Frequently asked questions about tax credit transfers

What do transferable tax credits cost? Who pays for insurance and legal fees? Is the tax benefit taxable? This comprehensive FAQ article breaks down the economics, risks, and legislative issues surrounding the growing market for clean energy tax credits.

.png)

Economics

What do transferable tax credits typically cost?

Tax credits generally range in price from $0.90 to $0.96. These prices are “all in,” meaning that the cost of tax credit insurance and any broker or intermediary cost is typically borne by the seller. The seller will also typically reimburse buyers for a capped amount of third party legal and diligence fees.

§48 investment tax credits from large, reputable sellers have historically traded in the $0.93 to $0.95 range. In late 2024 and early 2025, we observed sizable ($75M+) credits from investment-grade sellers for the 2024 tax year trading in the $0.95 range. Factors that impact pricing include:

- Financial strength of seller: Buyers pay a premium when seller has a strong balance sheet or investment-grade credit rating

- Credit type: There is more buyer demand for large utility scale projects versus distributed portfolios. Additionally, advanced manufacturing, solar, wind, storage and nuclear have more demand than renewable natural gas or carbon capture technologies

- Volume of opportunity: Buyers pay a premium for larger opportunities ($75M to $100M+). Very small opportunities (<$10 or $15M) have a larger discount due to relatively low absolute savings amount

- Payment terms and timing: Buyers pay a premium for delayed payment terms. Pricing also tends to increase the later a transaction occurs, as project supply dwindles and more last-minute buyers come into the market. Conversely, pricing tends to decrease for forward commitments, especially for those with longer time horizons into future tax years

Leading project developers often have lofty expectations on the pricing they expect to receive on their credits, and as a result there is often a robust back and forth before settling on a price.

Who pays for tax credit insurance?

Sellers typically purchase tax credit insurance, with the buyer listed as an “additional insured” on the policy. Buyers occasionally elect to purchase tax credit insurance instead of the seller, but this scenario is far less common.

Who pays for legal and diligence fees?

To minimize “above-the-line” expenses, buyers typically negotiate for sellers to pay a capped reimbursement amount for documented third party legal and / or diligence fees. The reimbursement is generally an absolute dollar amount (versus a percentage of the credit amount), and generally increases based on the complexity of the transaction. For example, a portfolio with many projects is likely to have a larger expense reimbursement compared to a single utility-scale asset.

Is the benefit — the difference between the face value of the credits and the purchase price — taxable?

The benefit is not subject to federal tax. While many states have rolling conformity to federal taxation rules, we recommend checking with your tax advisor on state-level taxation issues.

Markets

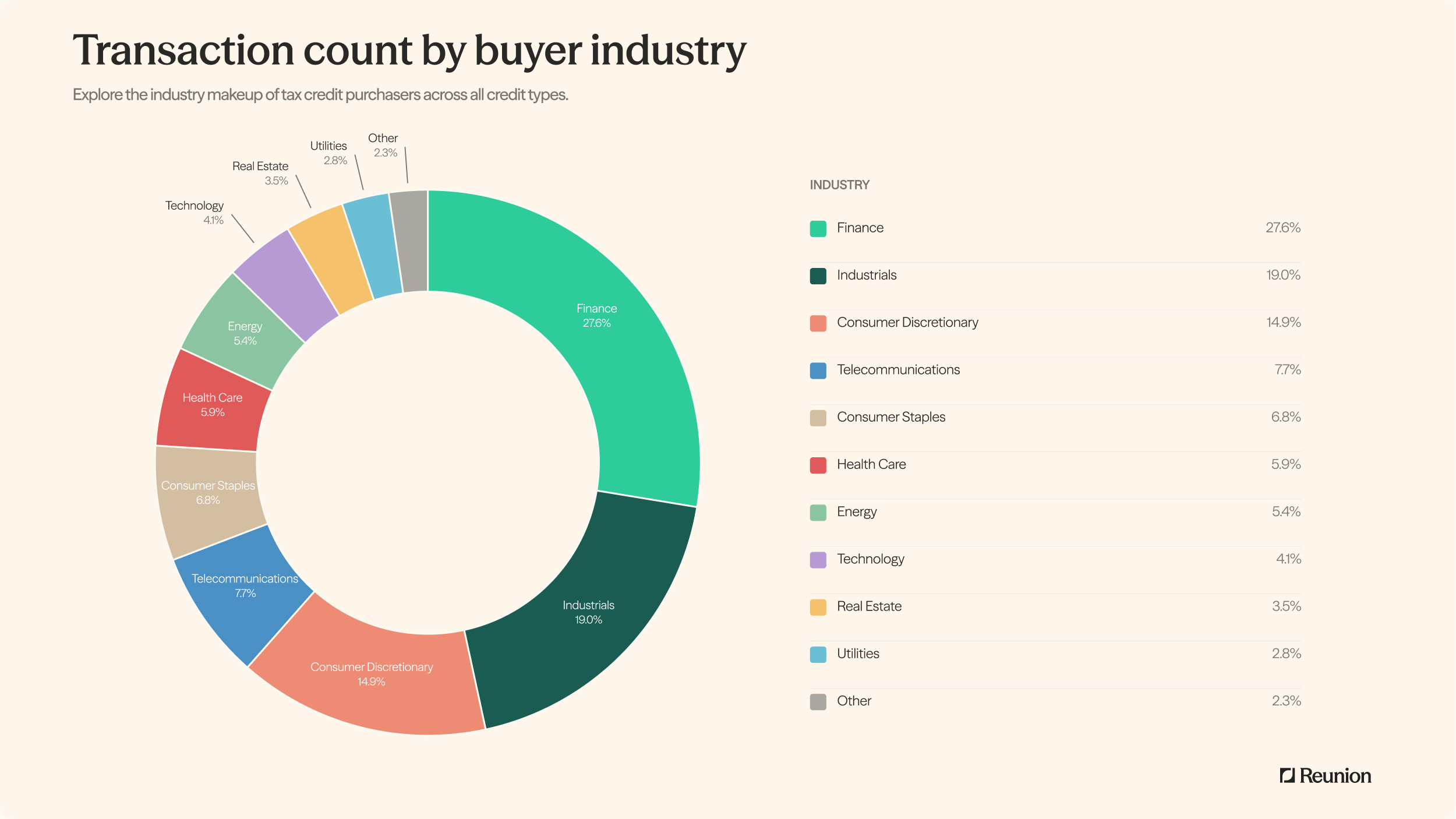

What other corporations are active in purchasing transferable tax credits?

Although public disclosures are very rare, Fortune 500 companies from nearly every sector are actively purchasing clean energy credits. Examples of publicly disclosed transactions include:

- Visa: $870M tax credit purchase from First Solar

- Fiserv: $700M tax credit purchase from First Solar

- MarketAxess: $16M tax credit purchase from Broadwind

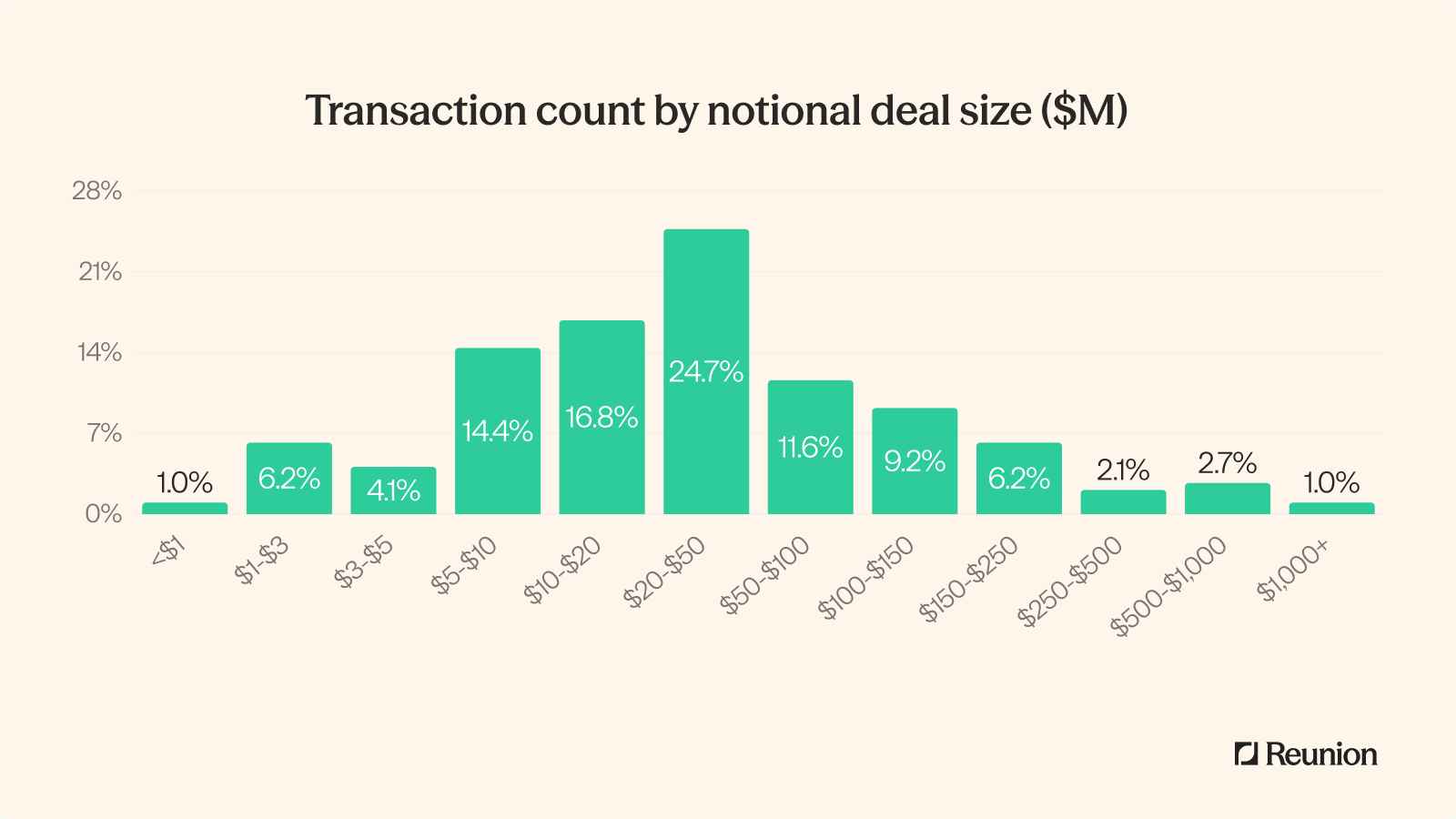

What is a typical tax credit purchase amount?

Reunion maintains a database that monitors over $25B of tax credit transactions. We observe that a majority of transactions are in the $15M to $200M range, though we have worked on multiple individual transactions in the $1 billion range.

Corporate taxpayers can offset up to 75% of their federal tax liability with general business credits, which include transferable tax credits. According to a 2024 Reunion survey, 85% of surveyed tax credit buyers plan to offset at least 50% of their tax liability using transferable tax credits.

Risks

What are the primary risks associated with purchasing a tax credit?

§48 ITCs are subject to several primary areas of risk, which buyers should thoroughly diligence:

- Qualification: Validate that the underlying project qualifies as energy property, the proper cost basis is used, and the project was placed in service in the appropriate tax year. If applicable, validate qualification for bonus credit adders such as energy community and domestic content. If applicable, the buyer should also validate that the project complies with Prevailing Wage and Apprenticeship requirements (for projects above 1 MW that began construction on or after January 29, 2023) and Foreign Entity of Concern restrictions (see below for more commentary on FEOC).

- Structure: Validate that seller is an eligible transferor, and that the seller’s underlying legal structure will be respected by the IRS.

- Recapture: ITCs are subject to the recapture provisions of §50. The ITC carries a five-year compliance period, in which the potential amount of credit that can be recaptured starts at 100% for the first year and steps down 20% per year. Practically speaking, recapture can occur in the following scenarios: (1) the property ceases to be a qualified energy facility or (2) there is a change in ownership of the property.

- Counterparty: Buyers should understand the corporate structure of the seller, and identify and diligence any disregarded entities between the project company and the seller. Doing so will ensure proper chain of title of tax credits to the seller. Additionally, buyers should understand the financial strength of the seller and, by extension, the “value” of the seller’s indemnity and / or guaranty

How do I ensure that the tax credits apply to the appropriate tax year?

The placed in service (PIS) date determines the tax year to which the credits can be applied. A project that is placed in service in 2026, for instance, generates ITCs that can be applied to a company’s 2026 tax liability (for calendar-year filers). As part of due diligence, the buyer should review documentation substantiating when the project was placed in service; the IRS employs a five-factor test to determine when a project is PIS for tax purposes.

There is a risk that a PIS date “slips” into a subsequent tax year, and the buyer is unable to apply the credits to a given tax year as planned. To mitigate this risk, buyers will often negotiate a two-tiered pricing approach, in which the price per credit is reduced if the credits slip from one year to the following (we have seen this discount commonly range from 1.5 to 3 cents).

Have other tax credit buyers been subject to audit activity?

There are many tax credit buyers that are in the Compliance Assurance Process (CAP) program; CAP buyers assume that the IRS will audit their tax credit purchase activity at some point. These buyers typically prioritize ensuring that they have all necessary documentation prepared in advance, in the event of an IRS information document request (IDR).

Reunion has worked with several companies in the CAP program that have satisfactorily responded to audit activity, including responding to IDRs.

We have not yet heard of buyers outside the CAP program subject to audit activity from tax credit transfers, but we do expect that it will happen.

Describe how the process works if the IRS does challenge a credit?

Tax proceedings are one of the heavily negotiated points in a tax credit transfer agreement (TCTA).

If the IRS performs an audit of the tax credit buyer and determines that the credits are excessive or invalid, the buyer will typically request an appeal with the IRS Independent Office of Appeals.

If the IRS Independent Office of Appeals upholds the decision, the buyer or the tax credit insurer may choose to proceed to litigation, typically in U.S. District Court or in U.S. Tax Court. The obligation to proceed to litigation, and how far to take the litigation (instead of triggering an indemnity payment from the seller) is a point of negotiation between buyers and sellers.

Tax credit insurers typically will include the right to litigate as part of the terms and conditions of the tax credit insurance policy, as the insurer will want the opportunity to litigate before needing to pay out a claim.

If there is a successful challenge or disallowance of the credit by the IRS, will I be made whole?

In case there is a loss event, a well-negotiated Tax Credit Purchase Agreement will ensure that the buyer will be made whole through the indemnity and / or tax credit insurance. The protections are designed to cover all potential losses, including penalties, interest, taxes, contest costs, and fees.

What are common negotiation points related to tax credit insurance?

One common point of negotiation between buyers and sellers is defining the scope of the tax credit insurance policy, and ensuring that the buyer is comfortable with the covered tax positions as well as any potential exclusions to the policy.

The other primary point is to define the limit of liability on the policy, to ensure that the buyer will be fully covered in the event of a loss. Buyers sometimes agree to a lower limit of liability in exchange for better pricing on the credit, or in cases where they see other factors that reduce risk on the transaction (e.g., strong seller balance sheet).

Legislative

Under what conditions are credits subject to new OBBBA provisions, such as foreign entity of concern (FEOC)?

Projects that began construction before the end of 2024 have the option to qualify for §48 credits rather than §48E credits. §48 credits are not subject to FEOC restrictions.

§48E credits that begin construction before the end of 2025 are not subject to the FEOC material assistance restrictions, which limit the amount manufactured products that can originate from restricted countries (China, Iran, North Korea, and Russia).

What happens if there’s another change in law between when execution of a tax credit transfer agreement, and funding of the transaction?

The tax credit transfer is not officially consummated until the transfer election statement is filed when the buyer and seller file their tax returns. Buyers typically negotiate TCTAs to include “no change in law” as a condition precedent (CP) to funding. Therefore, if there is a significant change in law between signing the TCTA but before funding, the buyer would have the option to walk away from the transaction.