Alessio De Falcis

January 22, 2025

Residential solar investment tax credits: A $6B market in 2025

ITCs from "resi" solar present an attractive investment opportunity for large corporates. The credits can be purchased in nine-figure tranches and are exempt from PWA requirements.

For Buyers

The current state of the residential ("resi") solar market

Residential, or "resi," solar, like much of the clean energy industry, has experienced its fair share of ups and downs in the past several years. Despite the obstacles, the industry remains resilient, and its leaders are more committed than ever to continually improving the ecosystem.

Poised for strong growth

2024 was a period of contraction for the resi solar industry, with an estimated 26% decline in installed capacity. This decline is largely attributable to a higher-for-longer interest rate environment that significantly impacted the cost of capital across the value chain, coupled with the phase out of NEM 2.0 in California.

However, the resi solar market is expected to grow significantly through 2030.

Increasingly financed through third-party ownership (TPO) arrangements

The bulk of resi solar is sold to customers as a financed product. Just as with other consumer finance asset classes such as auto, financing options make the product more accessible to a majority of homeowners. Resi financing comes in two flavors: loans and third-party ownership.

For much of the past decade, the resi solar market was dominated by loans. However, due to the combined effects of rising interest rates and the introduction of ITC bonus credit adders only available to TPO, the industry has shifted to a largely TPO-heavy financing model, which generate ITCs that are eligible for transferability.

Considerations for buyers evaluating resi solar third-party ownership (TPO) tax credits

Exempt from prevailing wage and apprenticeship (PWA) requirements

Resi solar is exempt from PWA given the size of the systems (generally 5-30 kilowatts), which are well under the 1 megawatt threshold. This in turn reduces complexity and scope of diligence (and can drive cost savings) relative to other projects requiring PWA compliance.

Easily structured around quarterly payments in arrears

Large resi solar developers operating at scale are placing systems in service on a daily basis, resulting in the creation of sizable portfolios of projects that are available for sale to tax credit buyers on a regular, recurring basis — often quarterly. This structure benefits buyers seeking to make payments quarterly in arrears to align with quarterly estimated tax payments, maximizing buyers’ internal rate of return.

Minimized placed-in-service risk

Project delays typically impact only a portion of a resi portfolio. In contrast, a large-scale project that delays placed-in-service beyond year-end has a binary risk that 100% of credits slip to the subsequent tax year.

Geographical diversity

Resi solar credit opportunities are sold as portfolios, which consist of many projects that are likely to be distributed across multiple geographies (i.e., across several states, territories, or counties).

This geographic distribution provides a natural hedge against unexpected weather or other events impacting all projects / tax credits in the portfolio (including unforeseen delays or recapture risk — see more below).

Recapture risk mitigants

Before jumping right into risk mitigants, let’s first explore tax credit recapture itself — what are the requirements?

The IRS requires that:

- Property remains a qualified energy property for five years after being placed in service. A property ceases to be a qualified energy property when an asset is disposed of, or otherwise ceases to be an investment credit property (i.e., destroyed and not rebuilt, abandoned, or repurposed to sell something other than electricity).

- There is no change in ownership of property during the five-year recapture period, which commences once a project has been placed in service.

Should a project fail to meet either of these requirements, the IRS will recapture the unvested portion of the ITC, which vests equally over a five-year period — 20% of the total ITCs claimed will vest on each anniversary of the project’s placed in service date.

With recapture risk now defined, how does resi solar measure up and what mitigants exist?

- The most common reason for a solar project ceasing to be a qualified energy property is the destruction of the project coupled with a failure to rebuild. Given resi solar projects are highly dispersed in location, systemic destruction is extremely unlikely. Furthermore, even if projects within a portfolio are destroyed, there is no mandated rebuild time following an insurable event — the developer must simply demonstrate intent to rebuild and place projects back in service.

- Resi solar customer agreements (leases/PPAs) commonly contain clauses that prohibit a change in ownership during the recapture period (i.e., customer cannot buyout system in first five years). Customers are generally contractually allowed to prepay contract at any time and/or request a contract transfer and reassignment to another homeowner, however, neither of these events constitutes a change in ownership.

As a tax credit buyer, conducting appropriate due diligence on all aspects of the transaction, including a review of items such as P&C insurance limits/exclusions, ongoing operations and maintenance support, and customer agreements, is paramount.

Reunion supports its customers through every step of the transaction process, including due diligence, and we invite all interested parties to reference our Section 48 ITC due diligence guide.

Market sizing and opportunity

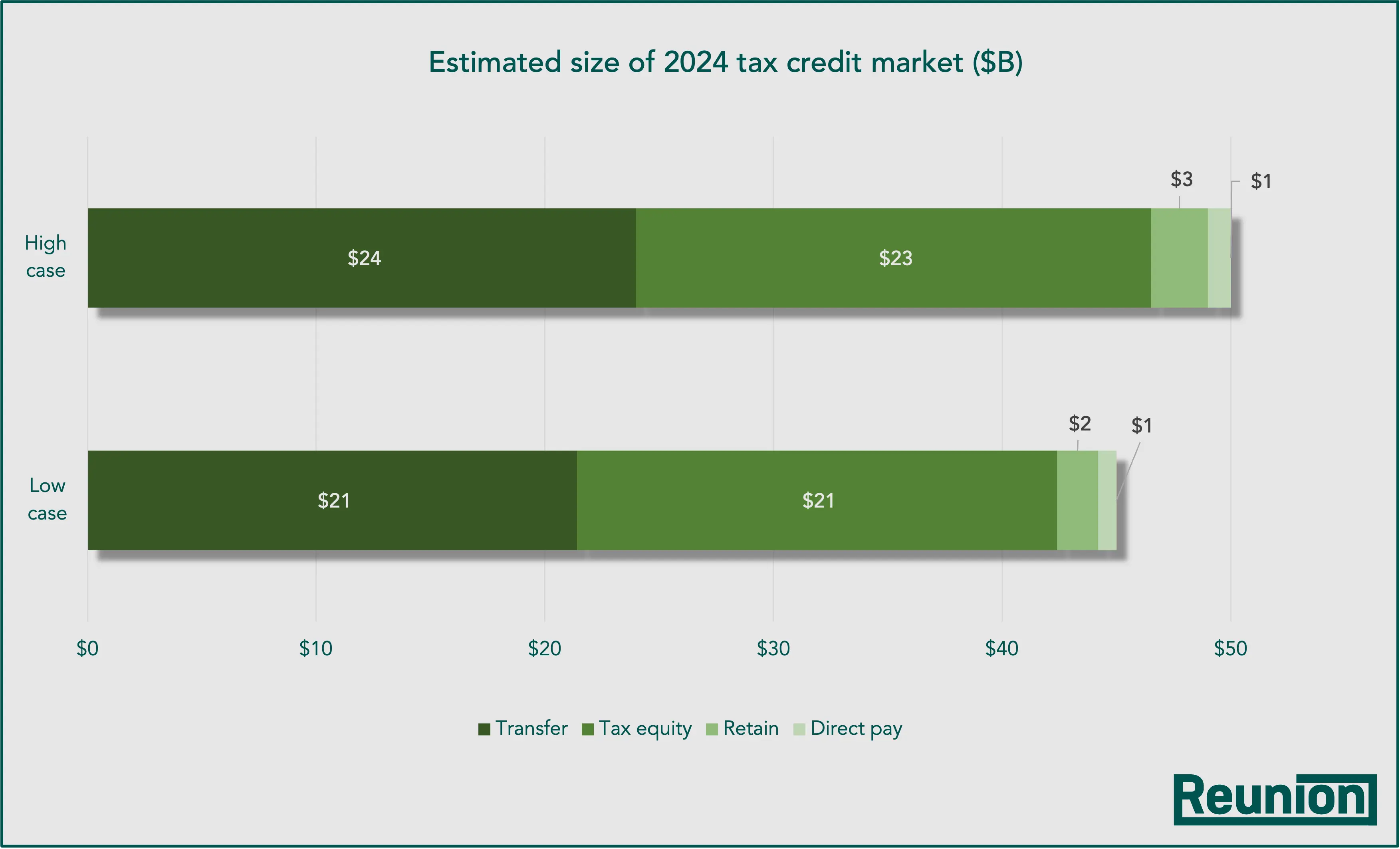

Using back-of-the-envelope math and conservative assumptions, we estimate that the resi solar market will generate approximately $6 billion in 2025 investment tax credits and continue to grow. Of course, not all of these ITCs will be transferred, as some developers may pursue traditional tax equity, retain the credits, or utilize direct pay, but as we note in our Q3 2024 market intelligence report, we expect roughly half of the clean energy tax credit market to be transferred.

This represents a sizable market for tax credit buyers with a strong potential for repeat transactions. The team at Reunion is excited to be working with many of the largest and most established resi solar developers in the space, and we look forward to supporting new and existing buyers in every step of the transaction process.

Frequently asked questions

Business model

What is the most common business model for resi solar developers operating at scale?

There are many different business models, but most scaled resi solar developers operate using an EPC/Sales Dealer model.

How does an EPC / Sales Dealer model work?

Under this model, the developer partners with EPCs (licensed contractors performing engineering, procurement and construction work) who design and install solar projects that are in turn purchased by the developer.

Occassionally, EPCs also employ salespeople to acquire new customers (i.e., homeowners). Most often, though, this work is subcontracted out to sales dealers employing individual sales reps at scale.

Customer acquisition

Who acquires new customers and what is the process?

Sales reps acquire new customers (typically single-family homeowners) via door-to-door sales. This conversation often involves looking at homeowner’s current utility bill and comparing future utility payments with and without solar. Developers often require upfront customer savings before moving forward with a customer and engaging an EPC.

How does a sales rep get paid?

Sales reps are paid a commission on each successful sale by the sales org employing him/her. EPC knows what it will get paid by the developer for each system configuration in each market and what it is willing to install the system for (the “redline”). Any amount over the redline goes to the sales rep as commission.

System construction and purchase

How is the system installed?

EPC procures equipment that is compliant with developer’s approved vendor list (including any manufacturer warranty requirements), designs and installs system subject to developer’s guidelines, and works with local utility to ensure system achieves permission to operate (PTO).

Who estimates the system production?

Developer typically partners with one or multiple approved system design tool platforms that are integrated into its systems. The production estimation engine behind these tools is often tested and validated by an independent engineering firm and published in a report.

What happens once the system is installed?

Developer “acquires” fully installed system from EPC at pre-determined price based on system configuration and utility market, aiming to achieve a minimum project-level rate of return on expected system cashflows (customer payments, net of expenses). Developer typically funds EPCs in two milestone payments to align incentives — a majority at install complete and the balance at PTO.

Developer third-party ownership

Who owns the system?

Developer owns the system and executes a lease or PPA with the homeowner that governs the monthly billing and terms of service which commonly include an operations and maintenance (O&M) obligation and a performance guarantee (PeGu) obligation.

Who is responsible for system repairs?

Developer is liable for any operations and maintenance (O&M) issue or system underperformance that is not the direct fault of the customer.

Alessio De Falcis

December 16, 2024

The IRA is Working – and Garnering Bipartisan Support

The Inflation Reduction Act has had a significant impact on clean energy deployment in the U.S., leading to accelerated growth among solar, wind, battery storage, and other clean energy technologies.

For Buyers

For Sellers

The IRA has fueled clean energy deployment

The Inflation Reduction Act has had a significant impact on clean energy deployment in the U.S., leading to accelerated growth among solar, wind, battery storage, and other clean energy technologies:

- The two-year post-IRA period has seen $89 billion in investment in new, US-based clean energy manufacturing, versus $22B in the two years preceding the IRA (see Figure 1)

- Investment in clean energy production and industrial decarbonization is $161 billion since the passage of the IRA, a 43% increase from the comparable pre-IRA period

Americans overwhelmingly support clean energy

Clean energy is now a major part of the US economy, employing over 3.5 million workers. Since 2020, the clean energy industry has added 400,000 new jobs, significantly outpacing the rest of the energy sector.

The federal solar investment tax credit was first passed under the George W. Bush administration via the Energy Policy Act of 2005, and for the last 20 years there has been a looming threat that this tax credit will be removed. But it has persisted, because it has been highly effective in driving solar adoption, and solar energy is extraordinarily popular among Americans.

The IRA has growing, bipartisan support

Similarly, the Inflation Reduction Act has bipartisan support:

- In August 2024, a group of 18 Republican Congress members wrote to a letter to Speaker Mike Johnson saying: “Prematurely repealing energy tax credits, particularly those which were used to justify investments that already broke ground, would undermine private investments and stop development that is already ongoing.” Speaker Johnson responded that when making changes to the IRA, “you’ve got to use a scalpel and not a sledgehammer.”

- The total clean investment of $493 billion in the two-year post-IRA period has flowed into all 50 states, but over half of that has gone to Republican states

We have reason for optimism that the major provisions in the Inflation Reduction Act will persist. It’s unlikely that a majority of Congress will support a significant repeal of a law that is driving new jobs and significant investments in clean energy. Repealing the IRA after it has been in force for over two years will also upend many private businesses, which have made billions in investments under the anticipation that the law will be in force for a decade, if not substantially longer.

Furthermore, the final house race was called December 2nd, landing at 220 Republican seats and 215 Democrat seats. Given that 218 votes are required to form a majority and pass legislation, Republicans have a very thin margin for defections - only two.

Buyers and sellers remain active in the market for 2025 tax credit and beyond

In the tax credit transfer space, we continue to see a heavy dose of activity that is, in fact, ramping up, particularly from buyers wanting to lock in 2024 and 2025 tax credits before any potential changes.

The team at Reunion remains highly optimistic about a clean energy future and stand ready to support all existing and new customers.

Reunion

November 15, 2024

Transferable Tax Credits Comprehensive Guide 2026

Explore transferable tax credits comprehensive guide, including an in-depth analysis of buying, selling, due diligence, and risk management strategies

For Buyers

For Sellers

Introduction

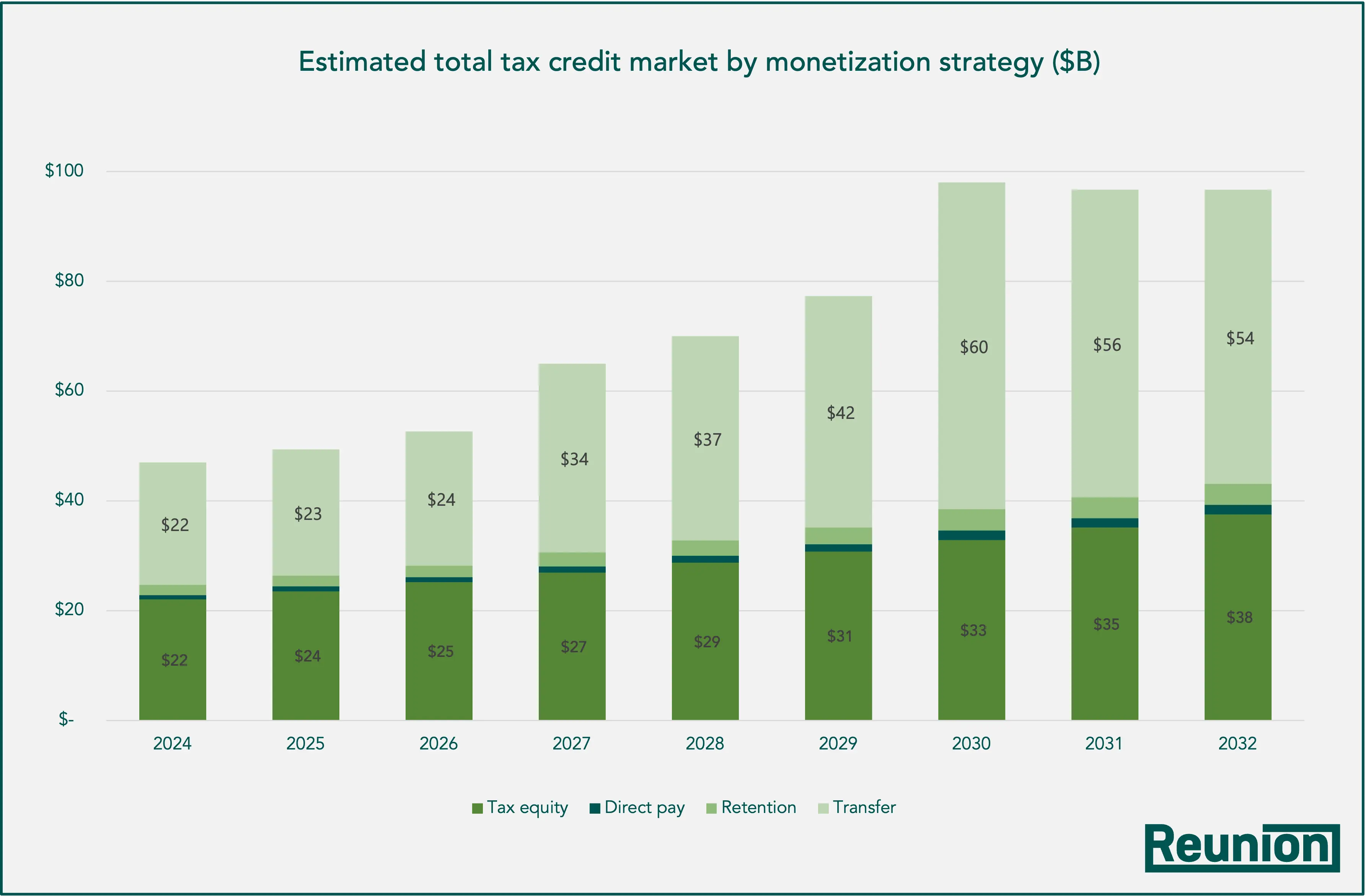

The Inflation Reduction Act of 2022 (IRA) was a landmark piece of legislation designed to accelerate the United States’ transition to clean energy. A key innovation of the IRA was the introduction of transferable tax credits, which allows clean energy developers to sell federal tax credits to third parties. This was a significant shift from the prior system, which relied heavily on a small number of large financial institutions for clean energy financing. Transferable tax credits have proven to be a game-changer, fulfilling their promise by broadening the pool of investors and helping to streamline project financing. Since the Department of the Treasury's regulations were finalized, the market has expanded rapidly, with an estimated over $25 billion in tax credits transferred in 2024.

While the market's momentum is undeniable, the landscape has been reshaped by the One Big Beautiful Bill Act of 2025 (OBBBA), which introduced new complexities. The OBBBA phased down certain tax credits for wind and solar projects and imposed new Foreign Entity of Concern (FEOC) restrictions that will add a layer of complexity for projects coming online in 2026. Despite these changes, the tax credit transfer market is expected to remain robust. Many technologies, including battery storage, geothermal, and advanced manufacturing, will continue to benefit from strong tax credit support, and a significant pipeline of wind and solar projects remains eligible for future credits. The OBBBA did not restrict tax credit transfers, and we expect the market to continue its growth in 2025, with new buyers entering to manage their tax liabilities. The clean energy industry's resilience suggests that it will adapt and thrive in this evolving policy environment.

Scope

This guide is primarily focused on federal tax issues and is for informational purposes only. Readers should not construe this content document or related materials as legal, tax, investment, financial, or other advice. All content in this handbook is information of a general nature and does not address the circumstances of any individual or entity.

Version 4.1 and the OBBBA

This Comprehensive Guide is a shortened version of the Transferable Tax Credit Handbook Version 4, which was republished following the enactment of the OBBBA on July 4, 2025. We have updated the following content to incorporate relevant changes, though further guidance will continue to emerge.

Impacts on Tax Credit Transfers following the passing of the OBBBA include:

- Accelerated phase-down of tech-neutral (§45Y and §48E) tax credits for solar and wind

- Accelerated phase-down of advanced manufacturing production credits (§45X) credits for wind components

- Termination of the clean hydrogen production credit (§45V) for projects beginning construction after December 31, 2027

- Several tax credits were expanded or extended, including §40A credits for small agri-biodiesel producers, §45X credits for metallurgical coal producers, and §45Z credits for clean fuel producers

- Rates were adjusted for §45Z and §45Q credits for parity across types

- For §45X integrated components (where a primary eligible component is sold to an affiliate to produce a secondary eligible component), both need to be produced in the same factory and 65% of the direct material costs for the primary components must be US-made

- New FEOC restrictions for §48E, §45Y, §45X, §45U, §45Z, and §45Q credits

- Transferability is preserved, though tax credit purchasers cannot be prohibited foreign entities

- Elimination of the permanent 10% minimum ITC under §48

- Although not a transferable credit, the §25D credit for homeowners for solar, geothermal heat pumps, and batteries was eliminated for equipment placed in service after December 31, 2025

- Addition of a nuclear energy community adder to §45Y for facilities in communities that are, or previously were, employed to advance nuclear power

The OBBBA introduced several tax policies, notably bonus depreciation and R&E expensing, that will reduce the tax liability of many prospective tax credit buyers. This in turn will impact the volume of credits that these buyers can purchase. The major corporate tax changes include:

- 100% bonus depreciation: introduces option to claim 100% bonus depreciation for qualified property acquired after January 19, 2025. Bonus depreciation is also available for manufacturing and production facilities that meet certain criteria

- Full expensing of domestic research and experimental (R&E) expenditures: §174A allows full expensing of domestically sourced R&E expenditures for taxable years beginning after December 31, 2024. Foreign sourced expenditures must be capitalized and amortized over a 15-year period

- §163(j) business interest adjustment: restores the Earnings Before Interest, Taxes, Depreciation, and Amortization-based (EBITDA) calculation of adjusted taxable income for purposes of the 30% cap on business interest deduction for taxable years beginning after December 31, 2024

- Base erosion and anti-abuse tax (BEAT): increases BEAT rate from 10% to 10.5%, rather than to the previously scheduled 12.5% rate for taxable years beginning after December 31, 2025. Also allows add-back of general business credits under §38 for BEAT purposes, which had previously been scheduled to sunset

Overview

Under §6418 of the Internal Revenue Code (IRC) (first introduced in the IRA), “eligible taxpayers” are allowed to elect to transfer (i.e., sell) certain tax credits to unrelated taxpayers for cash.

What are transferable tax credits?

Transferability is meant to incentivize a broader pool of capital to invest in clean energy projects.

Eligible taxpayers can elect to transfer all or a portion of an eligible credit, and the tax credit buyer is treated as the taxpayer with respect to such credit (or such portion thereof). The buyer is allowed to claim the transferred tax credits on its tax returns, while also assuming some risk in the event of a recapture event or a challenge by the IRS on the qualification of the transferred tax credit.

Tax credits can be transferred for tax years starting after December 31, 2022. The cash payments are excluded from the tax credit seller’s gross income and are not deductible by the buyer. In addition, the buyer does not record any gross income or gain for federal tax purposes, even if the buyer has purchased the tax credit at a discount from face value.

Tax credits under the following U.S. tax code sections can be transferred: §30C, §40A, §45, §45Q, §45U, §45V, §45X,§45Y, §45Z, §48, §48C, and §48E.

Tax credits can be transferred for tax years starting after December 31, 2022. The tax credit buyer does not record any gross income or gain for federal tax purposes, even if the credits are purchased at a discount.

What are the benefits of transferable tax credits?

Tax credits have historically been the main way the U.S. federal government subsidizes clean energy projects, but this system had a major flaw: most project developers and manufacturers don't have enough tax liability to use the credits themselves. Before the Inflation Reduction Act (IRA), this led to complex, restrictive tax equity structures like the partnership flip, where a third-party investor would co-own a project to receive most of the tax benefits. This cumbersome process has been dominated by a few large financial institutions: two major banks have accounted for more than 50% of tax equity investment in recent years. The IRA introduced tax credit transferability, a simpler process that allows a clean energy developer to directly sell a tax credit to another company, opening the door for a wider range of investors to participate without needing to enter into a complicated, long-term partnership.

Simplified structure and lower transaction costs

Transferability offers a simpler and more cost-effective alternative to traditional tax equity structures. Rather than the complex, expensive process of negotiating and forming a partnership, which can incur significant legal and accounting fees per transaction, a clean energy developer can simply sell a credit to a buyer. The sale is formalized through a Tax Credit Transfer Agreement (TCTA) and completed by making a transfer election on the original tax return for the year the credit is earned, significantly streamlining the process for both parties.

Less ongoing management

For tax equity investors, who are often co-owners of a project, a typical deal requires extensive ongoing asset management and financial reporting. At minimum, the investor must monitor project performance, conduct complex GAAP accounting analysis, which may include consolidation/variable interest entity assessments and hypothetical liquidation at book value (HLBV) accounting, prepare or collect K-1 and other tax forms , and ensure receipt of timely payments (e.g., preferred payments in a partnership flip structure).

More favorable reporting

Traditional tax equity has complex GAAP accounting treatment, which can increase volatility of earnings reporting for publicly traded companies. The accounting complexity, as well as risk of tax equity’s impact on reported earnings, has made tax equity a non-starter for many publicly traded companies. In contrast, a transferred tax credit has a more straightforward accounting treatment.

Narrower set of risks, primarily related to disallowance or recapture of credit by the IRS

A tax equity investor is investing true equity into a project, meaning their returns may be impacted if a project has lower performance than what was underwritten – for instance, if a wind turbine doesn’t produce as much power as originally estimated. In a tax credit transfer, the buyer is not directly subject to asset performance risk; the primary risk is a disallowance or recapture of the tax credit by the IRS.

The 12 transferable credits

Technical credit considerations

Who can sell credits?

Eligible credits can be transferred by taxpayers – including individuals, C-corporations, trusts, estates, partnerships, and S-corporations – beginning on January 1, 2023.

Tax-exempt entities, including municipal and rural electric co-ops, state and local governments, and tribal entities, are not able to transfer credits but can use the elective pay election under §6417. See the Elective pay section for further details.

For property held by a partnership, the transfer is made at the partnership level. However, each partner may direct the partnership to sell its respective share of credits without affecting any other partner’s allocation of credits.

Who can buy credits?

The credit must be transferred to an unrelated taxpayer. Related parties are defined in the IRC under §267(b) and §707(b)(1). The credit can be transferred in whole or in part (e.g., credits from a single project can be sold to multiple buyers).

Partnerships may purchase credits from unrelated taxpayers. Such credits are allocated to its partners and treated as nondeductible expenditures and reduce each partner’s capital account and tax basis in its partnership interests.

Tax treatment

For the seller

The purchase price of the tax credits is not included in the gross income of the seller. If a partnership is the owner of the credit property, the tax credits are sold by the partnership, and the amount of cash consideration received by the seller is treated as tax exempt income. This tax-exempt income is allocated to the partners in the same proportionate manner that the original credit would have been allocated.

For the buyer

The purchase price of the tax credits is not deductible by the buyer, and buyers do not recognize gross income on the discount portion of the credit. For example, a buyer that purchases $100M of tax credits for $95M in cash is not subject to federal tax on the $5M reduction in taxes payable to the IRS.

Other restrictions

Cash only consideration

Buyers must purchase transferable credits with cash – U.S. dollars, check, cashier’s check, money order, wire transfer, ACH transfer, or other bank transfer of immediately available funds. A disguised consideration, such as a buyer receiving a discount on services from the seller from whom they are purchasing credits, could cause the transfer election to be disallowed.

Prohibition against resale

Credits may only be transferred once. Once a buyer has purchased tax credits, they cannot resell them. If a buyer is unable to fully utilize the tax credits they purchased in a given year, they can carry the unused credits back three years and forward for up to 22 years.

While a tax credit seller who is an S corporation is subject to the no additional transfer rule, an allocation of a transferred specified credit portion to a direct or indirect shareholder of an S corporation is not a transfer for purposes of §6418.

No progress expenditures

Investment credits that are realized as progress expenditures may not be transferred.

Lessees may not transfer credits

To the extent that a lessee claims a credit pursuant to a lease passthrough structure, the lessee may not subsequently transfer the credit. However, lessors in a sale-leaseback transaction may elect to transfer the credits to a third party.

At-risk rules

For §48 investment tax credit sellers that are individuals or closely held C-corporations (or partnerships or S-corporations whose partners or shareholders include such taxpayers) are subject to the at-risk rules of §49. The rules apply an at-risk calculation to determine the amount of tax credits that the taxpayer is allowed to realize, based on each partner’s or shareholder’s amount of non-qualified non-recourse financing related to the credit property. To the extent that such at-risk rules apply, the amount of credit that a seller can claim and transfer may be limited.

Passive activity loss rules

Generally, individuals, estates, trusts, closely held C-corporations, and personal service corporations are subject to passive activity loss rules under §469. The passive activity loss rules require any taxpayers subject to such rules to only apply tax credits to passive income, and not active income, such as wage income, or portfolio income, such as capital gains or dividends.

There are, however, certain exceptions in place for closely held C-corporations as outlined in §469(e)(2)(A). Closely held C-corporations should consult with tax counsel on their ability to use tax credits to offset net active income.

Foreign entity of concern restrictions

The OBBBA introduced restrictions such that the benefits of the tax credits cannot be claimed by a “prohibited foreign entity” (PFE), as defined in §7701(a)(51), for many transferable tax credits starting in 2026. Therefore, neither the buyer nor the seller can qualify as a PFE. For more details on Foreign Entity of Concern download the full handbook.

Excessive credit transfers

If a credit transfer is deemed by the IRS to constitute an “excessive credit transfer,” the purchaser of the credit would be liable for an increase in tax by the amount of the excessive credit transfer plus a penalty of 20% of such amount. The penalty would not be applied to the extent the excessive credit transfer is due to “reasonable cause.”

For more information on reasonable cause download the full handbook here.

Required minimum documentation

A statement or representation must be made in the transfer election statement that the tax credit seller has provided the “required minimum documentation” to the tax credit buyer. Required minimum documentation differs from the reasonable cause standard for excessive credit transfers.

The minimum documentation threshold is intended to establish a baseline of information necessary to validate an eligible taxpayer’s claim to an eligible credit. Tax credit buyers will often require additional documentation to substantiate the credit, and to gain comfort that they will be able to provide the necessary documentation in the event of an IRS challenge.

Required minimum documentation includes:

- Information that validates the existence of the eligible credit property, which could include evidence prepared by a third party (such as a county board or other governmental entity, a utility, or an insurance provider)

- If applicable, documentation substantiating that the eligible taxpayer has satisfied the requirements to include any bonus credit amounts (as defined in §1.6418–1(c)(3)) in the eligible credit that was part of the transferred specified credit portion

- Evidence of the eligible taxpayer’s qualifying costs in the case of a transfer of an eligible credit that is part of the investment credit or the amount of qualifying production activities and sales amounts, as relevant, in the case of a transfer of an eligible credit that is a production credit

Carrybacks and carryforwards

§39(a)(4) generally allows a three-year carryback period in the case of any applicable credit (as defined in §6417(b)). For a tax credit buyer, utilizing the three-year carryback period for applicable credits is not a straightforward process. If a clean energy project is placed in service in a new tax year, the resulting credits must first be applied to that year's tax liability. Any unused credits can then be carried back, but they must be applied to the earliest available tax year first (e.g., a 2024 credit would first apply to 2021, then 2022, then 2023).

This carryback process requires amending prior-year tax returns, which can increase the risk of an audit. Alternatively, taxpayers can carry unused credits forward for up to 22 years (effectively 20 years from the current tax year).

Buyers and sellers with different tax years

The year that a buyer recognizes transferable tax credits depends on both the buyer and seller tax year. Pursuant to §6418(d), “a [tax credit buyer] takes the transferred eligible credit into account in its first tax year ending with, or after, the eligible taxpayer’s tax year with respect to which the transferred eligible credit was determined.” Corporate taxpayers will face one of three scenarios when engaging tax credit sellers.

Buyer and seller both have a calendar year-end

For transactions in which both the buyer and seller have a 12/31 tax year-end date, the credits simply apply to the tax year in which they were generated.

Buyer's tax year ends before that of the seller

For a transaction in which the buyer tax year ends before that of the seller – for example, the buyer has a 9/30 tax year, and the seller has a 12/31 tax year – any credits generated in the same calendar year are pushed into the next tax year for the buyer.

Buyer's tax year ends after that of the seller

Lastly, for a transaction in which the seller's tax year ends before that of the buyer, credits generated prior to the end of the seller tax year will apply to the current calendar year, but credits generated after the end of the seller tax year will push into the next calendar year.

Most eligible corporate taxpayers are calendar-year filers

There are approximately 600 publicly traded companies in the U.S. with a trailing 12-month income tax liability over $100M. Of these companies, 78% are calendar-year filers, while another 8.0% close out their fiscal year in February or September.

If we increase the threshold to $500M of trailing 12-month income tax liability, the numbers remain consistent: 78.2% of companies are calendar-year filers.

The approximately 20% of corporations who are not December filers may be somewhat disadvantaged when sourcing credits. A tax credit buyer who has a September fiscal year end, for example, would effectively need to source credits placed in service in 2025 (assuming a seller with a calendar tax year) for their 2026 return. This timing disconnect presents timing of payments challenges for both the tax credit seller and the tax credit buyer.

Transfer mechanics

To effectuate a valid credit transfer, the buyer and seller must complete several key steps.

Step 1 — Negotiate tax credit transfer agreement

First, the buyer and seller should enter into a contractual agreement to transfer the credits. See the Tax credit transfer agreements section for a summary of typical negotiated terms. This agreement is a private agreement between the buyer and seller and is not a public document that would be filed with the IRS.

Step 2 — Fulfill IRS pre-filing registration

The seller of the credit needs to fulfill the pre-filing registration requirements with the IRS, which is done electronically through an IRS pre-filing registration tool, and receive a registration number for each eligible credit property.

As part of this registration process, the seller will include information about the transferor taxpayer and the credit property, including addresses and coordinates, supporting documentation relating to the construction or acquisition of the credit property, beginning of construction date, and placed in service date. Such registration must be accompanied by a penalties of perjury statement, signed by a person with personal knowledge of the relevant facts and who is authorized to bind the registrant.

How many pre-filing registration numbers?

- A tax credit seller can only submit one pre-filing registration for a given tax year. Therefore, they must apply for registration numbers for all their credits in a single filing.

- If a tax credit seller needs additional registration numbers for different facilities or properties, they must wait until the most recent pre-filing registration submission is processed by the IRS and returned.

- A tax credit seller will need one registration number per eligible credit property/facility.

- A registration number is only valid for a single tax year, so the tax credit seller will need to apply for new registration numbers each year for projects that generate credits in more than one year – §45 PTCs, for example.

Step 3 — Complete relevant source credit forms and IRS Form 3800

The tax credit seller must complete the relevant source credit form and IRS Form 3800, General Business Credit (or its successor). A schedule must also be attached to the Form 3800, showing the amount of eligible credit transferred for each eligible credit property.

Below are links to available source credit forms for transferable tax credits; for example, Form 7207, Advanced Manufacturing Production Credit, is required if making a transfer election for a §45X credit:

Step 4 — Execute transfer election statement

A transfer election statement is a written document that memorializes the transfer of a specified credit portion between a tax credit buyer and seller. The tax credit seller and tax credit buyer must each attach a transfer election statement to their respective return. There is not a specific form, but the document must be labeled as a “transfer election statement” and be signed under penalties of perjury by an individual with authority to legally bind the tax credit seller. The statement must also include the written consent of an individual with authority to legally bind the tax credit buyer.

As stated in §6418, information that must be in the transfer election statement includes:

- Name, address, and taxpayer identification number of the tax credit seller and the tax credit buyer.

- A statement that provides the necessary information and amounts to allow the tax credit buyer to take into account the specified credit portion with respect to the eligible credit property, including:

- A description of the eligible credit (for example, advanced manufacturing production credit for a §45X transfer election), the total amount of the credit determined with respect to the eligible credit property, and the amount of the specified credit portion

- The taxable year of the tax credit seller and the first taxable year in which the specified credit portion will be taken into account by the tax credit buyer

- The amount(s) of the cash consideration and date(s) on which paid by the tax credit buyer

- The registration number related to the eligible credit property

- Attestation that the tax credit seller (or any member of its consolidated group) is not related to the tax credit buyer (or any member of its consolidated group) within the meaning of §267(b) or 707(b)(1))

- A statement or representation from the tax credit seller that it has or will comply with all requirements of §6418, the §6418 regulations, and the provisions of the Code applicable to the eligible credit, including, for example, any requirements for bonus credit amounts described in §1.6418–1(c)(3) (if applicable)

- A statement or representation from the tax credit seller and the tax credit buyer acknowledging the notification of recapture requirements under §6418(g)(3) and the §6418 regulations (if applicable)

- A statement or representation from the tax credit seller that the tax credit seller has provided the required minimum documentation (as described in paragraph (b)(5)(iv) of this section) to the tax credit buyer

Beginning of construction

A project's beginning of construction (BoC) date is critical for clean energy tax credits, as it determines a project's eligibility for certain credits, exemption from prevailing wage and apprenticeship requirements, and exemption from Foreign Entity of Concern (FEOC) restrictions. Historically, a project could establish its BoC in one of two ways:

- Commencing physical work of a significant nature and then maintaining a Continuous Program of Construction. This physical work can be done on-site, like excavating for foundations, or off-site, such as manufacturing a custom-designed component like a transformer (provided it is under a binding written contract and not from a manufacturer's inventory).

- Satisfying the Five Percent Safe Harbor, where a taxpayer pays or incurs 5% or more of the total project cost and demonstrates Continuous Efforts toward completion.

Both methods require continuous progress, known as the Continuity Requirement. The IRS provides a Continuity Safe Harbor where this requirement is deemed satisfied if the project is placed in service within four calendar years following the calendar year construction began, though this window has been extended for certain historical projects.

Under the OBBBA, solar and wind projects are subject to an early phasedown of tax credits. Solar and wind projects must be placed in service before January 1, 2028 to qualify for §45Y and §48E credits, unless the projects started construction before July 5, 2026. This has spurred a surge of developers seeking to establish BoC by July 5, 2026.

In August of 2025, the Treasury released Notice 2025-42 which significantly alters the BoC rules for most solar and wind projects seeking tax credits under §45Y and §48E. The major changes to the BoC rules are as follows:

- Wind projects and solar projects with a maximum net output greater than 1.5 MW can no longer use the Five Percent Safe Harbor. They must establish BoC solely by performing physical work of a significant nature and maintaining a continuous program of construction.

- Notably, the new guidance changed the language from "starting" to "performing" physical work, though the Treasury did not define a clear monetary or percentage threshold for meeting this "significant nature" standard.

- This new guidance does not apply to projects that established BoC under the old rules before September 2, 2025, or to smaller solar projects (1.5 MW or less).

It is important to note that Notice 2025-42 only addresses tax credit qualification under §45Y and §48E, and guidance regarding FEOC restrictions is still pending.

For more information on Beginning of Construction requirements, download the full handbook.

Corporate alternative minimum tax (CAMT)

Created by the IRA, the corporate alternative minimum tax (CAMT) seeks to place a 15% “floor” under corporate taxpayers to raise revenues and require companies with lower effective tax rates to bring their rates up to a uniform level.

The legislative language behind CAMT is designed to require profitable corporations to pay at least some federal income tax, regardless of the deductions and credits they may claim under the regular tax system. The law also intends to reduce the gap between the book income and taxable income of corporations, which has been a source of public criticism and scrutiny.

CAMT applies to large corporations – other than an S-corporation, regulated investment company, or real estate investment trust – who report more than $1 billion in profits to shareholders on their financial statements. CAMT imposes a 15% minimum tax on the adjusted financial statement income (AFSI) of these corporations, which is their income before taxes as reported on their financial statements, with certain adjustments. AFSI diverges from taxable income, sometimes significantly; as a result, corporations with an effective tax rate that exceeds 15% may still be subject to CAMT liability.

One of the most important adjustments for the CAMT is the allowance of general business tax credits to reduce tax liability back below the 15% threshold. General business tax credits, which include §45 PTCs, §45X AMPCs and §48 ITCs, can be used to offset up to 75% of a corporation’s net income tax. In conclusion, corporations facing CAMT can purchase transferable tax credits to offset tax liabilities, even below the 15% minimum tax threshold imposed through CAMT.

OECD Pillar Two

Pillar Two applies to MNEs with annual revenues above €750 million. It is a “top-up tax,” which is levied when the MNE’s effective tax rate (ETR) falls below 15% in any jurisdiction that has adopted Pillar Two in which the MNE operates. The right to tax income can be levied through each of the following mechanisms, in order:

- Qualified domestic minimum top-up tax (QDMTT): The jurisdiction in which the undertaxed entity is located has the first right to collect the top-up tax. There is a strong incentive to collect taxes locally, otherwise taxes can be collected by other entities (see below)

- Income Inclusion Rule (IIR): If the source country does not impose a top-up tax, the home country of the parent company can collect the tax. For example, the German government can collect top-up tax on the German parent of a U.S. subsidiary, if the ETR of the U.S. entity fell below 15%

- Undertaxed Payments Rule (UTPR): If neither of the above two taxes apply, then countries in which other constituent entities (such as subsidiaries and branches) are located can collect the tax by denying deductions for those constituent entities. No countries have yet assessed the UTPR, and the OECD’s latest guidance delayed implementation of the UTPR until 2026 in many jurisdictions

OECD guidance from July 2023 clarified that IRA tax credits will receive the same favorable treatment as refundable tax credits, even though IRA tax credits were not explicitly designated as refundable credits. Tax credits are treated as non-marketable credits from the buyer’s perspective, and marketable credits from the seller’s perspective.

For the buyer, the numerator of the effective tax rate (ETR) calculation is only reduced by the discount amount of the credit. For example, if a buyer purchases $1 of tax credits for $0.95, then the numerator of the ETR calculation is reduced by only $0.05. This alleviated concerns that the purchase of IRA tax credits would have a more significant impact on the ETR calculation for purposes of Pillar Two taxation.

For the seller, the proceeds from the sale of tax credits are treated as additional income, rather than a reduction of taxes. For example, if a seller sells $1 of tax credits for $0.95, then the denominator of the ETR calculation is increased by $0.95. For the seller, this tax treatment holds whether or not the tax credits are sold to a third party.

The most common credits: eligibility, risks, and due diligence

§48 and §48E ITCs

Eligibility and dates (§48)

Eligibility and dates (§48E)

Rates

PWA

Assuming Prevailing Wage and Apprenticeship requirements are met, the §48 and §48E ITCs are worth 30% of a project’s qualified basis. Otherwise, the credit is reduced to 6%.

Energy community

Projects that qualify for the energy community bonus receive:

- 2% of project’s qualified basis if PWA requirements are not met

- 10% of project’s qualified basis if PWA requirements are met

Assuming a project meets PWA requirements, for example, the energy community bonus results in an ITC value worth 40% of a project’s qualified basis.

Domestic content

Projects that qualify for the domestic content bonus receive:

- 2% of project’s qualified basis if PWA requirements are not met

- 10% of project’s qualified basis if PWA requirements are met

Assuming a project meets PWA requirements, for example, the domestic content bonus results in an ITC value worth 40% of a project’s qualified basis.

Low-income community

Projects that qualify for the low-income community bonus receive an additional 10% or 20% of the project’s qualified basis. The bonus is limited to projects of 5 MW or less and is an allocated credit, meaning tax credit sellers must apply for the bonus and receive an allocation.

Risks

Qualification

Buyers will need to ensure that tax credits qualify for the §48 or §48E ITC and will be respected in full by the IRS. Key areas of qualification include validation that the underlying project qualifies as energy property (as defined in §48) or a qualified facility or energy storage technology (as defined in §48E), the proper cost basis is used, the project was placed in service in the appropriate tax year, and that FEOC restrictions are considered (if applicable).

The IRS may challenge the cost basis of the energy property. If the cost basis is determined to be a lower amount, this will also reduce the ITC amount, resulting in an excessive credit transfer to the tax credit buyer.

Recapture

Investment tax credits under §48 and §48E are subject to the recapture provisions of §50, which states that, “if, during any taxable year, investment credit property is disposed of, or otherwise ceases to be investment credit property with respect to the taxpayer” then the credit will be recaptured. The ITC carries a five-year compliance period, in which the potential amount of credit that can be recaptured starts at 100% for the first year and steps down 20% per year.

Practically speaking, recapture can occur in the following scenarios:

- The property ceases to be a qualified energy facility

- There is a change in ownership of the property

For more details on recapture provisions, download the full handbook.

Foreign entity of concern

For §48E tax credits, strict rules around FEOC were added in the OBBBA. There is also a ten-year recapture period for §48E investment tax credits if some of these rules are not adhered to accurately. For the avoidance of doubt, §48 tax credits are exempt from this provision.

Due diligence

§48 and §48E ITCs generally carry a larger discount compared to §45 or §45Y PTCs and §45X AMPCs because due diligence is more complex, and credits are subject to risk of §50 recapture. Buyers should ensure that the project qualifies as energy property (as defined in §48) or a qualified facility or energy storage technology (as defined in §48E), the proper cost basis is used, and the project was placed in service in the appropriate tax year. Buyers should also ensure that risk mitigants are in place to avoid common recapture scenarios.

In this section, we focus on due diligence related to qualification, structure, and recapture of §48 and §48E ITCs.

Qualification: cost basis and basis step-ups

The buyer first will need to confirm that tax credits are generated from qualified energy property, as defined in IRC §48, or a qualified facility or energy storage technology as defined in §48E.

Buyers will also need to review detailed documentation to substantiate the project’s cost basis. A cost segregation analysis from a reputed third-party accounting firm is typically used to validate the cost basis for energy property eligible for the ITC.

If a project has a step-up in the cost basis, the buyer will want to:

- Diligence the transaction that effectuates the step-up

- Analyze the stepped-up valuation (with specific focus on the amount of step up relative to the cost basis of the project prior to such step-up)

Transaction structure for basis step-up: In some transactions, a tax credit seller will seek to increase, or “step up,” the cost basis to a fair market value that exceeds the original cost basis. A stepped-up cost basis drives a larger tax credit amount, as the ITC is calculated as a percent of the project’s cost basis.

The most common structure is to sell the project company to a partnership, which is composed of the project sponsor and a third party that owns a certain percentage of the partnership. Many infrastructure oriented private equity funds and other investors have emerged with “preferred equity” vehicles that will serve as the third-party investor in a partnership.

Valuation for basis step-up: To substantiate a project's fair market value, a buyer should get an appraisal from a qualified third-party firm in addition to the customary cost segregation analysis. The buyer should also examine the structure used to effectuate the step-up.

Recapture: continuation as a qualified facility

The IRS may "recapture" (i.e., revoke) the tax credit if the project ceases to be a qualified energy facility within the first five years of operation. This can happen if the facility is destroyed, abandoned, or changes its business model (e.g., selling something other than electricity).

To mitigate this risk, buyers should ensure the project will remain operational. This includes confirming the project has:

- Sufficient property and casualty insurance.

- Adequate site control (i.e., the project can't be removed from the land).

- The necessary rights to connect to the electricity grid.

Additionally, the seller should demonstrate they have contingency plans, such as alternative buyers, in case the primary electricity offtaker defaults.

Recapture: no change in ownership

The IRS may recapture the credit if the project owner transfers ownership of the facility within the five-year period of the project being placed in service. To protect this risk, buyers should receive from the seller:

- Detailed information about the project’s ownership structure

- Confirmation that financing parties do not have collateral interests that could cause recapture in the event of a default.

Recapture: FEOC restrictions

Added in the OBBBA, the IRS may recapture §48E credits any time in the ten years after the qualified facility is placed in service if the taxpayer makes certain to a specified foreign entity. To protect against this risk, buyers will need to review the contracts related to the qualified facility, and require annual certificates from the seller noting that all parties are in compliance. Further guidance from the IRS regarding FEOC compliance and related recapture is expected by the end of 2026.

Placed-in-service date

The placed-in-service date determines the tax year to which the tax credit applies. If a project’s anticipated placed-in-service date was 2025, but it was later found that the project was placed in service in 2026, then the buyer must treat the credits as having been generated in the 2026 tax year. This is particularly important to diligence at the end of the seller’s tax year, when ambiguity around the exact placed-in-service date can result in tax credits slipping to the subsequent tax year.

To make a determination of when a project is placed in service, there is a five-factor test generally considered by the IRS and various courts. None of the five factors are controlling:

- The procurement of required licenses and permits

- The passage of control of the facility to the ultimate taxpayer

- The completion of critical tests

- The commencement of regular operations

- The synchronization of the facility into a power grid for generating electricity to produce income (if applicable)

§45 and §45Y PTCs

Eligibility and dates (§45)

Eligibility and dates (§45Y)

One important distinction between §45 and §45Y: in the case of §45 credits, the taxpayer must own the qualified facility and sell the electricity produced there to an unrelated person. For §45Y credits, the taxpayer must either (i) own the facility and sell the electricity produced there to an unrelated person; or (i) own the facility, (ii) equip the facility with a metering device that is owned and operated by an unrelated person and (iii) sell, consume or store the electricity. There is not a requirement to sell electricity to claim §45Y credits, as long as the metering device is owned and operated by an unrelated person.

Rates

The IRS updates §45 and §45Y PTC rates on an annual basis, generally in Q2. Rates are determined using an inflation adjustment factor (IAF) and published in the Federal Register. The inflation adjustment factor for 2025 is 1.9971.

The §45Y PTC has one base rate, irrespective of when a qualifying project is placed in service. The base rate is $3 per megawatt-hour (MWh) of qualifying electricity produced and sold. With PWA compliance (or exemption), the rate increases to $15 per MWh. There is also an annual, calendar year inflation adjustment for the rates, in which the rates are multiplied by the inflation adjustment factor described above and rounded. The $3 base rate is rounded to the nearest multiple of $0.50, and the $15 PWA rate is rounded to the nearest multiple of $1. As such, using the 2025 inflation adjustment factor of 1.9971, the 2025 base rate and PWA rate (after rounding) is $6 and $30 per MWh of qualifying electricity produced and sold, respectively.

The §45 PTC has two different rates depending on whether a project was placed in service before January 1, 2022, or not. For more information on these placed in service considerations, download the full handbook here.

Energy community

Projects that qualify for the energy community bonus receive a 10% PTC value increase if PWA requirements are met; as such (using 2025 rates), a $6 and $30 per MWh rate would increase to $6.60 and $33 per MWh, respectively.

Domestic content

Projects that qualify for the domestic content bonus receive a 10% PTC value increase if PWA requirements are met; as such (using 2025 rates), a $6 and $30 per MWh rate would increase to $6.60 and $33 per MWh, respectively.

Reduced PTC rates for wind facilities that began construction in certain years

The IRA restored the full PTC rate for wind facilities that were placed in service after December 31, 2021. Prior to the enactment of the law, wind facilities claiming the §45 PTC that were placed in service before January 1, 2022 were subject to reduced PTC rates under §45(b)(5), based on when construction began.

For the full list of dates and eligibility, download the full handbook.

Risks

Qualification

Section 45 and 45Y Production Tax Credits (PTCs) are based on the amount of electricity a qualified facility generates and sells to an unrelated party (for §45Y, credits can also be generated even if electricity is not sold to a third party, so long the electricity is metered on a device that is owned and operated by a third party). A key advantage of PTCs is that the primary risk—accurate production accounting—is easily managed. To verify the credit, a tax credit buyer will review a production report from the facility's revenue-grade meter and a third-party confirmation of the electricity sale.

Unlike Investment Tax Credits (ITCs), PTCs are not subject to recapture risk. However, buyers should ensure the project has a placed-in-service date no more than 10 years prior. Projects that have been "repowered" (upgraded with new equipment) can qualify for a new 10-year PTC period, provided the fair market value of the used property does not exceed 20% of the total project value. Such transactions may require a third-party appraisal. PTCs from projects placed in service before 2023 can still be transferred if the credits were generated in a tax year beginning after December 31, 2022.

Foreign entity of concern

For §45Y PTCs, strict rules around FEOC are required for any taxpayer to claim the credit for projects beginning construction on or after January 1, 2026. For the avoidance of doubt, §45 tax credits are exempt from this provision.

Due diligence

The PTC is based on the amount of electricity the qualifying project produces and sells to a third-party once it is placed in service. Buyers should receive from the seller:

- Evidence that the project has been placed in service and has not been in operation for more than ten years

- If the project has been repowered or upgraded, evidence of the fair market value of the used equipment and the cost of the new equipment

- A production report from the project’s revenue-grade meter or other third-party substantiation (such as settlement statements from the grid operator)

- Confirmation of the electricity purchase by an unrelated third party

Buyers should also understand the circumstances under which the project may generate less electricity than anticipated – for example, curtailment – because that reduces the amount of PTCs generated.

§45X AMPCs

Eligibility and dates

Risks

Qualification

While §45X AMPCs are not subject to PWA requirements and do not carry the same recapture risks as §48 and §48E ITCs, they do carry additional qualification risks that are absent from other power generation-related tax credits such as the §45 and §45Y PTCs.

Components may be required to meet certain administrative or technological specifications to qualify as an eligible component that gives rise to a tax credit.

Foreign Entity of Concern

For §45X tax credits, strict rules around foreign entities of concern are required for any taxpayer to claim the credit for tax years beginning January 1, 2026.

Due diligence

To properly conduct due diligence for Section 45X tax credits, buyers should focus on six key areas:

- Credit amount and qualification: Verify the tax credit calculation, and that eligible components were produced in 2023 or later and meet the specific design and capacity requirements outlined in §45X. The credit is claimed in the year the sale is completed.

- Taxpayer as producer: Ensure the credit is claimed by the taxpayer who performed the "substantial transformation" of the component, not "mere assembly." In a contract manufacturing arrangement, a written agreement determines who claims the credit.

- Domestic production: Confirm that the eligible components were produced in the U.S. or its territories. While the final product must be made domestically, the raw materials and sub-components do not. Due diligence can include reviewing facility ownership or conducting a site visit.

- No §48C credits: If a facility has claimed a §48C investment tax credit, it can only qualify for §45X credits if the assembly lines for each are separate.

- Third-party sale: The credit is only generated when the component is sold to a third party. This can be verified by reviewing sales contracts and documentation. An exception exists for "integrated components" sold between affiliates, which may still qualify if certain domestic production and cost requirements are met and the final product is sold to an unrelated party.

- Comply with FEOC restrictions: download the full handbook.

Relationship to the §48C qualifying advanced energy project credit

Certain advanced manufacturers may elect the §45X AMPC or the §48C qualifying advanced energy project credit, though they cannot claim the §45X credit for products manufactured at a facility for which they claimed a §48C credit. There are instances, however, when vertically integrated manufacturers may qualify for both credits. For example, if a company manufactures a component from equipment for which it claimed a §48C credit and then uses that component to produce §45X components using other equipment, the company may be eligible to claim both credits.

Due diligence considerations for all common credits

When a buyer purchases various clean energy tax credits (such as §48, §48E, §45, §45Y, and §45X), several due diligence considerations are shared across all of them. These include:

- Corporate Structure: Buyers must understand the seller's corporate structure, including any disregarded entities, to ensure a valid chain of title for the tax credits. This involves reviewing corporate documents like articles of organization, by-laws, and lien searches.

- Financial Strength: Buyers should assess the seller's financial stability, as it determines the value of their indemnification for any tax credit recapture or disallowance. A seller with a strong balance sheet is more likely to fulfill their obligation to compensate the buyer if the credit is lost.

- Pre-filing Registration: Buyers should review the seller's IRS pre-filing registration documentation. While a transaction can close before the registration number is issued, it is a crucial component of the final tax return filing. Without the number by the filing date, the tax credit transfer may be invalidated.

Bonus credits

Introduction

The IRA created three bonus credits, or “adders,” for which projects can qualify:

- Energy community bonus

- Domestic content bonus

- Low-income community bonus

Each bonus has specific eligibility requirements that a project must meet. Tax credit buyers will bear some additional risk when assuming these bonus credits, as qualification for these adders is subject to IRS scrutiny and audit.

Bonus credits are not treated differently from base credits for the purpose of transferability. Treasury guidance released in June 2023 specified that all transferable credits must be sold as “vertical slices” and be pari passu to one another, as opposed to “horizontally” bifurcating bonus credits from base credits.

Energy Community Bonus Credit

Eligibility

To qualify for the energy community bonus as a project claiming investment and production tax credits under the §45, §45Y, §48, and §48E, a project must be in at least one of three energy community types:

- Brownfield

- Statistical area

- Coal closure

If a clean energy project is in two energy communities – a brownfield site within a coal closure, for instance – the bonus remains 10%.

The OBBBA adds an energy community bonus for §45Y nuclear facilities that are located in metropolitan statistical areas that are, or have previously been, nuclear communities (see Nuclear facility section below).

Timing

For §48 and §48E ITCs, eligibility for the energy community bonus is determined on the placed-in-service date and not retested. For §45 and §45Y PTCs (including repowers), eligibility must be determined each year during the ten-year credit period, with a facility treated as located in an energy community if it qualifies at any time during the year. If construction begins after December 31, 2022 in a location that is an energy community on that date, the location will continue to qualify for the full PTC period (§45, §45Y) or on the placed-in-service date (§48, §48E). Projects generating §45 PTCs placed in service before December 31, 2022 are not eligible, even if located in an energy community, as that date is set in the IRA (H.R.5376).

Nameplate capacity test

A project qualifies for the energy community bonus if at least half (50%) of its nameplate capacity is in an energy community.

Footprint test

If a clean energy facility does not have a nameplate capacity, it can qualify for the energy community bonus under the “footprint test.” If 50% or more of the project’s square footage is located in an energy community, then the project qualifies for the bonus.

Brownfield

A brownfield site as defined in certain subparagraphs of the Comprehensive Environmental Response, Compensation, and Liability Act of 1980 (CERCLA): “…real property, the expansion, redevelopment, or reuse of which may be complicated by the presence or potential presence of a hazardous substance, pollutant, or contaminant."

Three types of sites qualify as a brownfield under a safe harbor:

- Existing brownfield: Brownfields that are already tracked by a federal, state, territorial, or federally recognized Indian tribal brownfields program.

- Phase II assessment: A Phase II Assessment has been completed with respect to the site and such Phase II Assessment confirms the presence on the site of a hazardous substance.

- Phase 1 assessment (for projects with a nameplate capacity of not greater than 5 MWac): A Phase I Assessment has been completed with respect to the site and such Phase I Assessment identifies the presence or potential presence on the site of a hazardous substance, or a pollutant or contaminant.

Statistical area

A "metropolitan statistical area" (MSA) or "non-metropolitan statistical area" (non-MSA) that has (or had at any time after 2009):

- 0.17% or greater direct employment or 25% or greater local tax revenues related to the extraction, processing, transport, or storage of coal, oil, or natural gas; and

- An unemployment rate or above the national average unemployment rate for the previous year

Coal closure

A census tract (or directly adjoining census tract):

- In which a coal mine has closed after 1999; or

- In which a coal-fired electric generating unit has been retired after 2009

Nuclear facility

As added in the OBBBA, a new 10% energy community bonus is available for advanced nuclear facilities, or any nuclear facility that the Nuclear Regulatory Commission (NRC) has authorized to construct and issued a site-specific construction permit or combined license, claiming §45Y tax credits that are situated in a metropolitan statistical area where at least 0.17% of the community is (or has been at some time since December 31, 2009) employed directly by the advancement of nuclear activity.

Due diligence considerations

The energy community bonus is relatively straightforward to substantiate (other than qualification as a brownfield which can be more subjective). A developer should provide documentation that crosswalks their project’s location with at least one of the three energy community categories.

For §48 and §48E ITCs, eligibility for the energy community bonus credit is determined on the date that the project is placed in service. For §45 and §45Y PTCs, eligibility for the energy community bonus credit must be determined every year during the ten-year PTC period, although the IRS created a safe harbor for projects with beginning of construction dates on or after January 1, 2023. Specifically, for any ITC or PTC credit, if the project is in an energy community as of the beginning of construction date, then, with respect to that project, the location will continue to be considered an energy community for the duration of the credit period.

Nameplate capacity attribution rule

An IRS notice, Notice 2024-30, expanded the "nameplate capacity attribution rule" to make it easier for offshore wind projects to qualify for the energy community bonus credit.

The rule, which previously allowed offshore projects to qualify if their power-conditioning equipment was located in an energy community, has been broadened. Now, supervisory control and data acquisition (SCADA) equipment can also be used to qualify for the bonus.

- For additional information, download the full handbook.

Guidance

- October 5, 2022: IRS Notice 2022-51,

- April 4, 2023: IRS Notice 2023-29,

- April 7, 2023: IRS Notice 2023-45,

- June 15, 2023: IRS Notice 2023-47,

- March 22, 2024: IRS Notice 2024-30,

- June 9, 2024: IRS Notice 2024-48,

- June 23, 2025: IRS Notice 2025-31,

- July 4, 2025: One Big Beautiful Bill Act, Chapter 5.

Resources

- The Department of Energy (DOE) maintains an energy community map

- The Environmental Protection Agency (EPA) maintains a cleanups in my community map, which shows federally recognized brownfields

- The IRS maintains an FAQ

Domestic Content Bonus Credit

Eligibility

To incentivize the development of domestic clean energy production and manufacturing, the IRA includes a domestic content bonus. The domestic content adder is applicable to the §45, §45Y, §48, and §48E credits.

To qualify, a project must meet two overarching requirements:

- Steel and iron: 100% of all structural steel or iron products used must be produced in the U.S.

- Manufactured products: A minimum percentage of the total costs of manufactured products (including components) must be mined, produced, or manufactured in the U.S. Direct labor costs of incorporating a manufactured product into a project, such as installation costs, are not applicable

The minimum percentage of manufactured products is dependent on when the project begins construction, as amended in the OBBBA and effective on or after June 16, 2025:

- Before June 16, 2025: 40%

- June 16, 2025 – December 31, 2025: 45%

- January 1, 2026 – December 31, 2026: 50%

- After December 31, 2026: 55%

Safe harbor

To minimize the complexities associated with collecting and validating cost data from manufacturers, the IRS created a “new elective safe harbor” in IRS Notice 2024-41 for purposes of calculating the domestic content percentage. The new elective safe harbor allows developers to elect to determine their project’s domestic content percentage by aggregating fixed, IRS-determined percentages from an “exclusive and exhaustive” list of manufactured components and subcomponents instead of relying on the manufacturer to disclose their actual direct costs. IRS Notice 2025-08 modified Notice 2024-41 to adjust the percentages in the “First Updated Elective Safe Harbor.”

No partial reliance on safe harbor

If a developer chooses to use the elective safe harbor, they must do so for the entire project.

Elective safe harbor certification

If a developer uses the elective safe harbor to qualify for the domestic content bonus, they must submit a certification to the IRS alongside Form 8835 (for PTCs) or Form 3468 (for ITCs) in the first taxable year in which they report a domestic content credit amount for their project, including the:

- Project type

- Tax credit

- Placed-in-service date

- Location/coordinates

- Total amount of bonus credit claimed

Substantiation

Developers who claim the domestic content bonus credit must meet general recordkeeping requirements under §6001.

Due diligence considerations

Prior to the elective cost safe harbor, application of the domestic content bonus credit was minimal. With the elective safe harbor, domestic content due diligence becomes simpler (though the adder will likely remain the most complex of the three to diligence). Buyers will want to validate the developer’s safe harbor calculations, collect documentation confirming the sourcing of components and sub-components included in the calculations, and view the developer’s safe harbor certification. In many cases, a legal memorandum may be prepared by seller counsel to analyze and confirm compliance with domestic content requirements.

Guidance

- May 12, 2023: IRS Notice 2023-38,

- May 16, 2024: IRS Notice 2024-41,

- January 16, 2025: IRS Notice 2025-08,

Resources

Low-income community

Eligibility

The low-income bonus is designed to incentivize wind, solar, and associated energy storage investments in low-income communities, on Indian land, as part of affordable housing developments, and benefitting low-income households.

The low-income bonus is an allocated and capped credit, and 2025 capacity limitations are presented in Notice 2025-11. Projects in low-income communities or on Indian land receive a 10% bonus credit value, while projects on Qualified Low-Income Residential Building Project or as part of a Qualified Low-Income Economic Benefit Project receive a 20% bonus credit value. All low-income projects must be less than 5 MWac in size.

Beginning in 2025, the low-income community bonus credit is available under §48E(h).

Allocations

The DOE maintains a low-income communities program capacity dashboard, which displays the available capacity for each category.

How to apply

Since the low-income bonus is an allocated bonus, developers must apply for and receive an allocation from the IRS. The IRS makes it clear that a developer “may receive an allocation less than its [applied for] nameplate capacity.” The allocation, not the project’s capacity, determines the credit value.

If any category or sub-category is oversubscribed during the initial 30-day period, the IRS will make awards based on a randomized lottery. Following the initial 30-day period, any leftover capacity will be awarded on a first-come, first-served basis. Applicants may only submit one application per facility, per program year.

The IRS will make allocations with certain ownership and location priorities in mind:

- Ownership: Priority will be given to (1) projects owned directly or indirectly by Indian tribes; (2) consumer or purchasing cooperatives with controlling members who are workers or from low-income households; (3) tax-exempt charities and religious organizations; and (4) state and local governments, and U.S. territories, Indian tribes, and rural electrical cooperatives

- Location: Priority will be given to (1) persistent poverty counties, where 20% of residents have experienced high rates of poverty of the last 30 years; and (2) and census tracts designated as “disadvantaged” in the Climate and Economic Justice Screening Tool (CEJST)

Restrictions

Once a developer has an allocation, they have four years to place the project in service and cannot change its location; extensions are not permitted, and a project cannot be placed in service before receiving an allocation. After a project is placed in service – but before filing tax forms – the tax credit seller must update their DOE application with supporting documentation (scope depends on allocation category), attest that there have been no material ownership or application changes, and submit for review. The IRS will then determine if the facility retains its allocation or is disqualified; if eligible, the owner is notified. If nameplate capacity exceeds the allocated capacity (but is under 5 MWac), the percentage increase is reduced by a factor of allocated capacity divided by the installed capacity. If capacity is lower (but within the greater of 2 kW or 25%), the award is maintained; larger reductions result in disqualification.

Disqualification

A facility may become disqualified and lose its allocation if, prior to being placed in service, one or more of the conditions defined in 26 CFR § 1.48(e)‑1(m) occur.

Successor-in-interest changes

Developers may apply to transfer an allocation of environmental justice solar and wind capacity when there is a sale or transfer of an underlying facility. If the original allocation was based, in part, on meeting certain ownership criteria, a change in ownership can result in disqualification.

A tax credit seller may only apply for an allocation transfer when all three of the following conditions are valid:

- A sale or transfer of a facility from one taxpayer to another has taxpayer occurred

- The original owner has already applied for and been awarded an allocation for the applicable project

- The original owner has not already placed the project in service

Due diligence considerations

To qualify for the bonus, a developer must have an allocation award letter as well as confirmation that the project was placed in service within a statutorily set four-year period. To validate that the project was properly placed in service, the developer must provide documentation and make attestations in the DOE low-income community application portal.

For full documentation requirements, download the full handbook.

Guidance

- February 13, 2023: Notice 2023-17,

- May 31, 2023: Notice of Proposed Rulemaking,

- August 10, 2023: Final Regulations,

- August 10, 2023: Revenue Procedure 2023-27,

- March 29, 2024: Revenue Procedure 2024-19,

- March 6, 2025: Revenue Procedure 2025-11.

Resources