How Do Differences in Fiscal Year-End Dates Affect Tax Credit Transfers?

A review of how tax year-end affects transferability for buyers and sellers.

Transferable tax credits are a powerful tool for profitable companies looking to manage their federal tax liability. When buying transferable tax credits, however, companies must consider their tax year-end in conjunction with that of the seller in order to claim the credits correctly and to the greatest extent possible.

IRC §6418(d) dictates tax credit purchase timing between buyers and sellers

Internal Revenue Code §6418(d) explains the specific rule relating to the relationship between a buyer’s (transferee taxpayer) and seller’s (eligible taxpayer) tax year-ends.

"In the case of any credit (or portion thereof) with respect to which an election is made under subsection (a), such credit shall be taken into account in the first taxable year of the transferee taxpayer ending with, or after, the taxable year of the eligible taxpayer with respect to which the credit was determined."

Corporate taxpayers will face one of three scenarios when engaging tax credit sellers

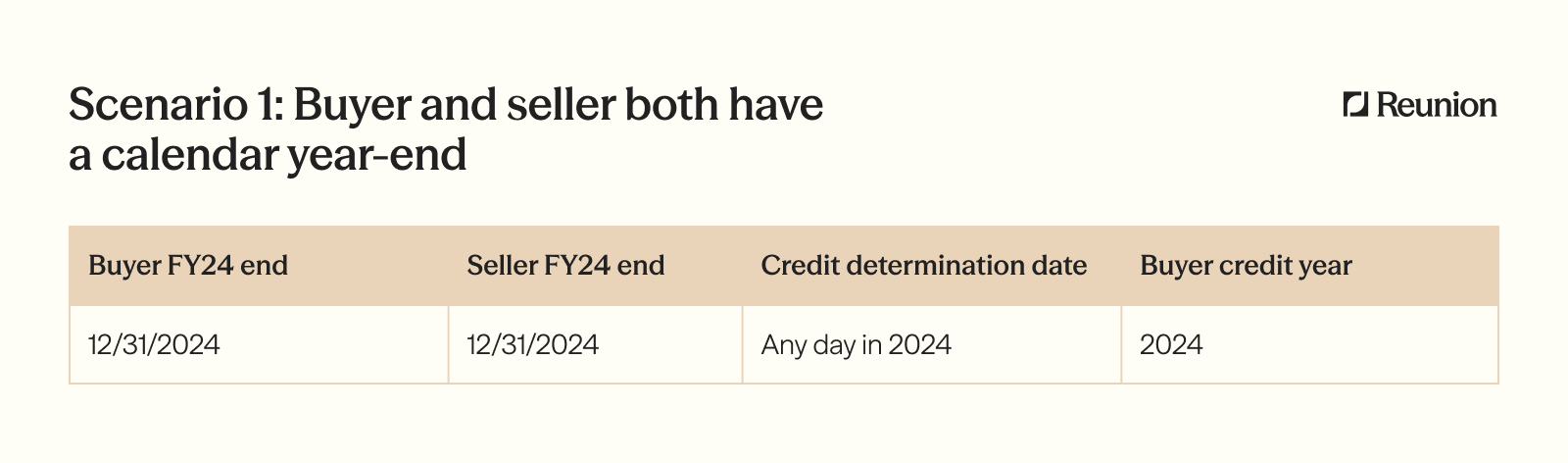

Scenario 1: Buyer and seller both have a calendar year-end

For transactions where both the buyer and seller have a 12/31 tax year-end date, the credits simply apply to the tax year in which they were generated.

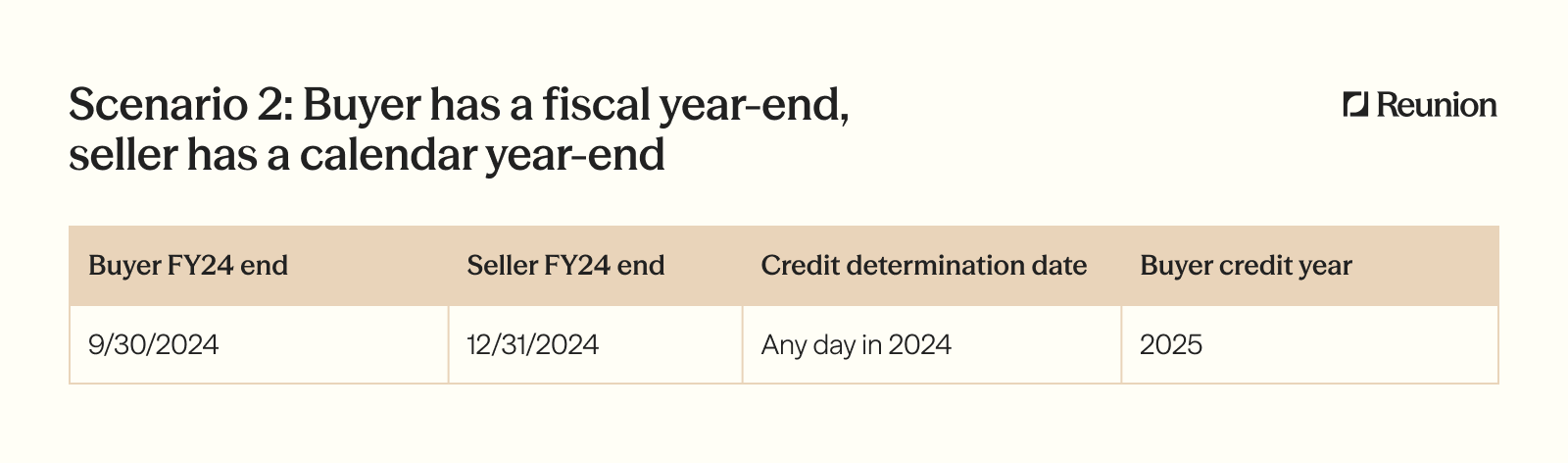

Scenario 2: Buyer's tax year ends before that of the seller

For a transaction where the buyer tax year ends before that of the seller – for example, the buyer has a 9/30 tax year, and the seller has a 12/31 tax year – any credits generated in the same calendar year are pushed into the next tax year for the buyer.

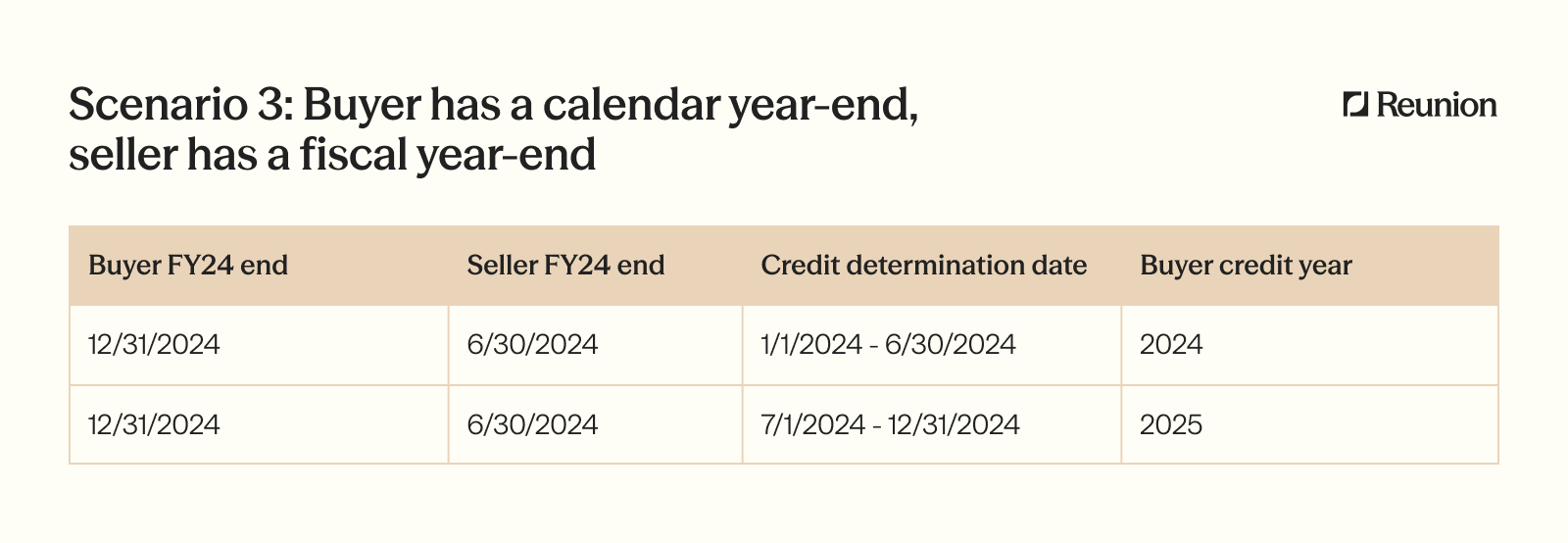

Scenario 3: Buyer's tax year ends after that of the seller

Lastly, for a transaction where the seller's tax year ends before that of the buyer, credits generated prior to the end of the seller tax year will apply to the current calendar year, but credits generated after the end of the seller tax year will push into the next calendar year.

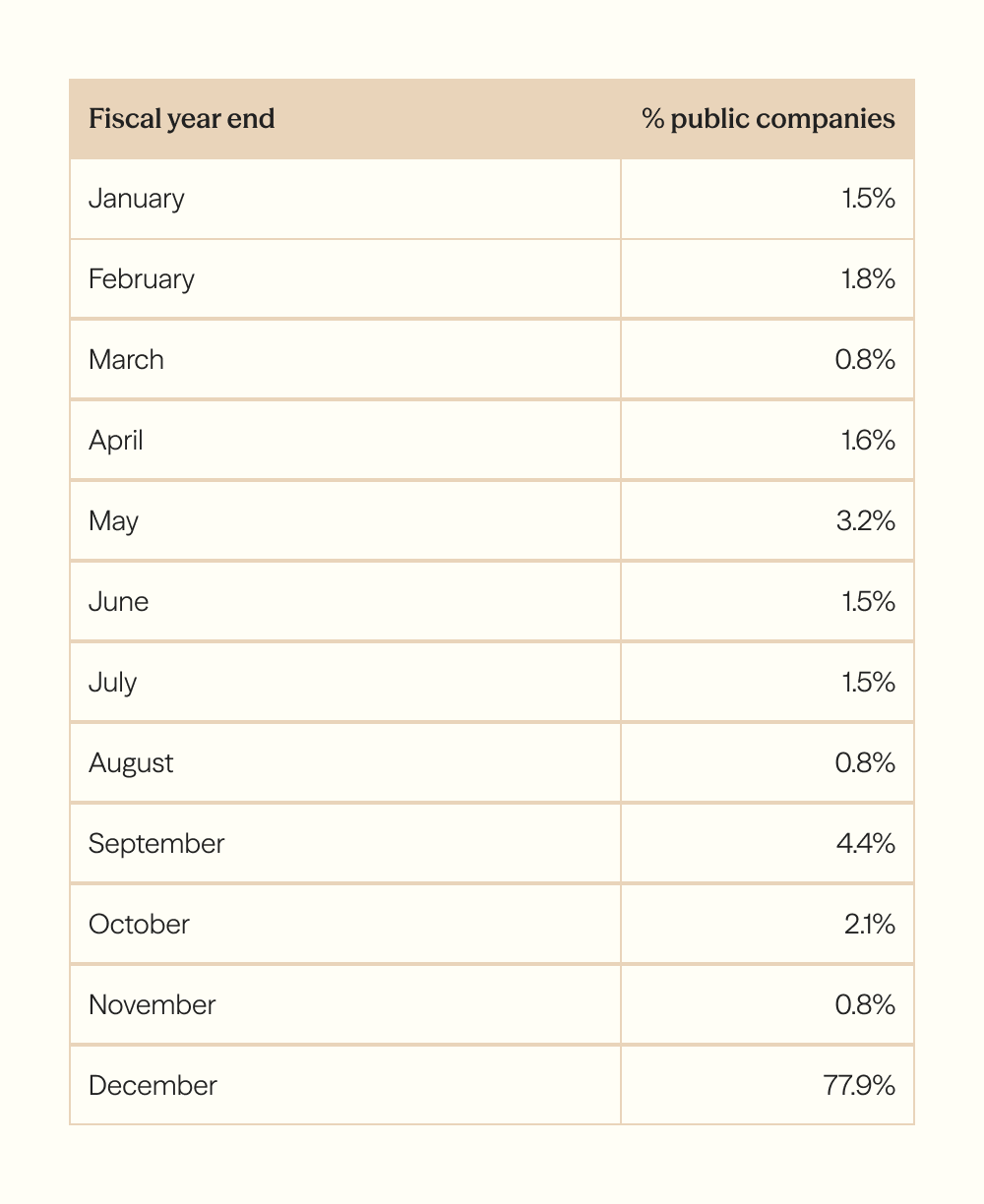

Most eligible corporate taxpayers are calendar-year filers

There are approximately 600 publicly traded companies in the U.S. with a trailing 12-month income tax liability over $100M (as of May 2024).

Of these companies, 78% are calendar-year filers, while another 8.0% close out their fiscal year in February or September.

If we increase the threshold to $500M of trailing 12-month income tax liability, the numbers remain consistent: 78.2% of companies are calendar-year filers.

Find credits that complement your company's tax year-end

To find clean energy tax credits that complement your company's tax year-end, please contact Reunion's transactions team. In addition to providing access to our tax credit marketplace, we can curate a list of projects that most closely align with your needs.