IRS Provides IRA Tax Credit Pre-Registration Portal Data Requirements and Review Timeline

The IRS published guidance for its transferable tax credit pre-registration portal. We created a checklist for each credit type.

In early December, the IRS launched a webpage for its pre-filing registration tool. As of this post, the actual tool is "unavailable to the public."

However, developers who want a head-start can review the portal's user guide to get a clear sense of what to expect – including the IRS's recommended 120-day review timeline.

Reunion's key takeaways from the pre-registration portal user guide

- Takeaway 1: The IRS pre-registration portal is not yet open, but the user guide discloses the portal's data and documentation requirements

- Takeaway 2: The IRS does not issue a registration number until the review is complete, and the IRS recommends at least 120 days for review

- Takeaway 3: Projects must be placed in service before submitting a registration

- Takeaway 4: For every credit, the portal requires standardized information about the registrant

- Takeaway 5: The portal includes credit-specific requirements, including a "non-exhaustive" list of documents. (Navigate directly to a credit's requirements: §30C, §45, §45Q, §45U, §45V, §45X, §45Y, §45Z, §48, §48C, §48E)

- Takeaway 6: Developers will need a registration number for each facility/property

- Takeaway 7: A registration number does not mean a registrant qualifies for a credit of any specific amount

Takeaway 1: The IRS pre-registration portal is not yet open, but the user guide discloses the portal's data and documentation requirements

In early December, the IRS launched a webpage for its pre-filing registration tool. As of this post (December 18, 2023), however, the actual tool is "currently unavailable to the public."

Although the portal is not yet live, developers can get a preview of the tool's look, feel, and workflow through the Pre-Filing Registration Tool User Guide and Instructions.

The 69-page guide includes step-by-step instructions for registering each facility/property, including a bulk upload functionality – complete with a spreadsheet template – for the §30C, §45, and §48 credits. (The template is not yet available.)

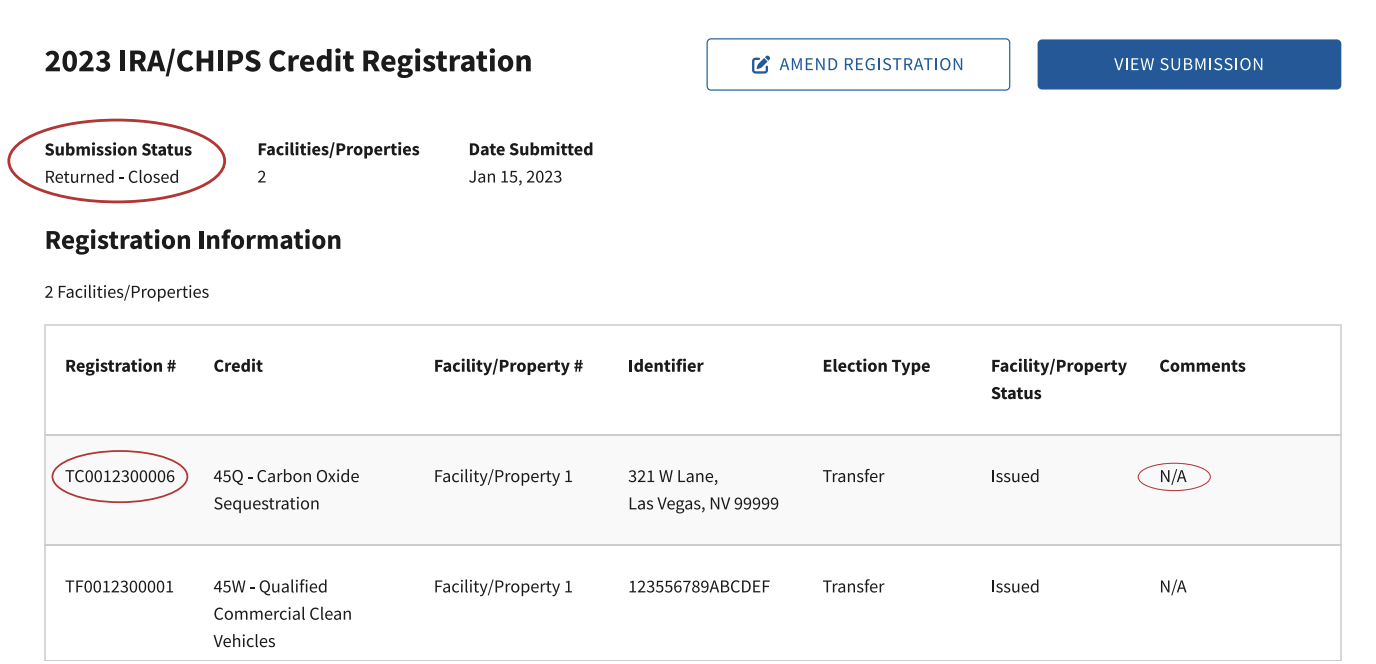

Takeaway 2: The IRS does not issue a registration number until the review is complete, and the IRS recommends at least 120 days for review

The IRS does not issue registration numbers until the application has been reviewed and marked as "Returned - Closed." The registration field will go from "pending" to an alpha-numeric string.

The guide counsels registrants to submit their pre-filing registration at least 120 days prior to when they plan to file their tax return. 120 days "should allow time for IRS review, and for the taxpayer to respond if the IRS requires additional information before issuing the registration numbers."

Importantly, 120 days is the IRS's current recommendation, suggesting this timeline could vary. Developers should prudently assume 120 days is the minimum.

Takeaway 3: Projects must be placed in service before submitting a registration

The guide states, "Before a facility/property can be registered to make a transfer election...that property or facility must have been placed in service no later than the date the registration is submitted." However, nothing prevents a registrant from getting a head-start on a draft submission.

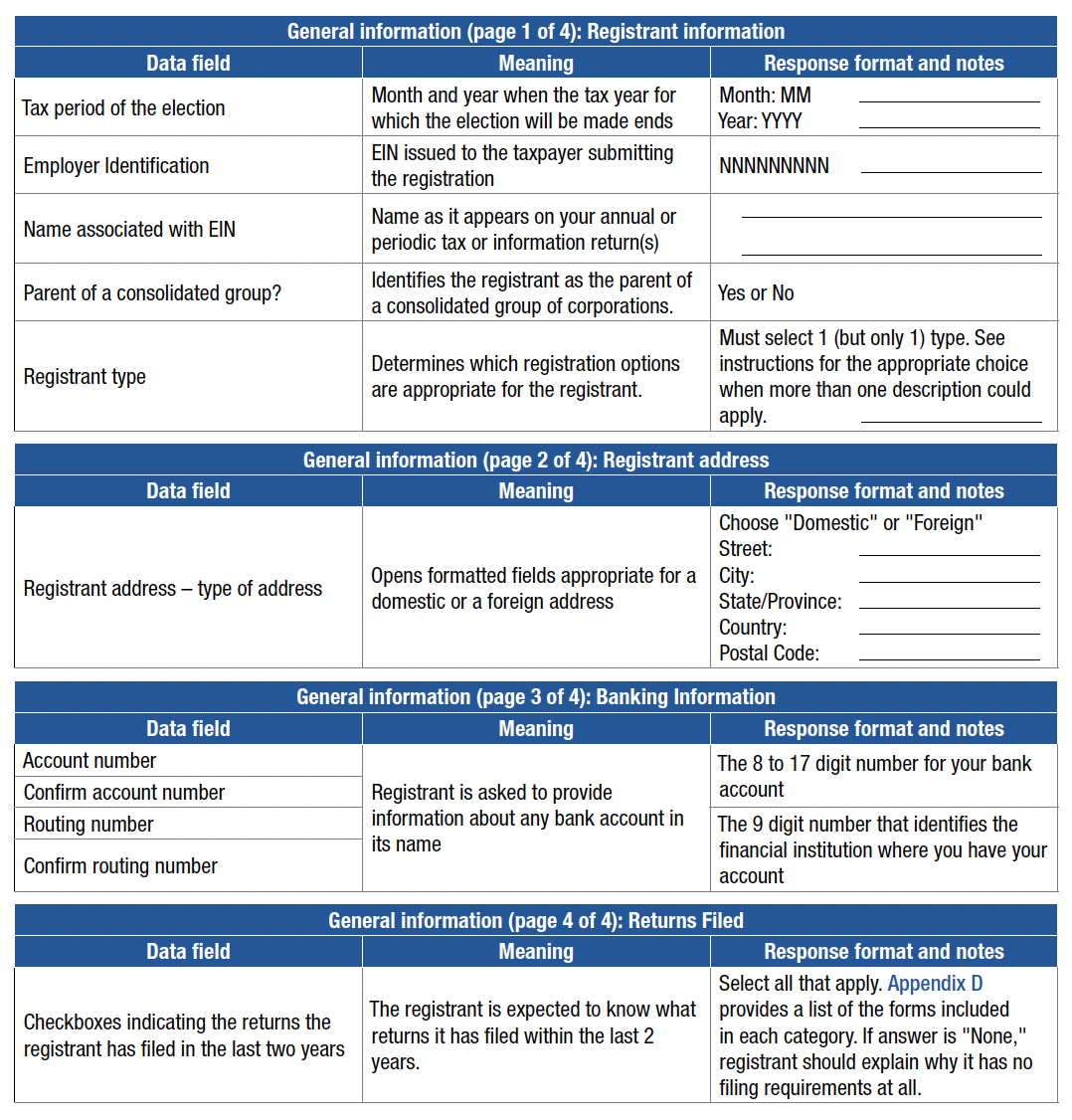

Takeaway 4: For every credit, the portal requires information about the registrant and allows for "additional information, if any"

All registrations must provide the following "general information" about the registrant:

- Tax period of the election

- EIN

- Name associated with EIN (as it appears on tax return)

- Parent of consolidated group?

- Registrant type (C corporation, sole proprietorship, etc.)

- Address

- Bank account information (account number, routing number)

- Type(s) of prior-year return(s) filed (Form 1120, Form 1040, etc.)

The portal also allows for "additional information, if any" as unformatted text. This field is optional but allows for the collection of "any additional information the registrant may wish to provide to identify a specific property or facility." In general, registrants should consider this field an opportunity to address any potential questions about their submission. Registrants should remove as much uncertainty in their application as possible.

Takeaway 5: The portal includes credit-specific requirements, including a "non-exhaustive" list of documentation

Depending on the type of credit a developer is registering, the portal will ask for specific data – the date construction began, for example – and a "non-exhaustive" list of supporting documentation.

According to the guide, "Supporting documents will usually be relatively short documents, such as permits, title documents, [and] sales documents (showing the name of the registrant, date of purchase, and identifying information such as serial numbers)." On several occasions, the user guide states, "Do not attach detailed project plans or contractual agreements."

The guide does not list requirements for credits that are pending:

- §45Y – Clean electricity production credit: Applies to facilities placed in service after 12/31/2024

- §45Z – Clean fuel production credit: Applies to transportation fuel produced after 12/31/2024

- §48E – Clean electricity investment credit: Applies to facilities placed in service after 12/31/2024

Scroll to a credit: §30C | §45 | §45Q | §45U | §45V | §45X | §45Y | §45Z | §48 | §48C | §48E

§30C – Alternative fuel refueling property credit

Data

- Subsidiary information (name, EIN)

- Date construction began (MM/DD/YYYY)

- Date placed in service (MM/DD/YYYY)

- Facility/property location (address, county, GPS coordinates)

- Source of funds ("N/A" for transfer election)

- Census tract

- Fuel type

- Additional information, if any

Supporting documentation

- Construction permit: A construction permit that clearly ties the facility/property to its physical location

- Equipment purchase: Equipment purchase documentation that shows the taxpayer as the buyer, identifies the seller, and specifically identifies the purchased property

- Operation permit: A permit issued by a government authority with jurisdiction over operation of alternative fuel refueling properties in the community where the facility/property is located

§45 – Renewable electricity production credit

Data

- Subsidiary information (name, EIN)

- Date construction began (MM/DD/YYYY)

- Date placed in service (MM/DD/YYYY)

- Facility/property location (address, county, GPS coordinates)

- Joint ownership (multiple owners?, taxpayer's % ownership)

- Attestation: not claiming §48

- Type of facility/property (geothermal, solar, wind, etc.)

- Additional information, if any

Supporting documentation

- Operating permit: Permits to operate from a utility (if connected to the grid). If not connected to the grid, electrical permits to operate from an authority having jurisdiction

- Description of the facility/property: A brief description of the facility/property signed by an executive-level representative of the taxpayer

- Independent engineer or commissioning report: Executive summary of an independent engineer or commissioning report

- Interconnection agreement: Executive summary of the interconnection agreement with the applicable utility, signed by an executive-level representative of the taxpayer

- Domestic content (if applicable): A document, signed by an authorized representative of the supplier of materials used for manufacture of components with regard to domestic content of such materials

§45Q – Carbon oxide sequestration credit

Data

- Subsidiary information (name, EIN)

- Choice of election (elective pay or transfer)

- Date construction began (MM/DD/YYYY)

- Date placed in service (MM/DD/YYYY)

- Facility/property location (address, county, GPS coordinates)

- Source of funds ("N/A" for transfer election)

- Sequestration activities (geological storage, direct air capture, etc.)

- Sequestration point (operator name, address)

- Additional information, if any

Supporting documentation

- Lifecycle analysis: Approved lifecycle analysis (LCA), or summary if the LCA is greater than five pages

- Proof of land use: Substantiation that the taxpayer will have use of the land where the sequestration facility is located, such as proof of land ownership or long term lease

- EPA permit application: Substantiation of EPA permit application

- Proof of sequestration wells: Proof of approval for geologic sequestration wells

- Permits: State and local government approvals or permits, including environmental approvals

§45U – Zero emission nuclear power production credit

Data

- Subsidiary information (name, EIN)

- Date construction began (MM/DD/YYYY)

- Date placed in service (MM/DD/YYYY)

- Facility/property location (address, county, GPS coordinates)

- Additional information, if any

Supporting documentation

- Operating license or permit: Copy of the license or permit issued to the taxpayer by an appropriate government agency authorizing the registrant's operations of the zero emission nuclear power facility

§45V – Clean hydrogen production credit

Data

- Choice of election (elective pay or transfer)

- Subsidiary information (name, EIN)

- Date construction began (MM/DD/YYYY)

- Date placed in service (MM/DD/YYYY)

- Facility/property location (address, county, GPS coordinates)

- Joint ownership (multiple owners?, taxpayer's % ownership)

- Type of facility/property (narrative description)

- Additional information, if any

Supporting documentation

- Operating permit

- Commissioning report

§45X – Advanced manufacturing production credit

Data

- Choice of election (elective pay or transfer)

- Subsidiary information (name, EIN)

- Date placed in service (MM/DD/YYYY)

- Facility/property location (address, county, GPS coordinates)

- Attestation: not claiming §48C

- Eligible components (solar energy, wind energy, etc.)

- Attestation: do you intend to make election under §45X(a)(3)(b)?

- Additional information, if any

Supporting documentation

- Ownership: Proof of ownership of the premises

- Permits: Permits to operate the manufacturing facility or to produce certain eligible components

If the §45X PTC relates to an offshore wind vessel, supporting documents should include the following:

- Coast Guard forms: Regarding the vessel (CG 1261 - Builder's Certification, CG 1340 - Bill of Sale, CG 1258 - Application for Certificate of Documentation)

- Official vessel number

- Hull identification number

- New or retrofitted vessel: Name of manufacturer or retrofitter, name of seller, name of buyer, vessel name

§45Y – Clean electricity production credit

Data

- Pending. Credit applies to facilities placed in service after 12/31/2024

Supporting documentation

- Pending. Credit applies to facilities placed in service after 12/31/2024

§45Z – Clean fuel production credit

Data

- Pending. Applies to transportation fuel produced after 12/31/2024

Supporting documentation

- Pending. Applies to transportation fuel produced after 12/31/2024

§48 – Energy credit

Data

- Subsidiary information (name, EIN)

- Date construction began (MM/DD/YYYY)

- Date placed in service (MM/DD/YYYY)

- Facility/property location (address, county, GPS coordinates)

- Additional information, if any

Supporting documentation

- Ownership: Proof of ownership of the facility/property

- Construction permit: Construction permit showing commencement of construction

- Operating permit(s): Permits to operate from a utility (if connected to the grid). If not connected to the grid, electrical permits to operate from an authority having jurisdiction

For §48 supporting documentation, the guide specifically states, "Do not attach contractual agreements. If the best support is a report on the planning or utilization of the tax credit property that includes an executive summary showing the ownership of the facility/property and bears the signature of the author of the report, attach the summary."

§48C – Qualifying advanced energy project credit

Data

- Subsidiary information (name, EIN)

- Date placed in service (MM/DD/YYYY)

- Additional information, if any

Supporting documentation

- Control number issued by the Department of Energy (DOE)

§48E – Clean electricty investment credit

Data

- Pending. Applies to property placed in service after 12/31/2024

Supporting documentation

- Pending. Applies to property placed in service after 12/31/2024

Takeaway 6: Developers will need a registration number for each facility/property

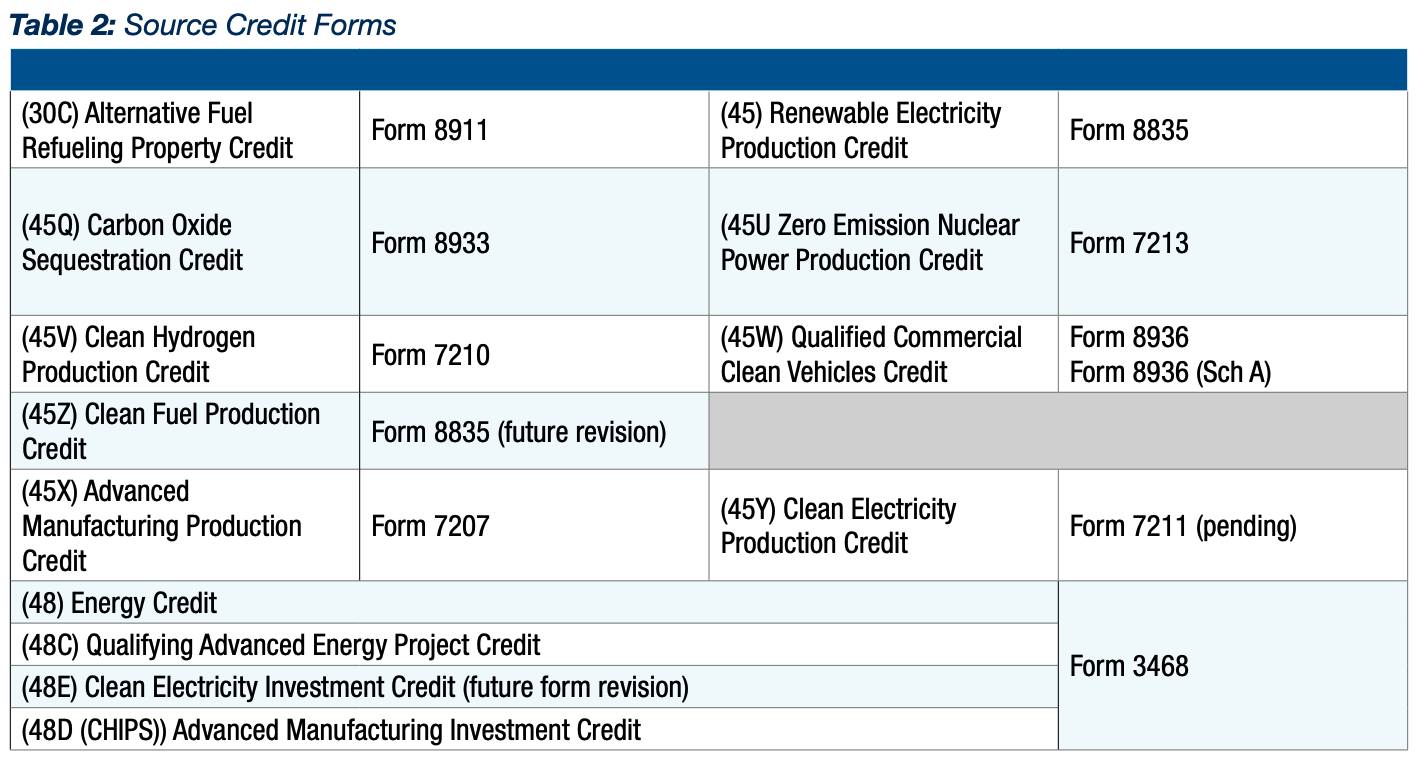

Developers will need a separate registration number for each facility/property, depending "on how the credits must be computed and reported on the source credit form and Form 3800."

The source forms for each credit are as follows:

Transferable tax credit source form links

Here are links to available source credit forms for transferable tax credits. Some forms, like 7213, are in draft as of this post (December 11, 2023):

- §30C (Alternative fuel refueling property credit) – Form 8911

- §45 (Renewable electricity production credit) – Form 8835

- §45Q (Carbon oxide sequestration credit) – Form 8933

- §45U (Zero emission nuclear power production credit) – Form 7213. As of December 2023, this form is draft

- §45V (Clean hydrogen production credit) – Form 7210. As of December 2023, this form is draft

- §45Z (Clean fuel production credit) – Form 8835. As of December 2023, this form is pending a future revision

- §45X (Advanced manufacturing production credit) – Form 7207

- §45Y (Clean electricity production credit) – Form 7211. As of December 2023, this form is pending

- §48 (Energy credit) – Form 3468

- §48C (Qualifying advanced energy project credit) – Form 3468

- §48E (Clean electricity investment credit) – Form 3468. As of December 2023, this credit will involve a future form revision

Takeaway 7: A registration number does not mean a registrant qualifies for a credit of any specific amount

The guide reminds registrants that the portal demonstrates an "intent to monetize" a credit. A registration number, in other words, "does not mean that the registrant has been determined to qualify for a credit of any specific amount."

To monetize a credit, a developer must meet other requirements to make a valid election, including:

- Reporting the credit on the applicable source credit form (see list above)

- Completing Form 3800

- Fully executed transfer election statement

- Attaching these forms to a timely-filed tax return

Interested in learning more?

To learn more about the pre-registration portal or the IRA tax credit market it supports, please contact Reunion.