Where tax credit deals get done

Reunion’s transaction process has been battle-tested across over $8 billion in transactions. Behind each step are details that we have honed across 100+ deals, leading to higher success rates and faster times to close.

Get Started

Reunion's due diligence memo was one of the best documents I've received in my 30 years as a tax professional.

VP of Tax at a publicly traded insurance company

The gold standard for tax credit transactions

We are deeply involved in every step of the tax credit transaction process, from sourcing off-market opportunities to providing institutional-grade diligence.

Access to walled garden of vetted credits

No stone left unturned

We widely canvass the market to find the highest quality and highest value credits.

Off-market opportunities

Reunion often gets access to off-market opportunities through our strong relationships with a wide network of sellers.

Securing ideal tax credits

Curated opportunities

Reunion curates attractive credit opportunities that cater to specialized buyer needs.

Understand market dynamics

We help buyers understand market dynamics and win favorable terms, drawing from Reunion's proprietary data and experience in closing 100+ transactions.

Hands-on deal guidance

Skilled mediation

Reunion quarterbacks the deal, providing skilled mediation through a transparent negotiation process that moves deals forward for all parties.

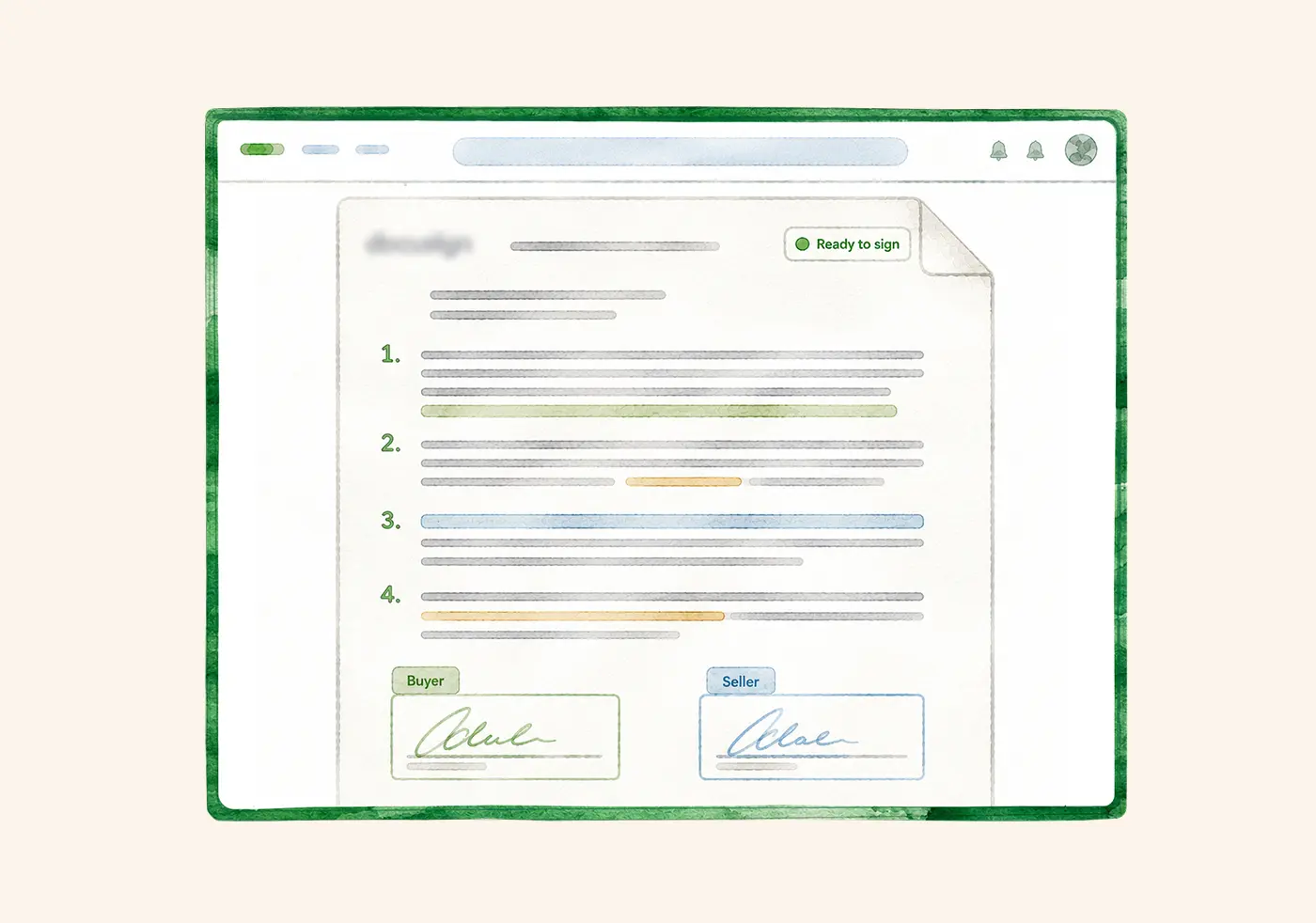

Comprehensive memo

Reunion provides a comprehensive diligence memo — a unique offering utilized by Fortune 100s for internal approvals. We produce the initial memo within 10 days of term sheet execution in order to identify key issues upfront.

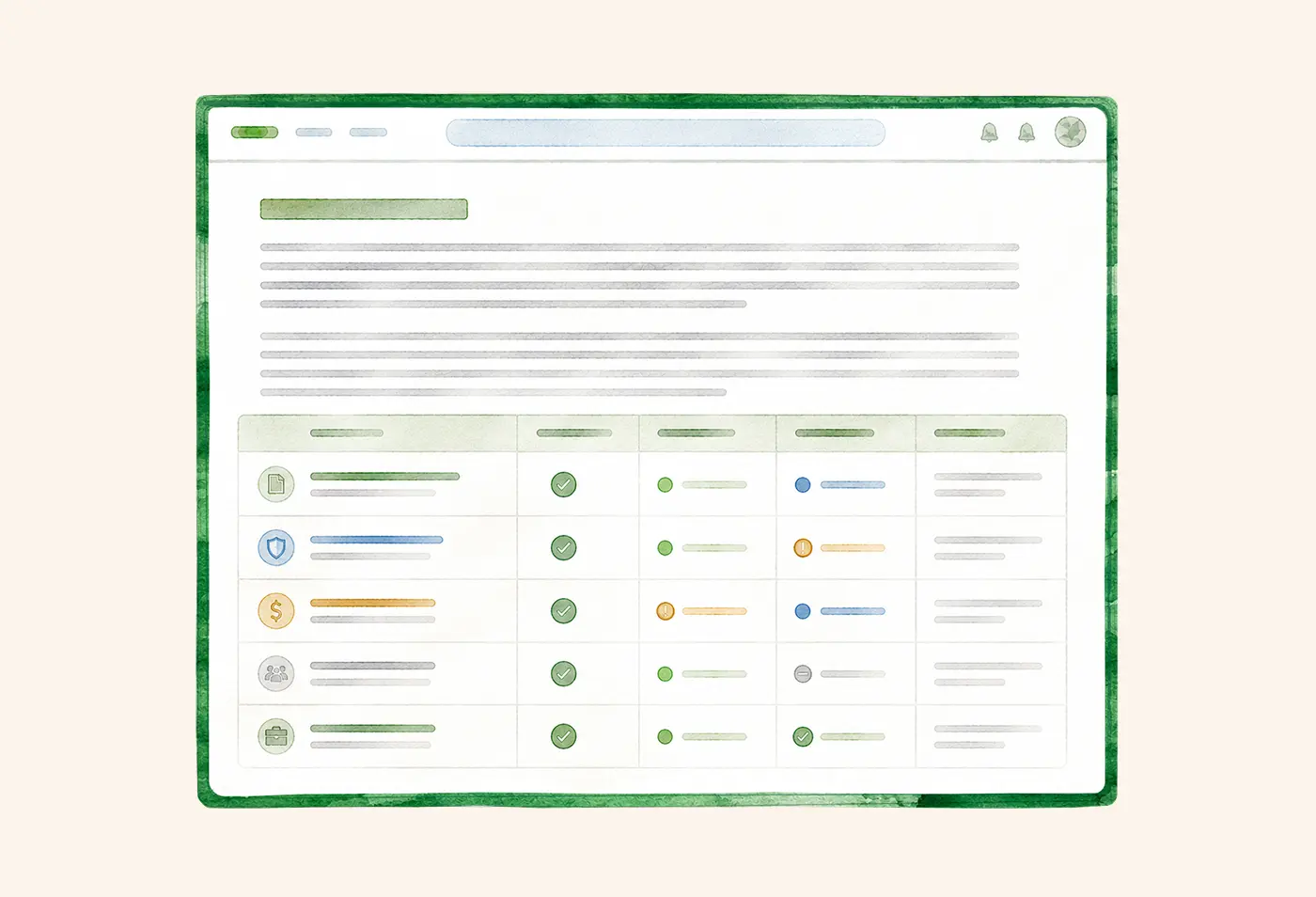

In-depth risk management

Risk management

We carefully examine deal structure and documents to manage risk, ensuring favorable contractual terms and risk mitigation

Organized documentation

We prepare detailed documentation to defend against a potential IRS audit, so you have a comprehensive and organized set of documents

Find the right credits for every tax strategy

The Reunion Transaction Process reduces risk and increases certainty of close

The Reunion Transaction Process (RTP) has been tested across over $8 billion in transactions.

Understand buyer requirements

Deeply understand buyer specifications for pricing, timing, and more

Curate opportunities

Provide 3 to 6 opportunities at a time, with clear explanation of how each opportunity meets buyer goals

Sign term sheet

Leverage market data and a proven negotiation process to drive alignment on a signed term sheet

Perform upfront diligence

Deliver initial diligence memo within 10 days of term sheet, to surface any risks early

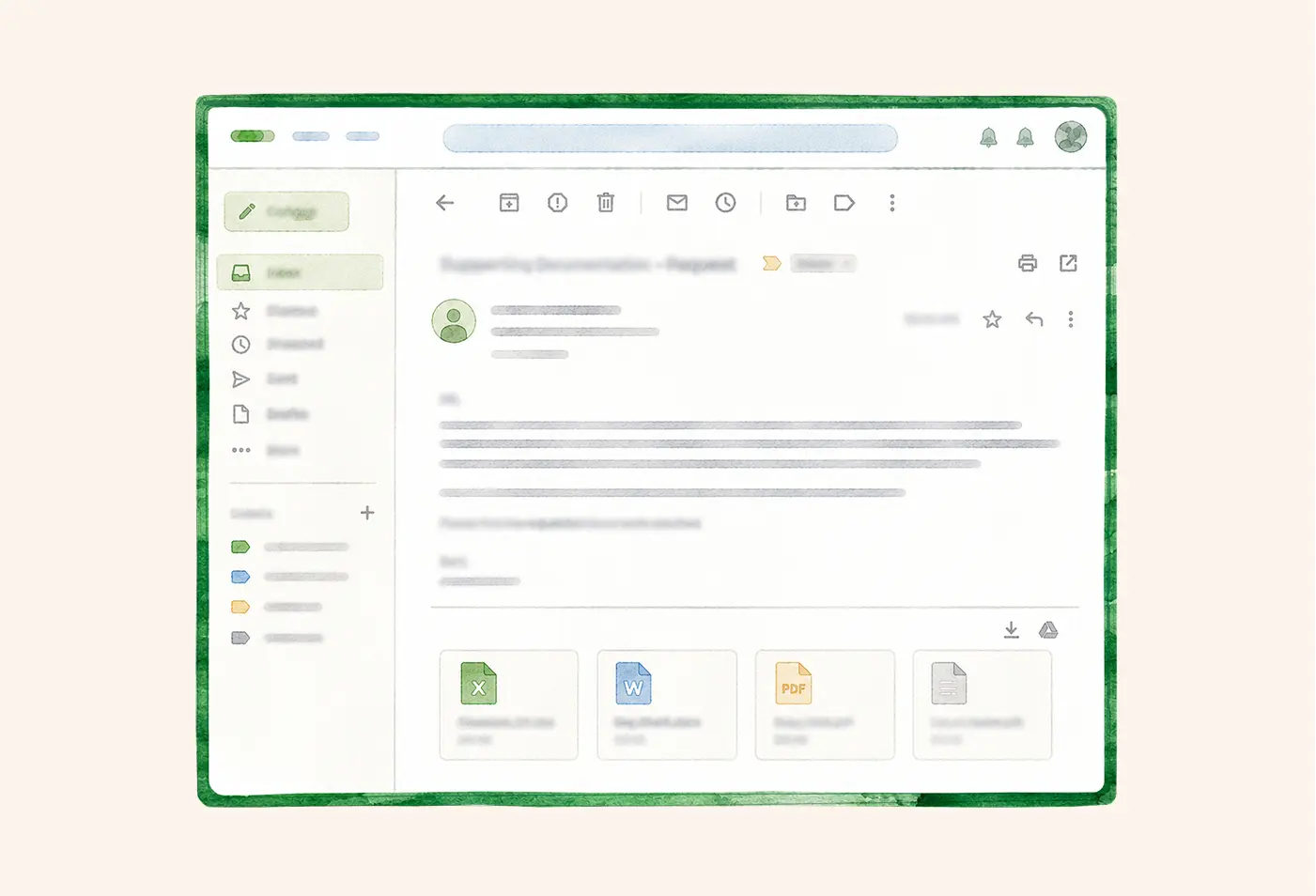

Collect supporting documentation

Collect and organize a comprehensive set of supporting documentation, giving buyers confidence in the event of future IRS challenge

Negotiate final contracts

Support negotiation of contracts through our skilled mediation process and extensive transaction experience

.avif)

.avif)

.avif)

.avif)

A first-time buyer closed $200M and opened a multi-year relationship

A Fortune 500 corporation was entering the §6418 market for the first time in 2024.

Already enrolled in the IRS Compliance Assurance Process, they couldn't afford a learning curve and needed audit-ready documentation from day one. They also wanted a single, experienced counterparty capable of delivering at scale, and terms that minimized out-of-pocket expenses.

Reunion delivered. And the buyer repeated the deal in 2025 and 2026.

A top 100 taxpayer's first $1B+ in advanced manufacturing credits

A publicly traded Fortune 500 company wanted to offset a significant portion of its $1B+ in federal taxes.

§45X credits were ideal given the scale involved, but were a newer credit type with limited market precedent. They needed a partner who could secure the ideal credits, lead diligence on a complex manufacturing portfolio, and build the internal case for executive approval.

Reunion ran the process end-to-end — from competitive bid through closing — and delivered the diligence memo that got the deal approved.

95% success from term sheet to close: Hear from our clients