ITC Vs PTC: IRA Tax Credits For Renewable Energy Projects

Compare ITC vs PTC under IRA tax credits for renewable energy. Learn about transferability, risks and how these credits benefit businesses in the clean energy sector.

Key features of the IRA's 11 transferable tax credits

The Inflation Reduction Act (IRA) created 11 transferable tax credits to promote investment into clean energy. This article summarizes key features of each transferable credit including technology, duration, period of availability, and rates. Depending on the credit, we included three rates:

- Base: Rate assuming prevailing wage and apprenticeship requirements are not met.

- Full: Rate assuming prevailing wage and apprenticeship requirements are met. The full rate is five times higher than the base rate.

- Bonus: Additional rates assuming bonus credits – energy community, domestic content, low-income community – are met.

To jump directly to a credit, click a link below:

- §45 PTC – Electricity produced from certain renewable sources

- §45Y PTC – Clean electricity production credit (technology-neutral PTC)

- §48 ITC – Energy credit

- §48E ITC – Clean electricity investment credit (technology-neutral ITC)

- §30C ITC – Alternative fuel vehicle refueling property credit

- §45U PTC – Zero-emission nuclear power production credit

- §45Q PTC – Credit for carbon oxide sequestration

- §45Z PTC – Clean fuel production tax credit

- §45V PTC – Clean hydrogen production tax credit

- §48C ITC – Advanced energy project credit

- §45X PTC – Advanced manufacturing production credit

§45 PTC - Electricity produced from certain renewable sources

Funding mechanism: Production tax credit

Technology grouping: Electricity

IRA Section: 13101

New or existing: Existing - modified and extended

Eligibility: Facilities generating electricity from wind, biomass, geothermal, solar, small irrigation, landfill and trash, hydropower, and marine and hydrokinetic renewable energy

U.S. Code: 26 U.S. Code §45

Duration: 10 years from the date the project is placed in service

Period of availability: Projects must begin construction prior to 1/1/2025. For projects placed in service in 2025 or later, the §45Y PTC will replace the §45 PTC

Stackability and limitations: Cannot be stacked with §48

Inflation adjustment: Subject to an annual inflation adjustment

Elective pay (direct pay): Only available to tax-exempt entities

Recapture: Not applicable

Rates

The §45 PTC has two different rate regimes depending on when a project was placed in service. If a project was placed in service before 1/1/2022, the full PTC calculation is [1.5 cents] x [inflation adjustment factor] rounded to the nearest 0.1 cents. Importantly, projects placed in service before 2022 are not subject to prevailing wage and apprenticeship requirements. If a project was placed in service after 12/31/2021, the full PTC rate calculation is [0.3 cents] x [inflation adjustment factor] rounded to the nearest 0.05 cents. For projects meeting PWA requirements, this product is multiplied by five.

- Base rate (placed in service before 1/1/22): Not applicable. Projects placed in service before 1/1/22 are not subject to prevailing wage and apprenticeship requirements. They receive the full rate

- Base Rate (placed in service after 12/31/21): $5.50 per MWh for wind, closed-loop biomass, geothermal, and solar. $3.00 per MWh for open-loop biomass, landfill gas, trash, qualified hydropower, and marine and hydrokinetic renewable energy

- Full rate: (placed in service before 1/1/22): $28.00 per MWh for wind, closed-loop biomass, and geothermal. $14.00 per MWh for open-loop biomass, landfill gas, trash, qualified hydropower, and marine and hydrokinetic renewable energy

- Full Rate (placed in service after 12/31/21): $27.50 per MWh for wind, closed-loop biomass, geothermal, and solar. $15.00 per MWh for open-loop biomass, landfill gas, trash, qualified hydropower, and marine and hydrokinetic renewable energy

- Energy Community: 10%

- Domestic Content: 10%

§45Y PTC - Clean electricity production credit

Funding mechanism: Production tax credit

Technology grouping: Electricity

IRA Section: 13701

New or existing: New

Eligibility: Technology-neutral tax credit for production of clean electricity. The §45Y PTC is for facilities generating electricity for which the greenhouse gas emissions rate is not greater than zero

U.S. Code: 26 U.S. Code §45Y

Duration: 10 years from the date the project is placed in service

Period of availability: Projects placed in service beginning in 2025 are eligible for the credit.

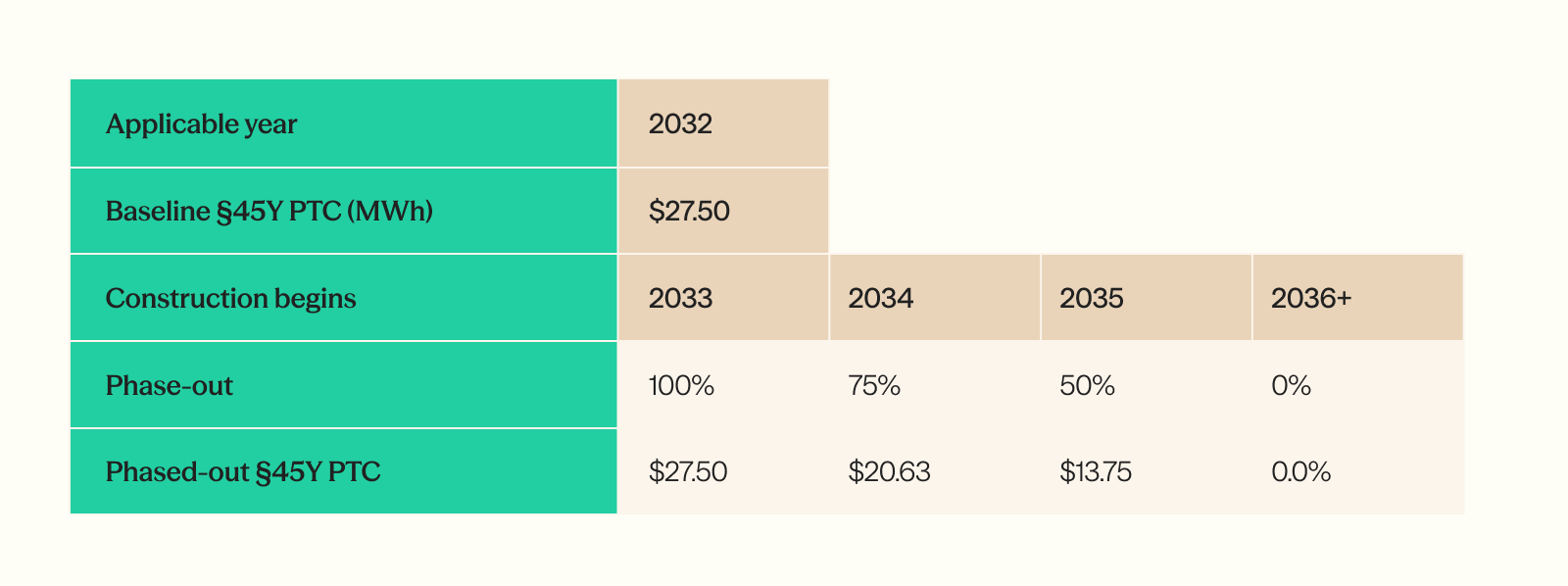

The credit is subject to a four-year phase-out (100%, 75%, 50%, 0%) for projects that begin construction in the first calendar year after the ”applicable year,” which is the later of (1) 2032 or (2) the calendar year in which the IRS determines that the annual greenhouse gas emissions from the production of electricity in the U.S. are equal to or less than 25% of the annual greenhouse gas emissions from the production of electricity in the U.S. in 2022.

Below is an example phase-out schedule, assuming the "applicable year" is 2032. An eligible project that begins construction in 2035 and meets PWA requirements will generate §45Y PTCs worth $13.75 per MWh when it is placed in service.

Stackability and limitations: Cannot be stacked with §48E or §45Q

Inflation adjustment: Subject to an annual inflation adjustment

Elective pay (direct pay): Only available to tax-exempt entities

Recapture: Not applicable

Rates

- Base rate: $5.50 per MWh (as increased by annual inflation adjustment factor from 2023)

- Full rate: $27.50 per MWh (as increased by annual inflation adjustment factor from 2023)

- Energy Community: 10%

- Domestic Content: 10%

Guidance: Further guidance pending. The credit is included in the IRS 2023-2024 Priority Guidance Plan

§48 ITC - Energy credit

Funding mechanism: Investment tax credit

Technology grouping: Electricity

IRA Section: 13102

New or existing: Existing - modified and extended

Eligibility: Fuel cell, solar, geothermal, small wind, energy storage, biogas, microgrid controllers, and combined heat and power properties

U.S. Code: 26 U.S. Code §48

Period of availability: Projects must begin construction prior to 1/1/2025. For projects placed in service in 2025 or later, the §48E ITC will replace the §48 ITC

Stackability and limitations:

- Cannot be stacked with §48E, §45, §45Y, §48C, §45Q

- Subject to recapture per §50

Inflation adjustment: None

Elective pay (direct pay): Only available to tax-exempt entities

Recapture: Subject to five-year recapture period beginning on placed-in-service date. Recapture amount decreases by 20% per year

Rates

- Base rate: 6%

- Full rate: 30%

- Energy Community: 10%

- Domestic Content: 10%

- Low-Income: 10% if located in low-income community or on Indian land. 20% if part of qualified low-income residential building project or qualified low-income economic benefit project. Limited to projects less than 5 MW

Guidance (since passage of the IRA):

- Notice of proposed rulemaking: Definition of Energy Property and Rules Applicable to the Energy Credit (11/22/2023)

- Final rule pending

§48E ITC - Clean electricity investment credit (technology-neutral ITC)

Funding mechanism: Investment tax credit

Technology grouping: Electricity

IRA Section: 13702

New or existing: New

Eligibility: Technology-neutral tax credit for investment in facilities generating electricity for which the greenhouse gas emissions rate is not greater than zero

U.S. Code: 26 U.S. Code §48E

Period of availability: Projects placed in service beginning in 2025 are eligible for the credit.

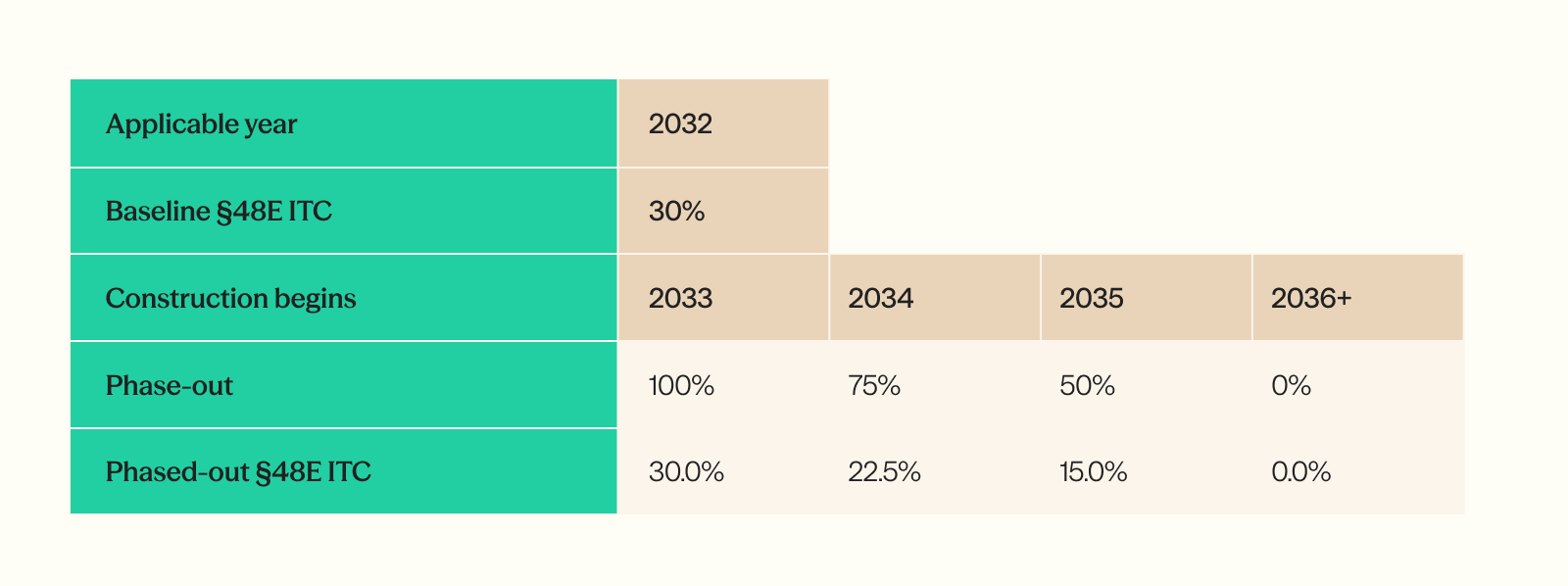

The credit is subject to a four-year phase-out (100%, 75%, 50%, 0%) for projects that begin construction in the first calendar year after the ”applicable year,” which is the later of (1) 2032 or (2) the calendar year in which the IRS determines that the annual greenhouse gas emissions from the production of electricity in the U.S. are equal to or less than 25% of the annual greenhouse gas emissions from the production of electricity in the U.S. in 2022.

Below is an example phase-out schedule, assuming the "applicable year" is 2032. An eligible project that begins construction in 2034 and meets PWA requirements will generate a §48E ITC worth 22.5% of the project’s qualified investment when it is placed in service.

Stackability and limitations:

- Cannot be stacked with §48, §45, §45Y, §48C, §45Q

- Subject to recapture per §50

Inflation adjustment: None

Elective pay (direct pay): Only available to tax-exempt entities

Recapture: Subject to five-year recapture period beginning on placed-in-service date. Recapture amount decreases by 20% per year

Rates

- Base rate: 6%

- Full rate: 30%

- Energy Community: 10%

- Domestic Content: 10%

- Low-Income: 10% if located in low-income community or on Indian land. 20% if part of qualified low-income residential building project or qualified low-income economic benefit project. Limited to projects less than 5 MW

Guidance: Further guidance pending. The credit is included in the IRS 2023-2024 Priority Guidance Plan

§30C ITC – Alternative fuel vehicle refueling property credit

Funding mechanism: Investment tax credit

Technology grouping: Vehicles

IRA Section: 13404

New or existing: Existing - modified and extended

Eligibility: For clean-burning fuels, as defined in the statute. Alternative fuels include electricity (charging property), ethanol, natural gas, liquified petroleum gas, hydrogen, and biodiesel

U.S. Code: 26 U.S. Code §30C

Period of availability: Project must be placed in service between 1/1/2023 and 12/31/2032

Stackability and limitations:

- The project must be in the U.S. in a low-income or rural area

- The credit is capped at $100,000 per property

Inflation adjustment: None

Elective pay (direct pay): Only available to tax-exempt entities

Recapture: Recapture provision is anticipated in Treasury proposed regulations

Rates

- Base rate: 6%

- Full rate: 30%

Guidance (since passage of the IRA):

- Notice 2022-56: Request for comments on Section 45W and Section 30C (12/3/2022)

- Notice 2024-20: Guidance on Satisfying the Geographical Requirements of the Section 30C AlternativeFuel Vehicle Refueling Property Credit (1/19/2024)

- Notice 2024-20 - Appendix A: List of 11-digit census tract GEOIDs that are eligible for § 30C using 2015 delineations ofcensus tract boundaries (1/19/2024)

- Notice 2024-20 - Appendix B: List of 11-digit census tract GEOIDs that are eligible for § 30C using 2020 delineations of census tract boundaries, including non-urban census tracts (1/19/2024)

- Further guidance pending. The credit is included in the IRS 2023-2024 Priority Guidance Plan. §30C was previously authorized under law, so existing guidance may still apply

§45U PTC – Zero-emission nuclear power production credit

Funding mechanism: Production tax credit

Technology grouping: Electricity

IRA Section: 13105

New or existing: New

Eligibility: Electricity from qualified nuclear power facilities

U.S. Code: 26 U.S. Code §45U

Duration: 2024-2032

Period of availability: Available for electricity produced and sold after 12/31/23, in tax years beginning after that date. Not available for tax years beginning after 12/31/32

Stackability and limitations:

- Cannot claim §45J credit

- Credit subject to “reduction amount” depending on the amount of energy produced and the gross receipts of the facility

- Payments from federal, state, or local zero-emission nuclear subsidies reduce the credit amount

Inflation adjustment: Subject to annual inflation adjustment

Elective pay (direct pay): Only available to tax-exempt entities

Recapture: Not applicable

Rates

- Base rate: $3.00 per MWh, subject to “reduction amount” depending on the amount of energy produced and the gross receipts of the facility

- Full rate: $15.00 per MWh, subject to “reduction amount” depending on the amount of energy produced and the gross receipts of the facility. Apprenticeship requirements do not apply to §45U to receive the full rate

Guidance: Further guidance pending. The credit is included in the IRS 2023-2024 Priority Guidance Plan

§45Q PTC - Credit for carbon oxide sequestration

Funding mechanism: Production tax credit

Technology grouping: Electricity

IRA Section: 13104

New or existing: Existing - extended and modified

Eligibility: The §45Q PTC is for carbon dioxide sequestration coupled with permitted end uses within the U.S.

U.S. Code: 26 U.S. Code §45Q

Duration: 12 years from the date facility is placed in service

Period of availability: Facilities must be placed in service before 2033

Stackability and limitations:

- Limited to U.S. facilities with minimum capture volumes:

- 1,000 metric tons of CO2 per year for direct air capture (DAC) facilities

- 18,750 metric tons for electricity-generating facilities with carbon capture capacity of 75% of baseline CO2 production

- 12,500 metric tons for any other facility

- Cannot be stacked with §45V, §45Z, §48, §48C, or §48E

Inflation adjustment: Subject to annual inflation adjustment

Elective pay (direct pay): Available to tax-exempt entities. Available to non-tax-exempt entities for up to five years. If a non-tax-exempt entity selects elective pay, such entity “shall be treated as having made such election for each of the four succeeding tax years.” During the five-year period, a non-tax-exempt entity “may elect to revoke the application” of elective pay for the remainder of the five-year period. The non-tax-exempt entity cannot “subsequently revoke” the elective pay revocation

Recapture: Subject to recapture if qualified carbon ceases to be captured, disposed of, or used as a tertiary injectant. Recapture period is three years, starting from first injection for disposal in secure geological storage or use as a tertiary injectant. Any recapture amount will be accounted for in the tax year that it’s identified and reported

Rates

- Base rate: $17/metric ton of carbon dioxide captured and sequestered ($36 for DAC facilities). $12/metric ton for carbon dioxide that is injected for enhanced oil recovery or utilized ($26 for DAC facilities)

- Full rate: $85/metric ton of carbon dioxide captured and sequestered ($180 for DAC facilities). $60/metric ton for carbon dioxide that is injected for enhanced oil recovery or utilized ($130 for DAC facilities)

Guidance (since passage of the IRA):

- Notice 2022-57: Request for comments on the Credit for Carbon Oxide Sequestration (11/3/2022)

- Further guidance pending. The credit is included in the IRS 2023-2024 Priority Guidance Plan

§45Z PTC – Clean fuel production tax credit

Funding mechanism: Production tax credit

Technology grouping: Fuels

IRA Section: 13204

New or existing: New

Eligibility: The §45Z PTC is for the domestic production of clean transportation fuels, including sustainable aviation fuels. Fuels with less than 50 kilograms of carbon dioxide equivalent per million British thermal units (CO2e per mmBTU) qualify as clean fuels eligible for credits

U.S. Code: 26 U.S. Code §45Z

Duration: 3 years

Period of availability: Available for fuels produced after 2024 and used or sold before 2028

Stackability and limitations:

- Producers must be registered as a producer of clean fuel under section 4101

- Fuels must be produced in the U.S.

- To be considered "clean," fuels must emit no more than 50 kilograms of carbon dioxide equivalent per one million British thermal units (CO2e per mmBTU)

- "Transportation fuels" must be deemed "suitable for use as a fuel in a highway vehicle or aircraft"

- Cannot be stacked with §45V or §45Q

Inflation adjustment: Subject to an annual inflation adjustment

Elective pay (direct pay): Only available to tax-exempt entities

Recapture: Not applicable

Rates

- Base rate: $0.20/gallon for non-aviation fuel and $0.35/gallon for aviation fuel, multiplied by the emissions factor of the fuel

- Full rate: $1.00/gallon for non-aviation fuel and $1.75/gallon for aviation fuel, multiplied by the emissions factor of the fuel

Guidance:

- Notice 2022-58: Request for Comments on Credits for Clean Hydrogen and Clean Fuel Production (11/3/2022)

- Further guidance pending. The credit is included in the IRS 2023-2024 Priority Guidance Plan

§45V PTC – Clean hydrogen production tax credit

Funding mechanism: Production tax credit

Technology grouping: Fuels

IRA Section: 13204

New or existing: New

Eligibility: The §45V PTC is for the production of clean hydrogen at a qualified clean hydrogen facility

U.S. Code: 26 U.S. Code §45V

Duration: 10 years from the date the project is placed in service

Period of availability: Credit is for hydrogen produced after 12/31/22. Credit is available for facilities placed in service before 1/1/33

Stackability and limitations:

- Producers must be in the U.S.

- The project developer can make a non-irrevocable election for an ITC (instead of the 45V PTC) as long as the project has not claimed the 45Q PTC for carbon sequestration

- Cannot be stacked with §45Q, §45Z, or §48C

Inflation adjustment: Subject to an annual inflation adjustment

Elective pay (direct pay): Available to tax-exempt entities. Available to non-tax-exempt entities for up to five years. If a non-tax-exempt entity selects elective pay, such entity “shall be treated as having made such election for each of the four succeeding tax years.” During the five-year period, a non-taxexempt entity “may elect to revoke the application” of elective pay for the remainder of the five-year period. The non-tax-exempt entity cannot “subsequently revoke” the elective pay revocation

Recapture: Not applicable

Rates

- Base rate: $0.60/kg multiplied by the applicable percentage. The applicable percentage ranges from 20% to 100% depending on lifecycle greenhouse gas emissions

- Full rate: $3.00/kg multiplied by the applicable percentage. The applicable percentage ranges from 20% to 100% depending on lifecycle greenhouse gas emissions

Guidance:

- Notice 2022-58: Request for Comments on Credits for Clean Hydrogen and Clean Fuel Production (11/3/2022)

- Notice of proposed rulemaking: Section 45V Credit for Production of Clean Hydrogen; Section 48(a)(15) Election to Treat Clean Hydrogen Production Facilities as Energy Property (12/21/2023)

- Final rule pending

§48C ITC – Advanced energy project credit

Funding mechanism: Investment tax credit

Technology grouping: Manufacturing

IRA Section: 13501

New or existing: Existing – modified and extended

Eligibility: For investments in advanced energy projects, as defined in §48C(c)(1). A project that:

- Re-equips, expands, or establishes an industrial or manufacturing facility for the production or recycling of a range of clean energy equipment and vehicles

- Re-equips an industrial or manufacturing facility with equipment designed to reduce greenhouse gas emissions by at least 20 percent

- Re-equips, expands, or establishes an industrial facility for the processing, refining, or recycling of critical materials

U.S. Code: 26 U.S. Code §48C

Period of availability: §48C is an allocated credit. It is available when the application and certification process begins and ends when the credit is fully allocated. Projects must be placed in service within two years of application approval and certification

Stackability and limitations:

- Allocated credit subject to $10 billion cap. At least $4 billion must be allocated to energy communities

- Cannot be stacked with §45X, §48, §48E, §45Q, or §45V

Inflation adjustment: None

Elective pay (direct pay): Only available to tax-exempt entities

Recapture: Subject to recapture per §50

Rates

- Base rate: 6%

- Full rate: 30%

Guidance (since passage of the IRA):

- Notice 2023-18: Initial Guidance for Qualifying Advanced Energy Project Credit Allocation Program Under Section 48C(e) (2/13/2023)

- Notice 2023-44: Additional Guidance for Qualifying Advanced Energy Project Credit Allocation Program Under Section 48C(e) (5/31/2023)

- Further guidance pending. The credit is included in the IRS 2023-2024 Priority Guidance Plan

§45X PTC – Advanced manufacturing production credit

Funding mechanism: Production tax credit

Technology grouping: Manufacturing

New or existing: New

IRA Section: 13502

Eligibility: The §45X PTC is for domestic manufacturing of components for solar and wind energy, inverters, battery components, and critical minerals

U.S. Code: 26 U.S. Code §45X

Duration: 2023-2032

Period of availability: Credit for critical materials is permanent starting in 2023. For other components, credit phases down over 2030-2032

Stackability and limitations:

- Production of eligible components must be in the U.S.

- Property must be sold to an unrelated party unless making an election under §45X(a)(3)(b)

- Cannot claim §45X credit for property produced at facilities that received the §48C credit

- Credit is subject to a phase-out beginning in 2030 (75%, 50%, 25%, 0%), except for critical minerals

Inflation adjustment: Although §45X is a PTC, the credit is not inflation-adjusted

Elective pay (direct pay): Available to tax-exempt entities. Available to non-tax-exempt entities for up to five years. If a non-tax-exempt entity selects elective pay, such entity “shall be treated as having made such election for each of the four succeeding tax years.” During the five-year period, a non-tax-exempt entity “may elect to revoke the application” of elective pay for the remainder of the five-year period. The non-tax-exempt entity cannot “subsequently revoke” the elective pay revocation

Recapture: Not applicable

Guidance:

- Notice of proposed rulemaking and public hearing (12/15/2023)

- Further guidance pending. The credit is included in the IRS 2023-2024 Priority Guidance Plan

Rates

Rates for the §45X PTC are component-specific and listed on IRS Form 7207. §45X does not have a PWA requirement