Guide For Energy Community Tax Credit Bonus and Eligibility

Explore the latest IRS guidance, eligibility criteria and categories for energy community tax credit bonus. Maximize your clean energy project tax credits.

The latest energy community guidance, which meaningfully expanded the number of qualifying areas, placed the 10% adder back in the spotlight for the transferable tax credit marketplace. At the same time, Reunion has observed a marked increase in the number of projects in our marketplace claiming the energy community bonus.

While our transferable tax credit handbook goes deep on energy communities, we wanted to share a comprehensive (and refreshed) look at the adder.

Our guide begins with the basics, so we invite you to jump ahead.

- Background and scope

- Credit and project eligibility

- Diligence

- Guidance

- Annual updates to areas qualifying as energy communities

- Resources

Background And Scope

The Inflation Reduction Act created three bonus credits, or "adders"

The Inflation Reduction Act (IRA) created three "bonus" credits that can increase the value of a clean energy project's transferable tax credits:

- Domestic content: 10% bonus

- Energy community: 10% bonus

- Low-income community: 10% or 20% bonus

The energy community adder provides a 10% bonus credit

The energy community bonus provides a 10% increase to a project's credit value if the underlying project is located in an energy community (and meets prevailing wage and apprenticeship requirements).

A utility-scale solar project, for instance, that meets PWA requirements would receive tax credits worth 30% of its eligible cost basis. If the same project is located in an energy community, it would receive tax credits worth 40% of its eligible basis.

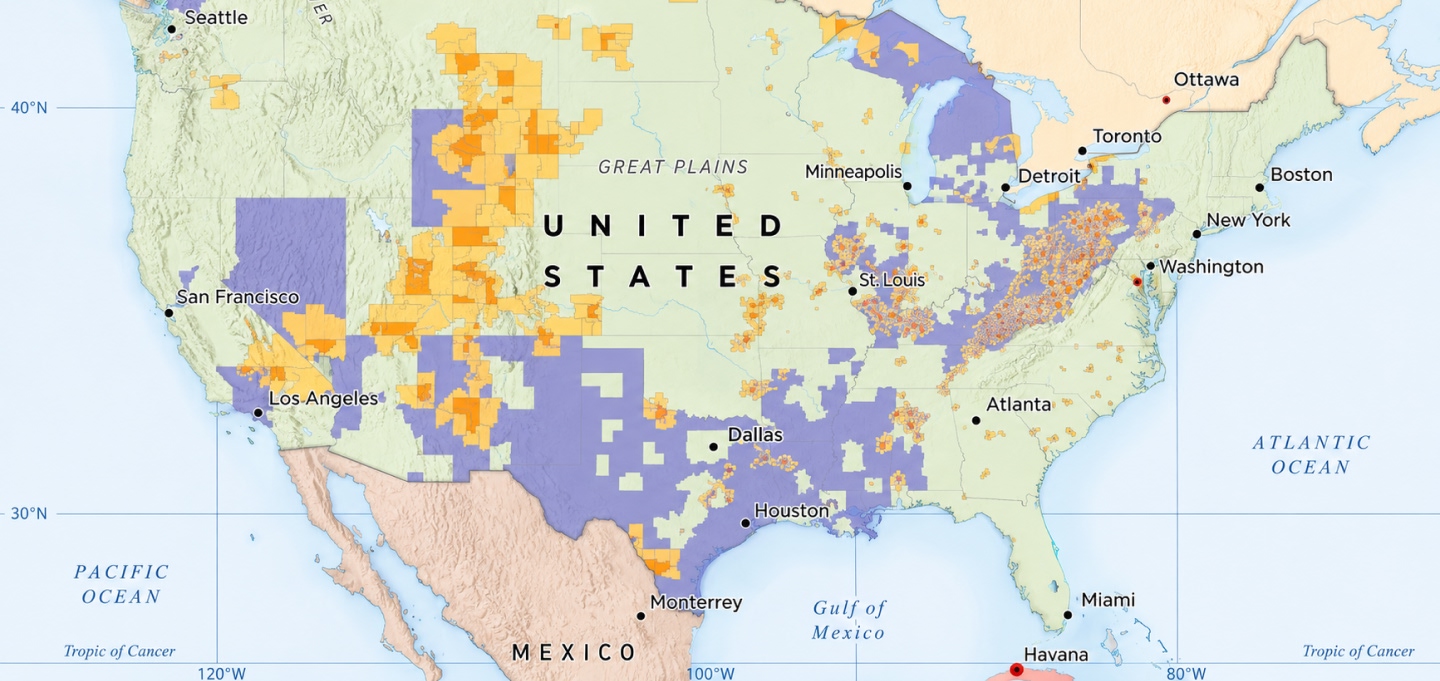

The IRA defines three types of energy communities

To qualify for the energy community bonus, a project must be located in at least one of three energy community "categories."

Category 1: Brownfield

A brownfield site is defined in 42 U.S.C. § 9601(39)(A) as "real property, the expansion, redevelopment, or reuse of which may be complicated by the presence or potential presence of a hazardous substance, pollutant, or contaminant" (as defined under 42 U.S.C. § 9601), and includes certain "mine-scarred land" (as defined in 42 U.S.C. § 9601(39)(D)(ii)(III)). A Brownfield site does not include the categories of property described in 42 U.S.C. § 9601(39)(B).

Three types of sites qualify as a brownfield under a safe harbor:

- Existing brownfield: Brownfields that are already tracked by a federal, state, territorial, or federally-recognized Indian tribal brownfields program. Many states, like Idaho and New York, have their own brownfields programs with supporting maps. A valid brownfield site could be tracked by a state program but not a federal program, and vice versa

- Phase II assessment: A Phase II Assessment has been completed with respect to the site and such Phase II Assessment confirms the presence on the site of a hazardous substance as defined under 42 U.S.C. § 9601(14), or a pollutant or contaminant as defined under 42 U.S.C. § 9601(33)

- Phase 1 assessment (for projects with a nameplate capacity of not greater than 5MWac): A Phase I Assessment has been completed with respect to the site and such Phase I Assessment identifies the presence or potential presence on the site of a hazardous substance, or a pollutant or contaminant.

Category 2: Coal closure

A census tract (or directly adjoining census tract):

- in which a coal mine has closed after 1999; or

- in which a coal-fired electric generating unit has been retired after 2009

Category 3: Statistical area

A "metropolitan statistical area" (MSA) or "non-metropolitan statistical area" (non-MSA) that has (or had at any time after 2009):

- 0.17% or greater direct employment or 25% or greater local tax revenues related to the extraction, processing, transport, or storage of coal, oil, or natural gas; and

- has an unemployment rate or above the national average unemployment rate for the previous year

The scope of "direct employment" is determined by ten NAICS codes.

Fossil fuel employment rate NAICS codes

| No. | 2017 NAICS Code | Definition |

|---|---|---|

| 1 | 211 | Oil and gas extraction |

| 2 | 2121 | Coal mining |

| 3 | 213111 | Drilling oil and gas wells |

| 4 | 213112 | Support activities for oil and gas operations |

| 5 | 213113 | Support activities for coal mining |

| 6 | 2212 | Natural gas distribution |

| 7 | 23712 | Oil and gas pipeline and related structures construction |

| 8 | 32411 | Petroleum refineries |

| 9 | 4861 | Pipeline transportation of crude oil |

| 10 | 4862 | Pipeline transportation of natural gas |

No double bonus for multiple energy communities

If a clean energy project is located in two energy communities – a brownfield site within a coal community, for instance – the bonus remains 10%. Developers cannot double up.

Bonus credits cannot be sold in stand-alone tranches

Bonus credits are not treated differently from base credits for the purpose of transferability. Treasury guidance released in June 2023 specified that all transferable credits must be sold as “vertical slices” and be pari passu to one another, as opposed to “horizontally” bifurcating bonus credits from base credits.

Credit And Project Eligibility

Four IRA credits are eligible for the energy community bonus

The IRA created 11 transferable tax credits, four of which are eligible for the energy community bonus:

- §45 PTC: Electricity produced from certain renewable resources

- §45Y PTC: Clean electricity production credit

- §48 ITC: Energy credit

- §48E ITC: Clean electricity investment credit

§48 and §48E ITC eligibility determined on placed-in-service date

For projects that claim an investment tax credit under §48 or §48E, eligibility for the energy community bonus credit is determined on the date that the project is placed in service (PIS) and is not tested again.

Because eligibility is determined on a PIS date that is subject to potential delays, developers should think carefully about how to incorporate the statistical area category into their financial assumptions.

The statistical area category is determined annually, based on the prior year's unemployment rate. As the IRS FAQs state, "Because an MSA's or non-MSA's status as an energy community depends on its unemployment rate for the previous year, an MSA or non-MSA that qualifies as an energy community in one period might not qualify as an energy community in a later period if its unemployment rate for the previous year falls below the national average."

§45 and §45Y PTC eligibility determined annually with a beginning-of-construction safe harbor

For projects that claim a production tax credit under §45 or §45Y, eligibility for the energy community bonus credit must be determined every year during the ten-year PTC period. Theoretically, a wind project could qualify one year under the statistical area category but not qualify the following year because of a change in employment rates.

However, the IRS created a safe harbor for PTC projects with beginning-of-construction dates on or after January 1, 2023. If the project owner determines that the project is eligible for the energy community bonus credit on the date construction is considered to have started for tax purposes, then the project will qualify for the bonus credit for the entire ten-year PTC period and is not tested again.

For insights on how the Energy Community Bonus Credit impacts a real-world transaction, refer to our Section 45 PTC transfer case study, which examines implications and lessons learned.

"Legacy" §45 PTCs are not eligible for energy community bonus

Projects that generate §45 PTCs that were placed in service before December 31, 2022 are not eligible for the energy community bonus, even if the project happens to be located in an energy community and is within its ten-year period of credit generation.

The December 31, 2022 date is set in the IRA itself (H.R.5376).

50% of a project's nameplate capacity (or square footage) must be in an energy community

A project qualifies for the energy community bonus if at least half (50%) of its nameplate capacity is in an energy community. According to the IRS, nameplate capacity is the DC capacity that a project is capable of producing on a steady-state basis during continuous operation under standard conditions.

For battery storage projects, at least half (50%) of the storage capacity, as measured in megawatt hours, should be in an energy community.

Lastly, for projects that do not generate nor store energy, like biogas, the 50% threshold is measured on a square footage basis.

Diligence

When performing due diligence on the energy community bonus, it's helpful to approach the process based on the credit type and energy community category.

Credit type

ITCs

Tax credit buyers should request documentation that demonstrates when and where the project was placed in service. Then, buyers and their advisors should crosswalk that location to an appropriate energy community siting resource, like one of the IRS's appendices. (We provide links to these appendices in the guidance section of this post.)

When validating a project's location, it's important to keep the "50%" rule in mind.

PTCs

Due diligencing the energy community bonus for PTCs is effectively the same as ITCs, although buyers will want to validate when and where the project began construction (versus when and where the project was placed in service). Once again, it's important to keep the "50%" rule in mind.

Energy community category

As far as each category is concerned, the statistical area and coal closure categories are relatively straightforward from a due diligence standpoint: the IRS has published lists of areas that qualify for each. The brownfield category, however, may present a slightly more nuanced due diligence process.

Statistical area

It's important to recall that the statistical area category changes every year, based on the prior year's unemployment rate. As we'll discuss below, the IRS is obligated to publish updates to this category every year, generally in May.

Coal closure

Unlike the statistical area category, the coal closure category cannot shrink – that is, once an area qualifies as a coal closure, it remains as such for the duration of the energy community bonus.

However, the coal closure category can expand, and we fully expect it to do so. According to a 2022 analysis by the Energy Information Agency (EIA), nearly a quarter of the operating U.S. coal-fired fleet is scheduled to retire by 2029. Every closure will add more census tracts to the list of areas eligible for the energy community bonus.

Brownfield

The IRS has not published – and, as far as we know, has no plans to publish – a consolidated list of areas that qualify as brownfields for purposes of the energy community bonus. In fact, the DOE energy community map doesn't even include federally-recognized brownfield sites. (The EPA, however, maintains a list of federally-recognized brownfields in its cleanups in my community map.)

We doubt the IRS or any federal agency will publish a definitive list of brownfields. There are simply too many moving parts across federal, state, local, and tribal brownfields programs.

So, an opinion from an environmental attorney may be warranted, and the scope of the opinion will vary based on which of the three brownfields safe harbors a project is claiming.

Guidance

Latest guidance expands the number of areas that are eligible for the energy community bonus

The most recent IRS guidance, Notice 2024-30, broadened eligibility for the energy community bonus through two key changes:

- Expansion of the "nameplate capacity attribution rule"

- Inclusion of two additional NAICS codes – which are in our list above – for determining the fossil fuel employment rate for a statistical area category

Expansion of the nameplate capacity attribution rule

The "nameplate capacity attribution rule" pertains to projects with offshore generation – namely, offshore wind – that have a nameplate capacity but are not located within a census tract, an MSA, or a non-MSA. The rule, essentially, allows developers to allocate their offshore nameplate capacity onshore for purposes of qualifying for the energy community bonus.

Prior to Notice 2024-30, the attribution rule generally allowed offshore wind projects to qualify for the energy community bonus if their power-conditioning equipment closest to the point of interconnection was in an energy community.

Notice 2024-30 expanded the nameplate capacity attribution rule to include not only power-conditioning equipment, but also supervisory control and data acquisition (SCADA) equipment.

SCADA equipment must be owned by the developer and located in an "energy community project port." To qualify as an energy community project port, a port must:

- Be used "either full or part-time to facilitate maritime operations necessary for the installation or operation and maintenance" of the project

- Have a "significant long-term relationship" with the project, meaning the developer owns or leases all or part of the port for a minimum term of ten years

- Be the location at which staff employed by, or working as independent contractors for, the project are based and perform functions essential to the project's operations. Essential functions include "management of marine operations, inventory and handling of spare parts and consumables, and berthing and dispatch of operation and maintenance vessels and associated crews and technicians"

Inclusion of two additional NAICS codes

Notice 2024-30 added two additional NAICS codes for determining the fossil fuel employment rate for a statistical area category:

- 2212: Natural gas distribution

- 23712: Oil and gas and pipeline and related structures construction

These NAICS codes cover workers in local gas distribution companies and construction workers on oil and gas pipelines.

According to Norton Rose Fulbright, "The biggest additions to the list of potentially eligible counties are in six Midwestern states: Minnesota (57), Missouri (57), Illinois (28), North Dakota (23), Wisconsin (23) and Indiana (20)."

The IRS has released five pieces of energy community guidance, with regulations to come soon

Energy community regulations should arrive by June 30, 2024

As Notice 2024-30 notes, proposed regulations are forthcoming. Until then, "taxpayers may rely on the rules described in sections 3 through 6 of Notice 2023-29, as previously clarified by Notice 2023-45 and modified by section 3 [of] this notice, for taxable years ending after April 4, 2023."

Based on the Q2 update to the IRS 2023-2024 Priority Guidance Plan, energy community regulations should arrive before the end of the current "plan year," which concludes on June 30, 2024.

Where to find the latest guidance

The IRS and Treasury maintain lists of IRA-related guidance, including guidance specific to the energy community adder. Although the lists generally overlap, there may be differences based on when each website was last updated.

Below is a close look at all the guidance that's been released through March 2024.

Notice 2022-51: Request for Comments on Prevailing Wage, Apprenticeship, Domestic Content, and Energy Communities Requirements under the Inflation Reduction Act of 2022

- Date: October 5, 2022

- News release: IRS

- Companion documents: N/A

Notice 2023-29: Energy Community Bonus Credit Amounts under the Inflation Reduction Act of 2022

- Date: April 4, 2023

- News release: IRS

- Companion documents: Appendix A, Appendix B, Appendix C

Notice 2023-45: Energy Community Bonus Credit Amounts under the Inflation Reduction Act of 2022

Notice 2023-47: Energy Community Bonus Credit Amounts or Rates (Annual Statistical Area Category Update and Coal Closure Category Update)

- Date: June 15, 2023

- News release: IRS

- Companion documents: Appendix 1, Appendix 2, Appendix 3

Notice 2024-30: Energy Community Bonus Credit Amounts under the Inflation Reduction Act of 2022

- Date: March 22, 2024

- News release: IRS

- Companion documents: Appendix 1, Appendix 2

Annual Updates To Areas Qualifying As Energy Communities

Expect energy community eligibility updates every May, beginning in 2024

According to Notice 2023-29, "The Treasury Department and the IRS intend to update the listing of the Statistical Area Category based on Fossil Fuel Employment annually. These updates generally will be issued annually in May."

The first update should arrive in May 2024 – that is, next month.

Resources from administering federal agencies

DOE, EPA, and IRS have provided energy community eligibility and project siting resources

U.S. federal agencies who are responsible for administering or managing parts of the energy community bonus credit have published several key resources that are valuable to buyers, sellers, and their advisors:

- Department of Energy (DOE): Energy community map

- IRS: Frequently asked questions

- DOE National Energy Technology Laboratory (NETL): Frequently asked questions

- Environmental Protection Agency (EPA): RE-powering America's land initiative

- EPA: Cleanups in my community

- Interagency working group: Energy community tax credit bonus

Learn More

To learn more, you can download our 100-page transferable tax credit handbook or start a conversation with our transactions team.