Reunion

November 12, 2025

Tax Credit Buyer Webinar: Navigating Carrybacks and Carryforwards in Clean Energy Tax Credit Transactions

Tax and legal leaders from CLA, Orrick, and McDermott discuss how tax credit carryback and carryforward provisions work in practice and what they mean for tax credit purchasers.

For Buyers

With Brandon Hill from CliftonLarsonAllen, Debbie Harrison from McDermott Will & Schulte, and Mark Christy from Orrick, Herrington & Sutcliffe

Clean energy transferable tax credits have created new opportunities for taxpayers to participate in the clean energy transition while offsetting tax liability, but understanding the mechanics of carrybacks and carryforwards is essential to capturing their full benefit.

Recording: Navigating Carrybacks and Carryforwards in Clean Energy Tax Credit Transactions

Insights from the conversation:

1. Carrybacks Create a Four-Year Tax Liability Window

The ability to carry a clean energy tax credit back 3 years and carry forward 22 years is the core mechanism. For a corporate buyer, this potentially aggregates four years of tax liability (the current year plus the three carryback years), making a carryback a great fit for any taxpayers with a trailing federal tax liability. Some examples of strong profiles for a carryback strategy include tax payers with a large, one-time event in a recent tax year or relatively smaller taxpayers looking to aggregate up to four years of liability to make a larger tax credit purchase. The carryback must first be applied to the current tax year, and then carried back to the earliest possible year first, with each year thereafter sequentially. Each tax year is subject to the statutory cap (75% of federal tax liability).

2. Cash Flow is the Primary Strategic Concern

One potential challenge of a carryback is the mismatch between the date the buyer pays for the credit and the date the refund is received from the IRS. Since a carryback claim is effectively filed simultaneously with the current year's tax return (which may be several months after year-end for corporates), there may be a notable lag. To alleviate this burden, tax credit buyers frequently negotiate delayed / split payment structures (or possibly lower upfront purchase prices) with tax credit sellers to improve the overall return on investment.

3. IRS Refund Timing is Variable (But Pays Interest)

Once the carryback claim is filed, the refund processing time is variable. The IRS publishes processing statuses online, which suggest an approximate 90-day timeline to process carryback claims. Notably, the IRS will pay interest on carryback refund claims that have been outstanding for more than 45 days. Subject to a given taxpayer’s internal cost of capital, some buyers have found interest payments to be accretive to the overall transaction ROI. Carryback refund claims under $5 million are not subject to Joint Committee on Taxation (JCT) review, which may also lead to faster processing.

4. Credit Ordering Rules Matter (Form 3800)

Taxpayers who have other general business credits (e.g., low-income housing, work opportunity, etc.) should be mindful of the instructions established in the Form 3800 General Business Credit (”GBC”) ordering rules. These rules dictate the order by which certain GBCs (including energy tax credits) must be applied against the current year's tax liability, and can have downstream impacts on carryback or carryforward mechanics.

Conversation overview:

- Welcome, Introductions, and Agenda Overview

- Mechanics of Carrybacks and Carryforwards: Rules, Caps, and Filing Forms (1139/1120X)

- Documentation, Negotiating Payment Timing, and Managing Cash Flow for Refunds

- Practical Considerations: IRS Refund Timing, Interest Payments, JCT Review, and Audit Risk

- Buyer Profile, Strategy, and Credit Ordering Rules for Carryback Optimization

- Market Update: Supply, Pricing Trends, and Emerging Credits (45Z Clean Fuel and 45U/45Y Nuclear)

- Audience Q&A and Final Closing Remarks

Alex Melehy

November 3, 2025

Apprenticeship Requirements for Clean Energy Projects: Ratios, Good Faith Efforts, and Common Gaps

To protect the IRA's PWA 5x bonus credit multiplier, clean energy developers and contractors must meet three apprenticeship requirements—labor hour thresholds, the participation rule, and journeyworker ratios—and failing to track these in real time is the most common and costly compliance mistake in PWA projects.

For Sellers

During clean energy project development, prevailing wage rules get most of the attention, but apprenticeship compliance is where projects actually trip up. Across the PWA projects Reunion tracks, failure to meet apprenticeship standards is the single biggest compliance risk—and the most misunderstood requirement of the Inflation Reduction Act (IRA).

To lock in the 5x bonus credit multiplier, developers and EPCs need to satisfy three core apprenticeship rules—or properly document a Good Faith Effort (GFE).

The Three Apprenticeship Requirements

1. Labor Hour ThresholdsA set percentage of total construction labor hours must be performed by qualified apprentices. The threshold depends on when the project began construction:

- 10% for projects that began construction before 2023

- 12.5% for projects that began construction in 2023

- 15% for projects beginning construction in 2024 or later

2. The Participation RequirementAny contractor, subcontractor, or taxpayer employing four or more laborers or mechanics on a clean energy project must employ at least one qualified apprentice.

3. Apprentice-to-Journeyworker RatiosApprentices must be supervised according to the daily apprentice-to-journeyworker ratios set by the applicable Registered Apprenticeship Program (RAP). If a contractor puts too many apprentices on site without enough journeyworkers to meet the daily ratio, the excess apprentice hours don't count toward the labor hour requirement—and those workers must be paid the full journeyworker prevailing wage.

Good Faith Efforts (GFE): Where Projects Fall Short

If a contractor can't find qualified apprentices, the IRS provides a Good Faith Effort exception. A contractor is excused from the participation requirement if the contractor requests apprentices from a RAP and either the request is denied (for reasons other than the contractor's refusal to comply with the program's standards) or the RAP doesn't respond within five business days. On top of that, a valid GFE generates a block of labor hours—based on the hours the requested apprentices would have worked—that counts toward the project-level apprentice labor hour requirement. That means even if no apprentices end up on site, the GFE hours still help close the labor hours gap.

In practice, though, many GFEs Reunion reviews are incomplete or flat-out invalid. The most common mistakes:

- Timing errors: The first request has to be made in writing at least 45 days before the apprentice is needed. Follow-up requests to the same program must go out at least 14 days in advance.

- Wrong recipients: Requests have to go directly to the RAP. Reaching out to a labor union—even one with a project labor agreement—doesn't count.

- Expiration: A GFE isn't a blanket pass for the life of the project. It only covers 365 days, so contractors need to re-submit requests annually to keep the exception active.

The "Zero Hours" Trap

The most common compliance gap we see? Zero apprentice hours. Contractors familiar with Davis-Bacon often don't realize the IRA added stricter apprenticeship rules, and they wrap up projects with no apprentice labor logged at all—well short of the 12.5% or 15% threshold.

We've reviewed projects where crews worked 500+ hours without a single apprentice on site and had no GFE documentation to cover the shortfall. By the time the project closes out, the only fix is costly penalties. The IRS penalty is $50 for every hour you're short, and it jumps to $500 per hour for intentional disregard.

You can't afford to wait until closeout to run the numbers. The only way to avoid this is tracking apprentice ratios, participation, and GFE submissions in real time—throughout the project, not after it's done.

Alex Melehy

October 29, 2025

A Comprehensive Guide to Complying with Beginning of Construction Requirements

Explore updated beginning of construction (BoC) requirements for wind & solar projects. Know eligibility, safe harbors & IRS 2025 guidance for renewable energy tax credits

For Buyers

For Sellers

Defining the beginning of the construction date for a renewable energy project has historically been a thorny task for developers with respect to tax credits qualification. A project’s beginning of construction (BoC) date is widely referenced in the statutes and related Treasury guidance governing clean energy tax credits. Notably, the BoC date determines:

- Eligibility of the project for certain tax credits/bonus credits

- Exemption from prevailing wage and apprenticeship requirements

- Exemption from PFE/FEOC restrictions

Historically, the two ways to establish BoC are by starting physical work of a significant nature, or by proving spend-to-date exceeds 5% of the total project costs (the “Five Percent Safe Harbor”).

Physical work of a significant nature

A taxpayer can establish BoC by starting physical work of a significant nature (within the meaning of section 4 of Notice 2013-29) and thereafter maintaining a continuous program of construction (“Continuous Construction”). Physical work may occur on-site or off-site, performed by either the taxpayer or by another party under a binding written contract. On-site physical work does not include preliminary activities such as planning and design, obtaining permits and licenses, or performing surveys, studies, test drilling, site clearing, or excavation for the purpose of recontouring land (as distinguished from excavation for footings and foundations).

For a wind facility, some examples of on-site physical work include the beginning of the excavation for the foundation, the setting of anchor bolts into the ground, or the pouring of the concrete pads of the foundation. For off-site physical work, the manufacture of components must be done pursuant to a binding written contract, with such components not held in a manufacturer’s inventory.

One of the most common ways to satisfy physical work of a significant nature through off-site means is through physical work on a custom-designed transformer that adjusts the voltage of electricity generated by a project for purposes of transmission and distribution.

Five percent safe harbor

Alternatively, a taxpayer can establish BoC through the Five Percent Safe Harbor by paying or incurring (within the meaning of §1.461-1(a)(1) and (2)) five percent or more of the total cost of the facility and thereafter making continuous efforts towards completion of the facility (“Continuous Efforts”). Only costs properly included in the depreciable basis of the facility are taken into account to determine whether the Five Percent Safe Harbor has been met; the total cost of the facility does not include the cost of land or any property not integral to the facility.

Continuity safe harbor

Given that both physical work of a significant nature and the Five Percent Safe Harbor require continuous progress toward completion once construction has begun via either Continuous Construction or Continuous Efforts (collectively, the “Continuity Requirement”), the IRS also provides a safe harbor (the “Continuity Safe Harbor”) pursuant to which the Continuity Requirement is deemed to be satisfied if a taxpayer places a project in service by the end of a calendar year that is no more than four calendar years after the calendar year during which construction began. For example, a project that begins construction in early 2026 will have until the end of 2030 to be placed in service. Notice 2021-41 extended the four-year window to six years for projects where construction began in 2016, 2017, 2018, or 2019, and to five years for projects where construction began in 2020.

Changes to BoC for solar and wind projects under §45Y and §48E

Under the OBBBA, solar and wind projects are subject to an early phasedown in tax credits; projects seeking §45Y or §48E credits must be placed in service before January 1, 2028, unless the projects started construction before July 5, 2026. As a result, solar and wind developers have been racing to establish BoC in order to secure additional time to complete projects. In connection with the OBBBA, President Trump issued Executive Order 14315, directing the Treasury to issue new and revised beginning of construction guidance within 45 days of the order. On August 15, 2025, the Treasury updated guidance (via Notice 2025-42) for purposes of determining whether a wind or solar project has started construction under §45Y or §48E.

Under Notice 2025-42, solar projects with a maximum net output of greater than 1.5 megawatts and all wind projects must perform physical work of a significant nature to establish the beginning of construction. These projects can no longer utilize the Five Percent Safe Harbor and must also maintain a continuous program of construction, which can be satisfied through the existing Continuity Safe Harbor if the project is placed in service by the end of a calendar year that is no more than four calendar years after the calendar year during which construction began.

One notable language change in the physical work requirement is that under the previous Notice 2013-29, a taxpayer could establish the beginning of construction by “starting” physical work of a significant nature, whereas the new Notice 2025-42 requires that the work be “performed.”

Other than re-stating that “there is no fixed minimum amount of work or monetary or percentage threshold required,” Treasury did not draw clear lines on what is required to meet the standard of performing physical work of a significant nature. Financing and insurance markets will need to determine where they are comfortable drawing the lines.

Certain projects can continue to use the old BoC rules that were in place before Notice 2025-42, and therefore can continue to use the Five Percent Safe Harbor:

- Projects that can establish BoC (using the old BoC rules) before September 2, 2025.

- Solar projects with a maximum net output of 1.5 MW or less. This capacity is generally measured at each inverter, though facilities will need to aggregate their output if they (i) are owned by the same taxpayer, (ii) are placed in service within the same year, and (iii) use the same point of interconnection.

The BoC guidance in Notice 2025-42 only pertains to tax credit qualification for wind and solar projects under §45Y and §48E; PFE/FEOC guidance (which is expected to include BoC provisions) is still being drafted by Treasury.

Guidance

Over a series of notices beginning in 2013, the IRS has established the standards for determining the date that a project began construction.

These notices remain the applicable standards for any references to BoC as it relates to the tax credits and associated guidance.

Frequently Asked Questions about the Beginning of Construction

- How is “Beginning of Construction” defined across different IRA tax credit sections, and what documentation substantiates compliance?

- Beginning of Construction (“BoC”) is established either by performing physical work of a significant nature or by meeting the Five Percent Safe Harbor (incurring ≥5% of total facility costs). The BoC definition is consistent across IRA tax credit types. Documentation to demonstrate BoC may include construction logs, invoices, contracts, images of site construction, or satellite imagery proving physical work.

- How do delays, redesigns, or partial project transfers affect the original BOC date and credit eligibility?

- The original BoC date generally remains valid if the taxpayer maintains Continuous Construction or Continuous Efforts, or qualifies under the Continuity Safe Harbor (usually 4 years to place in service). Transfers or redesigns may risk eligibility if they disrupt continuity or materially change project scope.

- What strategies can developers use to establish BoC early, in order to lock in eligibility before regulatory or incentive changes?

- Developers can begin physical work (e.g., foundation excavation, transformer manufacturing) or incur ≥5% of total costs under a binding written contract before a cutoff date. These actions “lock in” eligibility under current credit rules and rates.

- How do off-site manufacturing or preliminary activities (like grading or engineering) factor into BoC determinations?

- Offsite manufacturing counts towards the establishment of BoC only if performed under a binding contract for project-specific components that are not held in inventory. Preliminary activities (e.g., planning, grading, surveys, permit work) do not qualify as Begining of Construction.

- How should developers coordinate BoC documentation across multiple EPCs or component suppliers for audit readiness?

- Developers should maintain centralized records of binding contracts, invoices, manufacturing milestones, and delivery logs from all EPCs and suppliers. Consistent date tracking and certification statements ensure defensible audit evidence of BoC and continuity.

- How does BoC interact with prevailing wage/apprenticeship and domestic content rules for determining applicable credit multipliers?

- The BoC date determines whether a project is subject to or exempt from enhanced credit requirements under the IRA.

- Prevailing Wage & Apprenticeship (PWA):

- Projects that began construction before January 29, 2023, are exempt from PWA and automatically receive the 5X multiplier on the base credit rate. Projects starting on or after that date must meet PWA labor and apprenticeship rules to qualify for the higher rate.

- Domestic Content & PFE/FEOC:

- Prevailing Wage & Apprenticeship (PWA):

- The BoC date determines whether a project is subject to or exempt from enhanced credit requirements under the IRA.

- The BoC date “locks in” which Treasury guidance applies to domestic content thresholds (preliminary or final guidance) and could govern future PFE/FEOC sourcing restrictions once guidance is provided by Treasury in 2026.In short, BoC is the regulatory timestamp that fixes which labor and sourcing rules apply to a project’s credit eligibility and credit rate multiplier.

Denis Cook

October 29, 2025

Understanding transferable tax credit carrybacks and carryforwards

Transferable tax credits have created new opportunities for taxpayers to participate in the clean energy transition while offsetting tax liability. Understanding the mechanics of carrybacks and carryforwards is essential to capturing their full benefit.

For Buyers

Key takeaways

Carrybacks create a four-year tax liability window

The ability to carry a clean energy tax credit back 3 years and carry forward 22 years is the core mechanism. For a corporate buyer, this potentially aggregates four years of tax liability (the current year plus the three carryback years), making a carryback a great fit for any tax payers with a trailing federal tax liability. Some examples of strong profiles for a carryback strategy include tax payers with a large, one-time event in a recent tax year or relatively smaller taxpayers looking to aggregate up to four years of liability to make a larger tax credit purchase. The carryback must first be applied to the current tax year, and then carried back to the earliest possible year first, with each year thereafter sequentially. Each tax year is subject to the statutory cap (75% of federal tax liability)

Cash flow is the primary strategic concern

One potential challenge of a carryback is the mismatch between the date the buyer pays for the credit and the date it receives the refund from the IRS. Since a carryback claim is effectively filed simultaneously with the current year's tax return (which may be several months after year-end for corporates), there may be a notable lag. To alleviate this burden, tax credit buyers frequently negotiate delayed / split payment structures (or possibly lower upfront purchase prices) with tax credit sellers to improve the overall return on investment

IRS refund timing is variable (but pays interest)

Once the carryback claim is filed, the refund processing time is variable. The IRS publishes processing statuses online which suggest an approx. 90 day timeline to process carryback claims. Of note, the IRS will pay interest on carryback refund claims outstanding longer than 45 days. Subject to a given taxpayer’s internal cost of capital, some buyers have found interest payments to be accretive to the overall transaction ROI. Carryback refund claims under $5 million are not subject to Joint Committee on Taxation (JCT) review, which may also lead to faster processing.

Credit ordering rules in IRS Form 3800 are key

Taxpayers who have other general business credits (e.g., low-income housing, work opportunity, etc.) should be mindful of the instructions established in the Form 3800 General Business Credit (”GBC”) ordering rules. These rules dictate the order by which certain GBCs (including energy tax credits) must be applied against the current year's tax liability, which can have downstream impacts on carryback or carryforward mechanics

Introduction

The Treasury’s final transferability regulations allow corporations to carry transferable tax credits back up to three years, with the ability to offset up to 75% of prior-year tax liabilities. Companies may also carry credits forward up to 22 years.

Although carrybacks and carryforwards have been available for clean energy tax credits since the introduction of transferability under the Inflation Reduction Act (IRA), it's been only in the past six months that Reunion has seen a meaningful increase in companies exploring and modeling these strategies – with a particular interest in carrybacks.

In our view, this emerging interest in carrybacks reflects market maturity, as both experienced and first-time buyers seek to maximize the value and flexibility of their tax credit investments. By leveraging carrybacks, purchasers can expand the total credit volume under consideration, unlocking more favorable deal terms and better overall returns.

How does a tax credit carryback work?

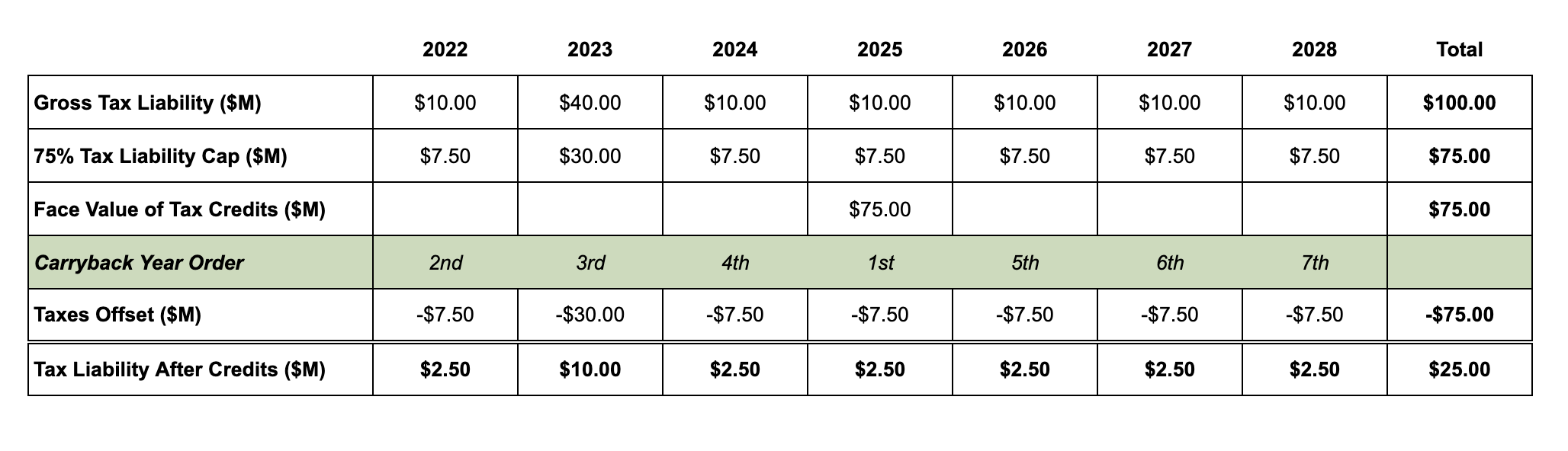

Tax credit buyers can carry credits back three years, and then apply credits forward to subsequent years. A company who purchases 2025 tax credits for a carryback, for instance, would first have to max out their 2025 capacity and then apply any unused amount to 2022, then 2023, and then to 2024. For each year, the company would apply credits up to the statutory cap (75% of total tax liability) before moving on to subsequent years. Buyers do not have the discretion to pick and choose which years to apply carryback credits.

It’s worth reiterating that a company may only carry back credits after they have exhausted their ability to apply those credits to the tax year of the credits. In other words, a company may only carry back 2025 credits once they have hit the 75% statutory cap for 2025.

Taxpayers may also carry applicable IRA tax credits forward up to 22 years.

Assume a taxpayer purchases $75 million of 2025 tax credits and is expected to have a gross tax liability of $100 million from 2022 through 2028. The tax credit deduction would follow the below structure:

What types of companies should consider a carryback?

A carryback generally makes sense for companies who have a significant tax liability across one or more of their three prior tax years. A common use case is a sizable tax event, like a strategic divestiture, within the three-year carryback window.

This holds true for public and private companies, both of whom Reunion has supported in carryback transactions.

When and how do you apply for a carryback refund request?

If a company is requesting a carryback refund via IRS Form 1139, Corporate Application for Tentative Refund, the tax team would typically submit Form 1139 at the same time as, but not in the same package with, their income tax return for the year of the credits they purchased for a carryback.

From Instructions for Form 1139:

- “When to File: Generally, the corporation must file Form 1139 within 12 months of the end of the tax year in which an NOL, net capital loss, unused credit, or claim of right adjustment arose. The corporation must file its income tax return for the tax year no later than the date it files Form 1139.

- Where to File: File Form 1139 with the Internal Revenue Service Center where the corporation files its income tax return. Do not file Form 1139 with the corporation's income tax return.”

Because a company effectively files their refund request at the same time as their income tax return, they will have a concrete understanding of how many credits are unused from the current tax year.

How long should it take to process a carryback refund request?

The IRS has 90 days to process a Form 1139 carryback refund request

The Instructions for Form 1139 states, “The IRS will process this application within 90 days of the later of:

- The date the corporation files the complete application, or

- The last day of the month that includes the due date (including extensions) for filing the corporation's income tax return for the year in which the loss or credit arose (or, for a claim of right adjustment, the date of the overpayment under section 1341(b)(1))”

Importantly, receiving a refund doesn't validate the application. The IRS may later assess penalties and interest for overvalued property, negligence, rule disregard, or substantial income tax understatement if deductions or credits are found incorrect.

Current refund processing times are around 90 days

The IRS publishes processing statuses for various tax forms online. As of the publication date of this note (October 2025), the IRS is processing Form 1139s from June 2025 – that is, generally within the prescribed 90-day window.

Reunion accessed the IRS processing status webpage on October 29. The footer stated that the page was last reviewed or updated on October 24.

Some companies are assuming more than 90 days for modeling purposes

Reunion has supported several corporate tax leaders who are baking additional time into their carryback modeling assumptions. These are generally larger C corporations who are requesting refunds over $5 million, which are subject to another level of review through the Joint Committee on Taxation (JCT).

Most of these companies consider 90 days their best-case scenario and anticipate that a refund could take longer – perhaps six to nine months.

The IRS pays interest on refunds that take longer than 45 days

It's worth bearing in mind that the IRS pays interest on refund requests that take longer than 45 calendar days (from the point at which the IRS deems the application complete).

For companies with relatively low costs of capital, the interest paid by the IRS may, in fact, be accretive to the overall transaction ROI.

What types of credits are most suitable for a carryback?

Tax credits with wider discounts generally work well

All transferable tax credits, irrespective of discount, can be suitable for a carryback as long as they are “applicable credits.” We included an exhaustive list below.

Generally speaking, however, due to the time-value-of-money implications of the refund process, tax credits with wider discounts are most suitable for a carryback. Section 48 ITCs and Section 45Z CFPCs, which tend to trade in the low $0.90s, are commonly used for carrybacks.

Delayed payments and delayed transactions can also make the economic case for a carryback

A buyer can achieve a comparable time-value-of-money benefit by negotaiting delayed payment with the seller. Reunion supported a publicly traded buyer, for instance, who purchased 2025 Section 45 PTCs for a carryback from a seller who was willing to accept payment in June 2026.

Along the same lines, a buyer can simply wait to purchase tax credits until their tax filing date is closer. Reunion supported over a dozen 2024 tax credit transfers in September 2025 alone, and many of these transactions involved a carryback allocation. It's worth recalling, however, that tax credit prices generally rise as tax filing dates approach.

Keep in mind your company's other general business credits

Taxpayers who have other general business credits ("GBC") – for example, R&D and low-income housing – should be mindful of the ordering rules established in Instructions for IRS Form 3800. These rules dictate the order by which GBCs (including energy tax credits) must be applied against the current year's tax liability, which can have downstream impacts on carryback or carryforward mechanics.

Several of Reunion's banking clients who have LIHTC exposure prioritize Section 45Z CFPCs over Section 48 ITCs because of the general business credit ordering rules: investment credits (including "energy credits" claimed on IRS Form 3468) are used before low-income housing credits.

"Applicable credits" that are eligible for a carryback

The following transferable tax credits are “applicable credits” that are eligible for carrybacks (per Section 39(a)(4) and Section 6417(b)):

- Section 48 ITCs

- Section 48E ITCs

- Section 45 PTCs attributable to qualified facilities which are originally placed in service after December 31, 2022

- Section 45Y PTCs

- Section 45X advanced manufacturing production credits

- Section 45U zero-emission nuclear power production credits

- Section 45Z clean fuel production credits

- Section 48C qualifying advanced energy project credits

- Section 45V clean hydrogen production credits attributable to qualified facilities which are originally placed in service after December 31, 2012

- Section 45Q carbon oxide sequestration credits attributable to carbon capture equipment which is originally placed in service after December 31, 2022

- Section 30C alternative fuel vehicle refueling property credits which, pursuant to subsection (d)(1) of such section, are treated as a credit listed in Section 38(b)

Watch Reunion's webinar on tax credit carrybacks and carryforwards

Reunion hosted a webinar, The Role of Carrybacks & Carryforwards in Clean Energy Tax Credit Transactions, on November 12. Our Head of Commercial Strategy, Alessio De Falcis, led a panel of tax and legal experts from CLA, Orrick, and McDermott to explored how carryback and carryforward provisions work and what they mean for corporate tax credit purchasers.

The panel discussed:

- How carryback and carryforward provisions apply to transferred credits under the IRA

- Key considerations for timing, documentation, and compliance

- How purchasers can plan for credit utilization across multiple tax years

- IRS guidance updates and emerging best practices from prior filing cycles

- Practical insights from recent transactions

We published a recording and transcript of the webinar.

Alex Melehy

October 27, 2025

A Comprehensive Guide to Prohibited Foreign Entities for Clean Energy Tax Credits

Learn how OBBBA’s new foreign entities of concern (FEOC) expand clean energy tax credit restrictions, eligibility, effective control agreements & compliance.

For Buyers

For Sellers

The One Big Beautiful Bill Act (OBBBA) added new “Prohibited Foreign Entity (PFE)” restrictions, primarily intended to prevent Chinese companies from benefiting from tax credits, and to reduce reliance on China for clean energy technology. PFE restrictions apply to entities connected to China, Russia, North Korea, and Iran, and prohibit them from claiming §48E, §45Y, §45X, §45U, §45Z, and §45Q tax credits, either directly or indirectly.

PFE restrictions are broadly divided into two sets of rules:

- Taxpayer level restrictions: taxpayers claiming §48E, §45Y, §45X, §45U, §45Z, and §45Q tax credits may not be a prohibited foreign entity (PFE), and the tax credit may not be transferred to a PFE (see Taxpayer level FEOC restrictions below). For §48E, §45Y, §45X credits, taxpayers may not give “effective control” to a specified foreign entity (SFE) through a binding contract or licensing agreement (see Effective control FEOC restrictions below)

- Project level restrictions: taxpayers claiming §48E, §45Y, and §45X tax credits may not receive “material assistance” from a PFE through the use of manufactured products or eligible components (see Material assistance FEOC restrictions below).

PFE restrictions take effect in tax years beginning after the OBBBA date of enactment: July 4, 2025. Projects claiming legacy §45 or §48 credits are not subject to any of the PFE restrictions. §45Y and §48E projects that start construction for tax purposes before January 1, 2026, are not subject to project-level material assistance requirements (but are subject to the entity-level restrictions beginning in the taxpayer’s first taxable year after enactment of the OBBBA).

Buyers will need to perform careful due diligence to ensure PFE compliance.

Taxpayer-level restrictions

Prohibited foreign entities (PFEs), which can be either a specified foreign entity (SFE) or a foreign-influenced entity (FIE), are not allowed to claim the following tax credit types: §45Y, §48E, §45X, §45Q, §45U, and §45Z

For §45Y, §48E, §45X, and §45Q, both SFEs and FIEs cannot claim credits starting the tax year beginning after July 4, 2025.

For §45U and §45Z, the prohibition on SFEs starts the tax year beginning after July 4, 2025. The prohibition on FIEs starts the second tax year beginning after July 4, 2025.

Specified foreign entities

Per §7701(a)(51)(B), an SFE is defined to be one of the following:

- A “foreign entity of concern” as defined in the William M. (Mac) Thornberry National Defense Authorization Act (NDAA) for Fiscal Year 2021. Entities meeting this criteria include foreign terrorist organizations, entities owned by the Chinese, Russian, North Korean, or Iranian government (the “Covered Nations” as defined in §4872(f)(2) of title 10, United States Code), and entities that could be a threat to national security

- A Chinese military company as defined in §1260H of the William M. (Mac) Thornberry National Defense Authorization Act for Fiscal Year 2021

- An entity manufacturing products that benefits from Uyghur forced labor in Xinjiang in China, per §2(d)(2)(B) of Public Law 117-78

- An entity included on the OFAC list that could pose a threat to national security per §154(b) of the National Defense Authorization Act for Fiscal Year 2024

- A “foreign-controlled entity” (FCE) as defined per §7701(a)(51)(C) as an entity that is 50% or more owned by one of the following:

- A government of one of the Covered Nations

- An agency of one of the governments of a Covered Nation

- A citizen or national from a Covered Nation (if not also a citizen, national, or green card holder of the United States)

- A company with its primary place of business in a Covered Nation

Foreign-influenced entity

As defined in §7701(a)(51)(D), an FIE is an entity where an SFE has “influence” in at least one of the following ways:

- An entity where the SFE has “direct authority” to appoint a “covered officer” (such as a board member, CEO, CFO, COO, general counsel, or senior vice president, defined in §7701(a)(51)(F))

- An entity that is 25% or more owned by an SFE

- An entity that is 40% or more owned by multiple SFEs

- An entity with 15% or more debt held by at least one SFE when issued

- An entity with “effective control” through contractual payments, as defined in the next section

Effective control restrictions

The OBBBA adds additional restrictions to entities that make “applicable payments” to an SFE during the taxable year through a binding contract or licensing agreement, therefore giving “effective control” (as defined in §7701(a)(51)(D)(ii)) over either the project, manufactured products, or eligible components as it relates to the claimed tax credits of §45Y, §48E, or §45X. The IRS will provide additional guidance to aid developers in identifying an instance of effective control. In the meantime, entities should avoid giving potential SFEs the unrestricted contractual right to:

- Determine the quantity or timing of production of an eligible component (for §45X)

- Determine the amount or timing of activities related to the production or storage of electricity (for §45Y or §48E)

- Determine which entity may purchase or use the eligible components or critical minerals

- Determine which entity may purchase or use the electricity

- Restrict access to data critical to production or storage of energy, or to the factory, mine, or mineral processing facility, to the personnel or agents of such contractual counterparty, or

- On an exclusive basis, maintain, repair, or operate any plant or equipment which is necessary to the production of eligible components or electricity

Effective control can also be triggered if a taxpayer enters into a licensing agreement with an SFE after the OBBBA date of enactment that gives the SFE a significant role. Entities should avoid giving potential SFEs the contractual right to:

- Specify or otherwise direct one or more sources of components, subcomponents, or applicable critical minerals to be used in an electricity or energy storage project, or in the production of an eligible component

- Direct the operation of an electricity or energy storage project, or a facility that produces eligible components or critical minerals

- Limit the taxpayer's utilization of intellectual property related to the operation of an electricity or energy storage project, or in the production of an eligible component

- Receive royalties for more than 10 years

- Require the taxpayer to enter an agreement for the provision of services for a duration longer than 2 years

In addition, manufacturers and mineral producers entering into licensing arrangements should have the “technical data, information, and know-how necessary to enable the licensee to produce the eligible component” without needing further involvement from the counterparty or other specified foreign entity.

A bona fide purchase or sale of intellectual property is not subject to these restrictions. However, arrangements where the “ownership of intellectual property reverts to the contractual counterparty after a period of time” shall not be considered a bona fide purchase or sale.

Recapture for §48E ITCs

In §50(a)(4), the recapture risk for ITCs is extended to ten years if there is any “applicable payment” sent to an SFE, and therefore allowing that entity to have effective control. If any payment is made to an SFE in the ten years after the qualified facility is placed in service, then the entirety of the credit is clawed back. This provision applies to taxpayers who claim a credit for any taxable year beginning after July 4, 2027 (e.g., 2028 and beyond for calendar year filers). This may have the impact of shifting more developers towards claiming a §45Y credit over §48E, if they have the option to do so.

Risk of public companies becoming PFEs

Public companies are largely exempt from being considered an SFE (per §7701(a)(51)(E)), except in the instance where the company is traded on a market in a Covered Nation. Additionally, they are at risk of being considered an FIE if an SFE has the authority to appoint a board member or executive officer. Public companies are also at risk of giving “effective control” to an SFE through a contractual payment or licensing agreement.

Transferred credits to SFEs

The OBBBA amended §6418(g) to prohibit the transfer of a §48E, §45Y, §45X, §45Q, §45U, or §45Z credit to an SFE. Therefore, tax credit transfer transactions involving these credits also need to diligence the purchaser.

Determination

Entities are tested to determine if they qualify as SFEs and FIEs on the last day of the tax year for which the applicable credit is claimed (see §7701(a)(51)(A)(ii)).

The only exception is the first taxable year after July 4, 2025, where the test takes place on the first day of the taxable year. Said another way, all entities will be tested on January 1, 2026, for the 2026 tax year, assuming they have a calendar fiscal year end.

Material assistance restrictions

The OBBBA restricts developers’ ability to claim §45Y, §45X, and §48E credits if they receive “material assistance” from a “prohibited foreign entity” as defined in §7701(a)(52). Material assistance is represented as a percentage of the total direct costs that meet the compliance threshold (for the avoidance of doubt, these are costs that are NOT affiliated with a PFE). For §48E ITCs and §45Y PTCs, the costs analyzed are the labor and material costs of the manufactured products and their components used in qualified facilities. For §45X AMPCs, the costs are the direct material costs of eligible components and critical materials.

In the case of §45Y and §48E credits, projects that begin construction for tax purposes before January 1, 2026, do not need to comply with material assistance requirements. The OBBBA codified that the beginning of construction rules in IRS Notices 2013-29 and 2018-59 (as well as any subsequently issued guidance clarifying, modifying, or updating either Notice), as in effect on January 1, 2025, apply to FEOC requirements. On August 15, 2025, the Treasury issued Notice 2025-42 modifying the BoC rules for wind and solar tax credit eligibility; however, the document reiterates in Footnote 3 that, “The guidance in this notice is not intended to address the beginning of construction rules for those foreign entity restrictions. The Treasury Department and the IRS are currently drafting additional guidance as is necessary and appropriate to implement those restrictions, as enacted by the OBBBA.”

Material assistance for tech-neutral credits (§45Y and §48E)

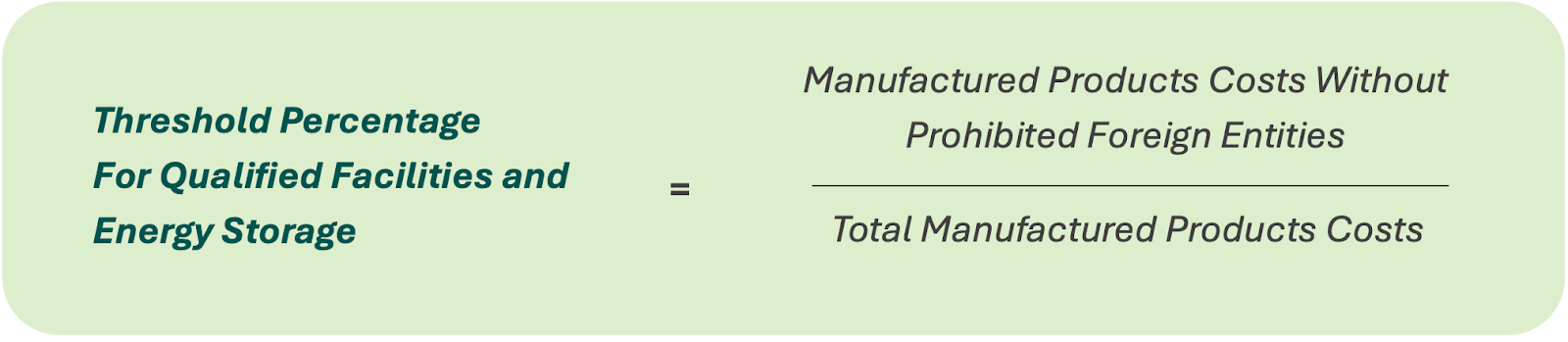

§7701(a)(52)(A)(i) provides guidance on how to meet the “threshold percentage for qualified facilities and energy storage,” as defined based on the following cost ratio for the manufactured products involved:

Total Manufactured Products Costs are the total direct costs for all “manufactured products (including components) which are incorporated into the qualified facility or energy storage technology upon completion of construction." Examples of manufactured products are solar modules and batteries that are produced in a factory, versus on-site construction materials.

Manufactured Products Costs Without Prohibited Foreign Entities are the total direct costs of manufactured products (including components) that are NOT “mined, produced, or manufactured by a prohibited foreign entity” (§7701(a)(52)(D)(i)(II)).

The “threshold percentage for qualified facilities and energy storage technology”, as defined in the above formula, must meet the requirements in the table below, depending on the year when the qualified facility or energy storage technology begins construction.

Threshold percentage requirements (§45Y and §48E)

Per §7701(a)(52)(B), the following threshold percentages apply for qualified facilities and storage technology claiming §45Y PTCs and §48E ITCs:

Material assistance for eligible components (§45X AMPCs)

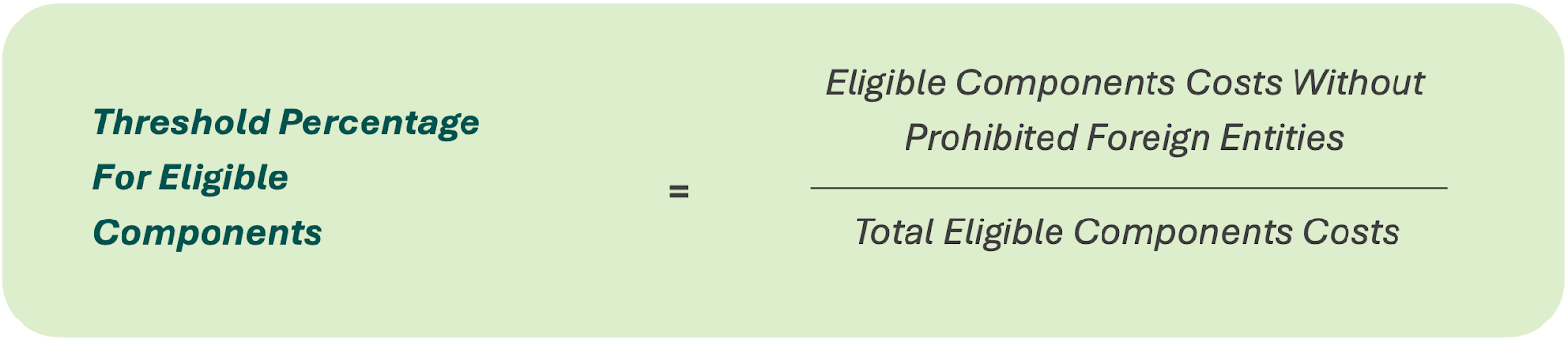

For eligible components and critical minerals, §7701(a)(52)(A)(ii) provides guidance on how to meet the “threshold percentage for eligible components,” as defined based on the following cost ratio for the eligible components involved:

Total Eligible Components Costs are the direct material costs paid or incurred for production of the eligible components.

Eligible Components Costs Without Prohibited Foreign Entities is defined to be the direct material costs paid or incurred for production of the eligible components that are NOT “mined, produced, or manufactured by a prohibited foreign entity” per §7701(a)(52)(D)(ii)(II).

The “threshold percentage”, as defined by the above formula, must meet the requirements in the table below, depending on the year in which the component is sold.

Threshold percentage requirements (§45X AMPCs)

Per §7701(a)(52)(B), the following “threshold percentages” apply for eligible components or critical minerals claiming §45X AMPCs. Note that for applicable critical minerals, the “threshold percentages” will be updated by December 31, 2027, and the OBBB provides Treasury with the discretion to increase these amounts to consider several subjective factors, including domestic availability and processing capacity, supply chain constraints, and national security concerns.

Documentation

Safe Harbor Tables

Per §7701(a)(52)(D)(iii), the IRS is expected to publish tables no later than December 31, 2026, to improve the ease of the calculation of the “threshold percentages” and provide all rules regarding material assistance (for §45Y, §48E, and §45X).

Until these tables are published, taxpayers can use existing domestic content tables from Notice 2025-08, issued in January 2025, and included in Appendix D. The domestic content tables only apply to solar, onshore wind, and battery storage projects. Other project types will need to use the actual material and labor costs that developers paid (note: this contrasts with the domestic content calculations, which require supplier costs).

Certificates

Project developers and manufacturers will ask equipment suppliers to provide certificates confirming whether products were manufactured by PFEs, and whether there are any PFEs in the supply chain. The certificate should confirm the payment amount charged to the taxpayer for non-PFE goods (see §7701(a)(52)(D)(iii)). Certificates should be retained by both the taxpayer and supplier for six years and include the following:

- EIN Number of the supplier

- Any foreign identification number

- Signatures from suppliers

- Statement about the relationship to a PFE, if applicable, for all Manufactured Products Costs or Eligible Components Costs

Material assistance exclusions

In the instance where the Manufactured Products Costs are derived from binding contracts and purchase orders entered into before June 16, 2025, the costs are excluded from the material assistance determination assuming the project begins construction by July 31, 2025, and is placed in service by December 31, 2029 (or by December 31, 2027 for solar or wind projects) (see §7701(a)(52)(D)(iv)). Similarly, for Eligible Components Costs, any costs incurred pursuant to binding contracts and purchase orders entered into before June 16, 2025, will also be excluded for eligible components sold by December 31, 2029.

Material assistance penalties

The IRS can challenge the material assistance determination anytime in the six years after the tax return is filed for a qualified facility, energy storage technology, eligible component, or critical mineral (see §6501(o)), and there are significant penalties if an inaccuracy is discovered. The penalties are calculated based on the understatement of income tax that occurred from the inaccurately claimed tax credit. The following penalties hold:

- Penalty to taxpayer: Per §6662(a), the penalty is 20% of the reduction in the tax basis that benefited from the tax credit if the taxpayer’s underpayment exceeds 1% of what they should have paid or $5,000, whichever is greater. Per §6662(d)(1)(B), if the taxpayer is a corporation, the penalty applies if the taxpayer’s underpayment exceeds 1% of what they should have paid or $10 million, whichever is less.

- Penalty to equipment supplier: Per §6695B, in the instances where a certificate (as described above and in §7701(a)(52)(D)(iii)) is inaccurate, the supplier of that certificate is subject to a penalty that is the greater of 10% of the understatement of the taxpayer’s tax basis, or $5,000. This penalty is only relevant if the understatement is greater than the lesser of 5% of the tax on the tax return or $100,000. Certificates provided before January 1, 2026, are exempt from this penalty.

Practical steps to maintaining compliance

To maintain compliance with PFE restrictions, Reunion recommends an ongoing audit of supply chain entities or potential tax credit purchasers and ongoing attention to contractual language in binding contracts or licensing agreements that could potentially provide “effective control” to a counterparty.

PFE restrictions are evolving and will likely gain additional clarity with the publishing of Treasury regulations in 2026. As such, Reunion recommends working with a knowledgeable third party to ensure ongoing compliance with PFE restrictions as well as maintaining records demonstrating PFE compliance for at least six years.

High-level compliance checklist

The following items are overall suggestions of evidence to maintain for proving PFE compliance in an ongoing manner. These items are not exhaustive and, given the dynamic nature of PFE restrictions, should not be considered a comprehensive list.

Taxpayer-level SFE requirements

Maintain the following evidence to verify that the taxpayer itself is not an SFE.

- Documentation of ownership structure listing all entities with direct ownership of the taxpayer entity

- Certificates of formation/incorporation for all entities within the ownership structure

- Exchange listing documentation (for publicly traded entities)

Taxpayer-level FIE requirements

Maintain the following evidence to verify that the taxpayer itself is not an FIE.

- Documentation of ownership structure listing all entities with direct ownership of the taxpayer entity

- Certificates of formation/incorporation for all entities within the ownership structure

- Complete list of debt holders showing total debt amounts

- Documentation showing any SFE “direct authority” to appoint a “covered officer”

Effective control requirements

Maintain the following evidence to verify that over the previous tax year, an SFE did not hold “effective control”, as defined in §7701(a)(51)(D)(ii), over key aspects of the production of eligible components, energy generation in a qualified facility, or energy storage which are not included in the measures of control through authority, ownership, or debt.

- Operations, Maintenance, or Asset Management Agreements: including long-term service, performance, or dispatch authority terms

- Supply, Procurement, or Manufacturing Agreements: for equipment, components, or critical minerals, especially those specifying approved vendors or sourcing restrictions

- Power Purchase, Offtake, or Energy Storage Agreements: governing generation schedules, dispatch, or output allocation

- Licensing or Technology Agreements: covering intellectual property, software, or SCADA systems used in production or operation

- Construction or EPC Contracts: where counterparties retain operational authority, site access, or equipment control rights

- Joint Venture, Development, or Shareholder Agreements: involving shared governance, veto, or consent rights

- Financing, Lease, or Royalty Agreements: imposing operational conditions, long-term payments, or extended obligations

- Data Access or Remote Operations Agreements: granting privileged access to system controls or operational data

- Consulting, Technical Service, or Training Agreements: that create long-term dependence or ongoing foreign involvement

Material assistance requirements

Maintain the following evidence to verify that the labor and material costs of manufactured products and their components (§48E and §45Y) or the direct material costs of eligible components and critical materials (§45X) used in a qualified facility exceeded the statutory thresholds for total costs not paid to a PFE as defined in §7701(a)(52) of the U.S. Code.

Supply chain mapping

- Documentation listing all suppliers and sub-suppliers of Covered Items for each qualified facility, including entity names, addresses, and countries of formation/operation

- Bills of materials, purchase orders, and invoices identifying all Covered Items and their source entities

- Payment records and proof of transaction completion

- Agreements with contractors, subcontractors, and suppliers

- Confirmation of physical receipt or completion of services for the Covered Items

Supply chain mapping

- Documentation listing all suppliers and sub-suppliers of Covered Items for each qualified facility, including entity names, addresses, and countries of formation/operation

- Bills of materials, purchase orders, and invoices identifying all Covered Items and their source entities

- Payment records and proof of transaction completion

- Agreements with contractors, subcontractors, and suppliers

- Confirmation of physical receipt or completion of services for the Covered Items

48E recapture requirements

Maintain the following evidence to verify that no “applicable payments” to an SFE have been made that would entitle the SFE to exercise “effective control” (as defined in §7701(a)(51)(D)(i)(II)), during the ten-year period after the facility has been placed in service.

- Operations, Maintenance, or Asset Management Agreements: including long-term service, performance, or dispatch authority terms

- Supply, Procurement, or Manufacturing Agreements: for equipment, components, or critical minerals, especially those specifying approved vendors or sourcing restrictions

- Power Purchase, Offtake, or Energy Storage Agreements: governing generation schedules, dispatch, or output allocation

- Licensing or Technology Agreements: covering intellectual property, software, or SCADA systems used in production or operation

- Construction or EPC Contracts: where counterparties retain operational authority, site access, or equipment control rights

- Joint Venture, Development, or Shareholder Agreements: involving shared governance, veto, or consent rights

- Financing, Lease, or Royalty Agreements: imposing operational conditions, long-term payments, or extended obligations

- Data Access or Remote Operations Agreements: granting privileged access to system controls or operational data

- Consulting, Technical Service, or Training Agreements: that create long-term dependence or ongoing foreign involvement

Guidance and resources

Guidance

- July 4, 2025: One Big Beautiful Bill Act, Chapter 5.

Resources

The OBBBA passed on July 4, 2025, and federal resources are still being updated with amended sections.

President Trump issued a July 7, 2025, Executive Order signaling that further guidance may be released as soon as 45 days after the enactment of the bill, and Notice 2025-42 denoted that guidance relating to FEOC restrictions is still forthcoming. The IRS will also release guidance on identifying PFEs no later than December 31, 2026 (see §7701(a)(51)(D)(iii)).

Frequently Asked Questions about Prohibited Foreign Entities

- How do PFE restrictions most impact eligibility for clean energy tax credits and financing?

- PFE restrictions, as introduced by the OBBBA, prohibit Prohibited Foreign Entities (PFEs) from claiming §45Y, §48E, §45X, §45Q, §45U, and §45Z tax credits. Additionally, tax credits may not be transferred to a PFE.

- What supply chain tracing methodologies are being accepted to demonstrate compliant sourcing of critical minerals and components?

- Taxpayers will need to verify which entities in their supply chains are considered PFEs and ultimately comply with the statutory supply thresholds specified by the IRS and Treasury. Per §7701(a)(52)(D)(iii) of the U.S. Code, the IRS is expected to publish tables no later than December 31, 2026, to improve the ease of the calculation of the “threshold percentages” and provide all rules regarding material assistance (for §45Y, §48E, and §45X). Until these tables are published, taxpayers can use existing domestic content tables from Notice 2025-08, issued in January 2025. The domestic content tables only apply to solar, onshore wind, and battery storage projects. Other project types will need to use the actual material and labor costs that developers paid (note: this contrasts with the domestic content calculations, which require supplier costs)

- How can developers assess PFE risk exposure during early procurement planning for battery, solar, or wind projects?

- Developers should work with a knowledgeable third party during the procurement phases of a project to ensure that the required percentage of components is sourced from non-PFEs. There are a number of technology and service vendors in the space that are able to assist developers with this assessment.

- What due diligence frameworks or certifications are recognized to prove PFE compliance?

- Given that the PFE requirements introduced by the OBBBA are so new, as of this writing, there are no widely accepted comprehensive formats for demonstrating PFE compliance. That said, §7701(a)(52)(D)(iii) of the U.S. Code provides some guidance on the information that should be included in supplier PFE certifications. Until Treasury guidance is released in 2026, Reunion recommends working with a knowledgeable third-party to gather and document PFE compliance in an ongoing fashion.

- How might evolving geopolitical designations of SFEs affect long-term asset compliance for operational projects?

- The recapture provisions surrounding §48E tax credits with respect to PFE compliance specify that any “applicable payment” as defined in §7701(a)(51)(D)(i)(II) of the U.S. Code, to an SFE that provides the SFE with “effective control” during the ten years after a facility has been placed in service, could result in the recapture of the entire tax credit. Given this risk, it will be important to clarify if evolving SFE designations need to be taken into account when tracking any “applicable payments” to potential SFEs during the recapture period.

- How can joint ventures or partnerships with foreign investors navigate FEOC limitations without jeopardizing credit eligibility?

- Developers should work with a third party with expertise in PFE compliance when navigating credit eligibility in a situation where foreign investors are involved. Developers should ensure documentation of any internal investigations into foreign investors' PFE status, as well as document foreign investors’ corporate formation documents, while ensuring that the investors are not SFE.

Billy Lee

October 9, 2025

An overview of trends in tax credit transfers for sellers - October 2025

An in-depth look at what Reunion is seeing in the market for October and a few recent transactions.

For Sellers

The rush to close out 2024 tax credits is finally coming to an end, with the October 15 tax filing deadline approaching. Read on for highlights on what the Reunion team has been seeing in the tax credit market, along with recent deal highlights.

What we’re seeing in the market:

More buyers are looking to delay payments for 2025 credits until 2026

- Due to the OBBBA, some corporations overpaid their estimated quarterly taxes relative to what they will end up owing for 2025. Therefore, they prefer delaying payments for tax credits until 2026, because they do not anticipate realizing the benefit of the credits until April 15, 2026

- We have observed more buyers looking to pursue carrybacks to offset prior year taxes; carryback buyers typically seek delayed payment terms, given uncertainty around when they will receive tax refunds from the IRS

- In general, we have seen an increasing share of transactions occurring well into the following calendar year, and expect this seasonal trend to continue. For example, Reunion closed approximately 15 transactions for the 2024 tax year, totaling over $550M in credit volume, in the weeks leading up to October 15, 2025

Sellers are showing flexibility in pricing for investment-grade buyers that are willing to forward commit to ITCs that will be generated in 2026 or 2027

- Sellers are unable to get high advance rates from lenders for tax credit transfer bridge loans without a committed buyer. The net advance rate is typically <70% of the face value of the tax credits

- Sellers are showing flexibility in pricing to secure commitments from investment-grade buyers to purchase credits generated in 2026 or 2027

- Reunion has also partnered with a major financial institution to offer forward ITC and 45X commitments for 2026 or 2027 credits with at least $50M in volume; please contact us for pricing and further details

Buyers are demanding §45U credits, and pricing remains high

- A number of large Reunion clients are focused specifically on identifying §45U credits, which are production-based credits generated by nuclear power facilities. Buyers are drawn to the relatively straightforward diligence process, lack of §50 recapture risk, and the current administration’s general support of nuclear power

- Spot 2025 pricing for credits remains elevated due to the fairly small universe of §45U credit sellers; as with other credits, buyers willing to enter into a multi-year agreement can achieve a 1 to 2.5 cent discount on pricing, depending on the length of commitment

Highlights from Recently Closed Transactions

Project Wind River

$150M+ in §45U nuclear credits transacted on a very short closing timeline due to high demand

Credit type: §45U

Overview: Reunion brought two highly motivated, publicly traded companies together to transact on §45U nuclear credits, going from a signed term sheet to closing in two weeks.

Highlights: Looming deadlines meant both buyer and seller needed to lean on legal and advisory resources, including Reunion, to negotiate terms and move quickly through due diligence and approvals.

Project Ginkgo

$75M+ in §48 credits from battery storage project with deferred payment schedule

Credit type: §48

Overview: Reunion worked with a repeat client to sell tax credits from a battery storage project to a publicly-traded buyer.

Highlights:The purchaser was able to offer a premium price in exchange for deferred payment, which was attractive given the seller’s access to low-cost capital. Resulting payment will take place over a year after the project was placed in service.

Reunion's Compliance Software

Tracking Prevailing Wage and Apprenticeship compliance for a large solar developer

Credit type: §48E

Overview: Reunion is under contract with a major solar developer to manage PWA compliance for their entire 2025-2026 portfolio. Reunion's report is a key piece of documentation for the developer's tax equity partner, which is a leading bank.

Highlights: The tax equity partner will receive frequent and thorough PWA updates via Reunion's software throughout the construction and O&M phases. It was critical for the tax equity partner to gain comfort with Reunion's PWA compliance process prior to closing the transaction.

Reunion

September 22, 2025

Frequently asked questions about tax credit transfers

What do transferable tax credits cost? Who pays for insurance and legal fees? Is the tax benefit taxable? This comprehensive FAQ article breaks down the economics, risks, and legislative issues surrounding the growing market for clean energy tax credits.

For Buyers

Economics

What do transferable tax credits typically cost?

Tax credits generally range in price from $0.90 to $0.96. These prices are “all in,” meaning that the cost of tax credit insurance and any broker or intermediary cost is typically borne by the seller. The seller will also typically reimburse buyers for a capped amount of third party legal and diligence fees.

§48 investment tax credits from large, reputable sellers have historically traded in the $0.93 to $0.95 range. In late 2024 and early 2025, we observed sizable ($75M+) credits from investment-grade sellers for the 2024 tax year trading in the $0.95 range. Factors that impact pricing include:

- Financial strength of seller: Buyers pay a premium when seller has a strong balance sheet or investment-grade credit rating

- Credit type: There is more buyer demand for large utility scale projects versus distributed portfolios. Additionally, advanced manufacturing, solar, wind, storage and nuclear have more demand than renewable natural gas or carbon capture technologies

- Volume of opportunity: Buyers pay a premium for larger opportunities ($75M to $100M+). Very small opportunities (<$10 or $15M) have a larger discount due to relatively low absolute savings amount

- Payment terms and timing: Buyers pay a premium for delayed payment terms. Pricing also tends to increase the later a transaction occurs, as project supply dwindles and more last-minute buyers come into the market. Conversely, pricing tends to decrease for forward commitments, especially for those with longer time horizons into future tax years

Leading project developers often have lofty expectations on the pricing they expect to receive on their credits, and as a result there is often a robust back and forth before settling on a price.

Who pays for tax credit insurance?

Sellers typically purchase tax credit insurance, with the buyer listed as an “additional insured” on the policy. Buyers occasionally elect to purchase tax credit insurance instead of the seller, but this scenario is far less common.

Who pays for legal and diligence fees?

To minimize “above-the-line” expenses, buyers typically negotiate for sellers to pay a capped reimbursement amount for documented third party legal and / or diligence fees. The reimbursement is generally an absolute dollar amount (versus a percentage of the credit amount), and generally increases based on the complexity of the transaction. For example, a portfolio with many projects is likely to have a larger expense reimbursement compared to a single utility-scale asset.

Is the benefit — the difference between the face value of the credits and the purchase price — taxable?

The benefit is not subject to federal tax. While many states have rolling conformity to federal taxation rules, we recommend checking with your tax advisor on state-level taxation issues.

Markets

What other corporations are active in purchasing transferable tax credits?

Although public disclosures are very rare, Fortune 500 companies from nearly every sector are actively purchasing clean energy credits. Examples of publicly disclosed transactions include:

- Visa: $870M tax credit purchase from First Solar

- Fiserv: $700M tax credit purchase from First Solar

- MarketAxess: $16M tax credit purchase from Broadwind

What is a typical tax credit purchase amount?

Reunion maintains a database that monitors over $25B of tax credit transactions. We observe that a majority of transactions are in the $15M to $200M range, though we have worked on multiple individual transactions in the $1 billion range.

Corporate taxpayers can offset up to 75% of their federal tax liability with general business credits, which include transferable tax credits. According to a 2024 Reunion survey, 85% of surveyed tax credit buyers plan to offset at least 50% of their tax liability using transferable tax credits.

Risks

What are the primary risks associated with purchasing a tax credit?

§48 ITCs are subject to several primary areas of risk, which buyers should thoroughly diligence:

- Qualification: Validate that the underlying project qualifies as energy property, the proper cost basis is used, and the project was placed in service in the appropriate tax year. If applicable, validate qualification for bonus credit adders such as energy community and domestic content. If applicable, the buyer should also validate that the project complies with Prevailing Wage and Apprenticeship requirements (for projects above 1 MW that began construction on or after January 29, 2023) and Foreign Entity of Concern restrictions (see below for more commentary on FEOC).

- Structure: Validate that seller is an eligible transferor, and that the seller’s underlying legal structure will be respected by the IRS.

- Recapture: ITCs are subject to the recapture provisions of §50. The ITC carries a five-year compliance period, in which the potential amount of credit that can be recaptured starts at 100% for the first year and steps down 20% per year. Practically speaking, recapture can occur in the following scenarios: (1) the property ceases to be a qualified energy facility or (2) there is a change in ownership of the property.

- Counterparty: Buyers should understand the corporate structure of the seller, and identify and diligence any disregarded entities between the project company and the seller. Doing so will ensure proper chain of title of tax credits to the seller. Additionally, buyers should understand the financial strength of the seller and, by extension, the “value” of the seller’s indemnity and / or guaranty

How do I ensure that the tax credits apply to the appropriate tax year?

The placed in service (PIS) date determines the tax year to which the credits can be applied. A project that is placed in service in 2026, for instance, generates ITCs that can be applied to a company’s 2026 tax liability (for calendar-year filers). As part of due diligence, the buyer should review documentation substantiating when the project was placed in service; the IRS employs a five-factor test to determine when a project is PIS for tax purposes.

There is a risk that a PIS date “slips” into a subsequent tax year, and the buyer is unable to apply the credits to a given tax year as planned. To mitigate this risk, buyers will often negotiate a two-tiered pricing approach, in which the price per credit is reduced if the credits slip from one year to the following (we have seen this discount commonly range from 1.5 to 3 cents).

Have other tax credit buyers been subject to audit activity?

There are many tax credit buyers that are in the Compliance Assurance Process (CAP) program; CAP buyers assume that the IRS will audit their tax credit purchase activity at some point. These buyers typically prioritize ensuring that they have all necessary documentation prepared in advance, in the event of an IRS information document request (IDR).

Reunion has worked with several companies in the CAP program that have satisfactorily responded to audit activity, including responding to IDRs.

We have not yet heard of buyers outside the CAP program subject to audit activity from tax credit transfers, but we do expect that it will happen.

Describe how the process works if the IRS does challenge a credit?

Tax proceedings are one of the heavily negotiated points in a tax credit transfer agreement (TCTA).

If the IRS performs an audit of the tax credit buyer and determines that the credits are excessive or invalid, the buyer will typically request an appeal with the IRS Independent Office of Appeals.

If the IRS Independent Office of Appeals upholds the decision, the buyer or the tax credit insurer may choose to proceed to litigation, typically in U.S. District Court or in U.S. Tax Court. The obligation to proceed to litigation, and how far to take the litigation (instead of triggering an indemnity payment from the seller) is a point of negotiation between buyers and sellers.

Tax credit insurers typically will include the right to litigate as part of the terms and conditions of the tax credit insurance policy, as the insurer will want the opportunity to litigate before needing to pay out a claim.

If there is a successful challenge or disallowance of the credit by the IRS, will I be made whole?

In case there is a loss event, a well-negotiated Tax Credit Purchase Agreement will ensure that the buyer will be made whole through the indemnity and / or tax credit insurance. The protections are designed to cover all potential losses, including penalties, interest, taxes, contest costs, and fees.

What are common negotiation points related to tax credit insurance?

One common point of negotiation between buyers and sellers is defining the scope of the tax credit insurance policy, and ensuring that the buyer is comfortable with the covered tax positions as well as any potential exclusions to the policy.

The other primary point is to define the limit of liability on the policy, to ensure that the buyer will be fully covered in the event of a loss. Buyers sometimes agree to a lower limit of liability in exchange for better pricing on the credit, or in cases where they see other factors that reduce risk on the transaction (e.g., strong seller balance sheet).

Legislative

Under what conditions are credits subject to new OBBBA provisions, such as foreign entity of concern (FEOC)?

Projects that began construction before the end of 2024 have the option to qualify for §48 credits rather than §48E credits. §48 credits are not subject to FEOC restrictions.

§48E credits that begin construction before the end of 2025 are not subject to the FEOC material assistance restrictions, which limit the amount manufactured products that can originate from restricted countries (China, Iran, North Korea, and Russia).

What happens if there’s another change in law between when execution of a tax credit transfer agreement, and funding of the transaction?

The tax credit transfer is not officially consummated until the transfer election statement is filed when the buyer and seller file their tax returns. Buyers typically negotiate TCTAs to include “no change in law” as a condition precedent (CP) to funding. Therefore, if there is a significant change in law between signing the TCTA but before funding, the buyer would have the option to walk away from the transaction.

Billy Lee

September 5, 2025

An overview of trends in tax credit transfers for sellers - September 2025

A look at market trends and insights, along with some highlights from recent Reunion transactions.

For Sellers

Starting in August, we have observed a wave of 2024 deals rushing to close, as buyers and sellers approach their final tax filing deadlines. We have been surprised by the volume of last-minute deals; Reunion is currently working to complete over $500M in transactions across more than a dozen deals with a 9/15 or 10/15 filing deadline.

Please reach out if you have credit opportunities that you would like to place with our pool of corporate buyers for the 2024, 2025, or 2026 tax years. We are seeing particular demand for:

- Last-minute 2024 tax credit opportunities of any size

- Large ($150M+) opportunities for the 2025 or 2026 tax year

Read on below for our September Market Digest series, which highlights Reunion’s market observations and recent deal highlights.

What we’re seeing in the market:

More buyers are coming to the table with specific pricing and terms in mind.

We view this as a sign of market maturity, as buyers have a clearer sense of terms they believe are fair. We have also observed more buyers who have successfully lined up internal approvals in advance and have a mandate to identify credits that meet certain criteria. Some examples of buyers with specific requirements on pricing and terms:

- Investment-grade buyer looking to pay $0.92 for 10-year PTC strips at a volume of up to $50M / year.

- Investment-grade buyer looking to pay in the low $0.90s for a forward commitment for 2026 ITCs, with transaction sizes of $175M and above. Requires tax credit insurance.

- Experienced buyer looking to pay $0.95 or better for “lowest risk” PTCs or AMPCs, with transaction sizes around $100M. Requires a seller with an investment-grade rating or a creditworthy balance sheet.

More buyers are willing to forward commit to credits for 2026 and beyond.

- While forward commitments for ITCs have been sparse in the past, we are seeing more taxpayers interested in committing now to get better deals for the 2026 or 2027 tax year.

- Buyers looking to forward commit to ITCs tend to be larger taxpayers who are comfortable making investments in advance, given their predictable annual tax liability. We find that taxpayers looking for ITCs below ~$15 or $20M tend to be more “opportunistic,” and look for tax credits as the year progresses or as their tax payments come due.

- We are also seeing buyers of various sizes look to lock in 10-year PTC strips at a discount.

New Beginning of Construction rules

The Treasury Department released new beginning of construction (BoC) rules for purposes of determining the timing of credit eligibility for wind and solar projects. We anticipate an uptick in developers that will need to find ways to use on-site physical work to establish beginning of construction.

- The Treasury Department released new BoC guidance that came into effect on Sept 2, 2025, that requires wind and solar projects to establish beginning of construction by starting physical work. The 5% safe harbor, which has widely been used in the past, now only applies to solar projects below 1.5MW.

- Many larger developers had planned to use transformer procurement as their BoC strategy, which qualifies as physical work and will continue to be respected under the new rules.

- Developers that did not plan to use a transformer or other off-site physical work strategy may not find it easy to procure transformers on short notice or favorable terms. We anticipate developers will increasingly use on-site physical work to establish BoC.

- Reunion offers a compliance product that helps developers establish and substantiate on-site physical work BoC.

Highlights from Recently Closed Transactions

Project Pinnacles

$45M in 2024, §48, §30C, Portfolio of onsite solar, storage and EV charging