A guide to quick refunds for tax credit buyers

Form 4466 quick refunds help tax credit buyers recoup their investment months sooner

In brief

A quick refund under IRC §6425 allows a corporation that has overpaid its estimated income taxes – perhaps due to buying tax credits – to get cash back before filing its full tax return. By filing IRS Form 4466 shortly after year-end (and before the regular return due date), eligible corporations can recover overpayments – so long as the excess exceeds both $500 and 10% of expected tax liability. For tax credit buyers in particular, quick refunds are a powerful cashflow tool, accelerating the economic benefit of credits by months compared to the standard refund process.

Quick refunds allow corporations to recover overpaid estimated taxes early

Under IRC §6425, a “quick refund” allows a corporation that has overpaid its estimated federal income tax to request an “adjustment” of its estimated income tax prior to filing its full annual return.

Corporations may request a quick refund by filing IRS Form 4466 (see the full Instructions for Form 4466).

Quick refunds have become a common mechanism for corporations purchasing tax credits to more quickly realize the benefit of their investment in the event that they overpaid their estimated tax.

Quick refunds accelerate cash recovery from tax credit purchases

If a corporation has overpaid estimated tax due to a tax credit transaction in their current tax year, the quick refund returns the overpayment much faster than the conventional refund process. This allows the corporation to more quickly realize the benefit of their investment.

Benefits are particularly pronounced for corporations who purchase credits in the months immediately preceding or following the close of their tax year. As a quick refund can only be requested after the end of a given tax year (see §6425(a)(1)), corporations purchasing tax credits in the months surrounding the end of their tax year may more quickly request and receive a quick refund.

A quick refund, however, yields benefits for any corporation that has overpaid their estimated tax, regardless of the timing of their tax credit purchase.

Eligibility depends on the size of the estimated tax overpayment

Corporations that have overpaid their estimated income tax in the current tax year are eligible for a quick refund under Form 4466. Take a company that has an estimated 2025 tax liability of $100M, which it pays in quarterly estimated tax payments of $25M each. Let’s assume that the company purchases $40M of tax credits, reducing their estimated tax liability to $60M.

- After their Q3 estimated payment date, they will have paid $75M in estimated taxes, which is an overpayment of $15M

- After their Q4 estimated payment date, they will have paid $100M in estimated taxes, which is an overpayment of $40M

If the corporation is in an overpayment position, they can file for a quick refund using Form 4466. To qualify, the overpayment must be:

- Greater than 10% of expected tax liability for the year AND

- Greater than $500

Form 4466 must be filed shortly after year-end

Corporations must apply for a quick refund after the end of their tax year (e.g., December 31 for calendar-year tax filers) but before the 15th day of the fourth month thereafter and their income tax return filing (Form 1120) for that year. Thus, a calendar-year filer would submit Form 4466 between January 1st and April 15th.

Form 4466 instructions state, “An extension of time to file the corporation’s tax return will not extend the time for filing Form 4466”, so corporations must file Form 4466 before their non-extended tax filing deadline, even if they extend. In other words, a corporation with a December year-end that extends their tax return filing date must still submit Form 4466 before April 15th. Practically speaking, corporations should file a quick refund request as soon as possible after their tax year-end to maximize cashflow benefit.

The corporation must also file a copy of the previously filed Form 4466 with its income tax return.

Refunds are typically issued within 45 days

The IRS is required to process a Form 4466 request within 45 days. The IRS may review elements of the filing, so corporations should be prepared to provide any requested information promptly to avoid delays in receiving the refund.

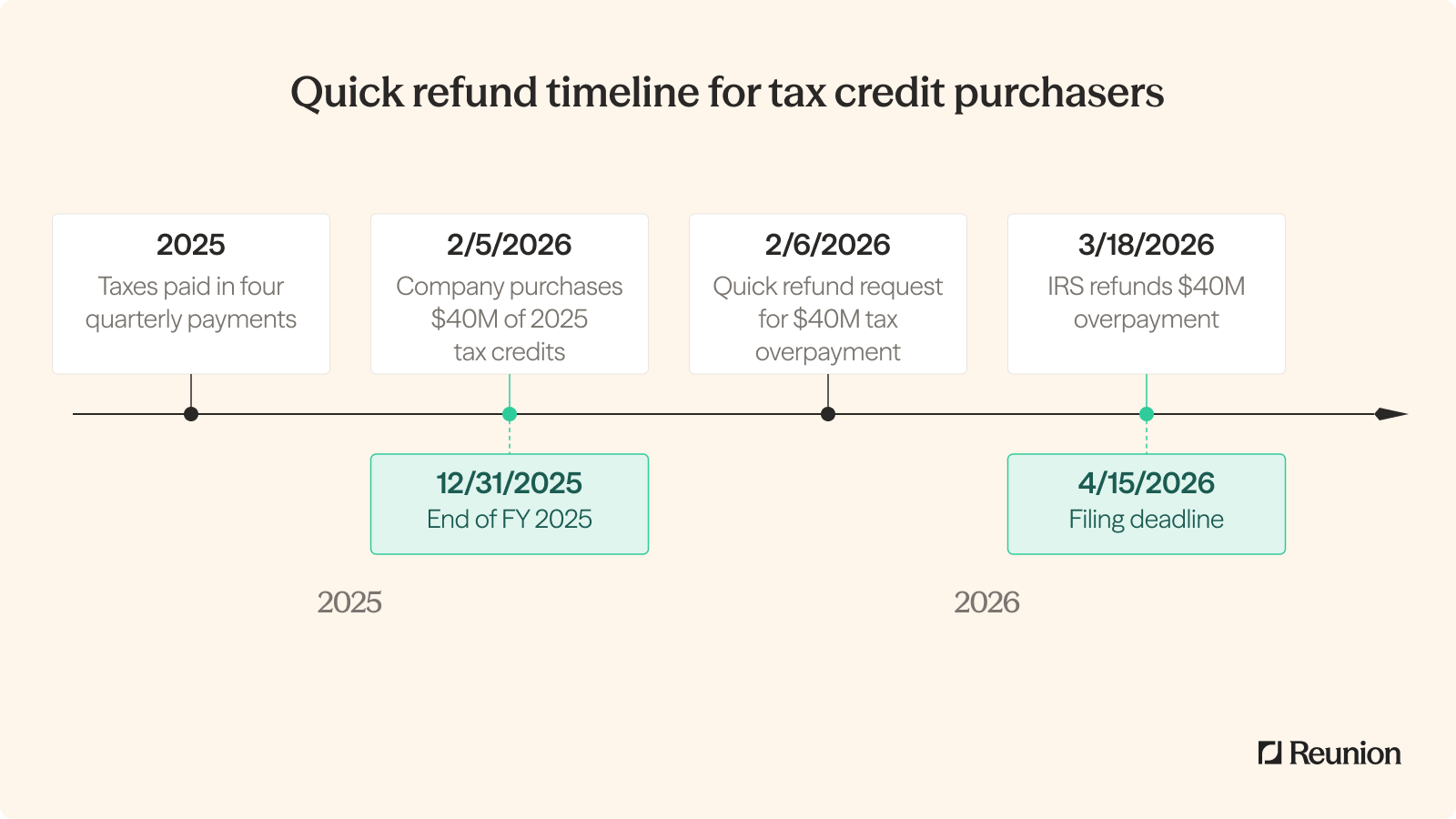

Here is a sample quick refund timeline for a calendar-year filer with a filing deadline of 4/15/26:

- The company has a 2025 estimated tax liability of $100M, which it already paid in four quarterly payments of $25M

- The corporation purchases $40M of Section 48 ITCs on 2/5/2026 for $36M. The corporation has now overpaid their 2024 taxes by $40M.

- The corporation submits Form 4466 on 2/6/2026, requesting a quick refund of their $40M overpayment

- The corporation receives $40M from the IRS on 3/18/2026, realizing their cash savings of $4M