A Comprehensive Guide to Complying with Prevailing Wage and Apprenticeship Requirements

Ensure compliance with the final regulations on prevailing wage and apprenticeship requirements for energy tax credits. Mitigate risks and avoid penalties.

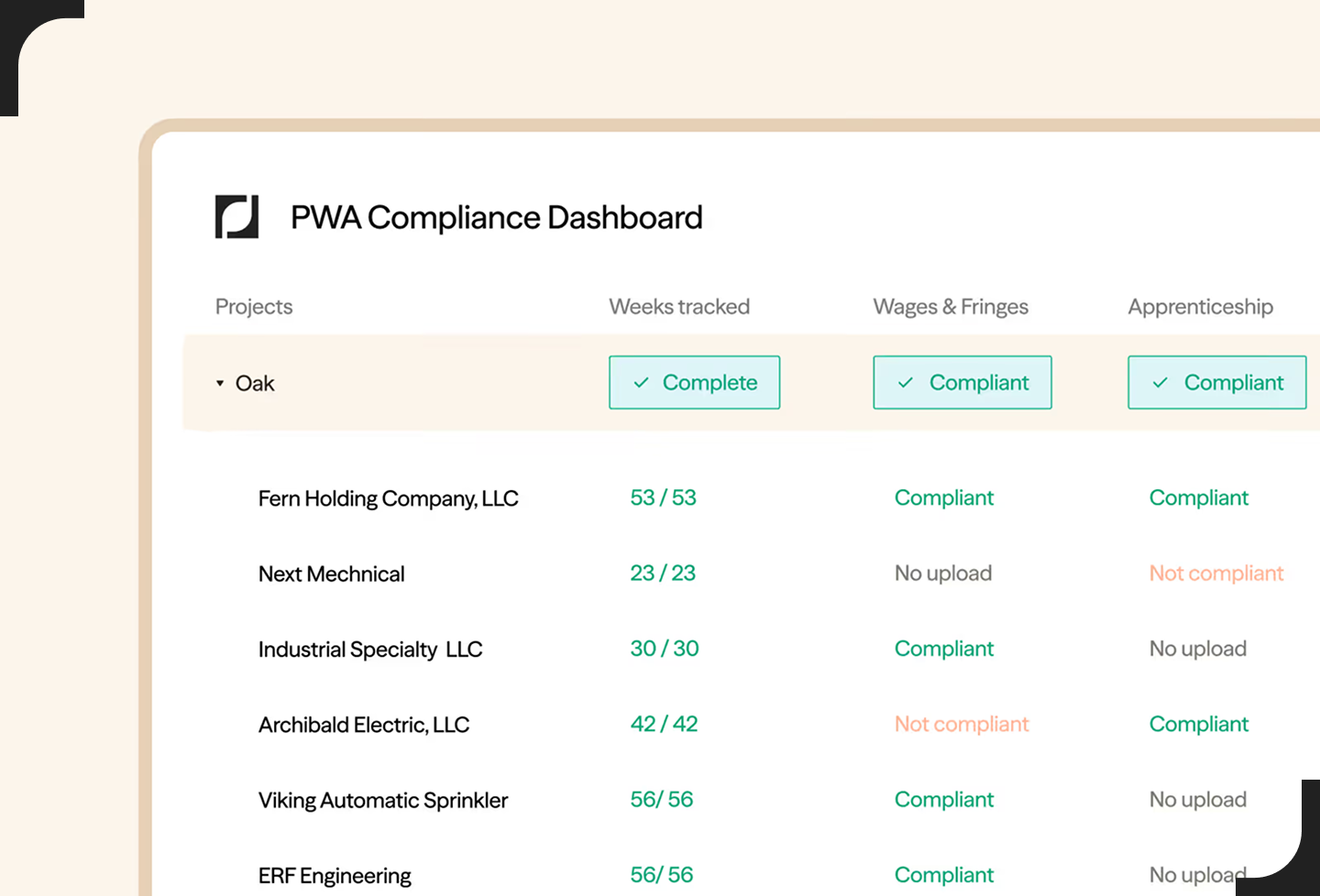

.jpg)

The Inflation Reduction Act (IRA) aims to create a robust market for well-paying clean energy jobs. To achieve this goal, the IRA significantly increases the tax benefits for projects that meet Prevailing Wage and Apprenticeship (PWA) requirements. The IRA introduced transferable tax credits, codified under §6418 of the Internal Revenue Code (IRC), allowing "eligible taxpayers" to sell certain energy tax credits to unrelated third parties for cash. Transferability intends to broaden the pool of investors participating in clean energy financing by simplifying complex structures like traditional tax equity arrangements.

Projects that comply with PWA requirements generally receive a tax credit that is five times greater than the base rate. Of the 12 tax credits eligible for transfer, only the §45X credit is not subject to PWA requirements.

The IRS and Treasury published final PWA regulations on June 18, 2024, which went into effect on August 26, 2024. Alongside the final regulations, the IRS published a fact sheet and updated its PWA FAQs.

For more information about Reunion’s PWA compliance product, please contact us here.

Prevailing wage rules

Overview of prevailing wage

Prevailing wage rules require that laborers and mechanics who are employed by the project developer, or by construction contractors or subcontractors working on the project, are paid a minimum prevailing wage specified by the U.S. Department of Labor (DOL). Prevailing wages must be paid during the construction of a facility or property, and during alteration or repair of a facility or property for a certain number of years after the project is placed in service (see Duration of PWA requirements section).

Prevailing wages apply not only to laborers and mechanics at the site of construction, but also to secondary sites where a significant portion of the construction, alteration, or repair of the facility occurs, provided that the secondary site either was established specifically for, or dedicated exclusively for a specific period of time to, the relevant project. Secondary sites include any adjacent or virtually adjacent dedicated support sites, such as job headquarters, tool yards, batch plants, or borrow pits.

Workers do not have to be paid prevailing wages for basic maintenance work, which is “routinely scheduled and continuous or recurring.” Examples of basic maintenance are regular inspections of the facility, regular cleaning and janitorial work, regular replacement of materials with limited lifespans such as filters and light bulbs, and the calibration of any equipment.

When to start paying prevailing wages

Prevailing wages must be paid from the time at which construction, alteration, or repair begins; the definition of construction, alteration, or repair is expansive and includes all types of work done on a particular building or work site, as defined in 29 CFR 5.2. This aligns with the Davis-Bacon Act (DBA) definition administered by the DOL, rather than the physical work and 5% tests the IRS has used to determine when construction starts for tax purposes (as discussed in the Beginning of construction section). For example, prevailing wages must be paid during certain demolition or removal activities, which would not be considered the start of physical work on the project for purposes of qualifying for tax benefits.

Determining the prevailing wage rate

Prevailing wage rates are published on the SAM website. The appropriate job type, location, and wage determination must be selected to comply with prevailing wage requirements. Occasionally, a job type for a given location will not be published. In this case, the taxpayer must contact the DOL at IRAprevailingwage@dol.gov to request a wage determination for the unlisted job type. The request to the DOL must include specific pieces of information such as form SF-1444, project name and location, contractor name, contract number (if applicable), name and description of the job classification needed, proposed wage rate and fringe benefits, the duties performed by workers in the proposed classification, explanation of why no current classification in the wage determination matches these duties, and an agreement or disagreement of the contracting officer and contractor with the proposed rate. The department has indicated that it will try to respond to wage determination requests within 30 days. For more information, please consult our PWA Help Center.

The prevailing wage rates that must be paid are locked in at the time the contract for the construction, alteration, or repair of the facility is executed by the project developer and the contractor. This is consistent with the timing of wage determinations in Davis-Bacon compliant projects. If a project developer enters into a contract for alteration or repair work over an indefinite period of time that is not tied to the completion of any specific work, the applicable prevailing wage rates must be updated on an annual basis on the anniversary date of such contract.

If the project developer executes separate contracts with more than one prime contractor, then for each such contract, the applicable prevailing wage rates are determined at the time the contract is executed with each prime contractor. The prevailing wage rates apply to all subcontractors under each prime contractor. Prevailing wage rates must be reset to current wage rates if the contract is later amended to add substantially to the scope of work or extend the contract period.

If work on a project straddles locations with different wage rates, then the project developer should pay the wages for each location based on where the work is done. Offshore wind projects should use the prevailing wages for the closest location on shore.

Reunion PWA automatically scrapes the SAM website for all wage determinations across all states and counties regularly. Reunion makes this data available and searchable via Reunion PWA so that developers and contractors can easily select the appropriate wage determinations for their projects.

Apprenticeship rules

The IRA’s apprenticeship rules fall into three main categories.

Labor hours requirement

The apprenticeship rules require a certain percentage of labor hours during construction, alteration, or repair for a project prior to the facility being placed in service to be performed by a qualified apprentice. The minimum percentage of hours that must be performed by qualified apprentices is:

- 12.5% for projects that began construction after December 31, 2022, and before January 1, 2024

- 15.0% for projects that begin construction after December 31, 2023

Hours worked by foremen, superintendents, owners, or persons employed in a bona fide executive, administrative, or professional capacity are excluded from the labor hours calculation, unless these persons devote more than 20% of their time during a workweek to manual or physical labor. In this case, the hours worked must be included in the denominator (total labor hours) of the apprentice labor hours calculation.

Ratio requirement

Any apprentices performing work on a project are subject to the applicable apprentice-to-journeyworker ratio as prescribed by the associated registered apprenticeship program. Apprentice-to-journeyworker ratios must be met daily and vary depending on the applicable apprentice program’s requirements.

Participation requirement

Any contractor, subcontractor, or taxpayer who employs four or more mechanics or laborers on the project must employ one or more qualified apprentices. The journeyworkers and apprentices, however, do not have to be employed at the same time, provided that the applicable apprentice-to-journeyworker ratio as prescribed by the associated apprenticeship program is met on days when the apprentice is working.

Duration of PWA requirements

The duration of the PWA compliance requirement depends on the tax credit type. The IRS clarified in the final regulations that apprentices are not required for work after a project is placed in service; therefore, compliance during the post-construction period applies only to prevailing wages.

As previously noted, §45X advanced manufacturing production credits are not subject to PWA requirements.

Impact of PWA Compliance on Tax Credits

Overview

The Prevailing Wage and Apprenticeship (PWA) requirements are a critical component of the Inflation Reduction Act of 2022 (IRA), and compliance with these rules has a direct and substantial financial impact on the value of most clean energy tax credits.

PWA compliance determines whether a project qualifies for an enhanced, significantly larger tax credit amount, which is generally five times greater than the base tax credit rate.

Financial Impact: The 5x Multiplier

For most transferable tax credits, meeting the PWA requirements results in a credit rate that is five times higher than the base rate.

The IRS updates §45 and §45Y PTC rates on an annual basis, generally in Q2. Rates are determined using an inflation adjustment factor (IAF) and published in the Federal Register. The inflation adjustment factor for 2025 is 1.9971. Specific examples of this financial enhancement include:

Investment Tax Credits (§48 and §48E ITCs):

- If PWA requirements are met (or exempted from), the credit is 30% of a project’s qualified basis.

- If PWA requirements are not met, the credit is reduced to the base rate of 6% of the qualified basis.

- Furthermore, achieving PWA compliance is necessary to receive the full value of certain bonus credits. For example, the Energy Community bonus or Domestic Content bonus is typically 10% of the qualified basis if PWA requirements are met, but only 2% if they are not met.

Production Tax Credits (§45 and §45Y PTCs):

- The §45Y PTC has one base rate, irrespective of when a qualifying project is placed in service. The base rate is $3 per megawatt-hour (MWh) of qualifying electricity produced and sold. With PWA compliance (or exemption), the rate increases to $15 per MWh. There is also an annual, calendar year inflation adjustment for the rates, in which the rates are multiplied by the inflation adjustment factor described above and rounded. The $3 base rate is rounded to the nearest multiple of $0.50, and the $15 PWA rate is rounded to the nearest multiple of $1. As such, using the 2025 inflation adjustment factor of 1.9971, the 2025 base rate and PWA rate (after rounding) are $6 and $30 per MWh of qualifying electricity produced and sold, respectively.

- For projects placed in service after December 31, 2021, the §45 PTC rate calculation is $3 per MWh of qualifying energy, multiplied by the inflation adjustment factor, and rounded to the nearest $0.50. For projects meeting PWA requirements, this product is multiplied by five. There is no separate PWA rate of $15 per MWh of qualifying energy for these projects, and as such, the resulting rate for PWA-compliant projects may have small differences from the PWA rates discussed above, as was the case in 2024. The same technology-specific rate adjustments apply for open-loop biomass, small irrigation power, landfill gas, and trash facilities, so the resulting rate is reduced by one-half. There is no phaseout adjustment for wind projects placed in service after December 31, 2021. The 2025 rate, assuming prevailing wage and apprenticeship compliance, is $30.00 per MWh for wind, closed-loop biomass, geothermal, and solar; and $15.00 per MWh for open-loop biomass, landfill gas, trash, qualified hydropower, and marine and hydrokinetic renewable energy. For qualified hydropower and marine and hydrokinetic renewable energy facilities placed in service after December 31, 2022, the 2024 rate is $15.00 per MWh, assuming prevailing wage and apprenticeship compliance.

- Similar to the ITC case, the Energy Community bonus and Domestic Content bonus add a 10% increase to the applicable rate (Base or PWA-compliant).

Impact on Risk and Due Diligence

For tax credit purchasers, PWA compliance is a major risk factor. If the requirements are not met and the project claimed the enhanced rate, the credit amount can be dramatically reduced (e.g., from 30% to 6% for an ITC), resulting in an "excessive credit transfer". The buyer is liable for this excessive credit amount plus a 20% penalty.

Therefore, PWA compliance heavily influences the due diligence process for transferable tax credit transactions:

- Buyers must ensure sellers maintain extensive records, including payroll records for all laborers and mechanics (including apprentices).

- Documentation must substantiate proper labor classifications, applicable wage rates, and comprehensive apprenticeship records (requests, hours worked, ratios).

- For §48 ITCs, the seller must provide an annual prevailing wage compliance report during the five-year recapture period.

- Buyers should validate if a seller claims an exception, such as verifying the BoC date or the project's output capacity.

- Due to the complexity, Reunion offers a PWA compliance software product to reduce the time and expense of complying with PWA requirements and generate a standardized report for due diligence purposes.

Records and documentation

If PWA requirements are not fulfilled, tax credit buyers who were expecting the full tax credit amount could face a credit disallowance and be subject to underpayment penalties. However, when PWA compliance is well-documented, a careful due diligence process can help buyers get comfortable that the tax credits are properly accounted for.

Prevailing wage records

PWA documentation must include “payroll records for each laborer and mechanic (including each qualified apprentice) employed by the taxpayer, contractor, or subcontractor employed in the construction, alteration, or repair of the qualified facility.”

The guidance also lists further information that the taxpayer “may include” in their records for prevailing wage compliance:

- Identifying information for each laborer and mechanic who worked on the construction, alteration, or repair of the qualified facility, including the name, the last four digits of a social security or tax identification number, address, telephone number, and email address

- The location and type of construction of the qualified facility

- The labor classification(s) the taxpayer applied to each laborer and mechanic for determining the prevailing wage rate and documentation supporting the applicable classification, including the applicable wage determination and copies of executed contracts for construction, alteration, or repair of the qualified facility with any contractor or subcontractor

- The hourly rate(s) of wages paid (including rates of contributions or costs for bona fide fringe benefits or cash equivalents thereof) for each applicable labor classification

- Records to support any contribution irrevocably made on behalf of a laborer or mechanic to a trustee or other third person pursuant to a bona fide fringe benefit program, and the rate of costs that were reasonably anticipated in providing bona fide fringe benefits to laborers and mechanics pursuant to an enforceable commitment to carry out a plan or program described in 40 U.S.C. 3141(2)(B), including records demonstrating that the enforceable commitment was provided in writing to the laborers and mechanics affected

- The total number of hours worked by each laborer and mechanic per pay period.

- The total wages paid for each pay period (including identifying any deductions from wages)

- Records to support wages paid to any qualified apprentices at less than the applicable prevailing wage rates, including records reflecting an individual’s participation in a registered apprenticeship program and the applicable wage rates and apprentice-to-journeyworker ratios prescribed by the registered apprenticeship program

- The amount and timing of any correction and penalty payments and documentation reflecting the calculation of the correction and penalty payments, including records to demonstrate eligibility for the penalty waiver in §1.45-7(c)(6)

- Records to document any failures to pay prevailing wages and the actions taken to prevent, mitigate, or remedy the failure (for example, records demonstrating that the taxpayer (or an independent third party engaged by the taxpayer) regularly reviewed payroll practices, included requirements to pay prevailing wages in contracts with contractors, and posted prevailing wage rates in a prominent place on the job site)

- Records related to any complaints received by the taxpayer, contractor, or subcontractor that the taxpayer, contractor, or subcontractor was paying wages less than the applicable prevailing wage rate for work performed by laborers and mechanics with respect to the qualified facility

Apprenticeship records

For apprentices, the developer should capture:

- Any written requests for the employment of apprentices from registered apprenticeship programs, including any contacts with the DOL’s Office of Apprenticeship or a state apprenticeship agency regarding requests for apprentices from registered apprenticeship programs

- Any agreements entered into with registered apprenticeship programs with respect to the construction, alteration, or repair of the facility

- Documents reflecting the standards and requirements of any registered apprenticeship program, including the applicable ratio requirement prescribed by each registered apprenticeship program from which taxpayers, contractors, or subcontractors employ apprentices

- The total number of labor hours worked with respect to the construction, alteration, or repair of the qualified facility, including and identifying hours worked by each qualified apprentice

- Records reflecting the daily ratio of apprentices to journeyworkers

- Records demonstrating compliance with the Good Faith Effort Exception in §1.45-8(f)(1) (including requests for qualified apprentices, correspondence with registered apprenticeship programs, and denials of requests)

- The amount and timing of any penalty payments and documentation reflecting the calculation of the penalty payments

- Records to document any failures to satisfy the apprenticeship requirements under §45(b)(8) and §1.45-8 and the actions taken to prevent, mitigate, or remedy the failure

- Records related to any complaints received by the taxpayer, contractor, or subcontractor that the taxpayer, contractor, or subcontractor was not satisfying the apprenticeship requirements

Annual prevailing wage compliance report

For §48 ITCs, tax credit sellers must submit an annual prevailing wage compliance report to the IRS during the five-year recapture period. The report should adequately document the payment of prevailing wages with respect to any alteration or repairs of the project.

Tax credit sellers submit the report to the IRS with their tax returns. To ensure compliance with the reporting requirement, tax credit buyers should receive confirmation of the seller’s annual submission.

Compliance

The IRS encourages tax credit sellers to take the following actions to ensure ongoing compliance:

- Regularly reviewing payroll records

- Ensuring that any contracts entered into with contractors require that the contractors and their subcontractors adhere to prevailing wage and apprenticeship requirements

- Regularly reviewing compliance with the prevailing wage and apprenticeship requirements (including the proper worker classifications of laborers and mechanics, the applicable prevailing wage rates, and the percentage of labor hours performed by qualified apprentices)

- Posting information about paying prevailing wages in a prominent and accessible location, or otherwise providing written notice regarding the payment of prevailing wage rates

- Establishing procedures for individuals to report suspected failures to comply with the prevailing wage and apprenticeship requirements without retaliation or adverse action

- Investigating reports of suspected failures to comply with the prevailing wage and apprenticeship requirements

- Contacting the DOL’s Office of Apprenticeship or the relevant state apprenticeship agency for assistance in locating registered apprenticeship programs

Exceptions

Beginning of construction

Projects that began construction before Jan. 29, 2023, are exempt from the prevailing wage and apprenticeship rules, except for credits under §48C and §45Z. To learn more, please refer to the Beginning of construction section.

For the avoidance of doubt, the beginning of the construction test to determine exemption from prevailing wage and apprenticeship requirements is a different test than determining when construction, alteration, or repair of a project began for purposes of starting compliance with prevailing wage rates (as discussed in the When to start paging prevailing wages section).

One megawatt

Projects under §45 and §48 (and their replacements under §45Y and §48E) are exempt from PWA if the maximum net output is less than one megawatt (as measured in alternating current) or the capacity of electrical or equivalent thermal storage is less than one megawatt. The net output will be determined by “nameplate capacity,” defined in 40 CFR 96.202, as the maximum output on a steady-state basis during continuous operation under standard conditions when not restricted by seasonal or other deratings.

In the case of thermal equipment, like geothermal heat pumps and solar process heating, a developer must use the equivalent of 3.4 million British thermal units per hour (mmBTU/hour) to determine maximum capacity. For hydrogen storage and clean hydrogen production facilities, 3.4 mmBTU/hour is equivalent to 10,500 standard cubic feet per hour. Finally, for qualified biogas, developers can convert 3.4 mmBTU/hour into a maximum net volume flow rate of 10,500 standard cubic feet/hour, after converting the gas output into a maximum net volume flow using the appropriate high heat value conversion factors found in an EPA table.

Electrochromic glass, fiber-optic solar, and microgrid controllers are not eligible for the one-megawatt exception because they do not generate electricity or thermal energy.

Remedies

Prevailing wages

If a developer does not meet the PWA requirements, the tax credit does not automatically get reduced to the base rate. A developer can cure any deficiencies and will be deemed to satisfy the PWA requirements if, within 180 days from when the IRS makes a final determination (which occurs on the date the IRS sends a notice to the developer stating that the developer has failed to satisfy the PWA requirements), they:

- Pay back-wages with interest: Pay the affected laborers or mechanics the difference between what they were paid and the amount they were required to have been paid (multiplied by three for intentional disregard), plus interest at the federal short-term rate (as defined in §6621) plus 6%; and

- Pay a penalty: Pay a penalty to the IRS of $5,000 ($10,000 for intentional disregard) for each laborer or mechanic who was not paid at the prevailing wage rate in the year. This penalty applies to each calendar year of the project. If, for example, a laborer is not paid the correct prevailing wage in two calendar years, the penalty is $10,000

The taxpayer can waive the penalty if they make a corrective payment with interest by the last day of the first month after the calendar quarter in which the wage shortfall occurred, and either of two conditions is true:

- The worker was not paid less than the prevailing wage for more than 10% of all pay periods of the calendar year during which the worker was employed on the project

- The shortfall in payment was not greater than 5% of what the worker should have been paid during the year

The penalty is waived if the laborer or mechanic was employed under a “qualifying project labor agreement” and if any correction payment owed to the laborer or mechanic is paid on or before a return is filed claiming an increased credit amount. A qualifying project labor agreement must meet six requirements, which can be found at 26 CFR §1.45-7(c)(6)(ii).

To avoid increased penalties due to intentional disregard, the taxpayer should undertake a quarterly (or more frequent) review of wages paid to mechanics and laborers to ensure that wages not less than the applicable prevailing wage rate were paid.

Apprentices

Apprenticeship cures are unique to the failure that occurred. To cure a failure of a particular requirement, the following processes apply:

- Apprentice labor hours requirement: Any shortfall in apprentice labor hours is calculated (see Labor hours requirement section above and reclassification of apprentices to journeyworkers in the Apprentice ratio requirement below) and multiplied by $50 (or $500 for intentional disregard) to determine the amount of cure payment owed.

- Apprentice ratio requirement: The required apprentice-to-journeyworker ratio is calculated daily (see Ratio requirement section above), and apprentices in excess of the ratio are required to be paid a journeyworker wage. Labor hours from apprentices in excess of the ratio are also accounted for as journeyworker labor hours in the apprentice labor hours requirement above. Any shortfall in prevailing wage payments resulting from this reclassification of apprentices to journeyworkers must be remedied to maintain compliance.

- Apprentice participation hours requirement: If the participation requirement is not met (see Participation requirement section above), the shortfall in participation hours is the total labor hours divided by the number of laborers or mechanics (for the laborers or mechanics that failed to meet the participation requirement). This shortfall in participation hours is then multiplied by $50 (or $500 for intentional disregard) to determine the amount of cure payment owed.

Good-faith effort exception

The apprenticeship requirement can be satisfied if the developer or contractor made a good-faith effort to comply. The developer or contractor must have requested qualified apprentices from a registered apprenticeship program and either:

- The request was denied for reasons other than the developer’s refusal to comply with the program’s standards and requirements

- The apprenticeship program failed to respond within five business days of receiving a request

- The apprentice program provided apprentices, but there were fewer than requested

To satisfy the good faith effort exception, the developer or contractor must make a written request to at least one registered apprenticeship program that has a geographic area of operation that includes the location of the facility, or that can reasonably be expected to provide apprentices to the location of the facility; trains apprentices in the occupation(s) needed by the developer performing construction, alteration, or repair with respect to the facility; and has a usual and customary business practice of entering into agreements with employers for the placement of apprentices in the occupation for which they are training, pursuant to its standards and requirements.

An apprenticeship request must be made at least 45 days before the qualified apprentice is requested to begin work on the facility, so that registered apprenticeship programs have adequate time to plan for the anticipated need. Subsequent requests to the same registered apprenticeship program must be made no later than 14 days before qualified apprentices are requested to begin work on the facility.

If no apprentice program covers the project location, trains apprentices in the occupations needed, and supplies apprentices to employers, then the project is deemed to have made a good-faith effort without the need to file a request for apprentices. In this case, however, developers or contractors must contact the DOL and/or a state apprentice agency to help find apprentices.

A good-faith effort exception can be applied as an exemption from a portion of the apprentice labor hours requirement for a period of 365 days (or 366 during a leap year). The good faith effort exception excuses a developer or contractor from the amount of labor hours that were requested from the applicable apprentice program by applying the requested block of labor hours towards the numerator (apprentice labor hours) of the apprentice labor hours calculation. Developers or contractors must submit a subsequent request within the 365-day (or 366-day) window to continue to satisfy the good-faith exception for an additional block of apprentice labor hours. The annual duration also applies if a developer or contractor is not able to locate a registered apprenticeship program with an area of operation that includes the location of the facility.

Due diligence

Under the IRS regulations, it is the seller’s obligation to maintain and preserve sufficient records demonstrating compliance with PWA requirements. But the liability for non-compliance is on the buyer in the form of an excessive credit transfer.

If the tax credit claims to be exempt from PWA requirements, the tax credit buyer should substantiate the exemption under one of two scenarios:

- Beginning of construction exemption: Validate and substantiate that construction began before January 29, 2023

- One megawatt exemption: Validate the size of the eligible project through an audit of relevant contracts

If the tax credit requires compliance with PWA requirements, the tax credit buyer should validate that proper documentation was collected by the seller and that compliance was substantiated by a third party. At a minimum, the IRS requires “payroll records for each laborer and mechanic (including each qualified apprentice) employed by the taxpayer, contractor, or subcontractor.” The IRS also lists several other items the taxpayer may include in their records for PWA compliance, including nine related to wages and five related to apprentices; the list is available at 26 CFR §1.45-12(c) and (d).

Tax credit buyers should ensure sellers (or a contracted third party) have properly collected, maintained, and reviewed payroll records to ensure that prevailing wages were paid and sufficient apprentice labor was utilized. Tax credit sellers often engage third parties to provide additional analysis with respect to PWA compliance. Furthermore, buyers should also review the covenants, representations, and warranties in contracts with the primary EPC (and potentially with their subcontractors) to validate that all parties have agreed to comply with PWA requirements.

In the case of the §48 ITC, the seller should also provide an annual compliance report to the IRS during the recapture period.

Guidance and resources

Guidance

- November 30, 2022: IRS Notice 2022-61, Prevailing Wage and Apprenticeship Initial Guidance Under §45(b)(6)(B)(ii) and Other Substantially Similar Provisions

- August 30, 2023: Notice of Proposed Rulemaking, Increased Credit or Deduction Amounts for Satisfying Certain Prevailing Wage and Registered Apprenticeship Requirements

- November 17, 2023: Notice of Proposed Rulemaking, Definition of Energy Property and Rules Applicable to the [§48] Energy Credit

- June 24, 2024: Final regulations, Increased Amounts of Credit or Deduction for Satisfying Certain Prevailing Wage and Registered Apprenticeship Requirements

Resources

- The IRS maintains a prevailing wage and apprenticeship requirements FAQ

- The Department of Labor determines and maintains prevailing wages

- To request a wage determination, developers can email iraprevailingwage@dol.gov with project and labor information

- Apprenticeship.gov provides resources for finding qualified apprentices

- Reunion maintains a Reunion PWA Help Center for Reunion PWA customers that includes information about various regulations and instructions for submitting information to the DOL

Frequently Asked Questions about Prevailing Wage & Apprenticeship

- How can developers structure contracts to ensure continuous compliance with prevailing wage requirements across multi-phase projects?

- Ensure that contracts with EPCs (or primary contractors) contain provisions obligating the EPC and all subcontractors to abide by prevailing wage and apprenticeship requirements. Additionally, ensure that the EPC is obligated to provide certified payroll records and other relevant information to the developer (or a third party) such that PWA compliance can be certified.

- What mechanisms exist to verify and document apprenticeship utilization to satisfy the IRA’s PWA requirements?

- Developers (and contractors) should ensure that apprentices are hired from a registered apprentice program (listed on apprenticeship.gov) and that all apprentices have a certificate of registration with the applicable apprenticeship program.

- How do project timelines and change orders affect prevailing wage determinations?

- Wage determinations are “locked in” on the execution date of the construction contract with the EPC for a facility. However, wage determinations must be updated in one of the following situations:

- A new contract for alterations or repairs is executed after the facility is placed in service. In this case, use the wage determinations that are in effect when that alteration/repair contract is signed.

- There is a material contract change to the initial EPC contract. If the EPC contract is amended to substantially add scope or extend the contract period, wage determinations must be reset to the then-current modifications.

- Indefinite-term contracts are not tied to specific work. In this case, wage determinations must be reset each new contract year.

- Wage determinations are “locked in” on the execution date of the construction contract with the EPC for a facility. However, wage determinations must be updated in one of the following situations:

- What are the financial and tax credit implications of partial non-compliance with PWA provisions?

- For the purposes of determining compliance with the PWA requirements for the eligibility of the 5X rate multiplier, there is no partial compliance. Either a project is PWA compliant or it is not. That said, there are cure methods for any shortfall with respect to the PWA compliance requirements, such that projects are able to remedy issues and maintain compliance even if mistakes are uncovered later.

- How can digital compliance systems or third-party verification tools be integrated to simplify PWA tracking and reporting?

- Reunion recommends establishing a PWA tracking method at least two months before the beginning of project construction. This ensures that all contractors are aware of their responsibilities with respect to PWA and reporting. The benefit of ensuring tracking is in place before construction is that all parties maintain real-time visibility into a project’s compliance status and are able to get ahead of any underpayments or non-compliant issues before penalties are incurred.

- How are apprentices hired in rural areas or with specialized trades where registered programs may not exist or provide apprentices in the applicable trade?

- If there is no registered apprentice program that both supplies apprentices in the project location and trains apprentices in the occupations needed, then the project is deemed to have made a good-faith effort with the need to file a request for apprentices. However, the US Department of Labor or a state apprentice agency must be contacted in such cases for help finding apprentices in order to claim the good-faith effort exception.