ASU 2023-09 should highlight adoption of IRA clean energy tax credits

ASU 2023-09, Improvements to Income Tax Disclosures, requires public and private companies to provide a more detailed tax rate reconciliation in their financial statements. Participation in the transferable clean energy tax credit market should become more clear.

Overview of ASU 2023-09

Accounting Standards Update (ASU) 2023-09, Improvements to Income Tax Disclosures, represents the FASB’s latest effort to modernize and enhance income tax disclosures under ASC 740, with a clear emphasis on improving transparency around effective tax rate drivers and cash taxes paid.

For corporate tax professionals, the update is less about changing tax accounting and more about significantly expanding what must be explained – and supported – in the tax footnote.

At its core, 2023-09 requires companies, public and private, to provide a more robust and structured explanation of why their effective tax rate differs from the statutory federal rate. The rate reconciliation must now be presented in a tabular format that includes both dollar amounts and percentages, and reconciling items must be categorized using prescribed groupings such as state and local taxes, foreign tax effects, tax credits, valuation allowance changes, and changes in tax laws.

When reconciling items exceed a quantitative threshold – generally 5.0% of the tax at the statutory rate – further disaggregation is required, often by nature or jurisdiction. The result is a more decision-useful, but also more data-intensive, reconciliation.

When do the disclosure updates go into effect?

ASU 2023-09 applies to public business entities (PBEs) and non-PBEs. Simplistically, a PBE is a public company, while a non-PBE is a private company.

The new requirements within ASU 2023-09 go into effect at different dates, depending on the type of entity:

- PBEs: Annual periods beginning after December 15, 2024 – generally, calendar year 2025

- Non-PBEs: Annual periods beginning after December 15, 2025 – generally, calendar year 2026

Impacts on transferable tax credit investments

ASU 2023-09 does not change the accounting for transferable tax credits, but it will make their financial statement impact more visible through enhanced income tax disclosures.

Most notably, tax credits that materially reduce tax expense will need to be more clearly reflected in the effective tax rate reconciliation. Under the new standardized categories and quantitative thresholds, significant transferable credits are likely to be disclosed as a separate reconciling item rather than being aggregated within broader “credits” or “other” categories, increasing transparency around their role in lowering the effective tax rate.

The new income taxes paid disclosure also affects companies that utilize transferable credits. Because these credits often reduce cash taxes owed, companies may report low or minimal taxes paid in certain jurisdictions. ASU 2023-09 requires income taxes paid, net of refunds, to be disaggregated by federal, state, and foreign jurisdictions, with separate disclosure for significant jurisdictions, making the disconnect between tax expense and cash taxes paid more apparent.

Finally, while the ASU is disclosure-focused, it may drive additional documentation and controls around transferable credits. Companies should expect greater scrutiny of the nature, materiality, and sustainability of tax credit investments, as well as more robust explanations in the tax footnote regarding how those credits affect both the effective tax rate and cash tax profile.

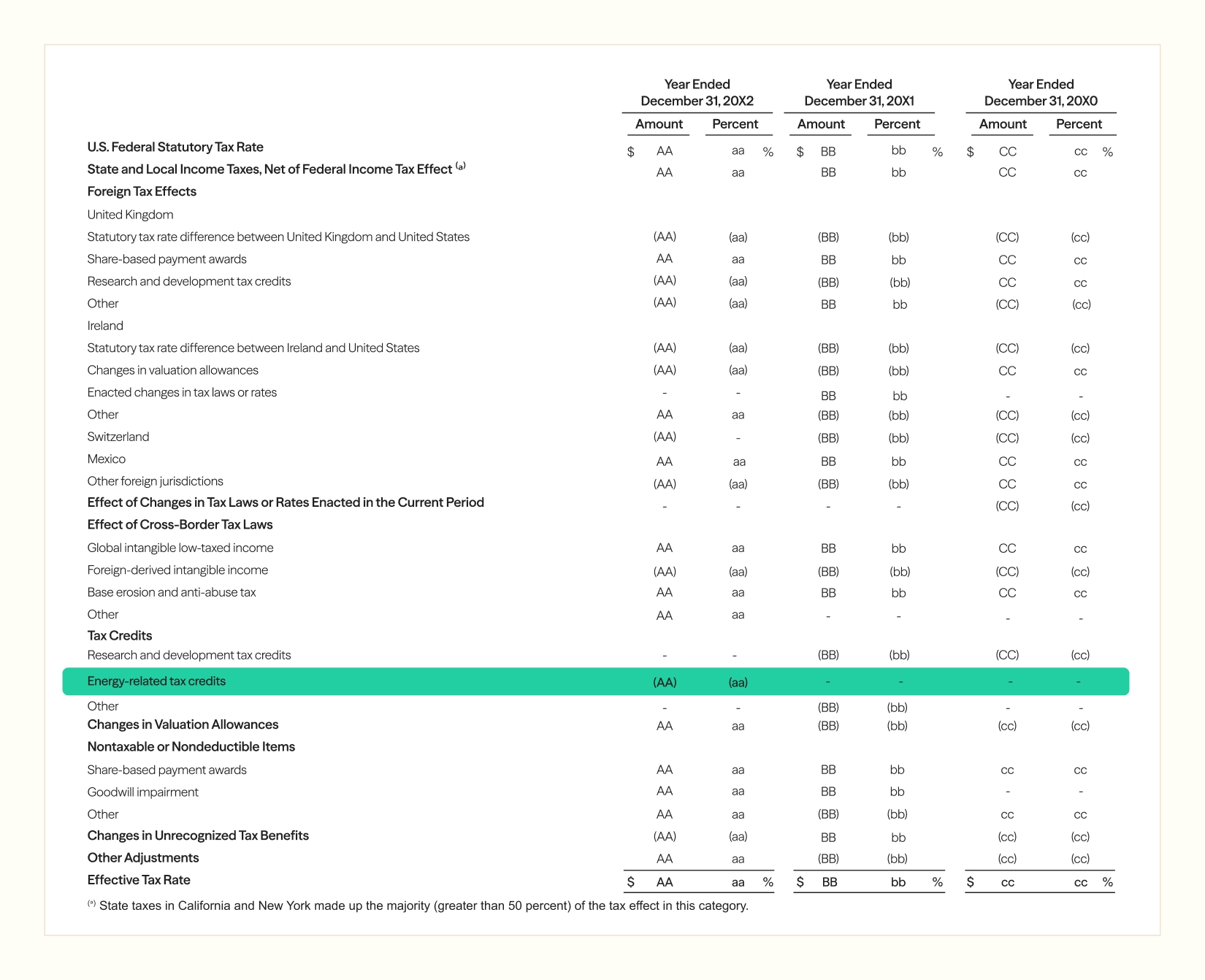

Sample income tax disclosure

ASU 2023-09 includes a “sample rate reconciliation between income tax expense (or benefit) and statutory expectations.”

Companies that have disclosed a transferable tax credit purchase

Reunion maintains a list of public companies that have disclosed a transferable tax credit purchase through an SEC filing. We invite you to request access to the evolving list.