A Comprehensive Guide to Prohibited Foreign Entities for Clean Energy Tax Credits

Learn how OBBBA’s new foreign entities of concern (FEOC) expand clean energy tax credit restrictions, eligibility, effective control agreements & compliance.

The One Big Beautiful Bill Act (OBBBA) added new “Prohibited Foreign Entity (PFE)” restrictions, primarily intended to prevent Chinese companies from benefiting from tax credits, and to reduce reliance on China for clean energy technology. PFE restrictions apply to entities connected to China, Russia, North Korea, and Iran, and prohibit them from claiming §48E, §45Y, §45X, §45U, §45Z, and §45Q tax credits, either directly or indirectly.

PFE restrictions are broadly divided into two sets of rules:

- Taxpayer level restrictions: taxpayers claiming §48E, §45Y, §45X, §45U, §45Z, and §45Q tax credits may not be a prohibited foreign entity (PFE), and the tax credit may not be transferred to a PFE (see Taxpayer level FEOC restrictions below). For §48E, §45Y, §45X credits, taxpayers may not give “effective control” to a specified foreign entity (SFE) through a binding contract or licensing agreement (see Effective control FEOC restrictions below)

- Project level restrictions: taxpayers claiming §48E, §45Y, and §45X tax credits may not receive “material assistance” from a PFE through the use of manufactured products or eligible components (see Material assistance FEOC restrictions below).

PFE restrictions take effect in tax years beginning after the OBBBA date of enactment: July 4, 2025. Projects claiming legacy §45 or §48 credits are not subject to any of the PFE restrictions. §45Y and §48E projects that start construction for tax purposes before January 1, 2026, are not subject to project-level material assistance requirements (but are subject to the entity-level restrictions beginning in the taxpayer’s first taxable year after enactment of the OBBBA).

Buyers will need to perform careful due diligence to ensure PFE compliance.

Taxpayer-level restrictions

Prohibited foreign entities (PFEs), which can be either a specified foreign entity (SFE) or a foreign-influenced entity (FIE), are not allowed to claim the following tax credit types: §45Y, §48E, §45X, §45Q, §45U, and §45Z

For §45Y, §48E, §45X, and §45Q, both SFEs and FIEs cannot claim credits starting the tax year beginning after July 4, 2025.

For §45U and §45Z, the prohibition on SFEs starts the tax year beginning after July 4, 2025. The prohibition on FIEs starts the second tax year beginning after July 4, 2025.

Specified foreign entities

Per §7701(a)(51)(B), an SFE is defined to be one of the following:

- A “foreign entity of concern” as defined in the William M. (Mac) Thornberry National Defense Authorization Act (NDAA) for Fiscal Year 2021. Entities meeting this criteria include foreign terrorist organizations, entities owned by the Chinese, Russian, North Korean, or Iranian government (the “Covered Nations” as defined in §4872(f)(2) of title 10, United States Code), and entities that could be a threat to national security

- A Chinese military company as defined in §1260H of the William M. (Mac) Thornberry National Defense Authorization Act for Fiscal Year 2021

- An entity manufacturing products that benefits from Uyghur forced labor in Xinjiang in China, per §2(d)(2)(B) of Public Law 117-78

- An entity included on the OFAC list that could pose a threat to national security per §154(b) of the National Defense Authorization Act for Fiscal Year 2024

- A “foreign-controlled entity” (FCE) as defined per §7701(a)(51)(C) as an entity that is 50% or more owned by one of the following:

- A government of one of the Covered Nations

- An agency of one of the governments of a Covered Nation

- A citizen or national from a Covered Nation (if not also a citizen, national, or green card holder of the United States)

- A company with its primary place of business in a Covered Nation

Foreign-influenced entity

As defined in §7701(a)(51)(D), an FIE is an entity where an SFE has “influence” in at least one of the following ways:

- An entity where the SFE has “direct authority” to appoint a “covered officer” (such as a board member, CEO, CFO, COO, general counsel, or senior vice president, defined in §7701(a)(51)(F))

- An entity that is 25% or more owned by an SFE

- An entity that is 40% or more owned by multiple SFEs

- An entity with 15% or more debt held by at least one SFE when issued

- An entity with “effective control” through contractual payments, as defined in the next section

Effective control restrictions

The OBBBA adds additional restrictions to entities that make “applicable payments” to an SFE during the taxable year through a binding contract or licensing agreement, therefore giving “effective control” (as defined in §7701(a)(51)(D)(ii)) over either the project, manufactured products, or eligible components as it relates to the claimed tax credits of §45Y, §48E, or §45X. The IRS will provide additional guidance to aid developers in identifying an instance of effective control. In the meantime, entities should avoid giving potential SFEs the unrestricted contractual right to:

- Determine the quantity or timing of production of an eligible component (for §45X)

- Determine the amount or timing of activities related to the production or storage of electricity (for §45Y or §48E)

- Determine which entity may purchase or use the eligible components or critical minerals

- Determine which entity may purchase or use the electricity

- Restrict access to data critical to production or storage of energy, or to the factory, mine, or mineral processing facility, to the personnel or agents of such contractual counterparty, or

- On an exclusive basis, maintain, repair, or operate any plant or equipment which is necessary to the production of eligible components or electricity

Effective control can also be triggered if a taxpayer enters into a licensing agreement with an SFE after the OBBBA date of enactment that gives the SFE a significant role. Entities should avoid giving potential SFEs the contractual right to:

- Specify or otherwise direct one or more sources of components, subcomponents, or applicable critical minerals to be used in an electricity or energy storage project, or in the production of an eligible component

- Direct the operation of an electricity or energy storage project, or a facility that produces eligible components or critical minerals

- Limit the taxpayer's utilization of intellectual property related to the operation of an electricity or energy storage project, or in the production of an eligible component

- Receive royalties for more than 10 years

- Require the taxpayer to enter an agreement for the provision of services for a duration longer than 2 years

In addition, manufacturers and mineral producers entering into licensing arrangements should have the “technical data, information, and know-how necessary to enable the licensee to produce the eligible component” without needing further involvement from the counterparty or other specified foreign entity.

A bona fide purchase or sale of intellectual property is not subject to these restrictions. However, arrangements where the “ownership of intellectual property reverts to the contractual counterparty after a period of time” shall not be considered a bona fide purchase or sale.

Recapture for §48E ITCs

In §50(a)(4), the recapture risk for ITCs is extended to ten years if there is any “applicable payment” sent to an SFE, and therefore allowing that entity to have effective control. If any payment is made to an SFE in the ten years after the qualified facility is placed in service, then the entirety of the credit is clawed back. This provision applies to taxpayers who claim a credit for any taxable year beginning after July 4, 2027 (e.g., 2028 and beyond for calendar year filers). This may have the impact of shifting more developers towards claiming a §45Y credit over §48E, if they have the option to do so.

Risk of public companies becoming PFEs

Public companies are largely exempt from being considered an SFE (per §7701(a)(51)(E)), except in the instance where the company is traded on a market in a Covered Nation. Additionally, they are at risk of being considered an FIE if an SFE has the authority to appoint a board member or executive officer. Public companies are also at risk of giving “effective control” to an SFE through a contractual payment or licensing agreement.

Transferred credits to SFEs

The OBBBA amended §6418(g) to prohibit the transfer of a §48E, §45Y, §45X, §45Q, §45U, or §45Z credit to an SFE. Therefore, tax credit transfer transactions involving these credits also need to diligence the purchaser.

Determination

Entities are tested to determine if they qualify as SFEs and FIEs on the last day of the tax year for which the applicable credit is claimed (see §7701(a)(51)(A)(ii)).

The only exception is the first taxable year after July 4, 2025, where the test takes place on the first day of the taxable year. Said another way, all entities will be tested on January 1, 2026, for the 2026 tax year, assuming they have a calendar fiscal year end.

Material assistance restrictions

The OBBBA restricts developers’ ability to claim §45Y, §45X, and §48E credits if they receive “material assistance” from a “prohibited foreign entity” as defined in §7701(a)(52). Material assistance is represented as a percentage of the total direct costs that meet the compliance threshold (for the avoidance of doubt, these are costs that are NOT affiliated with a PFE). For §48E ITCs and §45Y PTCs, the costs analyzed are the labor and material costs of the manufactured products and their components used in qualified facilities. For §45X AMPCs, the costs are the direct material costs of eligible components and critical materials.

In the case of §45Y and §48E credits, projects that begin construction for tax purposes before January 1, 2026, do not need to comply with material assistance requirements. The OBBBA codified that the beginning of construction rules in IRS Notices 2013-29 and 2018-59 (as well as any subsequently issued guidance clarifying, modifying, or updating either Notice), as in effect on January 1, 2025, apply to FEOC requirements. On August 15, 2025, the Treasury issued Notice 2025-42 modifying the BoC rules for wind and solar tax credit eligibility; however, the document reiterates in Footnote 3 that, “The guidance in this notice is not intended to address the beginning of construction rules for those foreign entity restrictions. The Treasury Department and the IRS are currently drafting additional guidance as is necessary and appropriate to implement those restrictions, as enacted by the OBBBA.”

Material assistance for tech-neutral credits (§45Y and §48E)

§7701(a)(52)(A)(i) provides guidance on how to meet the “threshold percentage for qualified facilities and energy storage,” as defined based on the following cost ratio for the manufactured products involved:

Total Manufactured Products Costs are the total direct costs for all “manufactured products (including components) which are incorporated into the qualified facility or energy storage technology upon completion of construction." Examples of manufactured products are solar modules and batteries that are produced in a factory, versus on-site construction materials.

Manufactured Products Costs Without Prohibited Foreign Entities are the total direct costs of manufactured products (including components) that are NOT “mined, produced, or manufactured by a prohibited foreign entity” (§7701(a)(52)(D)(i)(II)).

The “threshold percentage for qualified facilities and energy storage technology”, as defined in the above formula, must meet the requirements in the table below, depending on the year when the qualified facility or energy storage technology begins construction.

Threshold percentage requirements (§45Y and §48E)

Per §7701(a)(52)(B), the following threshold percentages apply for qualified facilities and storage technology claiming §45Y PTCs and §48E ITCs:

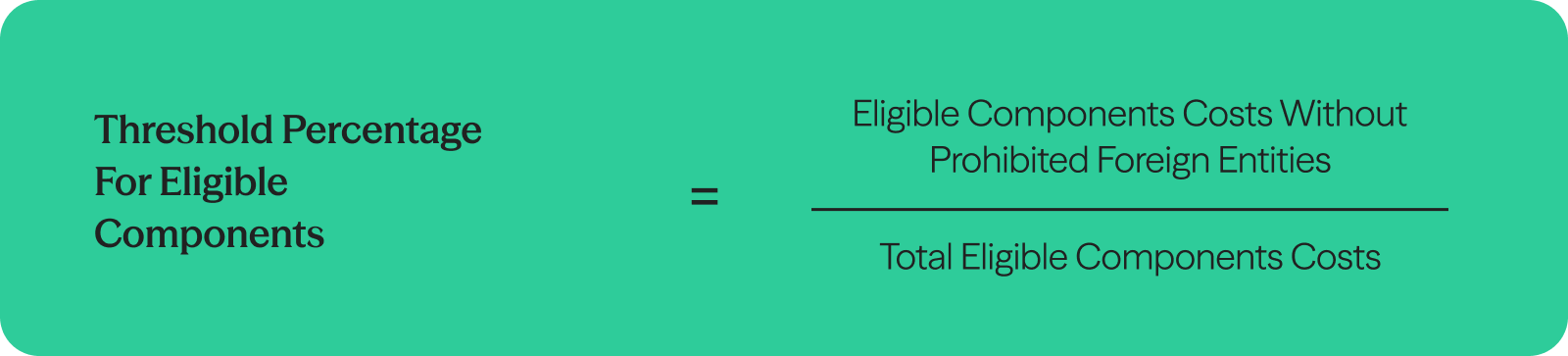

Material assistance for eligible components (§45X AMPCs)

For eligible components and critical minerals, §7701(a)(52)(A)(ii) provides guidance on how to meet the “threshold percentage for eligible components,” as defined based on the following cost ratio for the eligible components involved:

Total Eligible Components Costs are the direct material costs paid or incurred for production of the eligible components.

Eligible Components Costs Without Prohibited Foreign Entities is defined to be the direct material costs paid or incurred for production of the eligible components that are NOT “mined, produced, or manufactured by a prohibited foreign entity” per §7701(a)(52)(D)(ii)(II).

The “threshold percentage”, as defined by the above formula, must meet the requirements in the table below, depending on the year in which the component is sold.

Threshold percentage requirements (§45X AMPCs)

Per §7701(a)(52)(B), the following “threshold percentages” apply for eligible components or critical minerals claiming §45X AMPCs. Note that for applicable critical minerals, the “threshold percentages” will be updated by December 31, 2027, and the OBBB provides Treasury with the discretion to increase these amounts to consider several subjective factors, including domestic availability and processing capacity, supply chain constraints, and national security concerns.

Documentation

Safe Harbor Tables

Per §7701(a)(52)(D)(iii), the IRS is expected to publish tables no later than December 31, 2026, to improve the ease of the calculation of the “threshold percentages” and provide all rules regarding material assistance (for §45Y, §48E, and §45X).

Until these tables are published, taxpayers can use existing domestic content tables from Notice 2025-08, issued in January 2025, and included in Appendix D. The domestic content tables only apply to solar, onshore wind, and battery storage projects. Other project types will need to use the actual material and labor costs that developers paid (note: this contrasts with the domestic content calculations, which require supplier costs).

Certificates

Project developers and manufacturers will ask equipment suppliers to provide certificates confirming whether products were manufactured by PFEs, and whether there are any PFEs in the supply chain. The certificate should confirm the payment amount charged to the taxpayer for non-PFE goods (see §7701(a)(52)(D)(iii)). Certificates should be retained by both the taxpayer and supplier for six years and include the following:

- EIN Number of the supplier

- Any foreign identification number

- Signatures from suppliers

- Statement about the relationship to a PFE, if applicable, for all Manufactured Products Costs or Eligible Components Costs

Material assistance exclusions

In the instance where the Manufactured Products Costs are derived from binding contracts and purchase orders entered into before June 16, 2025, the costs are excluded from the material assistance determination assuming the project begins construction by July 31, 2025, and is placed in service by December 31, 2029 (or by December 31, 2027 for solar or wind projects) (see §7701(a)(52)(D)(iv)). Similarly, for Eligible Components Costs, any costs incurred pursuant to binding contracts and purchase orders entered into before June 16, 2025, will also be excluded for eligible components sold by December 31, 2029.

Material assistance penalties

The IRS can challenge the material assistance determination anytime in the six years after the tax return is filed for a qualified facility, energy storage technology, eligible component, or critical mineral (see §6501(o)), and there are significant penalties if an inaccuracy is discovered. The penalties are calculated based on the understatement of income tax that occurred from the inaccurately claimed tax credit. The following penalties hold:

- Penalty to taxpayer: Per §6662(a), the penalty is 20% of the reduction in the tax basis that benefited from the tax credit if the taxpayer’s underpayment exceeds 1% of what they should have paid or $5,000, whichever is greater. Per §6662(d)(1)(B), if the taxpayer is a corporation, the penalty applies if the taxpayer’s underpayment exceeds 1% of what they should have paid or $10 million, whichever is less.

- Penalty to equipment supplier: Per §6695B, in the instances where a certificate (as described above and in §7701(a)(52)(D)(iii)) is inaccurate, the supplier of that certificate is subject to a penalty that is the greater of 10% of the understatement of the taxpayer’s tax basis, or $5,000. This penalty is only relevant if the understatement is greater than the lesser of 5% of the tax on the tax return or $100,000. Certificates provided before January 1, 2026, are exempt from this penalty.

Practical steps to maintaining compliance

To maintain compliance with PFE restrictions, Reunion recommends an ongoing audit of supply chain entities or potential tax credit purchasers and ongoing attention to contractual language in binding contracts or licensing agreements that could potentially provide “effective control” to a counterparty.

PFE restrictions are evolving and will likely gain additional clarity with the publishing of Treasury regulations in 2026. As such, Reunion recommends working with a knowledgeable third party to ensure ongoing compliance with PFE restrictions as well as maintaining records demonstrating PFE compliance for at least six years.

High-level compliance checklist

The following items are overall suggestions of evidence to maintain for proving PFE compliance in an ongoing manner. These items are not exhaustive and, given the dynamic nature of PFE restrictions, should not be considered a comprehensive list.

Taxpayer-level SFE requirements

Maintain the following evidence to verify that the taxpayer itself is not an SFE.

- Documentation of ownership structure listing all entities with direct ownership of the taxpayer entity

- Certificates of formation/incorporation for all entities within the ownership structure

- Exchange listing documentation (for publicly traded entities)

Taxpayer-level FIE requirements

Maintain the following evidence to verify that the taxpayer itself is not an FIE.

- Documentation of ownership structure listing all entities with direct ownership of the taxpayer entity

- Certificates of formation/incorporation for all entities within the ownership structure

- Complete list of debt holders showing total debt amounts

- Documentation showing any SFE “direct authority” to appoint a “covered officer”

Effective control requirements

Maintain the following evidence to verify that over the previous tax year, an SFE did not hold “effective control”, as defined in §7701(a)(51)(D)(ii), over key aspects of the production of eligible components, energy generation in a qualified facility, or energy storage which are not included in the measures of control through authority, ownership, or debt.

- Operations, Maintenance, or Asset Management Agreements: including long-term service, performance, or dispatch authority terms

- Supply, Procurement, or Manufacturing Agreements: for equipment, components, or critical minerals, especially those specifying approved vendors or sourcing restrictions

- Power Purchase, Offtake, or Energy Storage Agreements: governing generation schedules, dispatch, or output allocation

- Licensing or Technology Agreements: covering intellectual property, software, or SCADA systems used in production or operation

- Construction or EPC Contracts: where counterparties retain operational authority, site access, or equipment control rights

- Joint Venture, Development, or Shareholder Agreements: involving shared governance, veto, or consent rights

- Financing, Lease, or Royalty Agreements: imposing operational conditions, long-term payments, or extended obligations

- Data Access or Remote Operations Agreements: granting privileged access to system controls or operational data

- Consulting, Technical Service, or Training Agreements: that create long-term dependence or ongoing foreign involvement

Material assistance requirements

Maintain the following evidence to verify that the labor and material costs of manufactured products and their components (§48E and §45Y) or the direct material costs of eligible components and critical materials (§45X) used in a qualified facility exceeded the statutory thresholds for total costs not paid to a PFE as defined in §7701(a)(52) of the U.S. Code.

Supply chain mapping

- Documentation listing all suppliers and sub-suppliers of Covered Items for each qualified facility, including entity names, addresses, and countries of formation/operation

- Bills of materials, purchase orders, and invoices identifying all Covered Items and their source entities

- Payment records and proof of transaction completion

- Agreements with contractors, subcontractors, and suppliers

- Confirmation of physical receipt or completion of services for the Covered Items

Supply chain mapping

- Documentation listing all suppliers and sub-suppliers of Covered Items for each qualified facility, including entity names, addresses, and countries of formation/operation

- Bills of materials, purchase orders, and invoices identifying all Covered Items and their source entities

- Payment records and proof of transaction completion

- Agreements with contractors, subcontractors, and suppliers

- Confirmation of physical receipt or completion of services for the Covered Items

48E recapture requirements

Maintain the following evidence to verify that no “applicable payments” to an SFE have been made that would entitle the SFE to exercise “effective control” (as defined in §7701(a)(51)(D)(i)(II)), during the ten-year period after the facility has been placed in service.

- Operations, Maintenance, or Asset Management Agreements: including long-term service, performance, or dispatch authority terms

- Supply, Procurement, or Manufacturing Agreements: for equipment, components, or critical minerals, especially those specifying approved vendors or sourcing restrictions

- Power Purchase, Offtake, or Energy Storage Agreements: governing generation schedules, dispatch, or output allocation

- Licensing or Technology Agreements: covering intellectual property, software, or SCADA systems used in production or operation

- Construction or EPC Contracts: where counterparties retain operational authority, site access, or equipment control rights

- Joint Venture, Development, or Shareholder Agreements: involving shared governance, veto, or consent rights

- Financing, Lease, or Royalty Agreements: imposing operational conditions, long-term payments, or extended obligations

- Data Access or Remote Operations Agreements: granting privileged access to system controls or operational data

- Consulting, Technical Service, or Training Agreements: that create long-term dependence or ongoing foreign involvement

Guidance and resources

Guidance

- July 4, 2025: One Big Beautiful Bill Act, Chapter 5.

Resources

The OBBBA passed on July 4, 2025, and federal resources are still being updated with amended sections.

President Trump issued a July 7, 2025, Executive Order signaling that further guidance may be released as soon as 45 days after the enactment of the bill, and Notice 2025-42 denoted that guidance relating to FEOC restrictions is still forthcoming. The IRS will also release guidance on identifying PFEs no later than December 31, 2026 (see §7701(a)(51)(D)(iii)).

Frequently Asked Questions about Prohibited Foreign Entities

- How do PFE restrictions most impact eligibility for clean energy tax credits and financing?

- PFE restrictions, as introduced by the OBBBA, prohibit Prohibited Foreign Entities (PFEs) from claiming §45Y, §48E, §45X, §45Q, §45U, and §45Z tax credits. Additionally, tax credits may not be transferred to a PFE.

- What supply chain tracing methodologies are being accepted to demonstrate compliant sourcing of critical minerals and components?

- Taxpayers will need to verify which entities in their supply chains are considered PFEs and ultimately comply with the statutory supply thresholds specified by the IRS and Treasury. Per §7701(a)(52)(D)(iii) of the U.S. Code, the IRS is expected to publish tables no later than December 31, 2026, to improve the ease of the calculation of the “threshold percentages” and provide all rules regarding material assistance (for §45Y, §48E, and §45X). Until these tables are published, taxpayers can use existing domestic content tables from Notice 2025-08, issued in January 2025. The domestic content tables only apply to solar, onshore wind, and battery storage projects. Other project types will need to use the actual material and labor costs that developers paid (note: this contrasts with the domestic content calculations, which require supplier costs)

- How can developers assess PFE risk exposure during early procurement planning for battery, solar, or wind projects?

- Developers should work with a knowledgeable third party during the procurement phases of a project to ensure that the required percentage of components is sourced from non-PFEs. There are a number of technology and service vendors in the space that are able to assist developers with this assessment.

- What due diligence frameworks or certifications are recognized to prove PFE compliance?

- Given that the PFE requirements introduced by the OBBBA are so new, as of this writing, there are no widely accepted comprehensive formats for demonstrating PFE compliance. That said, §7701(a)(52)(D)(iii) of the U.S. Code provides some guidance on the information that should be included in supplier PFE certifications. Until Treasury guidance is released in 2026, Reunion recommends working with a knowledgeable third-party to gather and document PFE compliance in an ongoing fashion.

- How might evolving geopolitical designations of SFEs affect long-term asset compliance for operational projects?

- The recapture provisions surrounding §48E tax credits with respect to PFE compliance specify that any “applicable payment” as defined in §7701(a)(51)(D)(i)(II) of the U.S. Code, to an SFE that provides the SFE with “effective control” during the ten years after a facility has been placed in service, could result in the recapture of the entire tax credit. Given this risk, it will be important to clarify if evolving SFE designations need to be taken into account when tracking any “applicable payments” to potential SFEs during the recapture period.

- How can joint ventures or partnerships with foreign investors navigate FEOC limitations without jeopardizing credit eligibility?

- Developers should work with a third party with expertise in PFE compliance when navigating credit eligibility in a situation where foreign investors are involved. Developers should ensure documentation of any internal investigations into foreign investors' PFE status, as well as document foreign investors’ corporate formation documents, while ensuring that the investors are not SFE.