Understanding transferable tax credit carrybacks and carryforwards

Transferable tax credits have created new opportunities for taxpayers to participate in the clean energy transition while offsetting tax liability. Understanding the mechanics of carrybacks and carryforwards is essential to capturing their full benefit.

Key takeaways

Carrybacks create a four-year tax liability window

The ability to carry a clean energy tax credit back 3 years and carry forward 22 years is the core mechanism. For a corporate buyer, this potentially aggregates four years of tax liability (the current year plus the three carryback years), making a carryback a great fit for any tax payers with a trailing federal tax liability. Some examples of strong profiles for a carryback strategy include tax payers with a large, one-time event in a recent tax year or relatively smaller taxpayers looking to aggregate up to four years of liability to make a larger tax credit purchase. The carryback must first be applied to the current tax year, and then carried back to the earliest possible year first, with each year thereafter sequentially. Each tax year is subject to the §38(c)(1) limitation: credits can offset 100% of the first $25,000 of net regular tax, plus 75% of the amount above $25,000. For C corporations in tax years beginning after December 31, 2022, the tentative minimum tax is treated as zero under §38(c)(6)(E), so this formula is the binding ceiling.

Cash flow is the primary strategic concern

One potential challenge of a carryback is the mismatch between the date the buyer pays for the credit and the date it receives the refund from the IRS. Since a carryback claim is effectively filed simultaneously with the current year's tax return (which may be several months after year-end for corporates), there may be a notable lag. To alleviate this burden, tax credit buyers frequently negotiate delayed / split payment structures (or possibly lower upfront purchase prices) with tax credit sellers to improve the overall return on investment

IRS refund timing is variable (but pays interest)

Once the carryback claim is filed, the refund processing time is variable. The IRS publishes processing statuses online which suggest an approx. 90 day timeline to process carryback claims. Of note, the IRS will pay interest on carryback refund claims outstanding longer than 45 days. Subject to a given taxpayer’s internal cost of capital, some buyers have found interest payments to be accretive to the overall transaction ROI. Carryback refund claims under $5 million are not subject to Joint Committee on Taxation (JCT) review, which may also lead to faster processing.

Credit ordering rules in IRS Form 3800 are key

Taxpayers who have other general business credits (e.g., low-income housing, work opportunity, etc.) should be mindful of the instructions established in the Form 3800 General Business Credit (”GBC”) ordering rules. These rules dictate the order by which certain GBCs (including energy tax credits) must be applied against the current year's tax liability, which can have downstream impacts on carryback or carryforward mechanics

Introduction

The Treasury’s final transferability regulations allow corporations to carry transferable tax credits back up to three years, with the ability to offset up to 75% of prior-year tax liabilities. Companies may also carry credits forward up to 22 years.

Although carrybacks and carryforwards have been available for clean energy tax credits since the introduction of transferability under the Inflation Reduction Act (IRA), it's been only in the past six months that Reunion has seen a meaningful increase in companies exploring and modeling these strategies – with a particular interest in carrybacks.

In our view, this emerging interest in carrybacks reflects market maturity, as both experienced and first-time buyers seek to maximize the value and flexibility of their tax credit investments. By leveraging carrybacks, purchasers can expand the total credit volume under consideration, unlocking more favorable deal terms and better overall returns.

How does a tax credit carryback work?

Tax credit buyers can carry credits back three years, and then apply credits forward to subsequent years. A company who purchases 2025 tax credits for a carryback, for instance, would first have to max out their 2025 capacity and then apply any unused amount to 2022, then 2023, and then to 2024. For each year, the company would apply credits up to the §38(c)(1) ceiling — 100% of the first $25,000 of net regular tax liability, plus 75% of the remainder — before moving to the next year.

It’s worth reiterating that a company may only carry back credits after they have exhausted their ability to apply those credits to the tax year of the credits. In other words, a company may only carry back 2025 credits once they have hit the 75% statutory cap for 2025.

Taxpayers may also carry applicable IRA tax credits forward up to 22 years.

Assume a taxpayer purchases $75 million of 2025 tax credits and is expected to have a gross tax liability of $100 million from 2022 through 2028. The tax credit deduction would follow the below structure:

What happens if a carryback year has no tax liability?

If an NOL reduced a prior year's taxable income to zero, the §38(c) limitation for that year is also zero. No credit can be absorbed there. Because buyers cannot elect to skip a loss year under §39(a)(2)(A), the unused credit cascades to the next year in the carryback window. Any amount that cannot be absorbed within the three-year window moves into the 22-year carryforward period.

A further wrinkle applies when both an NOL carryback and a credit carryback target the same year. The NOL reduces taxable income first, which lowers net regular tax liability, which in turn compresses the §38(c) capacity available for the credit. Each carryback year needs to be modeled sequentially and with full visibility into prior-year loss positions.

What types of companies should consider a carryback?

A carryback generally makes sense for companies who have a significant tax liability across one or more of their three prior tax years. A common use case is a sizable tax event, like a strategic divestiture, within the three-year carryback window.

This holds true for public and private companies, both of whom Reunion has supported in carryback transactions.

When and how do you apply for a carryback refund request?

If a company is requesting a carryback refund via IRS Form 1139, Corporate Application for Tentative Refund, the tax team would typically submit Form 1139 at the same time as, but not in the same package with, their income tax return for the year of the credits they purchased for a carryback.

From Instructions for Form 1139:

- “When to File: Generally, the corporation must file Form 1139 within 12 months of the end of the tax year in which an NOL, net capital loss, unused credit, or claim of right adjustment arose. The corporation must file its income tax return for the tax year no later than the date it files Form 1139.

- Where to File: File Form 1139 with the Internal Revenue Service Center where the corporation files its income tax return. Do not file Form 1139 with the corporation's income tax return.”

Because a company effectively files their refund request at the same time as their income tax return, they will have a concrete understanding of how many credits are unused from the current tax year.

Form 1139 is the faster route for most buyers. Corporations can alternatively claim a carryback refund by filing an amended return on Form 1120-X for each carryback year. There is no statutory 90-day processing clock for amended returns, so refunds take longer, but they typically receive more upfront IRS review before payment is issued rather than the tentative-refund-with-audit-authority model of Form 1139.

A note on the seller's transfer election

The seller's §6418 transfer election must be made on their original return, or a superseding return filed before the original due date. It cannot be made for the first time on an amended return, and no late-election relief is available under the final Treasury regulations (TD 9993, Treas. Reg. §1.6418-2(b)(4)). For buyers modeling a carryback, this means confirming early that the seller's election has been properly filed or will be filed on time. A missed election on the seller's side cannot be corrected after the fact, and the credit transfer does not occur.

How long should it take to process a carryback refund request?

The IRS has 90 days to process a Form 1139 carryback refund request

The Instructions for Form 1139 states, “The IRS will process this application within 90 days of the later of:

- The date the corporation files the complete application, or

- The last day of the month that includes the due date (including extensions) for filing the corporation's income tax return for the year in which the loss or credit arose (or, for a claim of right adjustment, the date of the overpayment under section 1341(b)(1))”

Importantly, receiving a refund doesn't validate the application. The IRS may later assess penalties and interest for overvalued property, negligence, rule disregard, or substantial income tax understatement if deductions or credits are found incorrect.

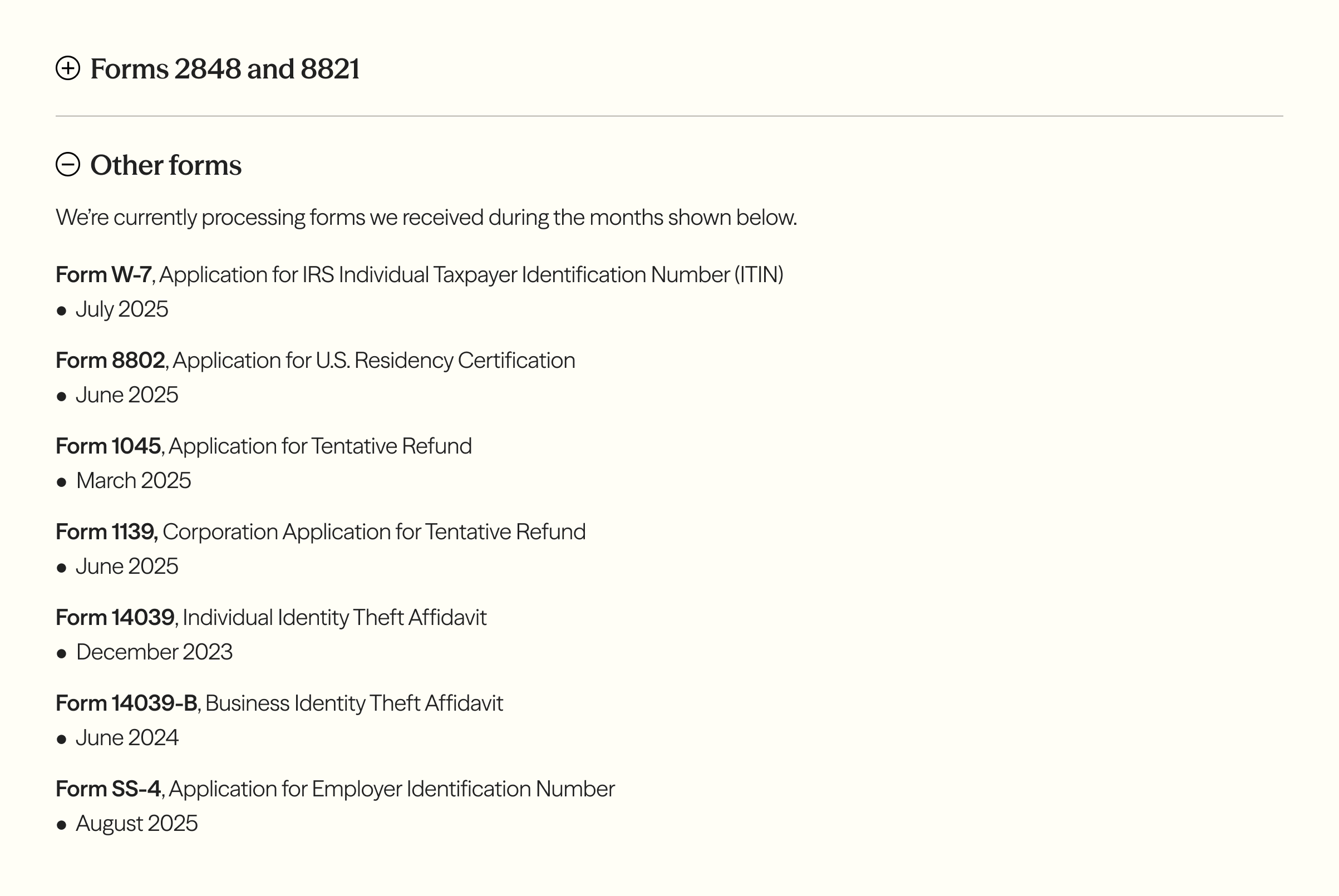

Current refund processing times are around 90 days

The IRS publishes processing statuses for various tax forms online. As of the publication date of this note (October 2025), the IRS is processing Form 1139s from June 2025 – that is, generally within the prescribed 90-day window.

Reunion accessed the IRS processing status webpage on October 29. The footer stated that the page was last reviewed or updated on October 24.

Some companies are assuming more than 90 days for modeling purposes

Reunion has supported several corporate tax leaders who are baking additional time into their carryback modeling assumptions. These are generally larger C corporations who are requesting refunds over $5 million, which are subject to another level of review through the Joint Committee on Taxation (JCT).

Most of these companies consider 90 days their best-case scenario and anticipate that a refund could take longer – perhaps six to nine months.

The IRS pays interest on refunds that take longer than 45 days

It's worth bearing in mind that the IRS pays interest on refund requests that take longer than 45 calendar days (from the point at which the IRS deems the application complete).

For companies with relatively low costs of capital, the interest paid by the IRS may, in fact, be accretive to the overall transaction ROI.

What types of credits are most suitable for a carryback?

Tax credits with wider discounts generally work well

All transferable tax credits, irrespective of discount, can be suitable for a carryback as long as they are “applicable credits.” We included an exhaustive list below.

Generally speaking, however, due to the time-value-of-money implications of the refund process, tax credits with wider discounts are most suitable for a carryback. Section 48 ITCs and Section 45Z CFPCs, which tend to trade in the low $0.90s, are commonly used for carrybacks.

Notably, "pre-IRA" credits, like 45 PTCs that are generarted from assets that were placed in service before the IRA, can only be carried back for one year.

Delayed payments and delayed transactions can also make the economic case for a carryback

A buyer can achieve a comparable time-value-of-money benefit by negotaiting delayed payment with the seller. Reunion supported a publicly traded buyer, for instance, who purchased 2025 Section 45 PTCs for a carryback from a seller who was willing to accept payment in June 2026.

Along the same lines, a buyer can simply wait to purchase tax credits until their tax filing date is closer. Reunion supported over a dozen 2024 tax credit transfers in September 2025 alone, and many of these transactions involved a carryback allocation. It's worth recalling, however, that tax credit prices generally rise as tax filing dates approach.

Keep in mind your company's other general business credits

Taxpayers who have other general business credits ("GBC") – for example, R&D and low-income housing – should be mindful of the ordering rules established in Instructions for IRS Form 3800. These rules dictate the order by which GBCs (including energy tax credits) must be applied against the current year's tax liability, which can have downstream impacts on carryback or carryforward mechanics.

Several of Reunion's banking clients who have LIHTC exposure prioritize Section 45Z CFPCs over Section 48 ITCs because of the general business credit ordering rules: investment credits (including "energy credits" claimed on IRS Form 3468) are used before low-income housing credits.

This ordering also matters within each carryback year. When applying a credit to a prior year, §38(c) capacity is consumed in the following sequence: carryforward credits from earlier years (oldest first), then the current-year credits for that prior period, and only then the carryback credit. A year that appears to have substantial tax capacity may have little room left for a carryback credit once existing carryforwards are accounted for. Modeling each carryback year's composition of credits — not just its headline tax liability — is essential before setting a purchase price.

"Applicable credits" that are eligible for a carryback

The following transferable tax credits are “applicable credits” that are eligible for carrybacks (per Section 39(a)(4) and Section 6417(b)):

- Section 48 ITCs

- Section 48E ITCs

- Section 45 PTCs attributable to qualified facilities which are originally placed in service after December 31, 2022

- Section 45Y PTCs

- Section 45X advanced manufacturing production credits

- Section 45U zero-emission nuclear power production credits

- Section 45Z clean fuel production credits

- Section 48C qualifying advanced energy project credits

- Section 45V clean hydrogen production credits attributable to qualified facilities which are originally placed in service after December 31, 2012

- Section 45Q carbon oxide sequestration credits attributable to carbon capture equipment which is originally placed in service after December 31, 2022

- Section 30C alternative fuel vehicle refueling property credits which, pursuant to subsection (d)(1) of such section, are treated as a credit listed in Section 38(b)

Watch Reunion's webinar on tax credit carrybacks and carryforwards

Reunion hosted a webinar, The Role of Carrybacks & Carryforwards in Clean Energy Tax Credit Transactions, on November 12. Our Head of Commercial Strategy, Alessio De Falcis, led a panel of tax and legal experts from CLA, Orrick, and McDermott to explored how carryback and carryforward provisions work and what they mean for corporate tax credit purchasers.

The panel discussed:

- How carryback and carryforward provisions apply to transferred credits under the IRA

- Key considerations for timing, documentation, and compliance

- How purchasers can plan for credit utilization across multiple tax years

- IRS guidance updates and emerging best practices from prior filing cycles

- Practical insights from recent transactions

We published a recording and transcript of the webinar.