Unlocking the Economic Benefits of Tax Credits Before Cash Payment

Corporate taxpayers can buy tax credits in a way that preserves the timing of existing tax-related cashflows, or even improves corporate cash availability relative to the status quo.

Treasury’s June 2023 guidance made clear that corporate taxpayers can offset their quarterly estimated tax payments using tax credits they “intend to purchase,” opening the door for tax credit buyers to realize most or all of the benefit of a tax credit prior to paying the tax credit seller.

An increasing number of corporate tax directors and treasurers are focused on these types of opportunities, which do not require the buyers to go “out of pocket” to invest in a tax credit. Instead, the buyer pays a clean energy company a discounted amount compared to what they would have paid the IRS; the payment is concurrent with, or in some cases even after their scheduled tax payment date.

In this article, we outline four scenarios where buyers can realize tax benefits prior to cash outlay. We assume the buyer is a corporation that pays $200M each year in federal tax, and is looking to purchase $50 to $100M in tax credits.

Structures that enable buyers to realize full tax benefit prior to cash outlay

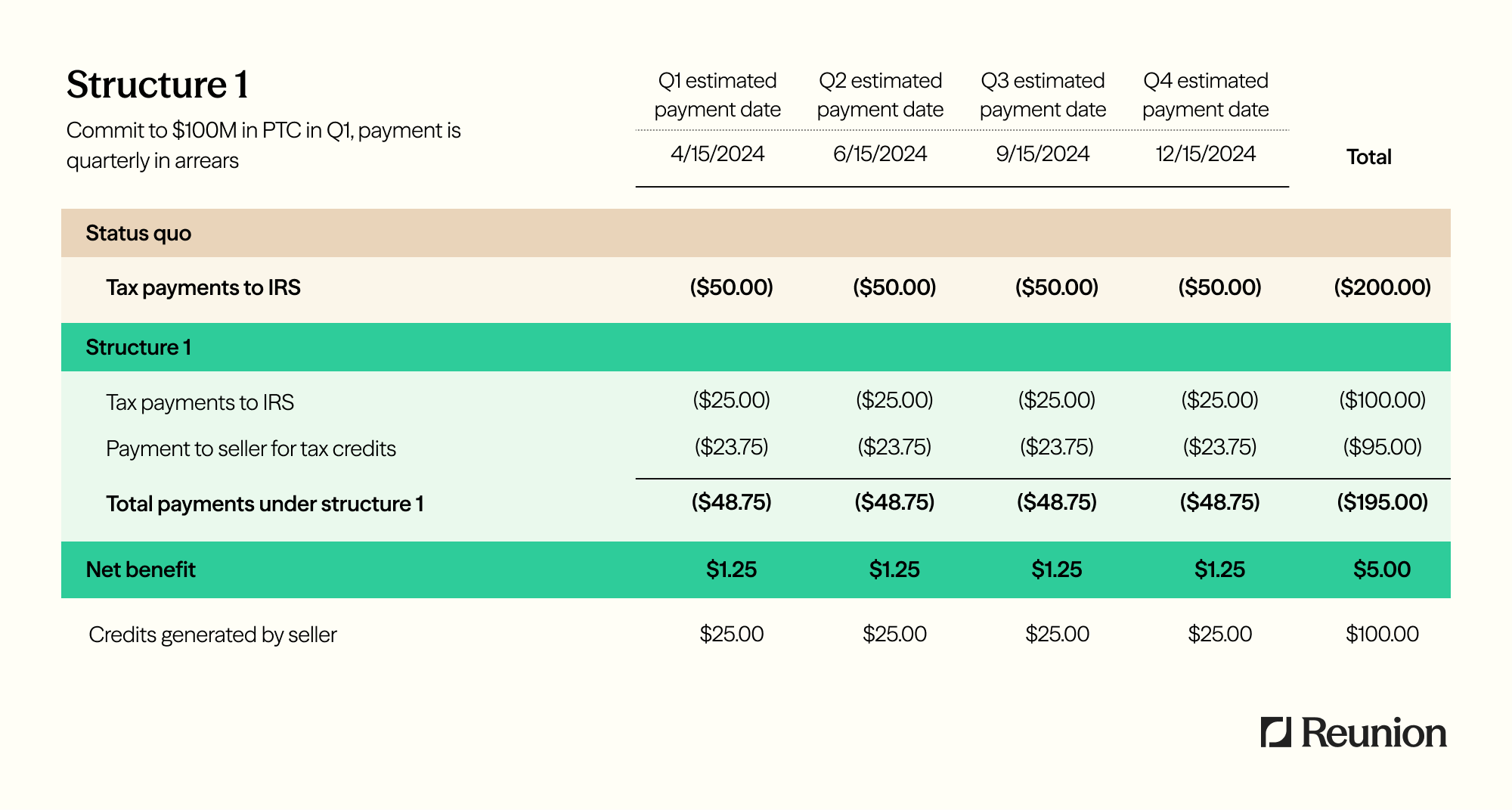

Structure 1: §45 PTCs, paid quarterly in arrears

The buyer commits to purchasing $100M in tax credits in Q1, which allows the buyer to offset $25M in tax payments each quarter. Note that if the buyer commits to purchase $100M in Q2 instead of Q1, there is a similarly strong benefit; the buyer can offset $50M in tax payments in Q2, and $25M in both Q3 and Q4.

§45 PTC transactions are typically paid quarterly in arrears. Often, the payment schedule is organized such that the buyer pays concurrently or shortly after each quarterly estimated tax payment date, based on actual tax credits generated during the preceding period. In this example, the buyer pays a clean energy developer $23.75M on each estimated tax payment date, instead of paying the IRS $25M. This results in a $1.25M net benefit each quarter, without any out-of-pocket investment.

For a real-world illustration of how this structure delivers value, see our Section 45 PTC transfer case study, which details transaction mechanics, cash flow timing, and buyer benefits.

Both §45 PTCs, from electricity generated by qualified renewable energy resources such as solar or wind, and §45X AMPCs from advanced manufacturing facilities, can be structured in this way.

Structure 2: §48 ITC portfolio, paid quarterly in arrears

A portfolio of ITCs can be structured similarly to the previous example, where the buyer pays quarterly in arrears (and is therefore able to utilize the full tax benefit prior to cash outlay).

In this example, the seller has a portfolio of rooftop solar projects that will be placed in service throughout the year, generating a total of $100M in tax credits. The seller is offering an 8% discount for the credits. The buyer commits to the tax credit purchase in Q1, and reduces their estimated tax payments by $25M each quarter.

The buyer will pay for the actual credits generated at the end of each preceding quarter. In this example, we assume that $20M in credits are generated in Q1 and Q2, while $30M is generated in Q3 and Q4. As a result, a relatively lower volume of credits need to be paid for in Q1 and Q2 (while the reduction in estimated tax payments remains fixed at $25M each quarter), resulting in a strong net benefit in Q1 and Q2. Overall, the buyer saves $8M in taxes over the course of the year, without any out of pocket investment.

There is a risk that the seller does not generate as many credits as anticipated in a given tax year; if so, a make-whole provision can be negotiated, which obligates the seller to make the buyer whole for any difference between what they agreed to pay for the credits and what they would have to reasonably pay for any replacement credits. In the event of a shortfall of credits, Reunion will also work with the buyer to source replacement credits.

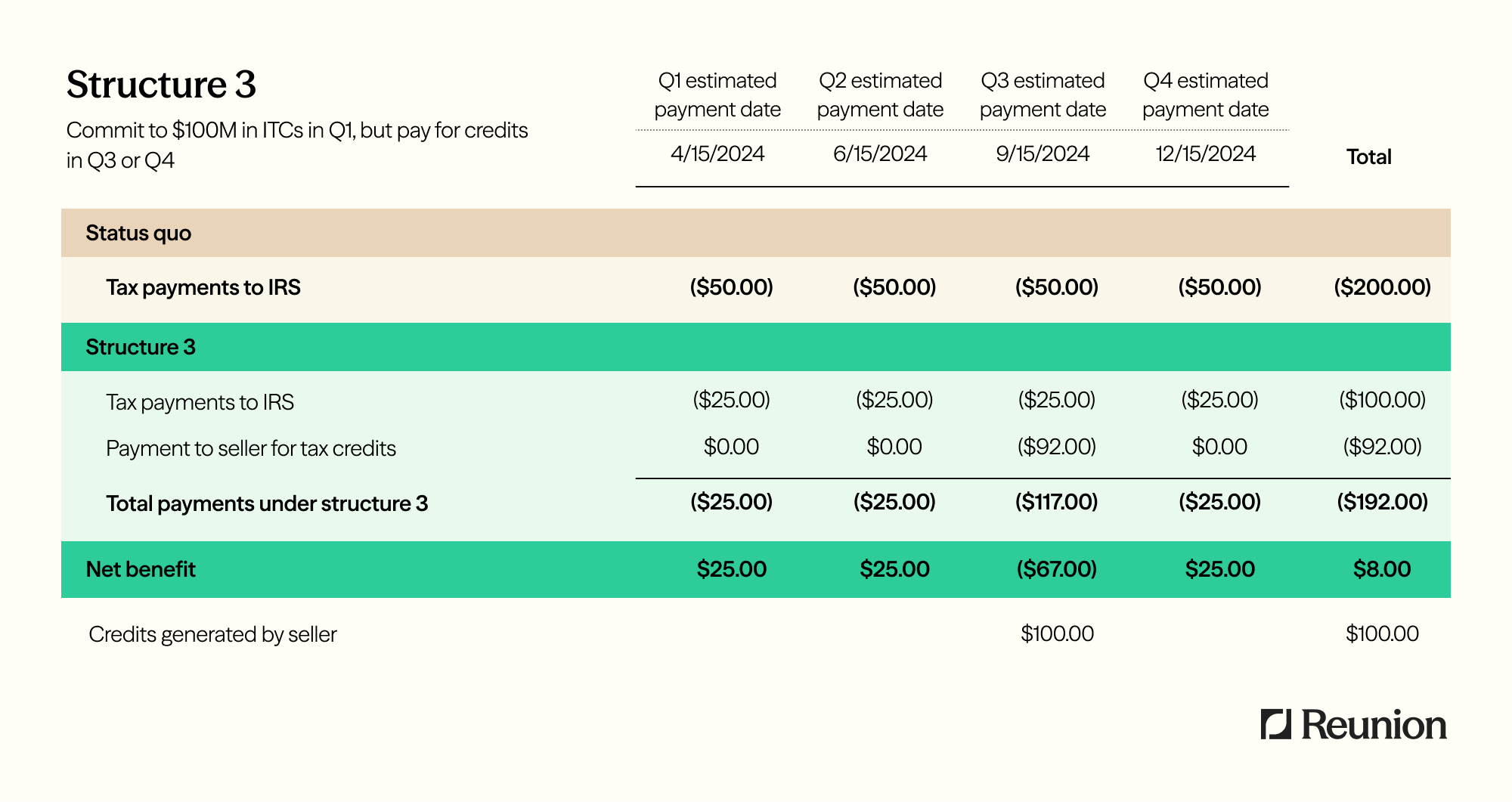

Structure 3: Commit to ITC early in the year, but pay late in the year

In this scenario, a buyer commits to purchasing ITCs that a developer will generate later in the year. While the IRS was clear that buyers can offset quarterly tax payments with tax credits they intend to purchase, it is up to buyers and their legal and tax advisors to decide what documentation is needed to establish intent.

Assume that the buyer and seller execute a tax credit transfer agreement in Q1, and the buyer uses this as a basis to start offsetting quarterly estimated tax payments. If the project is placed in service around or after the Q3 estimated tax payment date, the buyer will be able to offset taxes in Q1, Q2, and Q3 before having to pay the seller for the credits (see example below). This will free up $25M of additional cash each quarter for other corporate purposes, with the understanding that a lump sum will need to be paid to the tax credit seller at a later date.

Sellers typically prefer to receive payment as soon as the credits are generated, but it is possible to negotiate a delayed payment date. For example, if the payment date can be delayed to on or after the Q4 estimated payment date, the buyer will be able to take the full benefit of the tax credit before any cash outlay.

This strategy also applies if the buyer commits to the ITC in Q2 or Q3, and does not have to pay for the credit until later in the year.

Scenario 3 carries the risk that the project is not placed in service in 2024 tax year, which would require the buyer to source replacement credits. It is possible for the buyers to negotiate a make-whole provision, in the event that credits are not delivered as promised.

Structure 4: Buy tax credits to top up at the end of the year, resulting in a lower Q4 or final tax payment

The final scenario is a variation of Scenario 3. A company purchases tax credits at the end of the year, once they have a more concrete understanding of their total annual tax liability, and delays payment until their Q4 or final tax payment date.

Assume the buyer has paid $150M in taxes through the first 3 quarters, and has $50M due in taxes in Q4. The buyer can fully offset their remaining taxes due by committing to purchase $50M in credits in Q4. In this example, the buyer receives an 8% discount, paying $46M for the credits and achieving tax savings of $4M. The buyer can achieve the full benefit of the credit prior to cash outlay by arranging to pay the seller of the tax credit on or after the Q4 estimated tax payment date.

The same logic applies for credits purchased in time for the final tax filing (e.g., on April 15 for the prior tax year, for a calendar year filer). If a buyer has $20M in remaining payments due at final tax filing, they could offset the entire tax payment through purchase of a tax credit. Assuming they could identify and purchase a tax credit with an 8% discount, they would pay $18.4M to a tax credit seller, achieving $1.6M in tax savings. It is worth noting that if the buyer procures more than they end up owing in their final tax payment, the overpayment can be applied to the first estimated tax payment of the following year.

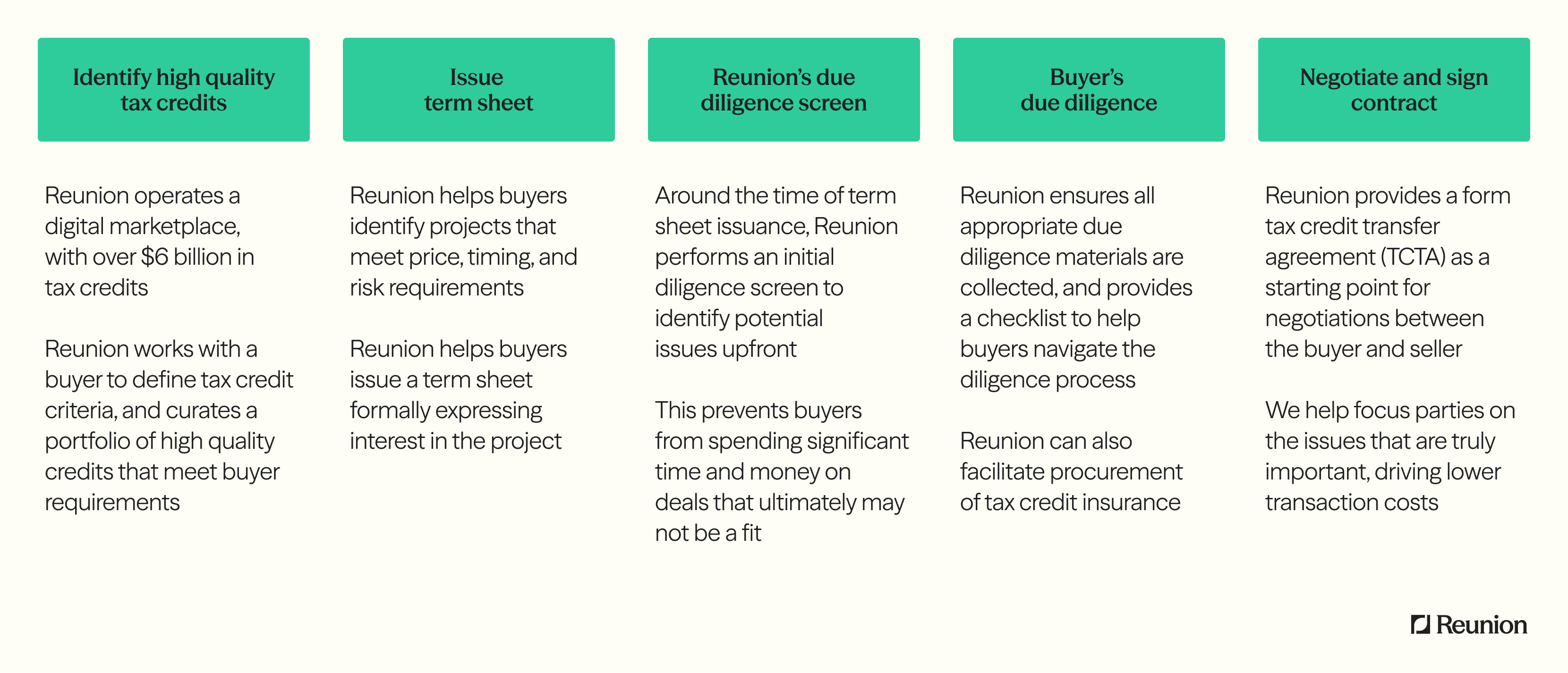

How Reunion works with corporate finance teams to purchase tax credits

Reunion partners with corporate tax and treasury teams to identify and purchase tax credits in a five-step process.

Customize these scenarios to your company

Tax credit buyers have a variety of objectives when choosing to purchase a tax credit. Some are focused on maximizing the amount they can save on taxes by looking for the largest discount, while others want to minimize complexity and risk.

We have observed an increasing number of corporate tax and treasury professionals who are focused on transactions that preserve the timing of existing tax-related cashflows, or even improve corporate cash availability relative to the status quo.

Please reach out to the Reunion team if you’d like to examine the cash flow impact of tax credit purchases in further detail, and hear about specific project opportunities that can be structured to maximize economic benefits prior to cash payment.