A New Kind of Club Deal: Efficiently Structuring a $30 Million §45Z Transaction

The mechanics of how a Clean Fuel Tax Credit transaction scaled up

In Q1 2026, Reunion facilitated a $30 million §45Z tax credit transfer among a major Midwest ethanol producer and two publicly traded banks.

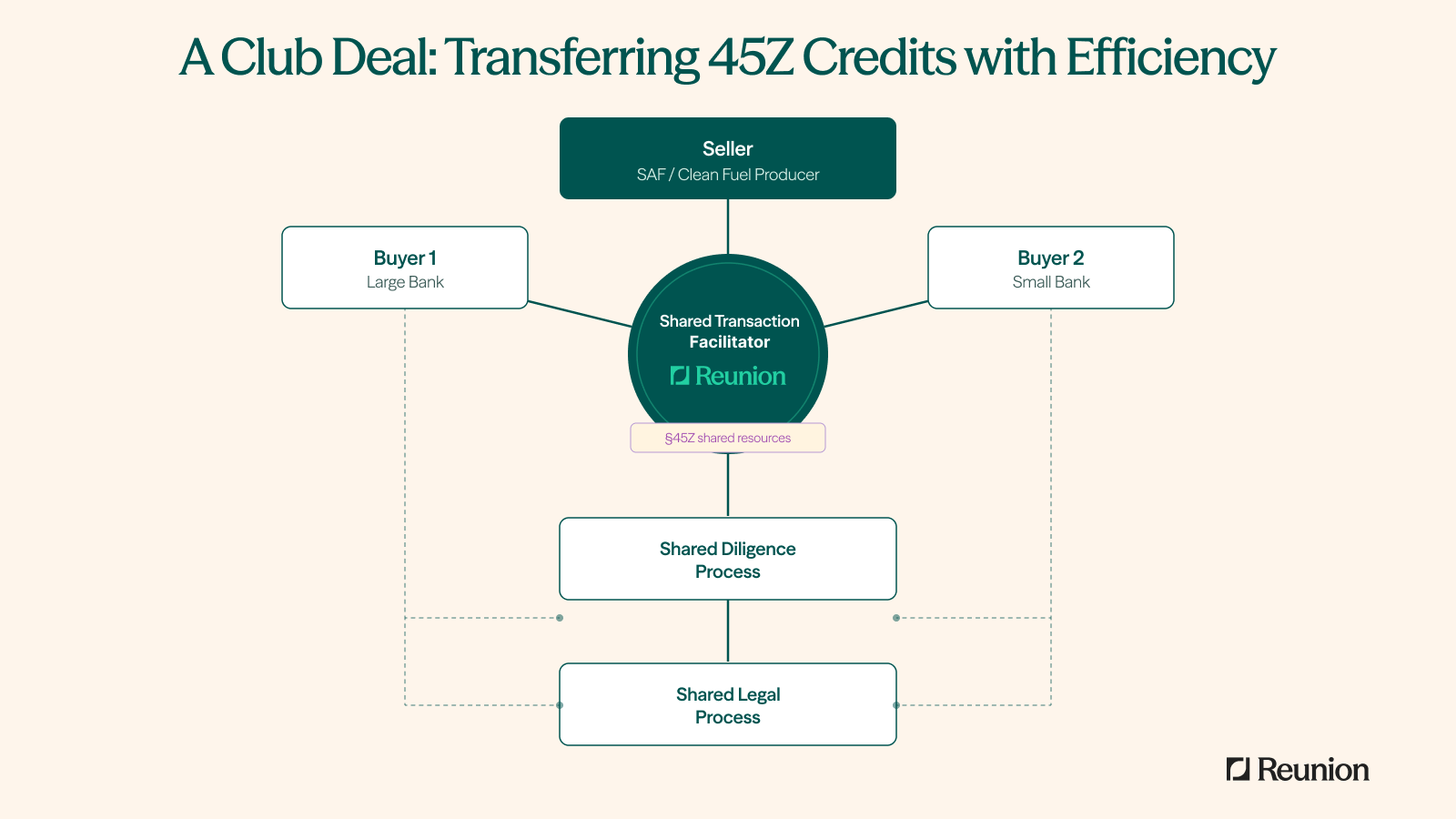

Reunion structured the transaction as a “club” deal, with the two buyers — while additional participants could have been included — aligning on negotiations, timing, due diligence, legal processes, and tax credit insurance requirements.

The deal offers insights not only into the mechanics and due diligence requirements of §45Z, but also how the club model can enable scale and efficiency.

The Credit

The §45Z PTC has become one of the most widely adopted credits to emerge from the Inflation Reduction Act. Available for transportation fuel produced domestically and sold between January 1, 2025 and December 31, 2029, the credit covers a range of low-carbon fuels such as ethanol, renewable natural gas, renewable diesel, and sustainable aviation fuel.

§45Z, like many production credits, is not subject to §50 recapture. This structural feature distinguishes it from §48 and §48E investment tax credits, which often trade at a deeper discount due to the need to diligence and protect against the risk of recapture.

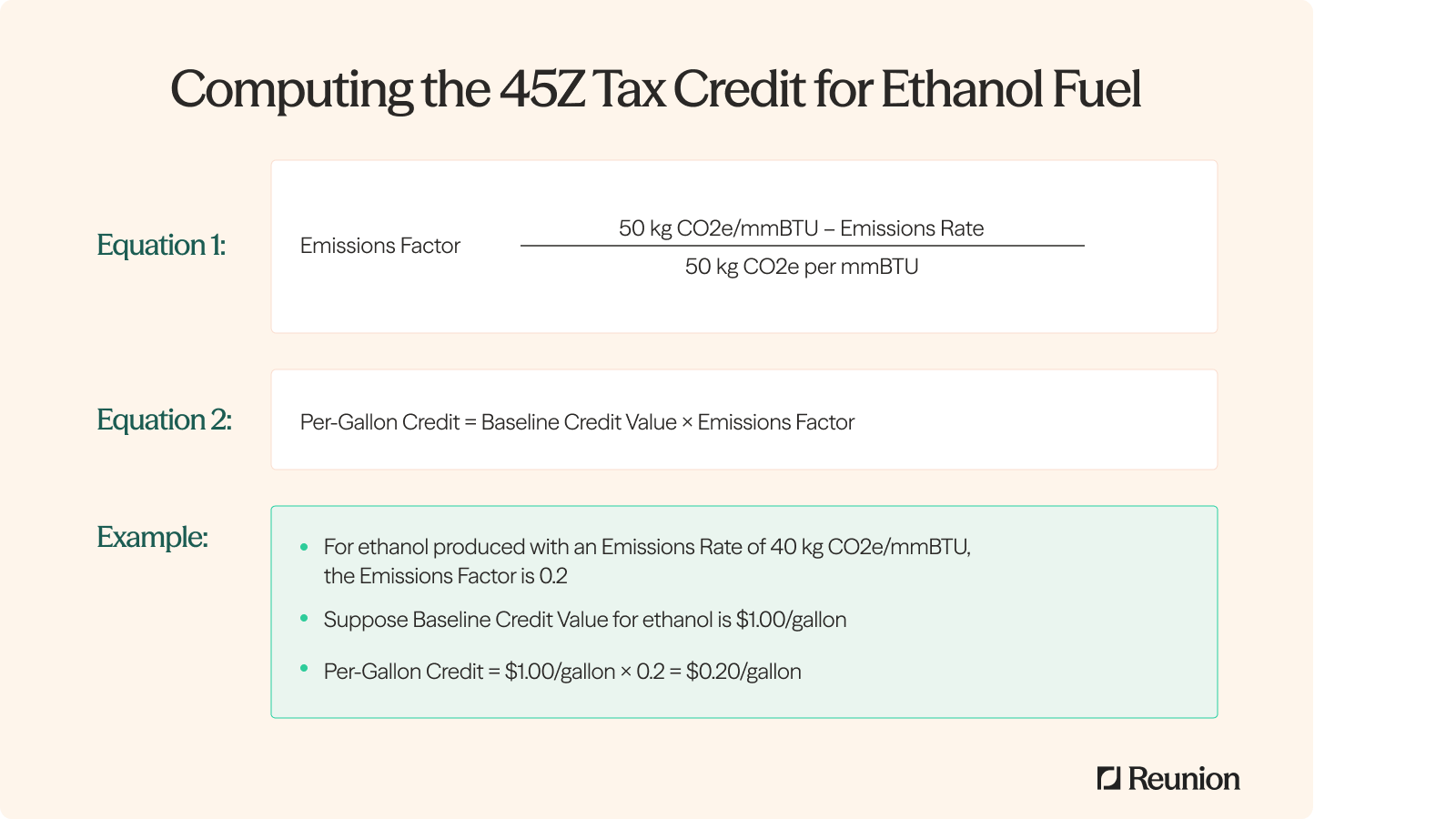

The §45Z PTC has garnered broad adoption, in large part, because it offers a sliding scale of credit value based on the emissions factor of the fuel. The base credit tops out at $1.75 for sustainable aviation fuel and $1.00 per gallon for other clean fuels. These credit amounts are adjusted annually for inflation. The following example shows a credit computation for ethanol fuel with a baseline credit value of $1.00 per gallon.

The Seller

The seller, who had successfully executed several 2025 §45Z transfers, was a Midwestern-based ethanol producer with over 50 years of operating history.

For this transaction, the seller elected to transfer credits from two facilities, each with a slightly different carbon intensity. The seller carved out $30 million from a broader credit portfolio exceeding $100 million, based on an expected per-gallon credit value of $0.10 to $0.20.

The Buyers

Two publicly traded community banks — a “lead” bank and a “follow-on” bank – partnered on the buy side of the deal:

Despite five successful deals between them, neither buyer had transactional experience with §45Z PTCs, which require a specialized set of third-party deliverables to properly diligence. To close this knowledge gap, the buyers elected to work with an accounting firm for additional due diligence support.

The “Club” Structure

Running two independent, even if parallel, transactions would have translated into an overarching process that added undue complexity and cost for everyone.

Reunion worked with the parties to devise a more efficient approach – a “club” deal. At its core, the structure brought both buyers to the table with the same legal counsel and accounting firm for diligence.

One Negotiation

With Reunion’s guidance, the lead bank set the key commercial terms for the transaction, including payment terms. Rather than a lump-sum payment, Reunion structured the deal as quarterly fundings across 2026 and into 2027.

The seller is scheduled to receive cash as production occurs and qualifying credits are generated. The buyers, likewise, will realize the credit value on a rolling basis.

One Timeline

The deal closed in Q1 2026 — a timeline that mattered. Both banks were motivated to close before quarter-end to recognize the credit benefit in their Q1 financials.

One Due Diligence Package

As the transaction facilitator, Reunion collaborated closely with all parties – including outside legal and diligence partners – to produce a diligence package that gave the buyers the confidence to move forward. The seller, for their part, was delighted to face a single set of questions and documentation requests.

One Tax Credit Insurance Policy

The buyers and seller agreed to a tax credit insurance policy with a limit of liability of at least 125% of the transaction volume. Unlike recapture insurance on ITC deals, tax credit insurance on a §45Z transfer is designed to protect against IRS disallowance of the credit itself – e.g., a determination that the credits were not validly generated.

Two Purchase Agreements

Reunion drafted individualized purchase agreements for each buyer, although the contents and scope were effectively the same.

The Diligence

As noted above, §45Z PTCs require a few specialized third-party deliverables that “typical” §45 wind or solar PTCs do not. That specialization is by design: because the §45Z credit amount is tied to a facility-specific emissions calculation, every element of that calculation must be verified, documented, and defensible.

- Emissions Rate: The producer's emissions rate consultant ran facility-level production data through the Department of Energy’s 45ZCF-GREET model, producing verified emissions rates for each production facility. The model rigorously incorporates elements like feedstock origin, transport logistics, and energy inputs.

- Qualifying Sales: Credits are only generated on sales to unrelated third parties for use as transportation fuel. The seller’s 2026 qualifying sales are expected to go to a range of major fuel distributors and petroleum companies. Each contract will require a review to confirm buyer identity, qualifying use, and volume traceability. Under prevailing guidance, there was an open question about whether sales to resellers and intermediaries qualified — a question the February 2026 proposed regulations resolved in the taxpayers' favor.

- Feedstock: All feedstock was confirmed as 100% domestically sourced corn — millions of bushels throughout the tax year — with agricultural purchase contracts reviewed as part of the diligence package. The proposed regulations confirmed that, for fuel produced after December 31, 2025, feedstock must be exclusively from the U.S., Mexico, or Canada.

- PWA: Because both facilities were placed in service before January 2025, Prevailing Wage and Apprenticeship (PWA) requirements applied only to ongoing alterations and maintenance — not original construction. The producer's compliance reviews and certified payroll reporting were reviewed and confirmed by the buyers' diligence partner.

- FEOC: With respect to Foreign Entity of Concern (FEOC) rules, the seller’s tax consultant confirmed the seller was not a Specified Foreign Entity (SFE).

The Takeaways

All Transacting Parties Experienced Efficiency Gains

Although the “club” formed on the buy side of the deal, all transacting parties experienced efficiency gains. The seller, as we mentioned, faced a single set of due diligence questions and requirements, while the buyers worked with the same legal and diligence partners.

Club Deals are Applicable to Other Credit and Counterparty Types

Although Reunion’s inaugural club deal involved §45Z PTCs, the key unifying features — negotiations, timing, due diligence, legal, form(s) of credit support — can be readily aligned across other credits and counterparties. Reunion is currently structuring club deals for §48 ITCs, §45U PTCs, and §45X PTCs.

“Lead” Buyers Welcome “Follow-On” Buyers and Vice Versa

When we initially proposed a club deal, we were pleasantly surprised by how receptive the prospective lead bank was to bringing a second bank into the transaction. In hindsight, it was a non-issue.

We attribute that openness to an under-appreciated feature of the tax credit market: tax, treasury, and finance leaders tend to be highly collaborative and inclined to share their expertise. As we see almost daily, it’s a relatively small community — one that consistently shows a willingness to support peers in meaningful ways.