Connor Danik

May 6, 2026

A New Kind of Club Deal: Efficiently Structuring a $30 Million §45Z Transaction

The mechanics of how a Clean Fuel Tax Credit transaction scaled up

For Buyers

For Sellers

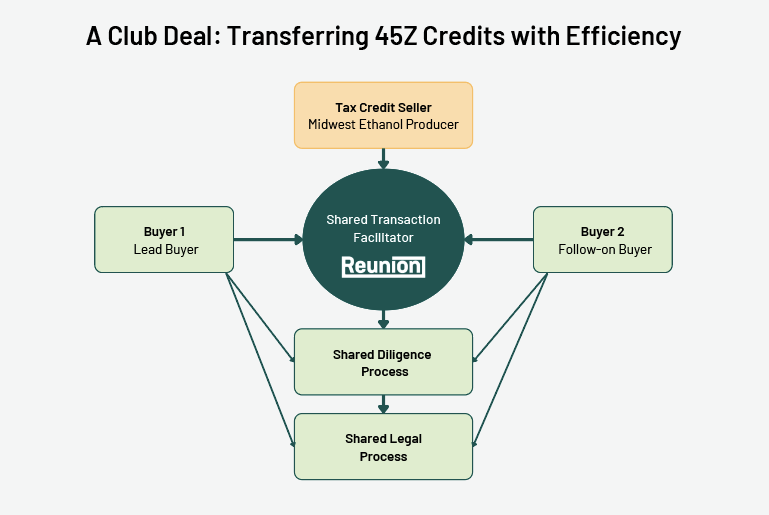

In Q1 2026, Reunion facilitated a $30 million §45Z tax credit transfer among a major Midwest ethanol producer and two publicly traded banks.

Reunion structured the transaction as a “club” deal, with the two buyers — while additional participants could have been included — aligning on negotiations, timing, due diligence, legal processes, and tax credit insurance requirements.

The deal offers insights not only into the mechanics and due diligence requirements of §45Z, but also how the club model can enable scale and efficiency.

The Credit

The §45Z PTC has become one of the most widely adopted credits to emerge from the Inflation Reduction Act. Available for transportation fuel produced domestically and sold between January 1, 2025 and December 31, 2029, the credit covers a range of low-carbon fuels such as ethanol, renewable natural gas, renewable diesel, and sustainable aviation fuel.

§45Z, like many production credits, is not subject to §50 recapture. This structural feature distinguishes it from §48 and §48E investment tax credits, which often trade at a deeper discount due to the need to diligence and protect against the risk of recapture.

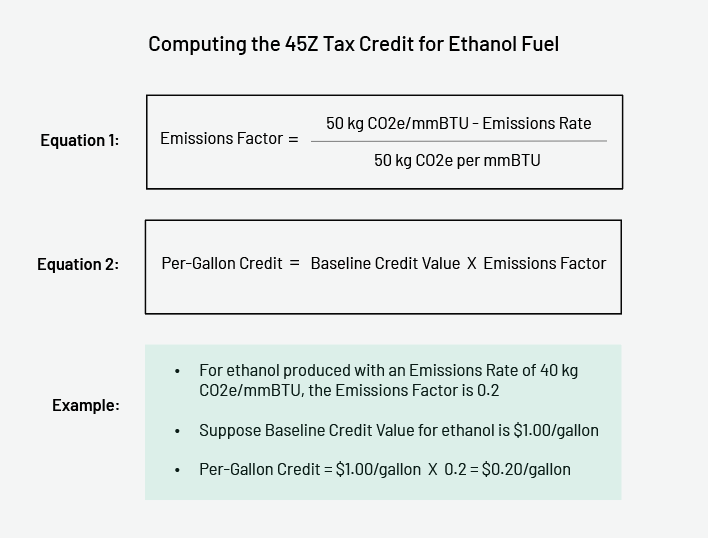

The §45Z PTC has garnered broad adoption, in large part, because it offers a sliding scale of credit value based on the emissions factor of the fuel. The base credit tops out at $1.75 for sustainable aviation fuel and $1.00 per gallon for other clean fuels. These credit amounts are adjusted annually for inflation. The following example shows a credit computation for ethanol fuel with a baseline credit value of $1.00 per gallon.

The Seller

The seller, who had successfully executed several 2025 §45Z transfers, was a Midwestern-based ethanol producer with over 50 years of operating history.

For this transaction, the seller elected to transfer credits from two facilities, each with a slightly different carbon intensity. The seller carved out $30 million from a broader credit portfolio exceeding $100 million, based on an expected per-gallon credit value of $0.10 to $0.20.

The Buyers

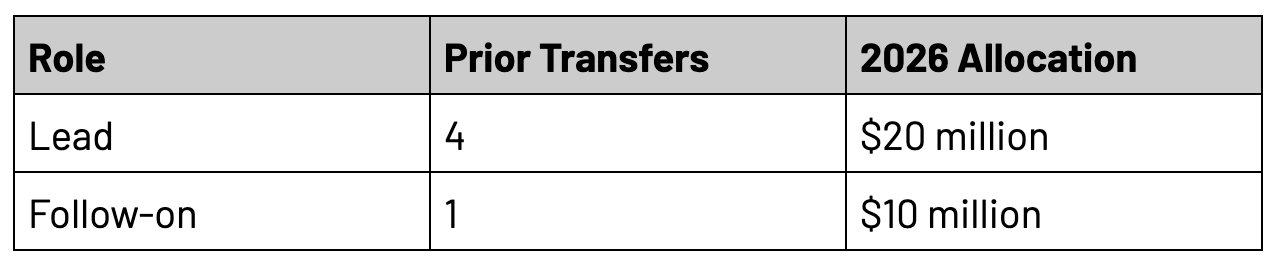

Two publicly traded community banks — a “lead” bank and a “follow-on” bank – partnered on the buy side of the deal:

Despite five successful deals between them, neither buyer had transactional experience with §45Z PTCs, which require a specialized set of third-party deliverables to properly diligence. To close this knowledge gap, the buyers elected to work with an accounting firm for additional due diligence support.

The “Club” Structure

Running two independent, even if parallel, transactions would have translated into an overarching process that added undue complexity and cost for everyone.

Reunion worked with the parties to devise a more efficient approach – a “club” deal. At its core, the structure brought both buyers to the table with the same legal counsel and accounting firm for diligence.

One Negotiation

With Reunion’s guidance, the lead bank set the key commercial terms for the transaction, including payment terms. Rather than a lump-sum payment, Reunion structured the deal as quarterly fundings across 2026 and into 2027.

The seller is scheduled to receive cash as production occurs and qualifying credits are generated. The buyers, likewise, will realize the credit value on a rolling basis.

One Timeline

The deal closed in Q1 2026 — a timeline that mattered. Both banks were motivated to close before quarter-end to recognize the credit benefit in their Q1 financials.

One Due Diligence Package

As the transaction facilitator, Reunion collaborated closely with all parties – including outside legal and diligence partners – to produce a diligence package that gave the buyers the confidence to move forward. The seller, for their part, was delighted to face a single set of questions and documentation requests.

One Tax Credit Insurance Policy

The buyers and seller agreed to a tax credit insurance policy with a limit of liability of at least 125% of the transaction volume. Unlike recapture insurance on ITC deals, tax credit insurance on a §45Z transfer is designed to protect against IRS disallowance of the credit itself – e.g., a determination that the credits were not validly generated.

Two Purchase Agreements

Reunion drafted individualized purchase agreements for each buyer, although the contents and scope were effectively the same.

The Diligence

As noted above, §45Z PTCs require a few specialized third-party deliverables that “typical” §45 wind or solar PTCs do not. That specialization is by design: because the §45Z credit amount is tied to a facility-specific emissions calculation, every element of that calculation must be verified, documented, and defensible.

- Emissions Rate: The producer's emissions rate consultant ran facility-level production data through the Department of Energy’s 45ZCF-GREET model, producing verified emissions rates for each production facility. The model rigorously incorporates elements like feedstock origin, transport logistics, and energy inputs.

- Qualifying Sales: Credits are only generated on sales to unrelated third parties for use as transportation fuel. The seller’s 2026 qualifying sales are expected to go to a range of major fuel distributors and petroleum companies. Each contract will require a review to confirm buyer identity, qualifying use, and volume traceability. Under prevailing guidance, there was an open question about whether sales to resellers and intermediaries qualified — a question the February 2026 proposed regulations resolved in the taxpayers' favor.

- Feedstock: All feedstock was confirmed as 100% domestically sourced corn — millions of bushels throughout the tax year — with agricultural purchase contracts reviewed as part of the diligence package. The proposed regulations confirmed that, for fuel produced after December 31, 2025, feedstock must be exclusively from the U.S., Mexico, or Canada.

- PWA: Because both facilities were placed in service before January 2025, Prevailing Wage and Apprenticeship (PWA) requirements applied only to ongoing alterations and maintenance — not original construction. The producer's compliance reviews and certified payroll reporting were reviewed and confirmed by the buyers' diligence partner.

- FEOC: With respect to Foreign Entity of Concern (FEOC) rules, the seller’s tax consultant confirmed the seller was not a Specified Foreign Entity (SFE).

The Takeaways

All Transacting Parties Experienced Efficiency Gains

Although the “club” formed on the buy side of the deal, all transacting parties experienced efficiency gains. The seller, as we mentioned, faced a single set of due diligence questions and requirements, while the buyers worked with the same legal and diligence partners.

Club Deals are Applicable to Other Credit and Counterparty Types

Although Reunion’s inaugural club deal involved §45Z PTCs, the key unifying features — negotiations, timing, due diligence, legal, form(s) of credit support — can be readily aligned across other credits and counterparties. Reunion is currently structuring club deals for §48 ITCs, §45U PTCs, and §45X PTCs.

“Lead” Buyers Welcome “Follow-On” Buyers and Vice Versa

When we initially proposed a club deal, we were pleasantly surprised by how receptive the prospective lead bank was to bringing a second bank into the transaction. In hindsight, it was a non-issue.

We attribute that openness to an under-appreciated feature of the tax credit market: tax, treasury, and finance leaders tend to be highly collaborative and inclined to share their expertise. As we see almost daily, it’s a relatively small community — one that consistently shows a willingness to support peers in meaningful ways.

Caroline Nevada

April 15, 2026

Prevailing Wage & Apprenticeship: Compliance Lessons From the Field

Seasoned practitioners share what they are seeing across real-world projects, from misclassification traps and payroll gaps to good faith effort documentation and the downstream impact on tax credit transactions.

For Sellers

The Inflation Reduction Act introduced a five-times multiplier on some renewable energy tax credits that is contingent on full compliance with Prevailing Wage and Apprenticeship (PWA) requirements. As projects have become eligible for this multiplier over the past few years, the industry has developed practical applications to meet the complex requirements and has encountered real-world examples of how risks can arise.

We brought together a panel of seasoned practitioners from Orrick and DLA Piper to discuss what they're actually seeing firsthand: the recurring pitfalls, costly surprises, and practical strategies that separate compliant projects from ones that end up in remediation. This post gives a quick refresh of PWA requirements, then provides key commentary from our April 7th webinar.

The Basics

We’ll start with a recap of PWA requirements.

Prevailing Wage Requirements: All laborers and mechanics performing construction, alteration, or repair work on a qualifying project must be paid at least the county-specific minimum wage rate, encompassing both base pay and fringe benefits, for their classification where work is performed. These rates are published and publicly available on SAM.gov and locked in when the work is contracted (assuming an EPC contract with a definitive end date).

Apprenticeship Requirements: There are three requirements related to apprenticeship that taxpayers must follow:

- The labor hours requirement states that at least 15% of total construction labor hours for the project must be performed by registered apprentices for projects beginning construction in 2024 or later (earlier projects are allowed to be compliant at lower percentages).

- The ratio requirement states that projects must also maintain the daily apprentice-to-journeyworker ratio established by the relevant registered apprenticeship program throughout the construction period.

- The participation requirement states that each contractor and subcontractor that employs four or more workers must either hire an apprentice at some point during the project or meet the good-faith effort exception requirements.

Where Projects Most Commonly Fall Short

1. Apprenticeship Requirements Shortfalls

The apprenticeship requirements are complex and cause the most issues in tax credit transactions. Contractors often struggle to source enough qualified apprentices to meet the labor hours and participation requirements. Then they still need to ensure the right ratios are maintained daily and document it all rigorously.

"At first glance, some of these non-compliance issues are not as cut and dry as they might look. If you have a required ratio of one apprentice to two journey workers and on a given day you only achieved one to one — it's not as simple as everything being non-compliant. If that apprentice was paid above journey worker wages, we can classify them as a journey worker instead and exclude their labor hours from the apprentice portion of the apprentice labor hours calculation." — Alex Melehy, Head of Product and Engineering, Reunion

Penalty payments exist as a remediation path for each of the apprenticeship requirements, but they can stack up. For example, if enough contractors on a project do not hire apprentices, then they may trigger penalties for the participation requirement and labor hours requirement. Additionally, if the ratio requirement is not met on a given day, then the labor hours of the apprentice who was under-supervised will not be included in the labor hours requirement calculation, which could lead to issues with the labor hours requirement if enough violations occur. It is recommended that the apprentice-to-journeyworker ratio be tracked in an automated platform so that daily violations are caught quickly and flagged to contractors before the violations lead to large penalties.

2. Worker Misclassification

Worker misclassification also ranks among the most frequent compliance failures — especially once work has begun and the wrong classification has already been selected. It is important to review the Department of Labor wage determinations classifications before starting work and assess which are the most appropriate for the job at hand. Unfortunately, internal job titles like "installer" or "pile driver" may not map neatly onto Department of Labor wage determination classifications. When contractors make assumptions based on title rather than actual duties performed, they can end up underpaying workers for the entirety of a project.

"You have to look holistically at the role and what duties are being performed. Things like 'installer' will really have to be remapped to the Department of Labor's classifications — general labor, skilled labor, power equipment operator. It really matters what exactly they're doing." — Vani Parti, Attorney, DLA Piper

A few specific scenarios come up repeatedly:

Experience may not change the rate. A laborer with 20 years of experience and one with one year of experience may fall under the same wage determination. There is often no tiered structure within a classification, and companies that apply internal pay scales may inadvertently fall out of compliance.

Multi-classification workers require meticulous tracking. When a worker performs duties across more than one classification in a given period, employers must track hours by classification and pay the applicable rate for each. Estimates, averages, and reconstructed records are not acceptable.

Foremen are not automatically exempt. When a foreman performs labor on site, those hours may need to meet the prevailing wage requirements if the foreman spends 20% of the week doing the work of a laborer or mechanic.

When misclassification is discovered late in construction, at the transaction stage, or beyond, the financial exposure compounds quickly as interest accrues and penalties stack. Remediation can require reviewing records from the very beginning of a project and involve contractors and subcontractors who have not been on-site for months.

3. The Payroll Data Gap

Compliance is only as strong as the data behind it. Getting complete, timely payroll data from every contractor and subcontractor on a project is a persistent operational challenge, especially if there are issues with the relationship between the contractors and the developer.

"We had a subcontractor get into a dispute with the developer. The subcontractor then refused to provide some of the data needed to pay the workers. The developer was still obligated to demonstrate PWA compliance for every hour those workers were on site. They had to pull certified payroll reports, reconstruct any misclassifications discovered at that point, work with the general contractor to validate the data, and then somehow find a way to pay these workers... it was a big undertaking."— Vani Parti, Attorney, DLA Piper

The path forward in situations like this requires pulling certified payroll reports, working with the general contractor to validate data, and, in some cases, invoking state "unclaimed property" laws to make correction payments to workers who could not be located. The best way to prepare for this scenario is to appropriately structure the risks and responsibilities in the contracts between the taxpayer and the contractors. EPC agreements, O&M agreements, and supply agreements should all include provisions that enforce cooperation for PWA.

"It's very important to make sure there's timely sharing of information because it can get very difficult. You have to have provisions in there — not only that the contractor is going to comply with prevailing wage and apprenticeship requirements, but provisions on maintaining records, sharing records, and making sure those records can be shared in a format that the PWA advisor can use in their system." — Mark Christy, Partner, Orrick

Additionally, contracts generally include indemnity provisions that are structured to allow parties to act on a PWA advisor's reasonable findings in real time — rather than waiting for a final IRS determination, at which point a transaction is often already under strain.

4. The Good Faith Effort Exception: A Safety Net With Fine Print

When apprentices are genuinely unavailable, the final Treasury regulations provide a good-faith effort exception. A taxpayer or contractor who has made a documented request to a registered apprenticeship program is exempt from compliance requirements for a given work period if one of the following conditions is true: they received either no response from the apprenticeship program within five business days, or the program confirmed that the program cannot fulfill the request, or fewer apprentices were provided than requested.

In practice, the exception is frequently mishandled.

"The biggest thing I would tell folks is follow exactly what the IRS says needs to be in those requests."— Alex Melehy, Head of Product and Engineering, Reunion

A compliant request must include, among other items, the number of apprentices being requested, the number of labor hours, the relevant trade, and the start and end dates of the work period. There is also a requirement to state that the request is made with an intent to employ apprentices in the occupation in which they are trained, in accordance with the requirements of the registered apprentice program, and consistent with the hours and dates included in the request. Requests that omit any of these elements do not qualify.

Timing is equally critical. Requests must be submitted no later than 45 days before apprentices are needed, and the exception itself expires after 365 days. For example, a good-faith effort exception covering a 16-month project period only protects the first 12 months — a new request must be submitted in order to include the requested labor hours of the last four months in the labor hours requirement calculation.

Additional pitfalls include directing requests to programs outside the geographic area of the project, declining a partial fulfillment and attempting to claim the full exception, and failing to confirm that a non-response is genuinely a non-response.

"We've had taxpayers who submitted by email, and the [apprentice] program responded — but it went to their spam folder. They took a good faith effort exception where one wasn't available."— Vani Parti, Attorney, DLA Piper

The operational standard here is straightforward: use a reliable template, track every request and response, set renewal reminders, and maintain all correspondence in a centralized location.

5. Navigating Transactions With an Imperfect PWA Report

On larger projects, a fully clean PWA report is the exception rather than the rule. A clear-eyed remediation plan, established early, is what allows transactions to move forward.

"Usually, I do see PWA reports that are often not clean. The parties are going to have to figure out what to do, and it's good to be able to quantify what the issue is and have a plan."— Mark Christy, Partner, Orrick

For prevailing wage shortfalls, correction payments flow to affected workers, plus interest at the federal short-term rate plus six percentage points. Penalty payments for both prevailing wage and apprenticeship requirement failures should be filed with the taxpayer's tax return. The IRS this year released Form 7220, which requires taxpayers claiming increased credit amounts to calculate and report PWA penalties at the facility level, with a tax return preparer signing off on the filing.

Under the statute, taxpayers have 180 days following a final IRS determination to make correction and penalty payments. This window exists as a post-audit remedy, but should not be relied on as a mechanism for managing known compliance gaps during a transaction. Tax credit buyers and tax equity investors will require documented evidence that all correction and penalty payments have been made before a transaction can proceed.

Looking Ahead

The regulatory landscape for PWA continues to evolve. The final Treasury regulations (published in mid-2024) are comprehensive, but gray areas remain, particularly around newer credit structures like Section 48E and 45Y, where PWA compliance is tracked by inverter block per the definition of a qualified facility for those tax credits.

The practitioners on this webinar consistently reiterated the value of getting ahead of these common pitfalls by focusing on PWA from day one. Managing risk, both for contractors, sub-contractors, and taxpayers, requires visibility into the data and early feedback if mistakes occurred and need to be corrected. Setting up this infrastructure will lead to smoother transactions and better relationships.

For more information about PWA and compliance, contact us here.

Denis Cook

March 5, 2026

Six Tax Credit Takeaways from Analyzing 6,000 Public Company Filings

A data-driven look at how companies are participating in the transferable tax credit market

For Buyers

For Sellers

Section 6418 of the Internal Revenue Code — effective for tax years beginning after December 31, 2022 — created something that did not previously exist in the U.S. tax code: a market for companies to purchase clean energy tax credits.

While the market has grown quickly, it has historically been difficult to get a clear picture of what companies are making tax credit purchases. This is now changing with the introduction of ASU 2023-09, a new accounting standard which requires more granular tax disclosures, making credit purchases easier to detect. ASU 2023-09 took effect for fiscal years beginning after December 15, 2024 (for public companies), which will drive greater visibility into market trends.

To date, Reunion has analyzed over 6,000 public filings submitted since January 2025, including 10-Ks and 10-Qs, across 1,400 of the largest companies listed in the US. Our AI-assisted process examines filings for tax credit purchase disclosures; all identified purchasing activity is then human-verified.

This analysis should be viewed as an early snapshot rather than a final dataset. Public companies are filing new 10-K and 10-Q reports virtually every day, and additional tax credit disclosures continue to emerge as reporting cycles progress. Our current methodology allows us to systematically scan filings, identify purchase disclosures, and incorporate them into a growing dataset that will continue to expand as more filings are released.

Below are six key takeaways from our filings analysis through March 2, 2026. The Wall Street Journal featured our research in a recent article.

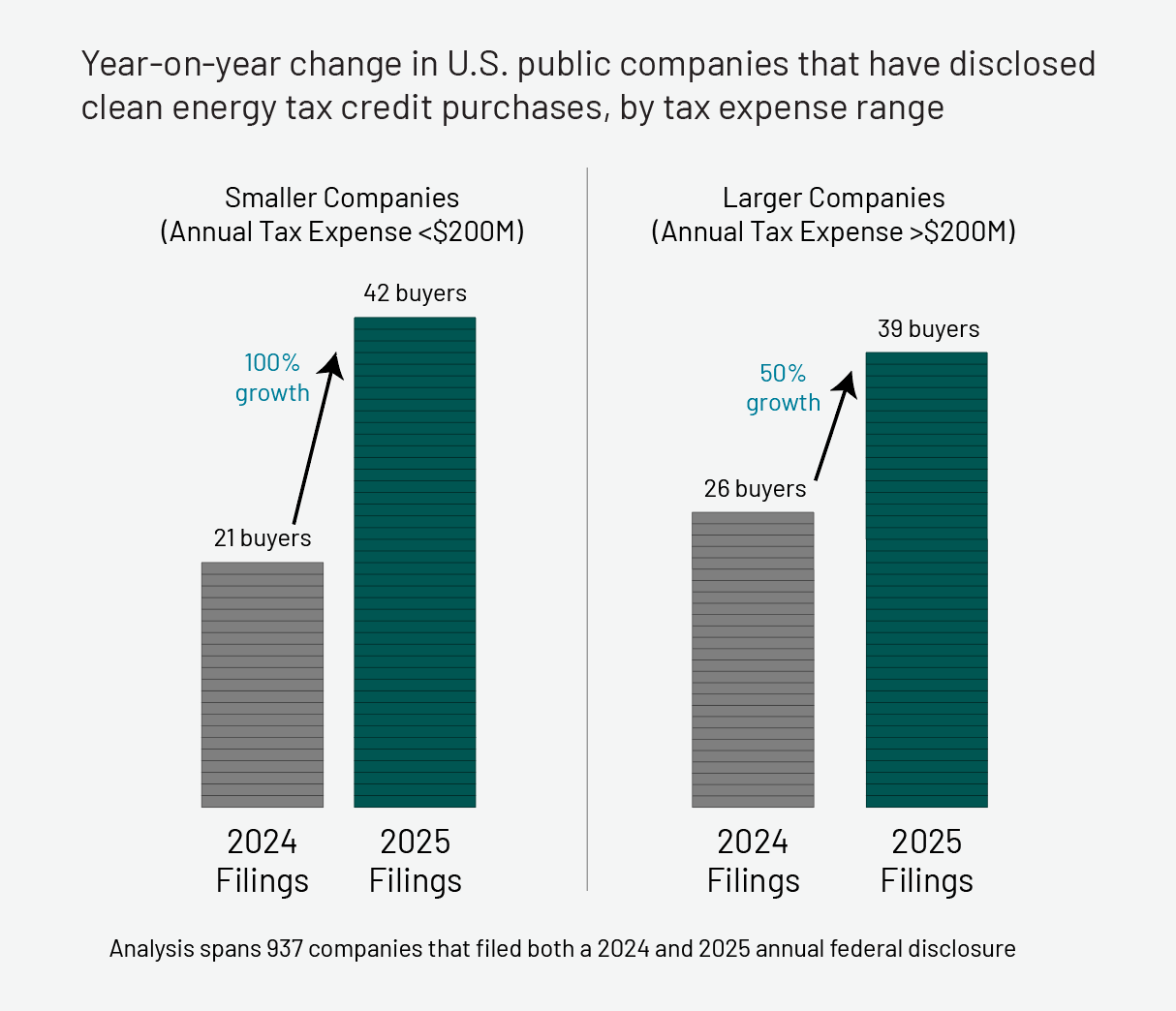

Insight 1: Buyer Participation Has Nearly Doubled — With Smaller Companies Accounting for 62% of Growth

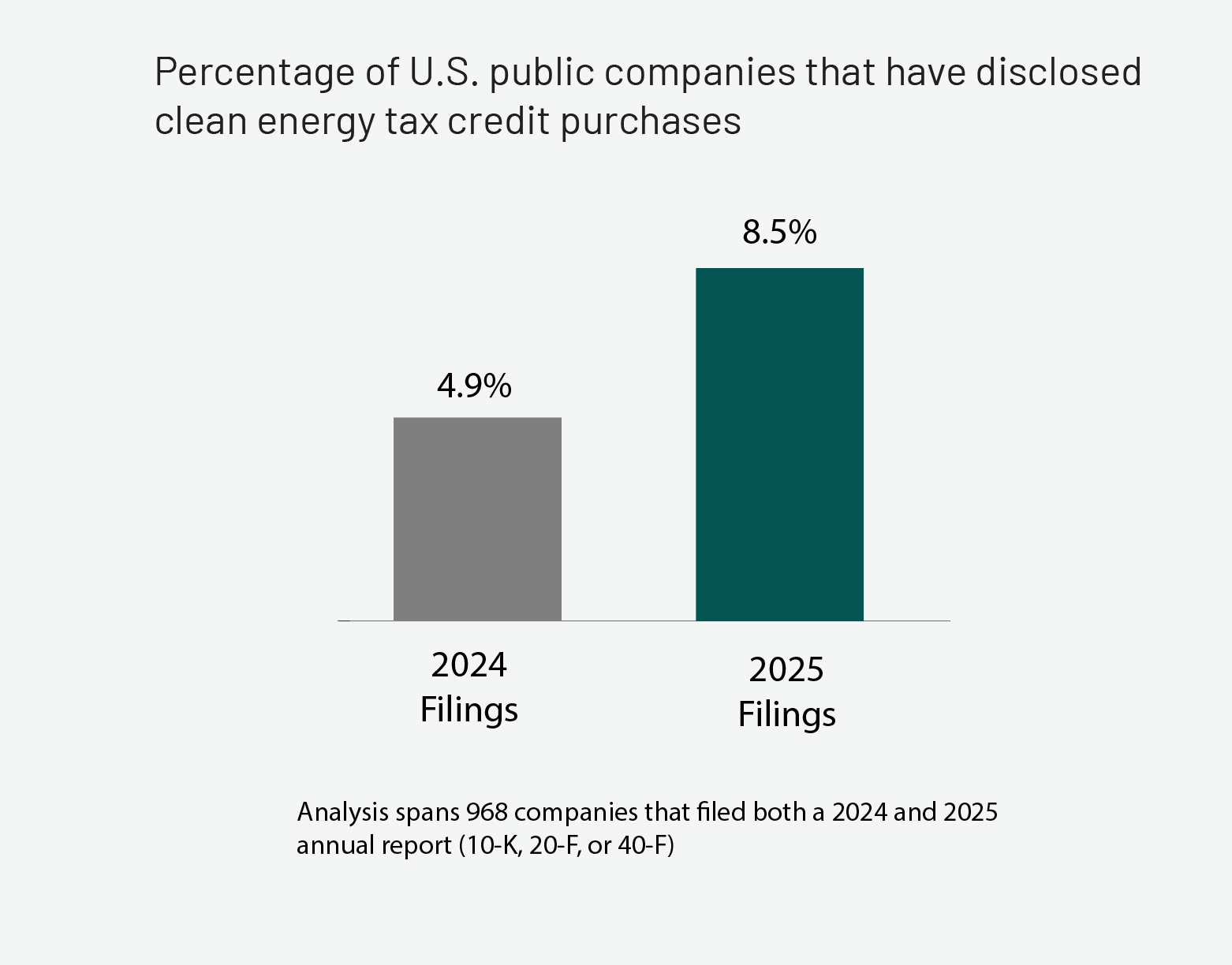

Across the nearly 1,000 public companies in our dataset that filed annual disclosures in both 2024 and 2025, we found that the share of firms disclosing tax credit purchases rose from 4.9% in 2024 to 8.5% in 2025.

The growth is even more pronounced among smaller taxpayers. Companies with under $200M in annual tax expense doubled their purchase rate year-over-year, from 21 buyers to 42 buyers in the matched sample. Purchasing among larger taxpayers also grew, albeit at a 50% rate – from 26 to 39 buyers.

Participation is broadening thanks to more standardized deal structures, increases in credit supply, and clarified IRS guidance. What began as a large-cap strategy is increasingly common among more modest taxpayers. We expect further convergence of tax credit purchase rates among company size cohorts as the market matures.

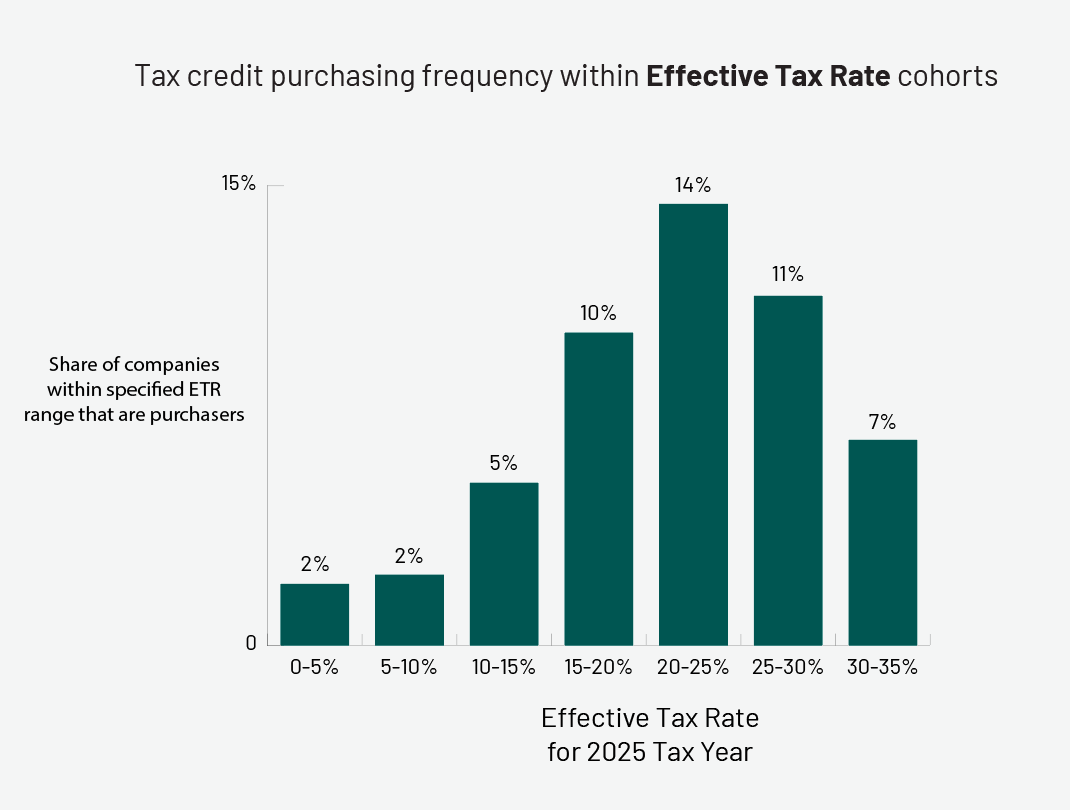

Insight 2: Tax credit purchase rates are highest for corporate taxpayers with ETRs in the 15% to 30% range

Our analysis of filings for the 2025 tax year suggests that over 10% of companies with ETRs in the 15% to 30% range purchased tax credits.

Purchase rates among companies with ETR’s of 20-25% are roughly 7 times higher than for companies with ETR’s below 10%.

Insight 3: Reductions in Effective Tax Rate Have Clustered Between 0.4% and 2.0%

Many companies purchase transferable tax credits with the express goal of “managing” their effective tax rate (ETR). Others focus on cash tax savings, although this, too, has an impact on ETR.

The chart below shows that nearly 80% of companies that purchased transferable tax credits in 2025 lowered their ETR between 0.4 and 2.0 percentage points – for example, from 23.2% to 21.2% for a 2.0% reduction.

Our analysis identified outliers at both ends of the distribution (see Methodology Note). Multiple companies reported effective tax rate reductions in excess of 5.0%.

Insight 4: Tax Expense Is the Strongest Predictor of Purchasing

Our analysis shows that purchase rates increase steadily as annual tax liability rises — then drops at the very highest levels.

Why the drop above $1 billion in annual tax expense? Very large corporations often have more alternatives when it comes to tax reduction strategies, such as complex deductions and cross-border tax planning. Deployment of these alternate strategies may translate into a dampened interest in buying transferable credits.

At the same time, we also know from our work in the tax credit market that many extremely large buyers do not acquire tax credits at a level that crosses the reporting thresholds prescribed in ASU 2023-09. If we were to layer these companies into our analysis - perhaps in a future report – we would expect a less dramatic drop.

We tested other size proxies, including revenue, employee count, and market capitalization. All are positively correlated with purchasing, but are also highly correlated with each other. Among all such size proxies, tax expense shows the strongest relationship with purchase behavior.

Insight 5: Tax Credit Purchasing Has Gained Traction Nationwide — with a Notable Outlier

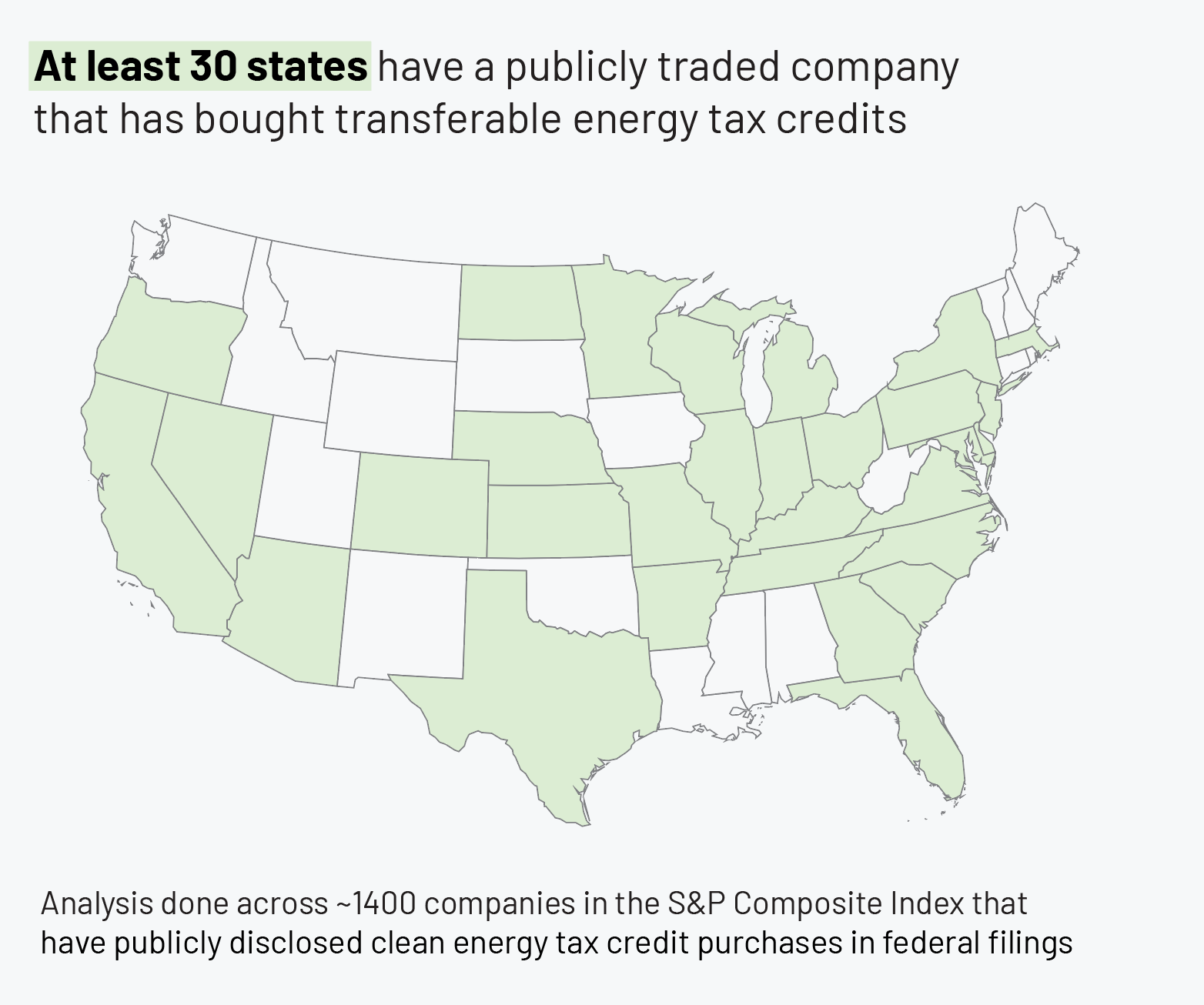

The market is attracting companies from all regions. More than 30 states are home to at least one public company that has disclosed transferable tax credit purchases.

It’s also worth noting that the actual number of states associated with corporate tax credit purchasing is greater than shown in the map above. For example, Reunion has worked with tax credit buyers in a number of the non-highlighted states including Idaho and Washington, but these buyers do not register in our analysis of federal filings because the buyers were either private companies or public companies that have yet to make tax credit disclosures in federal filings.

One state stood out in our geographic analysis – for its surprisingly weak buying activity.

California-headquartered companies purchase at less than half the national rate (3.4% vs. 8.5%). This gap persists across tax expense bands and across sectors.

A contributing factor may include that California’s technology companies already have robust tax reduction channels through their R&D spending and capital expenditures. One other observation is that prior to SB 302 (a California law effective January 2026), the state did not conform to IRC §6418 for tax purposes. Therefore, the discount on a purchased credit (e.g., buying a $100M credit for $90M) was potentially subject to state-level taxes for tax years before January 1, 2026.

Insight 6: Retail and Construction Stand Out

Purchase rates show meaningful variation across industries, with construction and retail leading the charge.

Factors leading construction companies toward greater tax credit purchases include predictable federal tax liabilities, and limited availability of tax strategies such as R&D credits and international structuring opportunities. Retail faces similar structural characteristics — often more acutely. Retail R&D intensity is minimal relative to technology or pharma, and retailers face large and recurring domestic tax expenses.

For many companies in these industries, transferable credits are the first meaningful new federal tax reduction tool in decades.

In Summary

Our analysis suggests that the transferable tax credit market continues to evolve in several important ways. Activity is increasing overall, participation is extending beyond the largest revenue companies, and geographic concentration is gradually dispersing. We are also observing particularly strong engagement in industries that historically have had limited access to tax credit opportunities.

Recent disclosure changes are making transaction activity more transparent, while market infrastructure continues to mature. As a result, buyer participation patterns are becoming easier to identify and evaluate.

This represents an early snapshot rather than a definitive assessment. As additional 2025 and 2026 filings become available, we will continue to monitor and analyze how the buyer market develops.

Exclusive access to underlying SEC data provided to existing buy-side and sell-side clients of Reunion. Reach out to your Reunion contact for access.

This research was featured in the Wall Street Journal. Read the article here.

Data Notes

Date of analysis: February - March 2026

Universe: ~1,400 of the largest public companies listed in the US

Filings reviewed: 10-K, 10-Q, 20-F, 40-F filed since January 1, 2025

Methodology Notes:

- Many filings reference “transferable tax credits” without specifying credit type. Since transferability is generally tied to Section 6418, we classify them as clean energy credits.

- Of the ~1,400 companies analyzed, roughly 1,000 had filed both a 2024 and a 2025 report during the period we examined. The remainder fall into two categories: companies that have not yet filed their 2025 annual report, and fiscal-year filers whose 2024 filings were published before our data collection began in January 2025. As a result, the year-over-year comparisons are based on the subset of companies for which both filings are available, ensuring an apples-to-apples comparison.

- In our assessment of effective tax rate reductions, we identified one outlier company that experienced an increase in its ETR as a result of the non-recurring accounting treatment associated with an investment tax credit (ITC) recapture event. We omitted this data point in our reported results, but intend to examine this recapture in greater detail in a forthcoming note.

Denis Cook

March 5, 2026

Which Sectors and Industries Purchase Transferable Tax Credits Most Often?

The final of a series of data-driven posts exploring how companies are participating in the transferable tax credit market.

For Buyers

For Sellers

Consumer cyclical companies – including construction companies and retailers – purchase transferable tax credits at the highest rate of any sector: 16 percent, or roughly five times the rate of technology companies.

Reunion analyzed over 6,000 public filings across approximately 1,400 of the largest U.S. public companies to determine which industries are most actively purchasing transferable clean energy tax credits under IRC Section 6418. ASU 2023-09, a new accounting standard in effect for fiscal years beginning after December 15, 2024, requires more granular tax disclosures by public companies and makes credit purchases easier to verify.

How Do Tax Credit Purchase Rates Vary by Sector?

The following table shows the share of companies in each GICS sector that have been verified as purchasers of transferable tax credits, based on SEC filings since January 2025.

Source: Reunion analysis of SEC filings (10-K, 10-Q, 20-F, 40-F) filed since January 1, 2025. Sectors based on Yahoo Finance GICS classification.

Consumer Cyclical Leads at 16%

The Consumer Cyclical sector – which includes retail, construction, restaurants, and lodging -- has the highest purchase rate at 16%. Within this sector, residential construction companies purchase at 33%, specialty retailers at 24%, and restaurants at 18%.

Factors leading construction companies toward greater tax credit purchases include predictable federal tax liabilities, and limited availability of tax strategies such as R&D credits and international structuring opportunities. Retail faces similar structural characteristics – often more acutely. Retail R&D intensity is minimal relative to technology or pharma, and retailers face large and recurring domestic tax expenses.

For many companies in these industries, transferable credits are the first meaningful new federal tax reduction tool in decades.

Financial Services Is the Second-Largest Buyer Sector

Financial services companies purchase at 12%, driven by banks, insurers, and asset managers. Many of these institutions have prior experience with tax-equity investing, making transferable credits a natural adjacent strategy. Regional banks are also active, purchasing at 13%.

Technology Purchases at Just 3%

Despite housing some of the largest taxpayers in the S&P Composite, the technology sector purchases at just 3% – roughly one-fifth the rate of Consumer Cyclical. Large technology companies typically already leverage substantial R&D credits, stock-based compensation deductions, and international tax planning structures that reduce their effective tax rates well below the statutory federal rate.

SIC Industry Classification Tells a Similar Story

Grouping by SIC division rather than GICS sector produces a similar picture:

Key Takeaway

The strongest predictor of tax credit purchasing is not company size or profitability – but rather the combination of a meaningful federal tax liability and limited access to alternative tax reduction strategies. Sectors where these two conditions converge (e.g. consumer cyclical, financial services, industrials) show purchase rates significantly higher than sectors where companies already have robust tax optimization tools.

For the first post in this series that explores the tax credit purchaser landscape by analyzing data from publicly available filings, click here.

Reunion maintains a database of public companies that have disclosed transferable tax credit purchases, available to entities buying or selling credits, and provides exclusive access to the underlying SEC data to existing buy-side and sell-side clients of Reunion. Reach out to your Reunion contact for access.

Data Notes

Analysis Period: February-March 2026

Universe: ~1,400 largest U.S. public companies

Filings Reviewed: 10-K, 10-Q, 20-F, 40-F filed since January 1, 2025

Sectors: Based on Yahoo Finance GICS classification

Methodology:

- Credit Classification: Many filings reference transferable credits without specifying type. These are classified as clean energy credits since transferability is generally tied to Section 6418.

- Sample Composition: Of approximately 1,400 companies, roughly 1,000 had filed both 2024 and 2025 reports during the analysis window. The remainder had not yet filed 2025 reports or had 2024 filings published before data collection began.

- Data Quality: An AI-assisted process was used to scan filings. All identified purchasing activity was then human-verified at the company level.

Denis Cook

March 5, 2026

Where Are Companies Buying Transferable Tax Credits? A State-by-State Look

The fourth of five data-driven posts exploring how companies are participating in the transferable tax credit market.

For Buyers

For Sellers

More than 30 states are home to at least one public company that has disclosed purchasing transferable tax credits under IRC Section 6418. But not all states are participating equally.

Reunion analyzed over 6,000 public filings across approximately 1,400 of the largest U.S. public companies to map where buyers are located. ASU 2023-09, a new accounting standard in effect for fiscal years beginning after December 15, 2024, requires more granular tax disclosures by public companies and makes credit purchases easier to verify.

The data shows broad geographic adoption – with one notable exception.

Which States Have Transferable Tax Credit Buyers?

Among the companies we analyzed, these five states housed the headquarters for the most number of companies that publicly disclosed tax credit purchases.

The following map shows which states have at least one verified public company purchaser.

It’s also worth noting that the actual number of states associated with corporate tax credit purchasing is greater than shown in the map above. Reunion has worked with tax credit buyers in a number of the non-highlighted states, such as Idaho and Washington, but these buyers do not register in our analysis of federal filings because the buyers were either private companies or public companies that have yet to make tax credit disclosures in federal filings.

Low Purchase Rate for California Companies

California is home to over 175 of the largest U.S. public companies – more than any other state. It is a leader in installed solar capacity and clean energy investment. Yet California-headquartered companies purchase transferable tax credits at less than half the national rate.

This gap persists across tax expense bands, sectors, and company sizes.

A contributing factor may include that California’s large technology companies already have robust tax reduction channels through their R&D spending and capital expenditures. One other observation is that prior to SB 302 (a California law effective January 2026), the state did not conform to IRC §6418 for tax purposes. Therefore, the discount on a purchased credit (e.g., buying a $100M credit for $90M) was potentially subject to state-level taxes for tax years before January 1, 2026.

Key Takeaway

Tax credit purchasing has spread to more than 30 states, demonstrating that this is not a regional phenomenon. While California's low purchase rate could be a regulatory outlier, the Golden State may close the gap with SB 302 now in effect.

For the next post that explores tax credit purchase rates by company sector and industry, click here. For the full series, start here.

Reunion maintains a database of public companies that have disclosed transferable tax credit purchases, available to entities buying or selling credits, and provides exclusive access to the underlying SEC data to existing buy-side and sell-side clients of Reunion. Reach out to your Reunion contact for access.

Data Notes

Analysis Period: February-March 2026

Universe: ~1,400 largest U.S. public companies

Filings Reviewed: 10-K, 10-Q, 20-F, 40-F filed since January 1, 2025

Methodology:

- Credit Classification: Many filings reference transferable credits without specifying type. These are classified as clean energy credits since transferability is generally tied to Section 6418.

- Sample Composition: Of approximately 1,400 companies, roughly 1,000 had filed both 2024 and 2025 reports during the analysis window. The remainder had not yet filed 2025 reports or had 2024 filings published before data collection began.

- Data Quality: An AI-assisted process was used to scan filings. All identified purchasing activity was then human-verified at the company level.

Denis Cook

March 5, 2026

What Impact Did 2025 Tax Credit Purchases Have on Effective Tax Rates?

The third of five data-driven posts exploring how companies are participating in the transferable tax credit market.

For Buyers

For Sellers

Reunion's analysis of public company filings shows that nearly 80% of companies purchasing transferable tax credits in 2025 lowered their effective tax rate (ETR) by between 0.4 and 2.0 percentage points.

We analyzed over 6,000 public filings across approximately 1,400 of the largest U.S. public companies to quantify the impact of tax credit purchases on effective tax rates. ASU 2023-09, a new accounting standard in effect for fiscal years beginning after December 15, 2024, requires more granular tax disclosures by public companies and makes credit purchases easier to verify.

The Typical Reduction: 0.4 to 2.0 Percentage Points

For a company paying a 23% effective rate, a typical credit purchase might bring that down to somewhere between 21% and 22.6%. In cash terms, a company with $1B in pre-tax income can save $10M in cash when reducing its ETR by 1 percentage point – which it can do by purchasing tax credits at a discount to face value.

This range reflects the economics of how most companies size their credit purchases: large enough to generate meaningful tax savings, but not so large as to create concentration risk with a single credit type or project.

What Is the Upper End of the ETR Reduction Range?

A smaller group of companies reported ETR reductions exceeding 5.0 percentage points – companies that made particularly large credit purchases relative to their overall tax liability. These are often mid-size companies where a single credit transaction represents a material share of total tax expense.

Key Takeaway

The 0.4–2.0 percentage point range provides a useful benchmark for companies evaluating their transferable tax credit purchase strategy. The clustering of reductions in this range suggests that the buyers have largely converged on sizing transactions to produce meaningful yet manageable impacts on their tax positions – neither making token purchases nor going all-in.

Transferable tax credit purchases are producing real, measurable reductions in effective tax rates for the companies that buy them. For companies with significant federal tax liabilities and effective rates near the statutory rate, this represents a new and accessible lever for tax optimization.

For the next post that explores the geographic incidence and spread of tax credit purchase rates, click here. For the full series, start here.

Reunion maintains a database of public companies that have disclosed transferable tax credit purchases, available to entities buying or selling credits, and provides exclusive access to the underlying SEC data to existing buy-side and sell-side clients of Reunion. Reach out to your Reunion contact for access.

Data Notes

Analysis Period: February-March 2026

Universe: ~1,400 largest U.S. public companies

Filings Reviewed: 10-K, 10-Q, 20-F, 40-F filed since January 1, 2025

Methodology:

- Credit Classification: Many filings reference transferable credits without specifying type. These are classified as clean energy credits since transferability is generally tied to Section 6418.

- Sample Composition: Of approximately 1,400 companies, roughly 1,000 had filed both 2024 and 2025 reports during the analysis window. The remainder had not yet filed 2025 reports or had 2024 filings published before data collection began.

- Data Quality: An AI-assisted process was used to scan filings. All identified purchasing activity was then human-verified at the company level.

Denis Cook

March 5, 2026

Tax Credit Purchase Rates by Company Size: Analysis of 1,400 Public Companies

The second of five data-driven posts exploring how companies are participating in the transferable tax credit market.

For Buyers

For Sellers

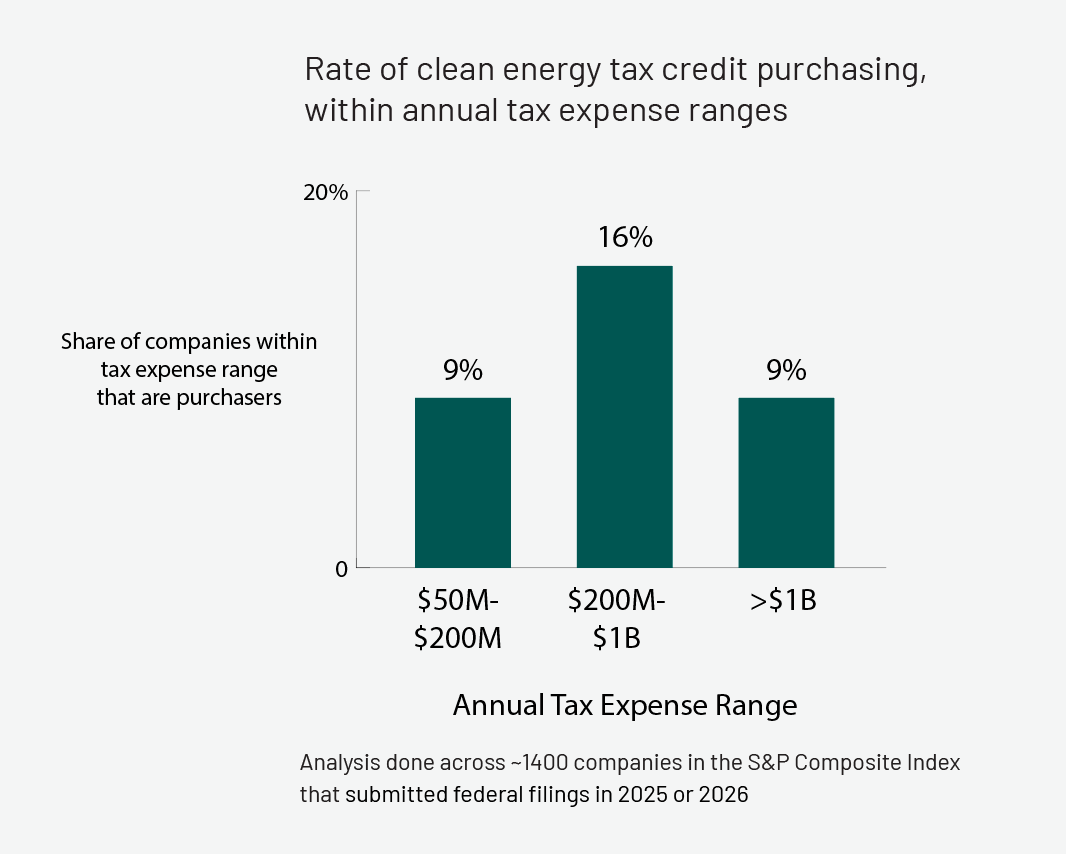

A common question in the transferable tax credit market is whether it is dominated by the largest corporations, or whether mid-size companies are meaningfully participating. SEC filings give the answer: mid-sized public companies, in the $50M-$1B annual tax expense range, showed the highest purchase rates.

Reunion analyzed over 6,000 public filings across approximately 1,400 of the largest U.S. public companies to quantify buyer participation. ASU 2023-09, a new accounting standard in effect for fiscal years beginning after December 15, 2024, requires more granular tax disclosures by public companies and makes credit purchases easier to verify.

Which Financial Metric Is the Best Proxy for Tax Credit Purchasing?

Among the size metrics we tested – revenue, market capitalization, employee count, and tax expense – annual tax expense showed the strongest correlation with purchasing behavior. This makes intuitive sense: tax expense directly measures the liability that transferable credits offset.

Companies in the $50M-$1B annual tax expense range showed the highest purchase rates, while those with lower tax expenses participated less frequently. The decline above $1B likely reflects that very large corporations often have alternative tax reduction strategies, including complex deductions and cross-border planning. It may also reflect that purchases for some large buyers do not cross ASU 2023-09 reporting thresholds.

However, growth in purchasers is fastest among smaller companies. Companies with under $200M in annual tax expense doubled their purchase rate year-over-year (from 21 buyers to 42 buyers, in the ~1,000 for whom Reunion analyzed both 2024 and 2025 annual filings). Purchasing among larger taxpayers also grew, albeit at a 50% rate – from 26 to 39 buyers.

Do Companies with Higher Effective Tax Rates Buy More Credits?

When we examine purchasing by effective tax rate rather than absolute tax expense, a parallel pattern emerges:

The highest purchase rate (14%) occurs among companies whose effective tax rate (ETR) is in the 20-25% range. The purchase rate stays elevated on both sides of the range as well, with over 1 in 10 companies with ETR’s of 15%-30% purchasing tax credits. Companies already benefiting from low effective rates (under 10%) have weaker incentive to purchase credits.

Key Takeaway

The transferable tax credit market is not just a large-company phenomenon. It is showing broad adoption among companies with tax expenses above $50M annually, with the fastest growth in adoption happening among companies with <$200M in annual tax expenses. This profile describes hundreds of public companies, and many private ones as well.

For the next post that explores the impact of tax credit purchases on company effective tax rates, click here. For the full series, start here.

Reunion maintains a database of public companies that have disclosed transferable tax credit purchases, available to entities buying or selling credits, and provides exclusive access to the underlying SEC data to existing buy-side and sell-side clients of Reunion. Reach out to your Reunion contact for access.

Data Notes

Analysis Period: February-March 2026

Universe: ~1,400 largest U.S. public companies

Filings Reviewed: 10-K, 10-Q, 20-F, 40-F filed since January 1, 2025

Methodology:

- Credit Classification: Many filings reference transferable credits without specifying type. These are classified as clean energy credits since transferability is generally tied to Section 6418.

- Sample Composition: Of approximately 1,400 companies, roughly 1,000 had filed both 2024 and 2025 reports during the analysis window. The remainder had not yet filed 2025 reports or had 2024 filings published before data collection began.

- Data Quality: An AI-assisted process was used to scan filings. All identified purchasing activity was then human-verified at the company level.

Denis Cook

March 5, 2026

How Big Is the Transferable Tax Credit Buyer Market, and How Fast Is It Growing?

The first of five data-driven posts exploring how companies are participating in the transferable tax credit market.

For Buyers

For Sellers

Section 6418 of the Inflation Reduction Act created a new market for companies to purchase clean energy tax credits – a mechanism that previously didn't exist in U.S. tax code. Two years in, we took a look at the buyer universe to understand its size and composition.

How Many Companies Have Publicly Disclosed Transferable Tax Credit Purchases?

As of early March 2026, 119 public companies – approximately 8.4% of the ~1,400 largest U.S. public companies – have disclosed purchasing transferable tax credits in SEC filings.

Reunion analyzed over 6,000 public filings across approximately 1,400 of the largest U.S. public companies to quantify buyer participation. ASU 2023-09, a new accounting standard in effect for fiscal years beginning after December 15, 2024, requires more granular tax disclosures by public companies and makes credit purchases easier to verify.

The above count reflects human-verified disclosures in 10-K, 10-Q, 20-F, and 40-F filings filed since January 1, 2025. The 119 verified purchasers span 30+ states and 11 industry sectors. They range from Fortune 100 corporations to regional banks.

How Fast Is the Transferable Tax Credit Market Growing?

Across the nearly 1,000 public companies in our dataset that filed annual disclosures in both 2024 and 2025, we found that the share of firms disclosing tax credit purchases rose from 4.9% in 2024 to 8.5% in 2025 – an increase of approximately 74%.

Growth was broad-based across sectors and company sizes, though it was particularly pronounced among smaller taxpayers. Companies with under $200M in annual tax expense doubled their purchase rate. Participation is broadening thanks to more standardized deal structures, increases in credit supply, and clarified IRS guidance.

Why This Matters

The transferability provision of the IRA fundamentally expanded the buyer community beyond the small group of traditional tax-equity investors that historically participated in clean energy finance. Any corporation with federal tax liability can now purchase credits directly, and the filing data shows they are doing so in increasing numbers. The 119 verified purchasers represent only publicly disclosed transactions. The actual buyer count, including private companies and transactions below disclosure thresholds, is almost certainly larger.

For the next post that explores tax credit purchase rates by company size and effective tax rates, click here.

Reunion maintains a database of public companies that have disclosed transferable tax credit purchases, available to entities buying or selling credits, and provides exclusive access to the underlying SEC data to existing buy-side and sell-side clients of Reunion. Reach out to your Reunion contact for access.

Data Notes

Analysis Period: February-March 2026

Universe: ~1,400 largest U.S. public companies

Filings Reviewed: 10-K, 10-Q, 20-F, 40-F filed since January 1, 2025

Methodology:

- Credit Classification: Many filings reference transferable credits without specifying type. These are classified as clean energy credits since transferability is generally tied to Section 6418.

- Sample Composition: Of approximately 1,400 companies, roughly 1,000 had filed both 2024 and 2025 reports during the analysis window. The remainder had not yet filed 2025 reports or had 2024 filings published before data collection began.

- Data Quality: An AI-assisted process was used to scan filings. All identified purchasing activity was then human-verified at the company level.

Connor Danik

February 20, 2026

Section 45Z Proposed Regulations Are Out — What Changed?

On February 3, 2026, the Department of Treasury and the Internal Revenue Service (IRS) issued proposed regulations for the Clean Fuel Production Credit.

For Buyers

For Sellers

On February 3, 2026, the Department of Treasury and the Internal Revenue Service (IRS) issued proposed regulations for the Clean Fuel Production Credit (§45Z). The proposed regulations were published in the Federal Register on February 4, 2026, and are generally consistent with the prior guidance issued.

Noted below are key changes and additions, as well as clarifying or confirmatory guidance that was issued in the proposed regulations.

Jump to a section:

Sold for use in a trade or business

A taxpayer is eligible for the 45Z credit only if it produces transportation fuel and subsequently sells it to an unrelated person (i) for use by such person in the production of a fuel mixture, (ii) for use by such person in a trade or business, or (iii) such person sells such fuel at retail to another person and places such fuel in the fuel tank of such other person. The proposed regulations confirm that the term “sold for use in a trade or business” includes sales of fuel to an intermediary or reseller. The definitions in Section 3.03(7) and the "Appendix - Draft Text of Forthcoming Proposed Regulations" of Notice 2025-10 previously defined the term to mean fuel sold for “use as a fuel” in a trade or business. After stakeholders raised concerns that this language could prevent sales for resale, the proposed regulations removed the “use as a fuel” requirement from the definition of “sold for use in a trade or business.” The proposed regulations also conforms the definition for “sold for use in a trade or business” with the meaning under Internal Revenue Code Section 162.

Safe Harbor Certificates

The proposed regulations introduce two new safe harbors for substantiating the emissions rate for a transportation fuel as well as substantiation for qualified sales. For non-SAF transportation fuel, taxpayers may substantiate an emissions rate determined under the 45ZCF-GREET model by obtaining a certification in substantially the same manner required for sustainable aviation fuel (SAF) under proposed regulation §1.45Z-5. For qualified sales, taxpayers may obtain from the purchaser a certificate in substantially the same form as described in proposed regulation §1.45Z-4(g)(3)(ii). However, a key requirement is the taxpayer must obtain the certificate from the purchaser prior to or at the time of sale (or, for multiple sales, before or at the first covered sale). In addition, the proposed regulations state the Purchaser agrees to provide the person liable for tax with a new certificate if any information in the certificate changes.

Related Party Sales

The proposed regulations adopt a broader related-party “look-through” rule. Under Notice 2025-10, a taxpayer that is a member of a consolidated group is treated as selling fuel to an unrelated person if another member of the group (the related person) ultimately sells the fuel to an unrelated person. Under the broader related-party rules, a taxpayer that is not a member of a consolidated group is also treated as selling fuel to an unrelated person if and when a related person sells the fuel to the unrelated person.

Energy Attribute Certificates & Incrementality

Certain taxpayers may purchase energy attribute certificates (EACs) such as renewable energy certificates (RECs) to reduce their carbon intensity score and resulting emissions rate. The proposed regulations confirm that when incorporating EACs into the 45ZCF-GREET model, rules similar to final regulation §1.45V-4(d) apply. When applying the rules for purposes of the 45ZCF-GREET-Model, the facility is considered placed in service in the first taxable year it produces transportation fuel. The proposed regulations require the EAC-generating facility (or if the EAC facility uses carbon capture and sequestration technology) to have a commercial operations or placed in service date no more than 36 months prior to the first day of the taxable year in which the 45Z facility first produced transportation fuel.

Emissions Rate Table

The proposed regulations clarify that the applicable emissions rate table establishes the emissions rate for a fuel if the emissions rate table includes both the type and category of that fuel. The applicable emissions rate table for a taxpayer is the first publicly available emissions rate table that is in effect during the taxpayer's taxable year of production. However, if an allowed methodology is updated with respect to an included type or category of fuel and is publicly available after the first day of the taxable year of production (but still within such taxable year), then the taxpayer could choose to treat such updated version as the most recent version of such methodology. If an emissions rate table does not initially include a type or category of fuel but an allowed methodology is updated to add such type or category during the calendar year, then that fuel type or category will be considered included in such emissions rate table, and an impacted taxpayer must use this version as its the first publicly available version that includes its type and category of fuel.

Facility Ownership

The proposed regulations confirm the taxpayer is not required to own the qualified facility and credit eligibility is tied to the production of transportation fuel at a qualified facility and subsequent qualified sale.

Timing of Sale

The proposed regulations confirm that production of a transportation fuel may occur in a prior taxable year than the taxable year in which the qualified sale of the fuel occurs, but that a qualified sale may not occur before the date the fuel is produced.

Double Crediting

Code §45Z(d)(5)(A)(iv) states transportation fuel means a fuel which “is not produced from a fuel for which a credit under this section is allowable.” The proposed regulations clarify that the first transportation fuel in the production chain qualifies for the §45Z credit. However, a fuel could still qualify for the §45Z credit if its production process uses a transportation fuel solely as a process fuel or other non-primary-feedstock input.

Feedstock

The proposed regulations confirm that transportation fuel produced after December 31, 2025, must be exclusively derived from a feedstock that was produced or grown in the United States, Mexico, or Canada.

Negative Emissions Rate

Except for transportation fuel in which its primary feedstock is derived from animal manure, the proposed regulations confirm that the emissions rate may not be less than zero for any transportation fuel produced after December 31, 2025.

Indirect Land Use

The proposed regulations confirm that the emissions rate should exclude any emissions attributed to indirect land use change for transportation fuel produced after December 31, 2025.

Production

The proposed regulations clarify that the term production must involve substantial processing by the producer and does not include instances in which a person engages in minimal processing such as creating a fuel mixture or otherwise engaging in activities that do not result in a chemical transformation. For example, this definition of production would exclude any person that removes conventional or alternative natural gas (CANG) from a pipeline, compresses it further after removal, and then sells such further compressed CANG; compression of CANG that is already interchangeable with fossil natural gas would also not meet the proposed definition of production.

Carbon Capture Equipment

The proposed regulations confirm carbon capture equipment will be considered a part of the qualified facility if the equipment contributes to the lifecycle GHG emissions rate of the transportation fuel, which includes emissions from all stages of the fuel’s production and use, including feedstock production and transportation, fuel production and distribution, and use ofthe finished fuel.

Undenatured Ethanol

There was an open question if undenatured ethanol would qualify as transportation fuel as the previous guidance only referenced denatured ethanol. The proposed regulations clarify that undenatured fuel ethanol that meets the qualifications of ASTM D8651 for blending with gasoline and that has an emissions rate that is not greater than 50 kilograms of CO2e per mmBTU meets the definition of non-SAF transportation fuel.

Suitable Use

Code §45Z(d)(5)(A)(i) specifies transportation fuel means a fuel which “is suitable for use as a fuel in a highway vehicle or aircraft.” The proposed regulations clarify that actual use as a fuel in a highway vehicle or aircraft is not required.

Written or electronic comments must be received by April 6, 2026 and a public hearing will be held on May 28, 2026. Taxpayers may rely on the proposed regulations as long as they rely on them in their entirety and in a consistent manner.

Reunion Accelerates Investment Into Clean Energy

Reunion’s team has been at the forefront of clean energy financing for the last twenty years. We help CFOs and corporate tax teams purchase clean energy tax credits through a detailed and comprehensive transaction process.