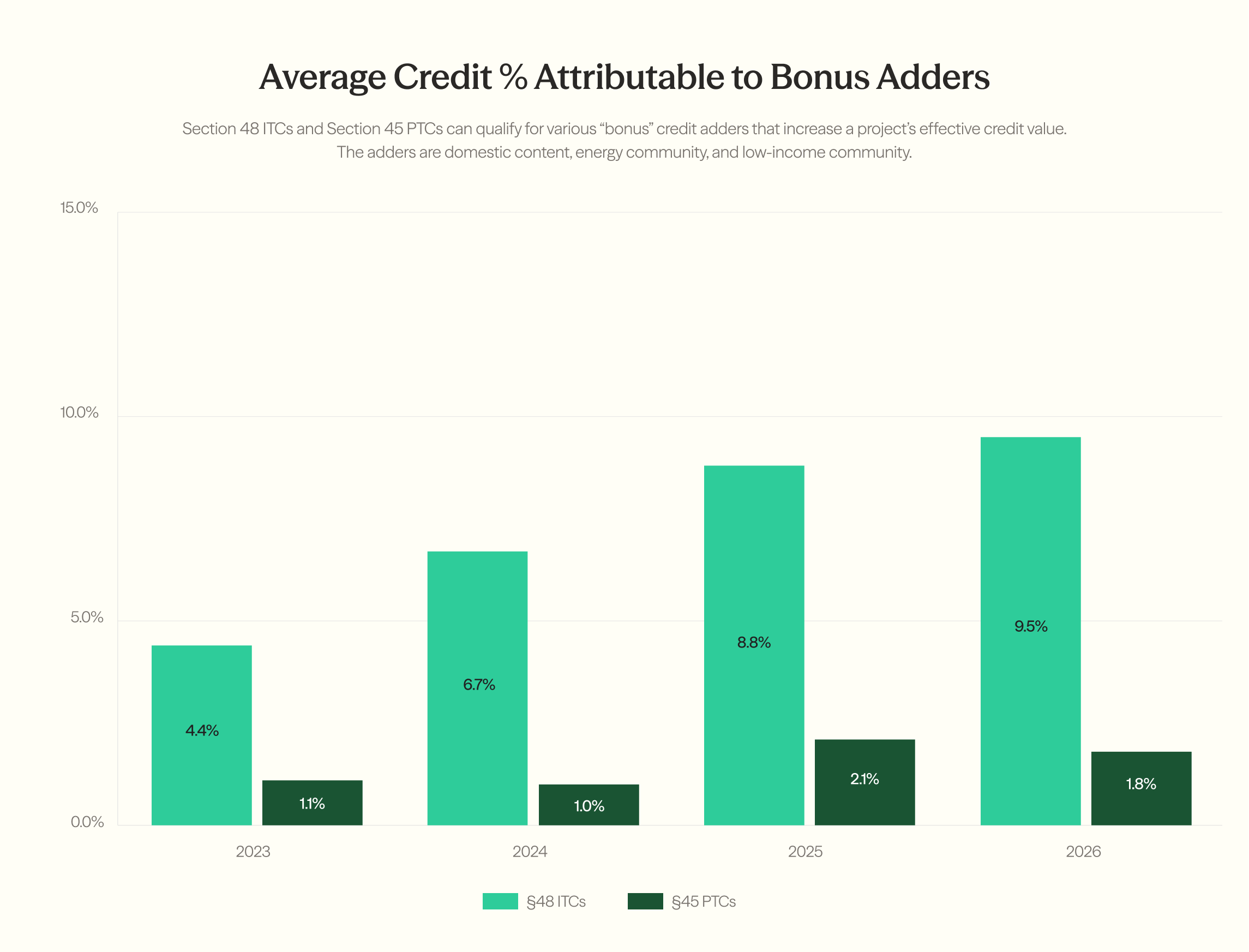

Section 48 ITCs and Section 45 PTCs can qualify for various “bonus” credit adders that increase a project’s effective credit value.

Since 2023, average ITC credit amount above the 30% baseline (assuming PWA compliance), have risen from 4.4% to 9.5%, indicating that most developers are now effectively incorporating at least one credit adder.

From a buyer’s perspective, Section 48-eligible projects without a bonus credit adder have become relatively scarce.

Section 45 PTCs, by contrast, show a different pattern. Average PTC rates above the base credit amount have remained relatively flat from 1.1% in 2023 to 1.8% in 2026. This stability is expected, however, because many Section 45 PTCs originate from projects that pre-date the Inflation Reduction Act’s introduction of bonus credit adders.

Access Reunion's Q3 Update to Market Monitor

Explore the latest pricing trends, transaction data, and market dynamics shaping the transferable tax credit market.