A Real-World Case of Investment Tax Credit Recapture

Lessons from a rare instance of the IRS recapturing energy tax credits

This article — authored by Andy Moon and Denis Cook — was originally published in the May 4, 2026, issue of Tax Notes Federal.

A recent regulatory filing reveals one of the first publicly documented cases of the IRS recapturing transferable clean energy tax credits. More than $24 million in solar investment tax credits originally purchased by Missouri-based Enterprise Financial Services Corp. (EFSC) were recaptured because of a change in project ownership resulting from the seller’s bankruptcy. The case illustrates how transferable tax credits can encounter financial distress, and how comprehensive due diligence and risk management can ensure that buyers are made whole.

The Background

The Inflation Reduction Act created transferability, which has allowed banks and other corporations to access the economic benefits of energy tax credits without navigating the complexities of traditional tax equity. But transferability did not alter recapture rules. Certain transferable tax credits, namely section 48 and section 48E ITCs, remain subject to recapture under section 50(a) if the underlying clean energy project changes ownership or ceases to be investment credit property within five years of being placed in service.

While tax credit sellers typically agree to indemnify tax credit purchasers for any loss event including recapture, the liability ultimately rests with the purchaser. Purchasers of ITCs must carefully screen for and protect against recapture risk. With that said, IRS recapture of transferable credits is very rare. Given the high economic stakes, market participants take special care to avoid situations that could lead to a recapture event.

What Triggered Recapture for EFSC

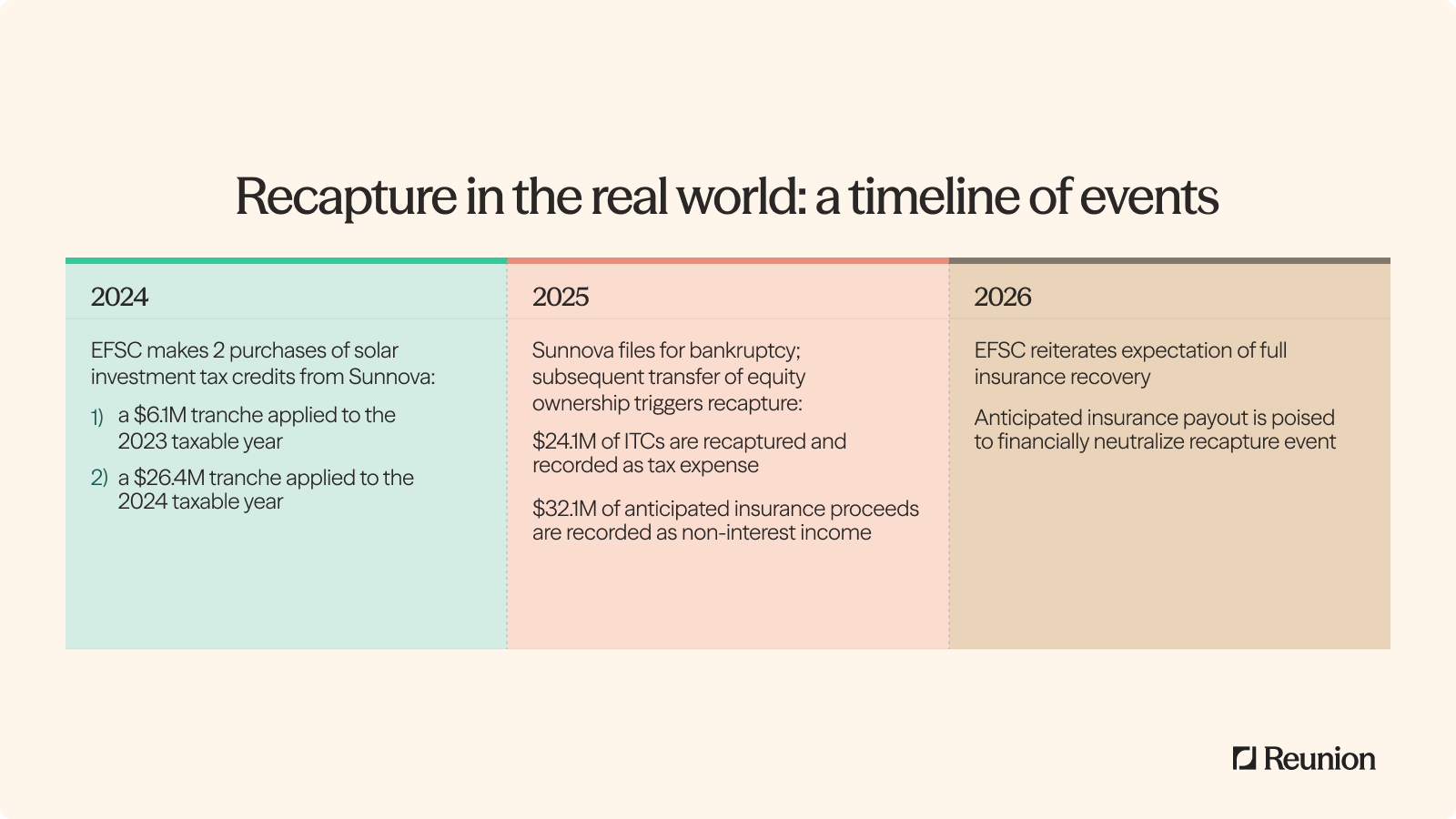

In September 2024 EFSC executed a tax credit purchase agreement with Sunnova Energy, a residential solar developer. The tax credit purchase agreement covered about $6 million of ITCs from 2023 and $26.4 million of ITCs from 2024.

Less than 10 months later, in June 2025, Sunnova filed for chapter 11 bankruptcy protection in the U.S. Bankruptcy Court for the Southern District of Texas. The resulting liquidation of the underlying project assets triggered IRS recapture rules — not because the solar assets were physically impaired, but because the ownership change itself constituted a recapture event.

Importantly, the 2023 and 2024 ITCs that EFSC purchased were likely from projects wholly and directly owned by Sunnova. When Sunnova entered bankruptcy, creditors were able to force a change in asset ownership, thereby triggering recapture.

In contrast, buyers of Sunnova tax credits held in tax equity partnerships may not have been subject to recapture. Treasury regulations stipulate that changes of control that create recapture are borne at the partner level and allocated to the partner, as opposed to being borne by the partnership (shielding the impact to the tax credit purchaser). It is also possible that the tax equity partnerships had forbearance agreements in place to mitigate the risk of recapture.

EFSC was required to relinquish most of the previously claimed credits — a recapture of $24.1 million. The recapture was only partial because under section 50(a), the clawback percentage starts at 100 percent in year 1 and declines by 20 percentage points annually, reaching 20 percent in year 5. Because the underlying solar projects had been placed in service in 2023 and 2024 — EFSC and Sunnova are both calendar-year filers — the recapture percentage appropriately appears to have been between 60 percent and 80 percent.

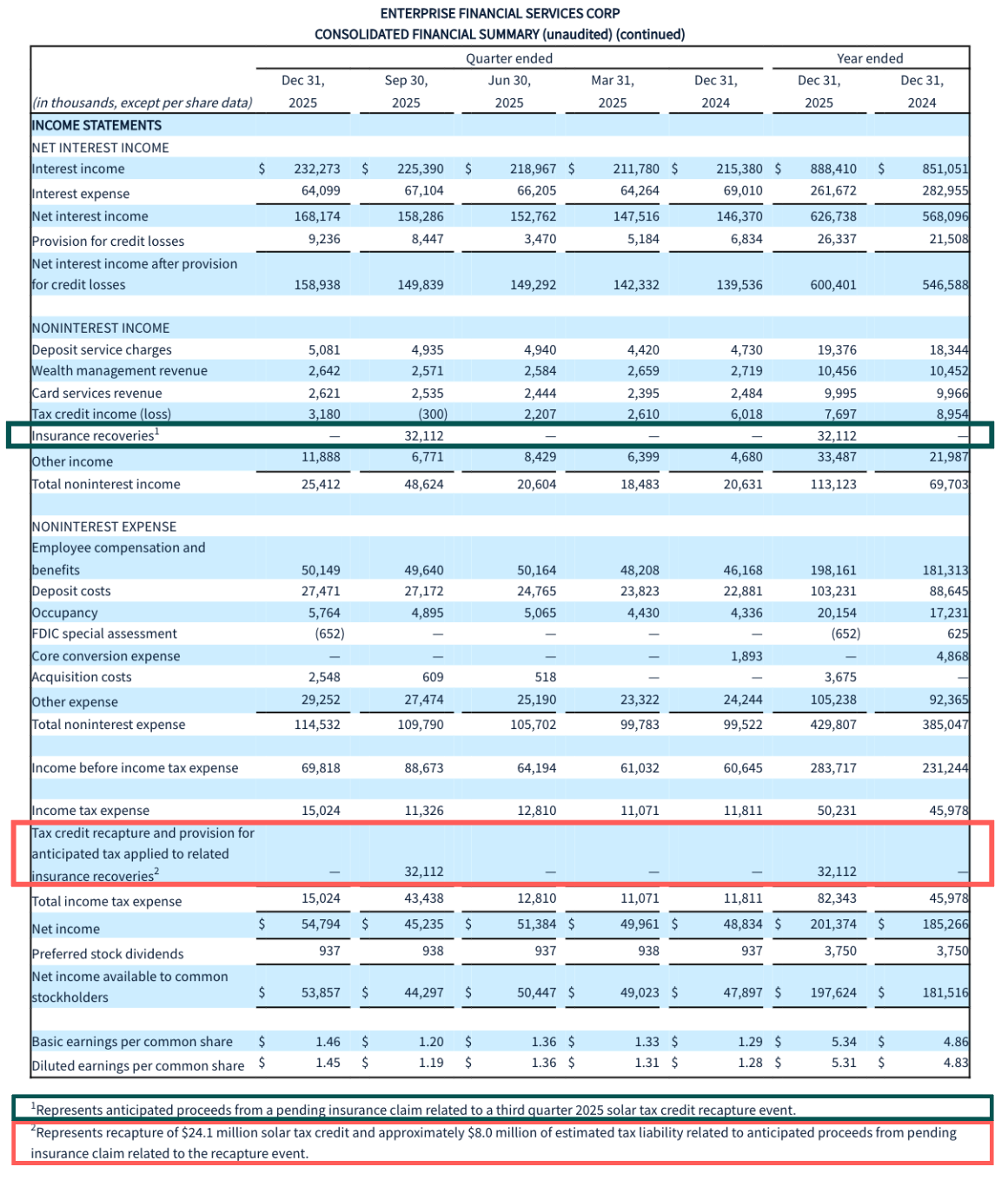

In its financial records for the third quarter of 2025, EFSC recorded the $24.1 million recapture as a portion of its income tax expense for the quarter. This expense is captured in the entries in Figure 1, seen in the company’s consolidated financial summary from January.

The Mitigation

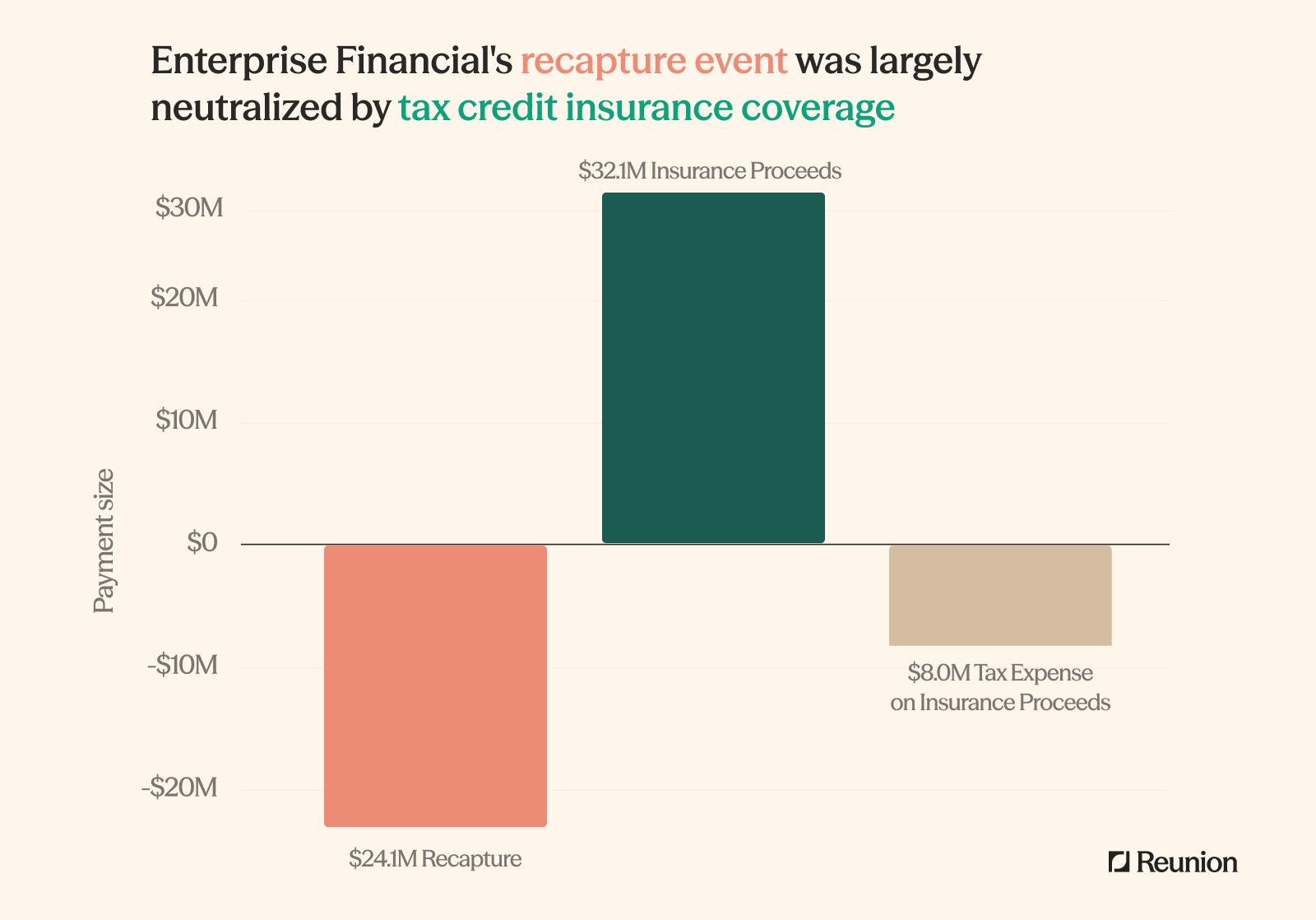

The tax credit purchases EFSC closed in 2024 included tax credit insurance, which covered recapture risk — a decision that worked out well for the corporation. Following the recapture, the company recognized approximately $32.1 million in anticipated insurance proceeds. These proceeds, highlighted in Figure 1, encompassed the $24.1 million value of the forfeited tax credit, as well as an additional $8 million to cover other costs. EFSC recorded the full $32.1 million insurance proceeds as non-interest income for the third quarter of 2025.

This amount was taxable, and the company characterized an $8 million portion as a tax expense related to the proceeds. The $24.1 million recapture event was therefore largely neutralized by the anticipated insurance payout and the taxes owed on it, as shown in the sequenced bars in Figure 2. In the company’s full-year 2025 results, EFSC management characterized the recapture event as nonrecurring and indicated that the insurance was expected to fully offset the economic impact.

Key Takeaways for Managing Recapture Risk

EFSC’s recapture event raises a practical question for tax credit buyers: How can recapture risk be managed in practice? Here are some practical takeaways from the EFSC case:

• Understand the sellerʹs financial situation and whether contractual terms mitigate recapture risk in the event of bankruptcy or foreclosure. As the ESFC case shows, recapture can be triggered by a direct change of control of the underlying project assets. Buyers should assess the bankruptcy or foreclosure risk of the seller entity, and whether partnership structures or forbearance agreements are in place to mitigate risk of change in ownership in the event of a liquidation.

• Tax credit insurance can protect against downside risk when uncertainty exists around a seller’s ability to pay indemnity claims. EFSC made a prudent decision to secure an insurance policy with sufficient coverage to zero out the economic effects of the recapture, even after accounting for taxes that needed to be paid on the insurance proceeds. We have observed a wide range in limits of liability — from 30 to 130 percent of the tax credit amount. In this case, a low limit of liability would have led to a substantial financial loss for EFSC.

• Understand contract terms in the event of financial stress. Diligence should look at terms that govern downside scenarios. For example, buyers should assess what happens to underlying assets if the sponsor goes bankrupt. If project-level debt is present, buyers should understand if there is a forbearance agreement in place during the recapture period, to avoid a recapture triggered by a debt foreclosure.

• Not all credits are subject to recapture. While ITCs typically provide superior pricing, they come with the risk of section 50 recapture. Recapture incidents are rare, but the case of EFSC shows that it can happen. Corporate buyers that want to avoid recapture rules entirely should consider production tax credits, which generally trade at a premium to ITCs but are not subject to section 50 recapture.

Looking Ahead

Although the transferable tax credit market nearly doubled from 2024 to 2025, acquisition and due diligence practices are still being shaped by early cases like this one. EFSC’s experience is a useful data point: The statutory risk of recapture is real, the tools to mitigate it work, and properly structuring a transaction makes the difference between an accounting event and an economic loss.