What Should Corporations Expect to Pay for IRA Tax Credits?

In 2023, IRA tax credits traded in fairly narrow pricing bands defined by risk and scale. Reunion believes risk and scale will continue to drive pricing in 2024, though pricing bands will widen

2023, the first full year of the Inflation Reduction Act, is officially behind us. As year-end approached, transactions closed in lockstep with the release of further IRS guidance and other market-enabling milestones.

With the turn of the calendar, we wanted to share our 2023 pricing observations and 2024 pricing predictions.

Overview of tax credit transfer pricing

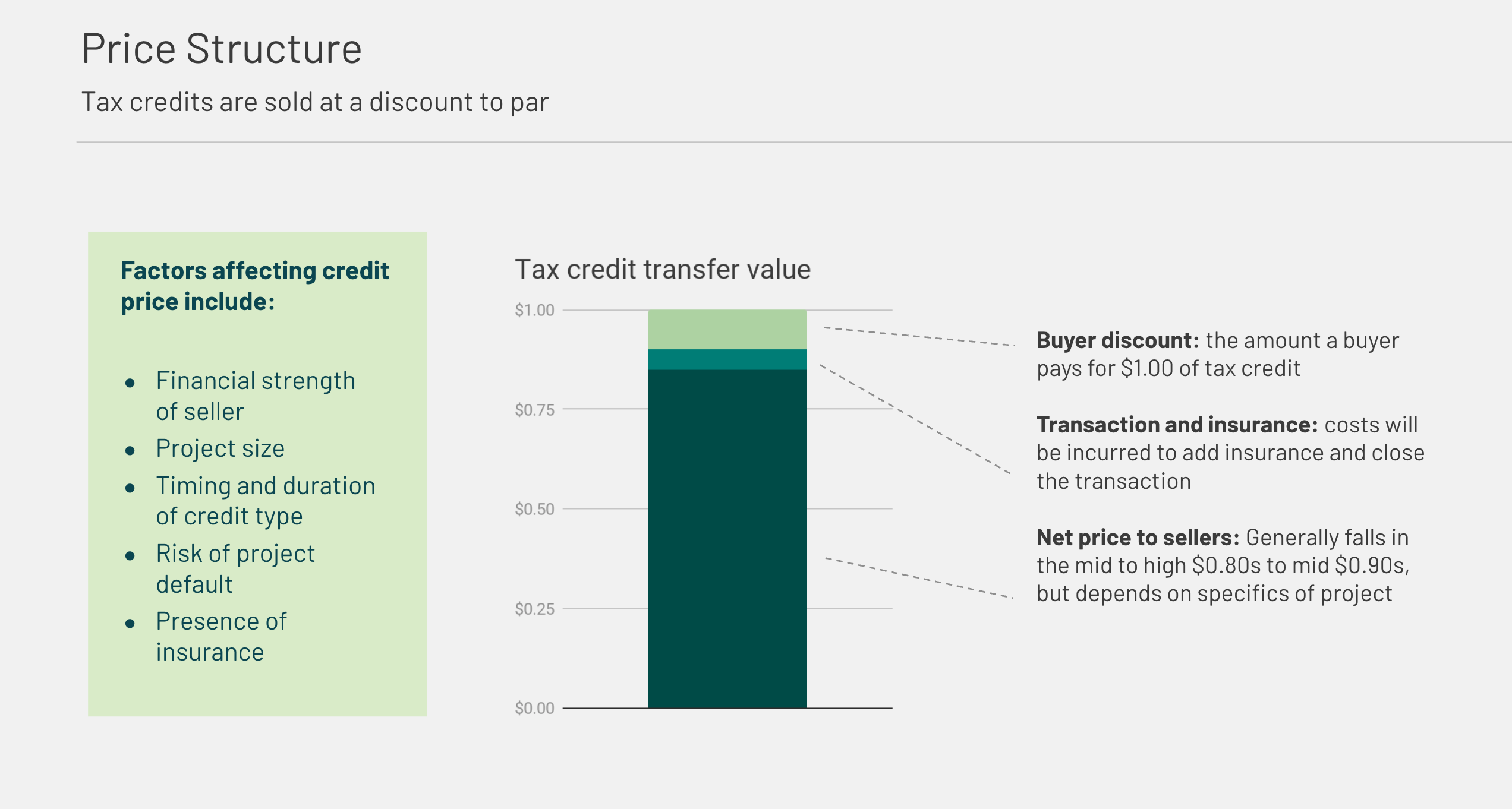

Transferable tax credits are sold at a discount per $1.00 of credit, and the discount is the primary incentive for a buyer to enter into a tax credit transaction. A corporation, for example, buying credits for $0.90 would pay $90M in cash in exchange for $100M in tax credits. The company would realize $10M of savings, which is not treated as gross income and, therefore, not subject to taxes.

The net price the seller receives for the credit is typically the buyer’s purchase price less the cost of tax credit insurance and transaction fees (e.g., fees paid to a platform or facilitator such as Reunion).

Looking back on 2023 pricing

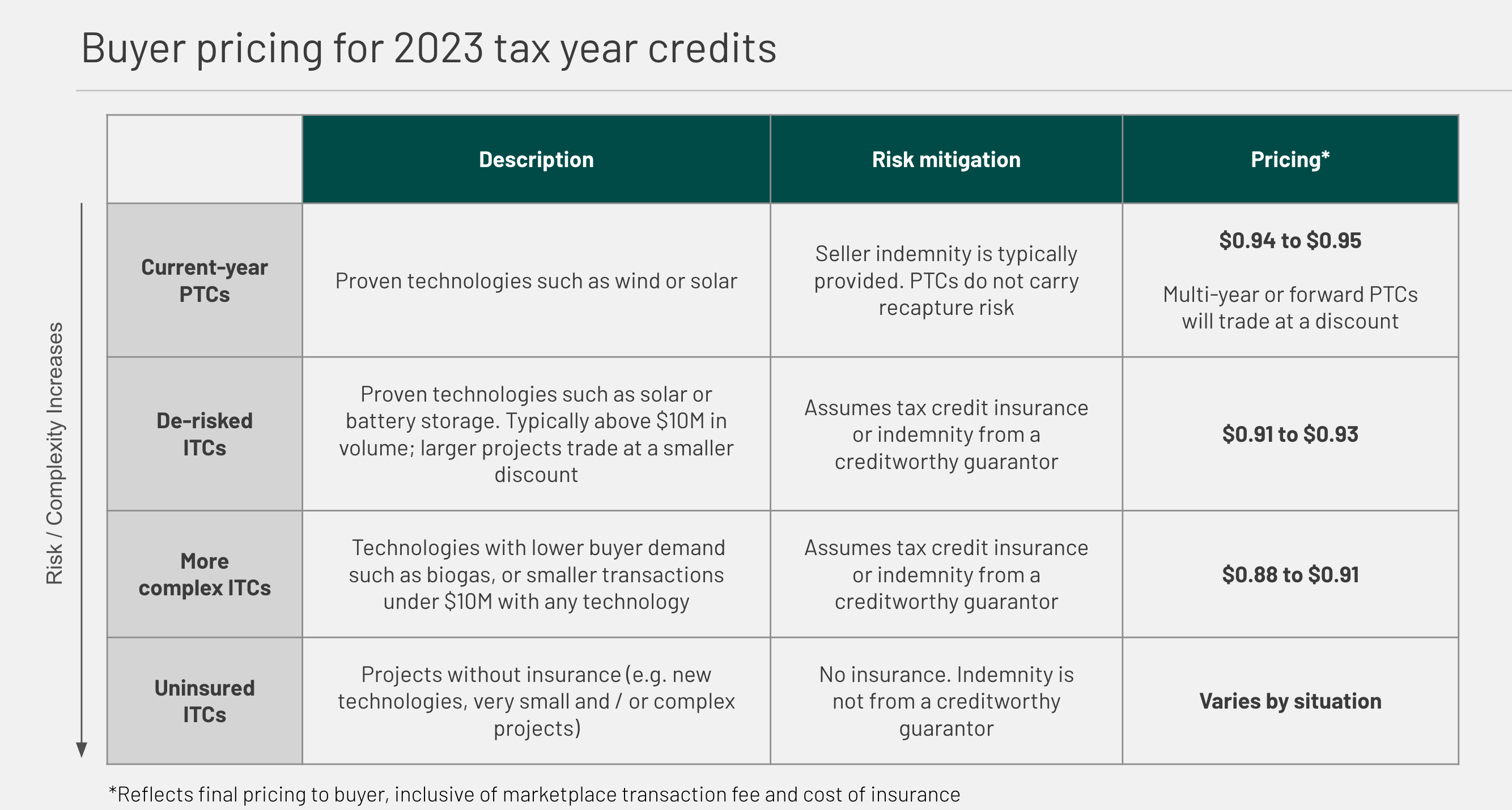

The market for transferable tax credits remains nascent, as transactions started in earnest following Treasury guidance on June 14, 2023. We have found that offers (and closed transactions) for 2023 tax-year credits are within fairly narrow pricing bands based on risk/complexity.

Across these pricing bands, projects with more scale have tended to drive smaller discounts.

§45 production tax credits (PTCs)

§45 PTCs are the simplest transaction to execute, as the credit is straightforward to validate. Buyers commonly review production reports and related documents to confirm that electricity was produced from an eligible project type and sold to an unrelated third party. Importantly, §45 PTCs do not carry recapture risk.

Current-year PTCs have been trading in the $0.94 to $0.95 range. Buyers who have committed to paying for PTCs that will be generated in future tax years have received larger discounts.

For a deeper understanding of how pricing dynamics and forward commitments affect transaction structures, refer to our Section 45 PTC transfer case study, which explores a real-world transaction and deal specifics.

§48 investment tax credits (ITCs)

§48 ITCs carry more complexity. The buyer will need to validate the cost basis used to calculate the ITC as well as the tax year that the project was placed in service:

- Cost basis: If the cost basis has not been properly calculated, the credit can be subject to disallowance by the IRS

- Placed-in-service date: The project must be placed in service in the desired tax year; if a project is placed into service in a later-than-expected tax year, the tax credits can be carried back up to three years but the process is not straightforward

§48 ITCs are subject to recapture rules, which require that (1) the property remains a qualified energy facility for five years, and (2) there is no change in ownership for five years. If these conditions are not met, the IRS will recapture the unvested portion of the ITC (the ITC vests equally over a five-year period).

2023 summary pricing

The discount is only one financial metric. Many buyers are also interested in timing of cash flows

While the discount is often the first question that we receive about tax credit pricing, it is not the only metric to evaluate the financial return of a tax credit transfer.

The timing of cash flows from a tax credit transfer is also important to buyers. Treasury’s June 2023 guidance clearly states that a “transferee taxpayer [i.e., a tax credit purchaser] may also take into account a specified credit portion that it has purchased, or intends to purchase, when calculating its estimated tax payments.”

Below are several examples of how timing of a tax credit purchase can impact returns (assuming buyers purchase credits for $0.90):

Finally, buyers commonly request to delay payments for a tax credit transfer to line up with their quarterly estimated tax payments. This is a key negotiation point, as sellers prefer to get paid as soon as possible after credits are generated.

Going forward, we expect delayed payment terms to result in a smaller headline discount for the buyer, since the seller will want to be compensated for their cost of capital.

In September 2023, we wrote a detailed discussion on buyer returns.

Looking forward to 2024 pricing

As we consider macro-level tax credit pricing in 2024, two major themes come to mind: increased credit supply and market bifurcation. The former is an emerging trend, while the latter extends from 2023.

Increased tax credit supply

Early analysts predicted that discounts would shrink as the market matures. We do not believe this is a foregone conclusion.

There is a significant increase in supply of clean energy tax credits for the 2024 tax year; Reunion’s digital platform already lists over $3 billion in tax credit opportunities for the 2024 tax year. This increased volume of tax credits looking for buyers will put downward pressure on pricing, at least until buyer demand grows commensurately.

In contrast, the supply of 2023 tax year credits was constrained, with a relatively small number of projects for buyers to invest in.

Continued market bifurcation

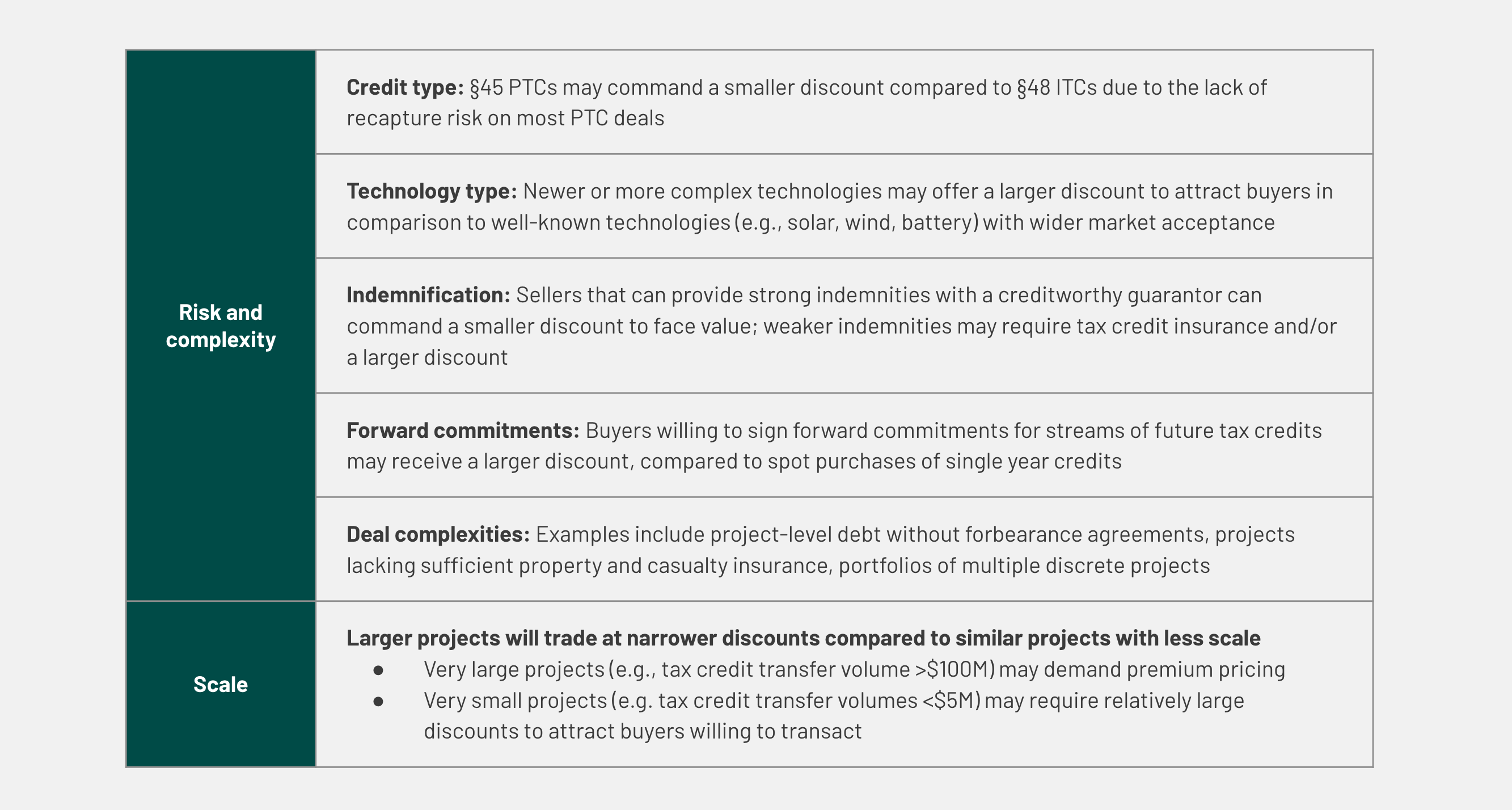

Heading into 2024, we believe that the market will bifurcate: certain credits will demand premium pricing while other credits (e.g., uninsured ITCs without an indemnity from a creditworthy guarantor) will need to offer a deep discount and/or novel ways to mitigate risk.

Common project types that will garner premium pricing include:

- §45 PTCs from solar and wind with an indemnity from a creditworthy guarantor or tax credit insurance. Certain §45X credits from advanced manufacturers will trade at a premium, if the size of the credit is significant and the seller provides a creditworthy guarantee or tax credit insurance

- §48 ITCs from sizable solar or battery projects (larger transaction sizes will demand a premium price), with an indemnity from a creditworthy guarantor or tax credit insurance

- §48 ITCs from solar or battery projects sold out of tax equity partnerships with experienced sponsors and tax equity investors

2024 summary market drivers

Overall, our view is that risk/complexity and scale will be the two main drivers of pricing. Projects that present buyers with lower risk and greater scale will, ultimately, enjoy higher pricing.

How Reunion helps

The Reunion team is available to meet with buyers looking to purchase 2023 or 2024 tax-year credits, and is also available to answer questions for those looking to learn more about the rapidly growing tax credit transfer market.

Please find us on LinkedIn or email us at info@reunioninfra.com.