.avif)

.avif)

.avif)

.avif)

Guiding tax credit transactions with speed and certainty

Reunion partners with leading corporations and clean energy companies to realize the full value of transferable tax credits.

sheet sign to close

Reunion-affiliated projects

Unmatched expertise in tax credit transfers, every step of the way

Hands-on deal guidance

We serve as a trusted partner during every step of the transaction.

Proven process

We have a tested and efficient process, honed across 100+ transactions ranging from $10M to $1B+.

Our sole focus

Tax credit transactions and compliance are all we do, which means deeper expertise and better outcomes for every client.

100+ closed transfers. Each one sharpens the next.

Reunion has consistently delivered high-quality tax credits quickly and provided the due diligence expertise to move our transactions forward. We have now partnered with Reunion across multiple transactions, and their collaborative approach has made the buying process smooth from start to finish.

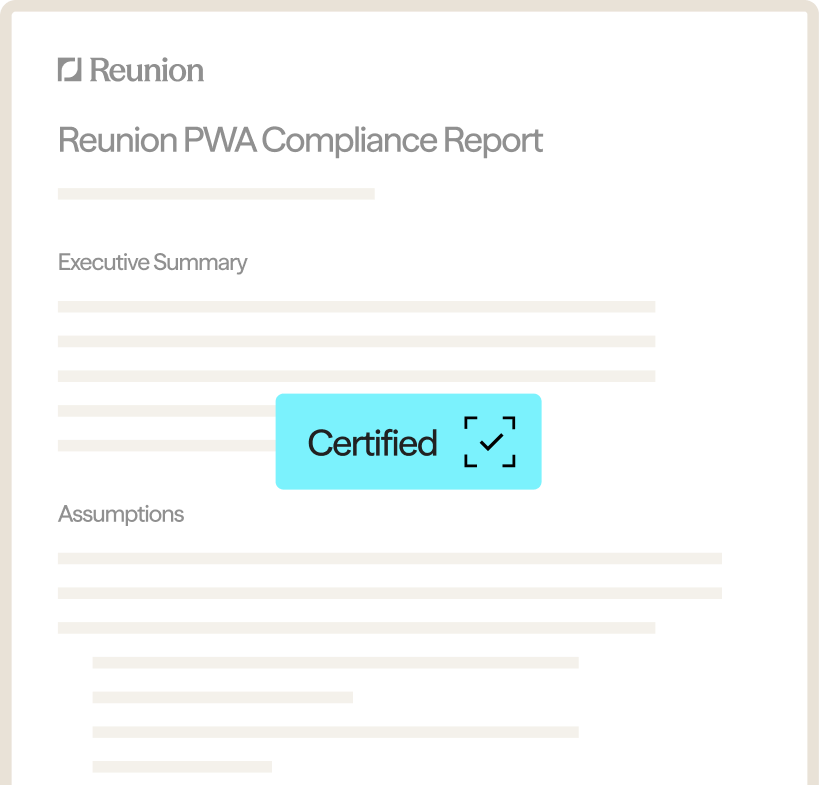

Real-time tax credit compliance

Reunion provides an advanced suite of technology and expert-driven solutions to navigate requirements for tax credit compliance.

Our software analyzes data in real time and produces audit-ready reports verified by our team to ensure your credits are compliant.

Clients can monitor their compliance status 24/7 in an easy-to-use platform that reflects the most current data from government and market sources.

Learn more about compliance

Compliance

This was a really valuable learning experience for our project, especially around PWA compliance requirements. Reunion’s support helped us see real-time compliance insights within two weeks and get to an audit-ready posture in under three months.