What Companies Facing BEAT Need to Know Before Buying Tax Credits

Certain transferable tax credits provide more economic benefit to companies that are potentially subject to BEAT.

In the realm of energy tax credits, special rules apply to U.S. companies that are subject to the corporate minimum tax known as BEAT, or the Base Erosion and Anti-Abuse Tax.

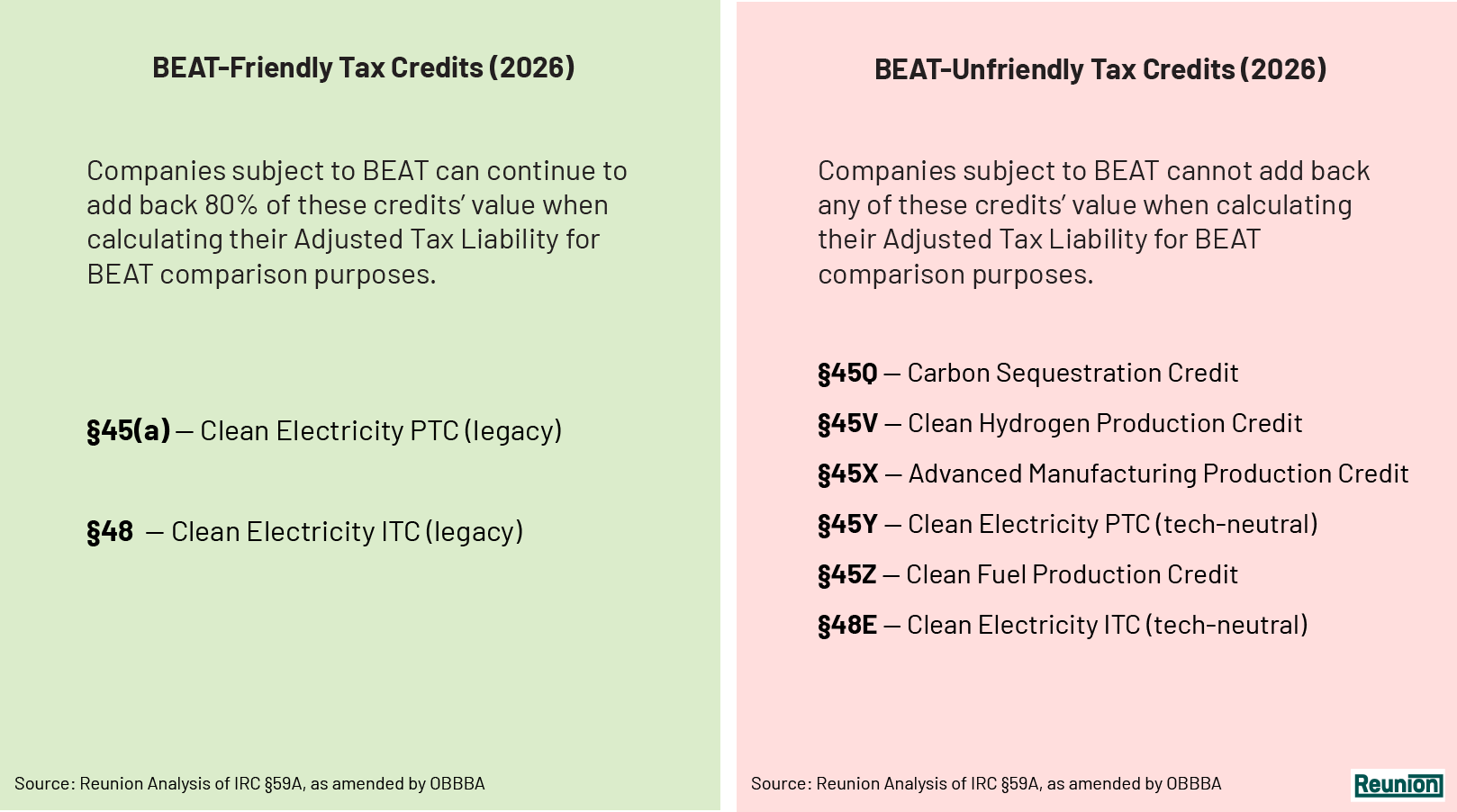

Certain credits, namely "legacy" §45(a) production tax credits and §48 investment tax credits, are treated favorably under BEAT, whereby 80% of the credit value can be “added back” when calculating BEAT. Other energy credit types, including §45Y, §48E, §45Q and §45Z credits, are not treated favorably when calculating BEAT.

There is some debate as to whether other credit types were intentionally excluded from favorable treatment. However, the current statute indicates that only §45 and §48 credits are treated favorably for BEAT taxpayers.

What is BEAT? Who is subject to it?

The Base Erosion and Anti-Abuse Tax (BEAT) was enacted as part of the 2017 Tax Cuts and Jobs Act (TCJA) to prevent large multinational corporations from eroding their U.S. tax base by shifting profits to foreign affiliates.

BEAT applies to any corporation that meets two criteria:

- Revenue threshold: Average annual gross receipts of at least $500 million over the preceding three years (measured at the consolidated global level, including foreign affiliates).

- Base erosion percentage: At least 3% of total deductions come from payments to related foreign parties — such as royalties, interest, services fees, or depreciation on transferred assets. The threshold is 2% for banks and registered securities dealers.

Companies that meet both thresholds must calculate their BEAT liability every year. BEAT functions as a minimum tax: if a company's regular tax liability falls below the calculated BEAT level, then the company must pay the difference as a top-up.

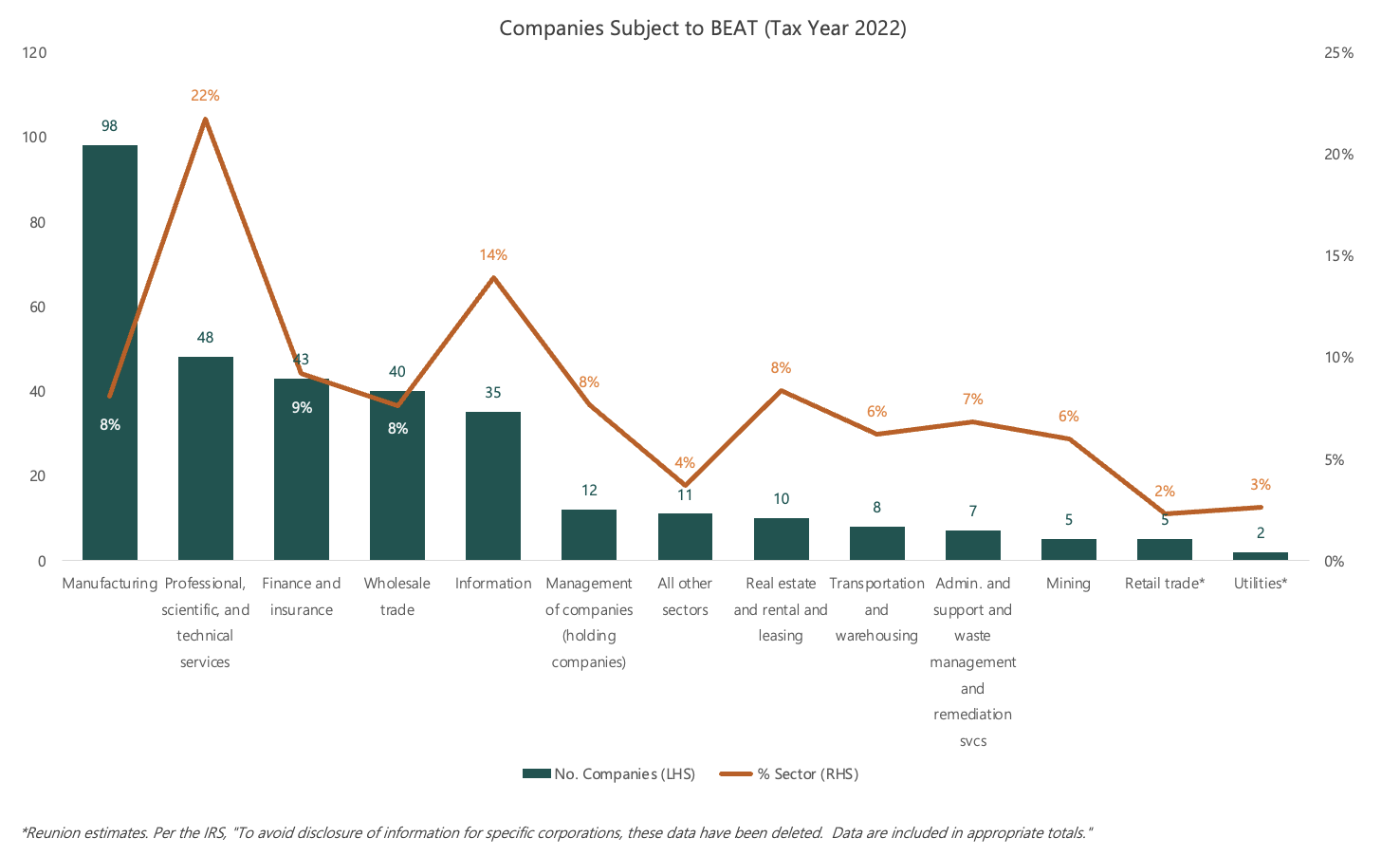

The IRS’ most recent available data about BEAT is for the 2022 tax year. That year, there were 324 companies that owed BEAT – and had to “top-up” their regular tax liability.

Explaining the BEAT Calculation through Key Terms

The following key terms help explain how BEAT is calculated:

- Base Erosion Payments: Tax-deductible payments made by a U.S. corporation to a related foreign affiliate. These payments are often used by multinational companies to shift profits out of the U.S., lowering their tax bill

- Regular Taxable Income: A company’s income, minus all eligible deductions (includes deductible Base Erosion Payments).

- Regular Tax Liability: A company’s Regular Taxable Income times the statutory 21% corporate tax rate.

- Regular Tax Liability After Credits: A company’s Regular Tax Liability minus the full value of credits.

- Modified Taxable Income: MTI is the sum of Regular Taxable Income and an add-back of deductions associated with Base Erosion Payments to foreign-related parties.

- Preliminary BEAT: Modified Taxable Income x BEAT Tax Rate (10.5% in 2026 and subsequent years).

- Adjusted Tax Liability: Used for BEAT calculation purposes, an adjustment that takes “Regular Tax Liability After Credits,” then adds back 80% of the value of eligible credits.

- BEAT Payment Due: If the company’s preliminary BEAT is larger than its Adjusted Tax Liability, then the difference is the BEAT Payment Due. If the Adjusted Tax Liability is equal to or greater than the preliminary BEAT, then the company’s BEAT Payment Due is zero.

Now, let’s explore which specific tax credits still qualify for the add-back in 2026 and beyond.

How the OBBBA Protected Credits for Taxpayers Subject to BEAT

The One Big Beautiful Budget Act (OBBBA) introduced two adjustments that were advantageous in the context of BEAT and tax credits:

- Set the permanent BEAT rate at 10.5%: Prior to the OBBBA, the BEAT rate was projected to increase to 12.5%, which would have increased the number of companies impacted by BEAT.

- Made the tax credit add-back permanent: Since 2017, companies have been able to add back 80% of the value of certain tax credits to their Regular Tax Liability, to arrive at their Adjusted Tax Liability. The OBBBA made the add-back permanent, preserving the value of credits for BEAT taxpayers.

BEAT-Friendly vs. BEAT-Unfriendly Credits

The OBBBA's add-back provision is narrowly defined. Under the amended §59A, "Applicable Section 38 Credits" eligible for the 80% add-back are limited to:

- The renewable electricity production credit determined under section 45(a)

- The investment credit determined under section 46, but only to the extent properly allocable to the energy credit determined under section 48

The low-income housing credit determined under section 42(a), which is not a transferable tax credit, is also eligible for the 80% add-back.

However, the list does not include other credit types, such as the technology-neutral §45Y and §48E credits. The table below summarizes the BEAT treatment of the most commonly traded transferable credits.

Three Numerical Examples of BEAT

The following examples help illustrate how credit selection changes the outcome when BEAT is in play.

Let’s assume that the company has the following characteristics:

- $600M in Taxable Income

- $20M in deductions not attributable to Base Erosion Payments

- $80M in Base Erosion Payments to foreign affiliates

- Regular Taxable Income of $500M ($600M - $20M - $80M)

- Regular Tax Liability Before Credits, of $105M (21% x $500M)

- MTI of $580M ($500M + $80M)

- Preliminary BEAT of $60.9M (10.5% x $580M)

Example 1: No tax credit purchases

Based on the assumptions above, the Regular Tax Liability Before Credits is $105M, and the Preliminary BEAT calculation is $60.9M. Because $60.9M is less than $105M, there is no requirement to pay BEAT top-up tax.

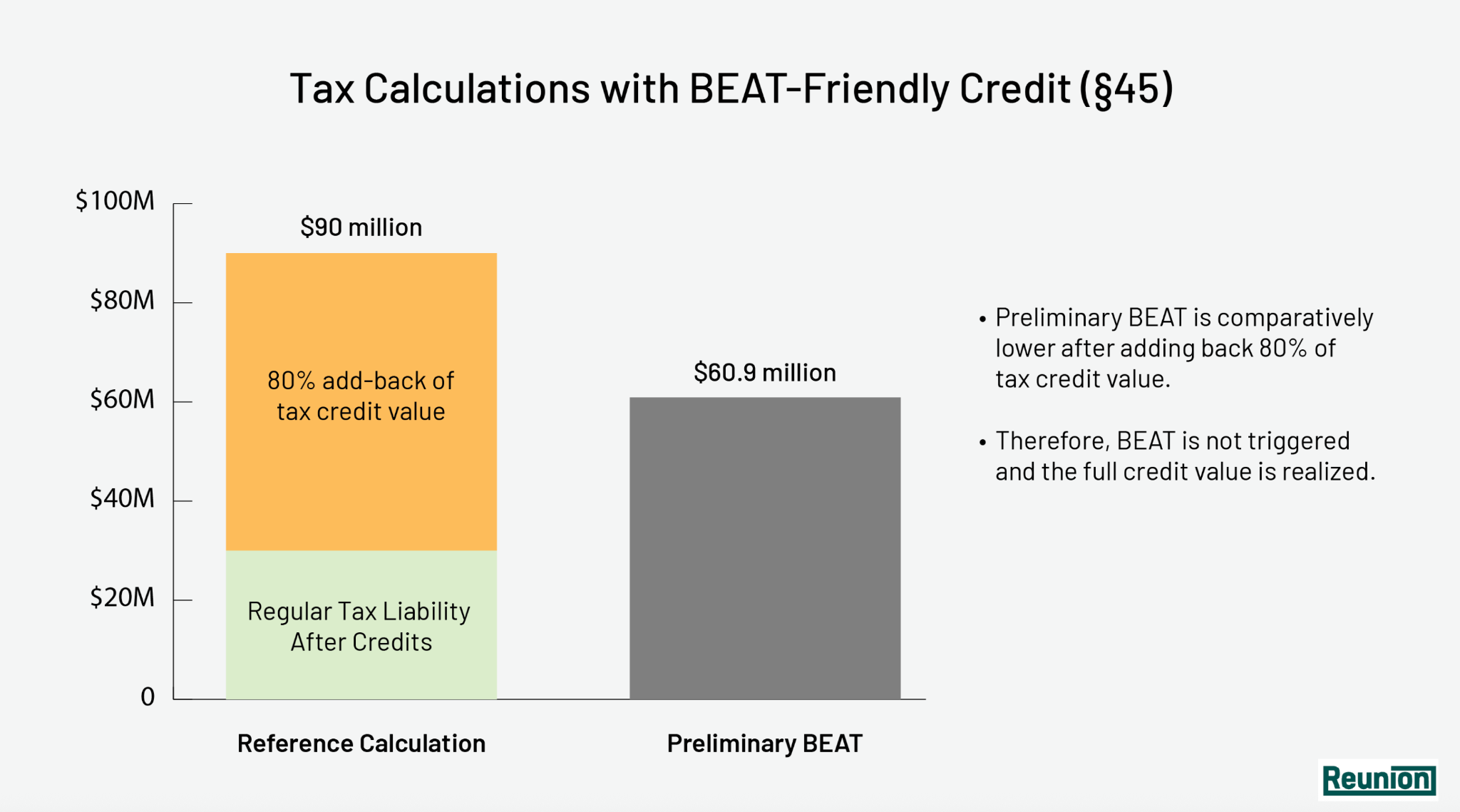

Example 2: Purchase $75M in §45(a) PTCs — BEAT-Friendly

This time, the company purchases $75M in §45(a) legacy PTCs. Since this is a BEAT-friendly credit, the company can retain 80% of the credit in their calculation of Adjusted Tax Liability.

Regular Tax Liability Before Credits is $105M.

Regular Tax Liability after Credits is $30M.

Adjusted Tax Liability is $90M, which is calculated by adding back 80% of the credit’s value ($60M, which is 80% of $75M) to Regular Tax Liability after Credits ($30M).

Adjusted Tax Liability ($90M) exceeds the Preliminary BEAT floor ($60.9M). Therefore, the company avoids BEAT and realizes the full $75M value of the tax credit. Their final tax liability is the Regular Tax Liability after Credits, or $30M.

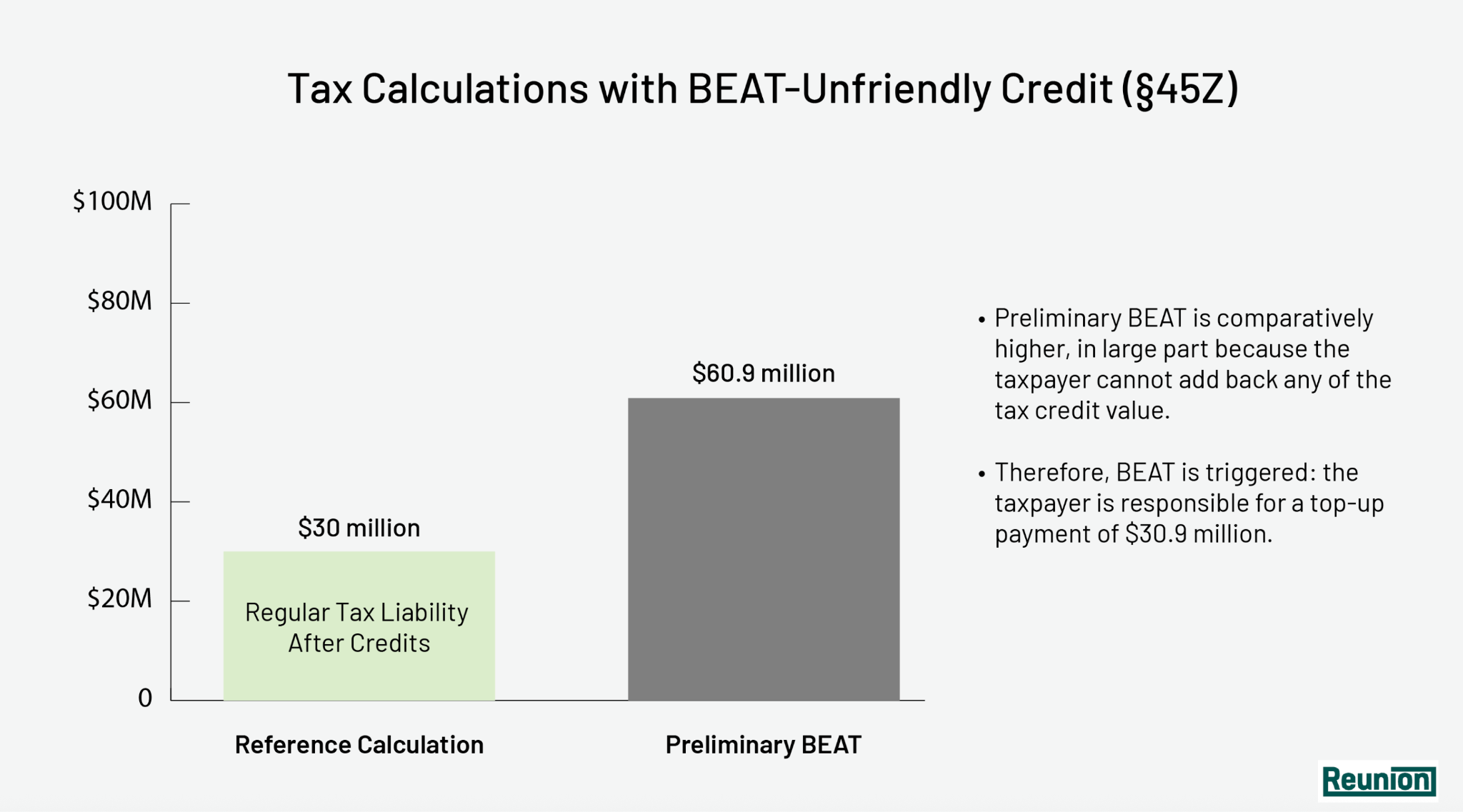

Example 3: Purchase $75M in §45Z PTCs — BEAT-Unfriendly

This time, the company purchases $75M in §45Z in Clean Fuel Credits. Unfortunately, since this is not a BEAT-friendly credit, the company cannot add back any of the credit in their calculation of Adjusted Tax Liability.

Regular Tax Liability before Credits is $105M.

Regular Tax Liability after Credits is $30M.

Adjusted Tax Liability is also $30M, since credits cannot be added back.

Adjusted Tax Liability falls below the Preliminary BEAT of $60.9M, so BEAT is triggered and a top-up payment is required of $30.9M (calculated by “topping up” the $30M Adjusted Tax Liability to reach the $60.9M Preliminary BEAT level).

Assume that the company paid $69M for the $75M transferable tax credit (a price of $0.92 per tax credit). The company only realized $44.1M ($75M - $30.9M) in tax savings for the current year, despite paying $69M.

Key Takeaways

BEAT-subject buyers should prioritize legacy §45(a) and §48 energy credits, which are treated favorably when calculating BEAT. The OBBBA preserved an 80% add-back for §45(a) and §48 credits only. Newer credits — §45Y, §48E, §45Z, §45Q, and others — do not benefit from this treatment.

Know your exposure before you transact. While only a few hundred companies may be subject to BEAT each year, many more approach thresholds that put them at risk. Companies with meaningful foreign affiliate payments should confirm their BEAT status before purchasing credits.

.png)