Denis Cook

September 9, 2024

What Is Tax Credit Market, Its Size & How It works

Explore the projected $45B-$50B growth of the transferable tax credit market size, with monetization strategies like transferability, tax equity & direct pay.

For Buyers

Executive summary

Over the past 12 months, the rate of growth in the transferable tax credit market has continually surprised industry observers and participants.

Reunion has analyzed how large the transferable tax credit market could be on an annual basis, as well as the size of various monetization strategies – tax equity, direct pay, retention, and transfer.

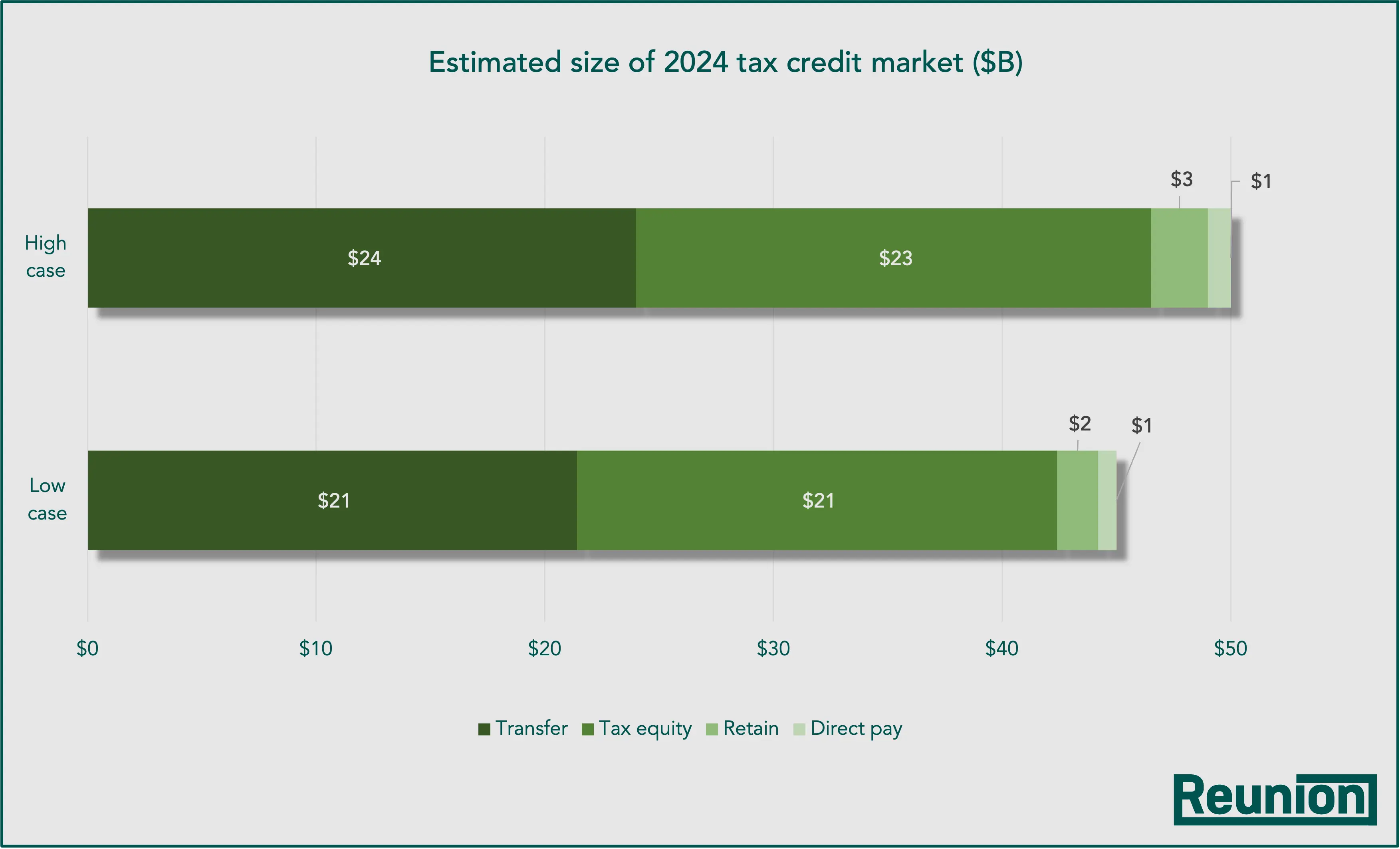

We estimate that the total size of the transferable tax credit market in 2024 will range from $45B to $50B, which will be broken into four key monetization strategies:

- Transfer: $21B to $24B

- Tax equity: $21B to $23B

- Retain: $1.8B to $2.4B

- Direct pay: $0.8B to $1.0B

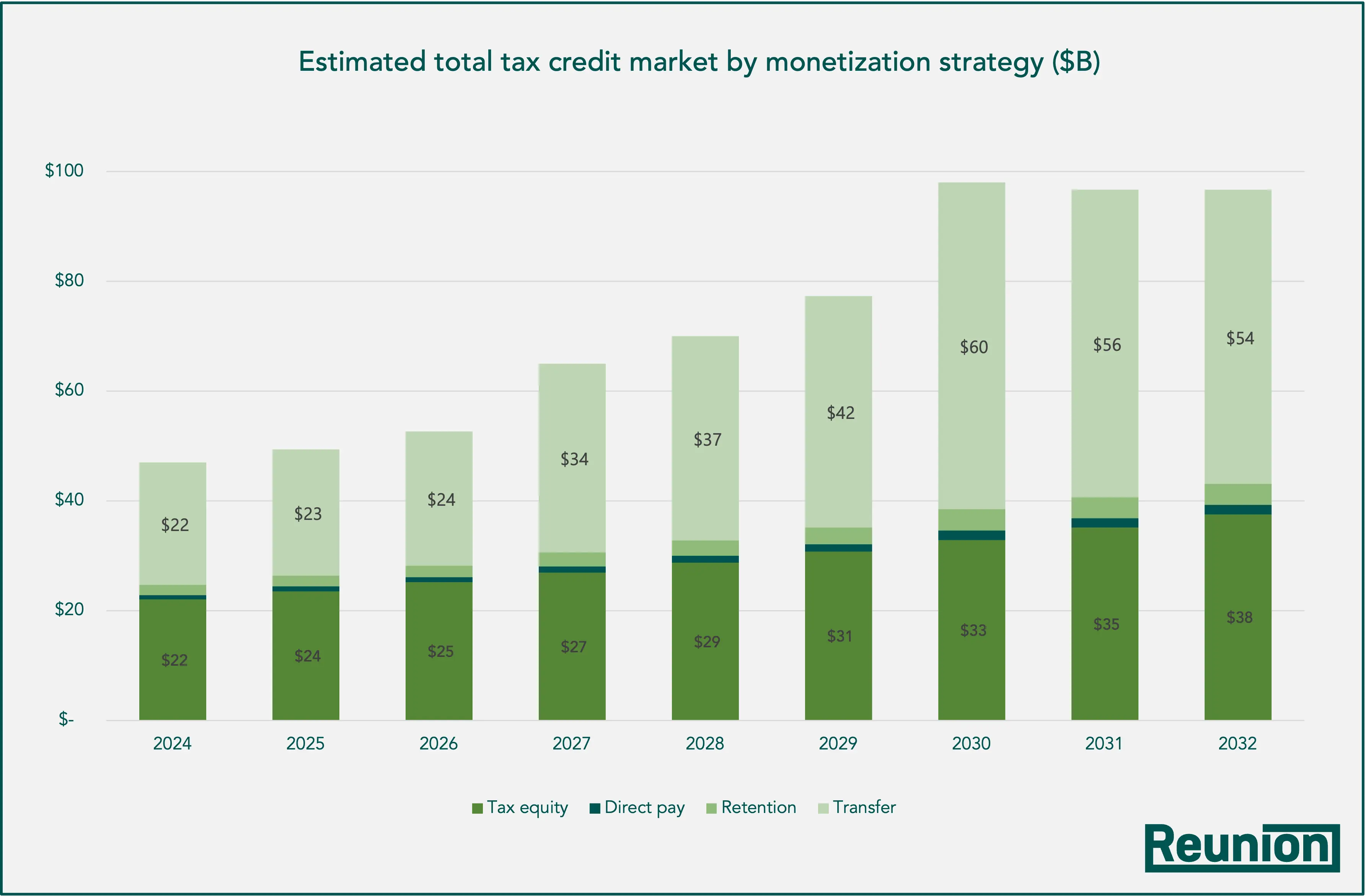

Over a nine-year period, Reunion estimates the total volume of clean energy tax credits to steadily climb, surpassing $90B in 2030.

Of the annual total, we expect approximately 50% to 60% to be monetized through transferability.

We ran our estimate through 2032 for two reasons. Under the §45X credit, manufactured components are subject to a four-year phase-down beginning in 2030 (75%, 50%, 25%, 0%). Therefore, manufactured components will no longer be eligible for the §45X after 2032. Also, 2032 is the first potential "applicable year" for the four-year phase-out of the §45Y PTC and §48E ITC.

Jump to a section

- Total transfer market: How many clean energy tax credits will be transfer in 2024?

- Tax equity: How many clean energy tax credits that are eligible for transferability will be monetized through traditional tax equity in 2024?

- Direct pay: How many clean energy tax credits that are eligible for transferability will be monetized through direct pay in 2024?

- Retain: How many clean energy tax credits that are eligible for transferability will be monetized directly by the developer, manufacturer, or refiner in 2024?

- Transfer: How many clean energy tax credits will be transferred in 2024?

- Stranded: How many clean energy tax credits will not be monetized in 2024?

- Looking ahead: How many clean energy tax credits will be eligible for transfer through 2032? Of these, how many will be transferred?

Total Transfer Market: $45B - $50B

How many clean energy tax credits will be eligible for transfer in 2024?

To estimate the total size of the market for transferable tax credits in 2024, we reviewed several existing estimates by industry observers:

- Congressional Budget Office

- Credit Suisse

- Evercore ISI

- Goldman Sachs

- University of Pennsylvania, Penn Wharton Budget Model

Our analysis identified two key trends:

- A significant increase in estimates following the passage of the IRA: Before August 2022, estimates of the volume of tax credits that would be generated following the passage of the IRA were clustered below $20B. After the IRA became law, estimates markedly increased

- Clustering between $45B and $50B: More recent estimates have fallen between $45B and $50B

$19B | University of Pennsylvania, Penn Wharton Budget Model (July 2022)

Shortly before the passage of the IRA, the University of Pennsylvania's Penn Wharton Budget Model (PWBM) provided a preliminary estimate of the budgetary effects of the legislation from 2022 through 2031.

The report pegged the ten-year cost of the IRA's "climate and energy" provisions at $369B and the 2024 cost at $35.7B. Importantly, PWBM's climate and energy bucket includes several sets of provisions:

- Tax rebates and credits to lower energy costs for households

- Tax credits, research, loans, and grants to increase domestic manufacturing capacity for wind turbines, solar panels, batteries, and other essential components of clean energy production and storage

- Tax credits to reduce carbon emissions

- Programs to reduce the environmental impact of agriculture

- A new fee on methane emissions

To isolate transferable tax credits, we can pull percentages for the various climate and energy provisions from an updated PWBM analysis (which we'll discuss in further detail):

The resulting cost of transferable tax credits for 2024, then, is 54% of $35.7B, or $19.2B. If we apply the same percentage to the ten-year window, we arrive at a total cost of $198.3B for transferable tax credits.

$11B | Congressional Budget Office (August 2022)

In an August 2022 report, the Congressional Budget Office (CBO) estimated the annualized budgetary effects of the Inflation Reduction Act (IRA) from 2022 to 2031. The report covers the entirety of the IRA, although transferable tax credits are broken out by their IRA section. IRA section 13101, for example, extends the §45 PTC.

The CBO estimates the ten-year budgetary impacts of transferable tax credits at $209.8B, $10.5B of which is in 2024.

$20B | University of Pennsylvania, Penn Wharton Budget Model (August 2022)

Once the Senate had passed the IRA, PWBM updated their July 2022 estimated budgetary effects of the IRA. The analysis, from August 2022, resulted in a slight uptick in cost across the board.

To estimate the size of the transferable tax credit market, we have to again scale the "climate and energy" provisions by 54%. The result is $20.0B for 2024 and $206.8B for 2022 through 2031.

$49B | Credit Suisse (November 2022)

Credit Suisse produced one of several analyses that argued initial estimates of the size of the IRA were low – perhaps as much as 3x too low:

"Climate spending will likely be significantly higher than the headline estimate. Roughly two-thirds of the baseline spending is allocated to provisions where the potential federal credit/incentive is uncapped. Our assessment of potential demand for clean electricity production tax credits (PTC) and investment tax credits (ITC), carbon capture, clean hydrogen, and renewable/battery manufacturing credits shows federal spending could reach >3x the cost estimates assigned for these key provisions. The advanced manufacturing provision alone could cost US$250 billion given the credits across solar, wind, and battery supply chains."

Credit Suisse estimated the ten-year cost of transferable tax credits at $528B and the 2024 cost at $49B.

Wood Mackenzie similarly argued that the long-term cost of the IRA would greatly surpass initial estimates. However, Wood Mackenzie focused their analysis on ITCs and PTCs from solar, wind, and storage, so we omitted it from our review.

$33B | Goldman Sachs (March 2023)

Goldman Sachs published an in-depth analysis of the costs and benefits of the IRA and, like Credit Suisse, concluded that early estimates were drastically low. Goldman Sachs estimated the IRA will cost the U.S. government $1.2T by 2032, with some incentives continuing into 2040.

To arrive at an estimate for the 2024 tax credit market, we should remove EVs and buildings from Goldman's estimate because these credits apply largely to individuals and will not be transferred. In exhibit 18, Goldman Sachs estimates that EV- and biofuel-related IRA programs will cost the U.S. government $393B and $43B, respectively.

If we apply this ratio – 90.1% EVs, 9.9% biofuels – to the combined 2024 estimate for “EVs and biofuels,” we remove approximately $9B of cost from 2024, resulting in an annual total of approximately $35B. Buildings further reduce this estimate by approximately $2B, resulting in an 2024 cost of approximately $33B.

Although Goldman Sachs did not publish a year-by-year estimate for transferable tax credits, they assembled a chart of annual IRA spending:

$48B | University of Pennsylvania, Penn Wharton Budget Model (April 2023)

Shortly after the Goldman Sachs report, PWBM released a third estimate of the budgetary effects of the IRA. Importantly, GWBM relied heavily on the Goldman Sachs report: "In preparing these updated estimates, PWBM consulted with private sector experts to understand the likely growth in utilization by climate and energy provision. We are especially grateful to the energy team at Goldman Sachs who helped break down each area and further aided our efforts to produce a budget score against the pre-IRA baseline."

PWBM estimated the total cost of the IRA's energy and climate provisions from 2023 through 2032 – a new ten-year window – at $1.0B. If we isolate transferable tax credits, we arrive at a total of $561B.

We can allocate the $561B total over the ten-year window, assuming a similar annual allocation percentage from PWBM's earlier estimates. Under this assumption, we get $48.3B for 2024.

$47B | Evercore ISI (April 2024)

“Drawing on projections from the U.S. Treasury,” Evercore ISI estimated that the “total addressable market of potentially transferable energy tax credits is $47 billion in 2024.” Evercore notes that “not all these credits will ultimately be transferred” – a key detail we'll explore below.

Viewing the estimates through time

When viewed through time, the eight estimates we've examined exhibit two trends:

- A significant increase in estimates following the passage of the IRA: Before August 2022, estimates of the volume of tax credits that would be generated following the passage of the IRA were clustered below $20B. After the IRA became law, estimates markedly increased

- Clustering between $45B and $50B: More recent estimates have tended to fall in the high $40B range

Tax Equity: $21B - $23B

How many clean energy tax credits that are eligible for transferability will be monetized through traditional tax equity in 2024?

With the passage of the IRA, clean energy tax credits can be monetized through transferability, traditional tax equity, or "hybrid" structures involving some mix of both. To properly size the transferability market, then, we need to remove "pure play" tax equity.

Although precise tax equity transaction volumes are not publicly available, Norton Rose Fulbright provides reliable snapshots in their annual cost of capital webinar. In the 2024 cost of capital webinar, for example, Jack Cargas of Bank of America and Rubiao Song of JPMorgan estimated the 2023 tax equity market at $20B to $22B:

- Jack Cargas, Bank of America: "We estimate that the volume was $20 to $21 billion [in 2023], roughly in the same ballpark as the year before."

- Rubiao Song, JPMorgan: "We saw a slight uptick in tax equity volume in 2023 compared to 2022. We put the traditional tax equity at $21 to $22 billion in 2023."

We can create a ten-year series by reviewing the transcripts from prior years – 2023, 2022, 2021, etc.

When estimating 2024 tax equity volumes, Rubiao Song said, "If the economy remains strong, we could see tax equity volume growing by single-to-low double digits."

Despite uncertainty around the potential impacts of Basel III requirements on tax equity investments, Reunion estimates that $21B to $23B of tax credits will be monetized through traditional tax equity in 2024.

Importantly, the amount of tax equity investment is not directly representative of tax credit generation, as some amount of investment is associated with benefits of depreciation and the rights to future project cash flows. However, for purposes of this simplified analysis, we have ignored this distinction and will address it in future discussions.

Direct Pay: $0.8B - $1.0B

How many clean energy tax credits that are eligible for transferability will be monetized through direct pay in 2024?

Of the approximately $47B in 2024 tax credits that are eligible for transfer, some will be monetized through direct pay. As Evercore notes in their report, "For a subset of credits" – 45X, 45Q, and 45V – "companies may take advantage of a time-limited provision through which they can receive the credit as a direct payment from the [IRS] after filing their tax returns."

Evercore goes on to emphasize that, "Figures on project registrations released by the U.S. Treasury suggest that even in cases where the seller would have the option for 'direct pay' after filing tax returns, the vast majority are still opting for transfer."

As the Treasury stated, "More than 98% of...facilities or projects are pursuing transferability."

Based on Reunion's 2024 transactions data, which covers nearly $5B in verified transactions, Reunion estimates $0.8B to $1.0B in 2024 tax credits will be monetized through direct pay in 2024. (We can perform a simple check on our estimate by scaling our $47B total market value by 98%, which results in $0.94B.)

Retain: $1.8B - $2.4B

How many clean energy tax credits that are eligible for transferability will be monetized directly by the developer, manufacturer, or refiner in 2024?

Based on SEC filings from large, publicly traded utilities, Reunion estimates that 4% to 5% of 2024 tax credits will be retained by developers, manufacturers, and refiners to offset their own tax liability. They will not, in other words, transfer all of their IRA tax credits.

In their 2023 10-K, for example, Duke Energy states, "...due to its existing tax attributes and projected tax credits to be generated related to the IRA, Duke Energy does not expect to be a significant federal cash taxpayer until around 2030."

Reunion's estimates that $1.8B to $2.4B of clean energy tax credits will be retained by their originator.

Transfer: $21B - $24B

How many clean energy tax credits will ultimately be transferred in 2024?

In the simplest sense, tax credit transfers become the "plug" in our equation: [total tax credit market] = [tax equity] + [direct pay] + [retention] + [transfer].

Recognizing that we have provided estimated ranges for each value, we can create a "high" and "low" case resulting in an estimated transfer market range of $21B to $24B.

"Stranded" Credits

How many clean energy tax credits will fail to be monetized, irrespective of strategy?

Although we've focused our anaylsis on accretive monetization strategies, it's worth noting the existence of a fifth bucket: "stranded" credits. These are credits that are generated but, for whatever reason, not monetized through tax equity, transferability, direct pay, or retention.

Reunion has seen stranded credits first-hand with smaller developers who were unable to successfully transfer 2023 credits with values in the low hundreds of thousands. We also assume some stranded credits will emerge from developers in financial distress.

We believe stranded credits constitute a de minimis and hard-to-estimate segment of the transferability market and have excluded them from our analysis.

Looking Ahead

How many clean energy tax credits will be eligible for transfer through the early 2030s? Of these, how many will be transferred?

We expect the overall tax credit market to grow by an average of 10% to 15% per year, peaking in 2030. The highest percentage of this growth will occur in transferability (versus other monetization strategies). We estimate that the total tax credit market will approach $700B through 2032, over $350B of which will be monetized through transferability.

We ran our estimate through 2032 for two reasons. Under the §45X credit, manufactured components are subject to a four-year phase-down beginning in 2030 (75%, 50%, 25%, 0%). Therefore, manufactured components will no longer be eligible for the §45X after 2032. Also, 2032 is the first potential "applicable year" for the four-year phase-out of the §45Y PTC and §48E ITC.

Further updates to come

Reunion will update and refine this analysis as we facilitate more transactions and further data comes to market. If your team has data to share on an anonymized basis, we would welcome the opportunity to connect.

Andy Moon

August 28, 2024

Reunion and CAC Specialty to host webinar on Thursday, September 5th for tax credit buyers

Jordan Tamchin, Executive Vice President and leader of the Tax Insurance Practice at CAC Specialty, joins our Q3 buyer office hours on Thursday, September 5th at 2:00pm ET.

For Buyers

Jordan Tamchin, Executive Vice President and leader of the Tax Insurance Practice at CAC Specialty, will join Reunion's transactions team for a 60-minute workshop covering recent market developments in tax credit insurance and a lively discussion about unique tax insurance solutions that have emerged in 2024.

Topics

- Tax credit insurance at a glance: Typical covered tax positions and exclusions

- Market snapshot: Depth of insurance market, pricing considerations, underwriting standards

- Emerging issues and trends: Coverage of step ups, PWA underwriting, bonus credit adder coverage, buy side vs sell side policies, typical limits of liability, audit experience

- Audience Q&A

Speakers

Jordan Tamchin – CAC Specialty

Jordan Tamchin is Executive Vice President and leader of the Tax Insurance Practice at CAC Specialty, where he specializes in delivering innovative and unique insurance solutions for the most complex tax risks across a variety of tax credit and tax equity deals.

Andy Moon and Billy Lee – Reunion

Andy Moon and Billy Lee are the co-founders of Reunion and work closely with Fortune 500 corporations and clean energy companies to buy and sell clean energy tax credits.

Andy and Billy have led hundreds of clean energy financings since 2006, including some of the first solar transactions with institutions such as US Bank, JP Morgan, Wells Fargo, Bank of America, D.E. Shaw, and others.

Questions welcome

We want our office hours to be interactive, so please bring any questions you have, whether related to current market conditions, pricing, or commercial terms.

You're welcome to ask questions beforehand.

Connie Chern, CPA

August 23, 2024

Section 48 ITC Updates & Impact Of Regulations on Due Diligence

Navigate Section 48 ITC transactions with a comprehensive due diligence guide. Address risks, ensure compliance & secure valuable bonus credits effectively.

For Sellers

For Buyers

Executive summary

Transferable tax credits are sold at a discount to face value, providing attractive financial benefits to corporate investors. They are not without risk, however, and tax credit buyers should have a clear sense of how to identify, track, and mitigate relevant risks.

At the same time, clean energy developers should understand the scope of due diligence during a tax credit transfer.

This due diligence checklist and documentation guide gives tax credit buyers, sellers, and their respective advisors a set of shared expectations on the required analysis and documentation for Section 48 Investment Tax Credits.

To download a PDF version of this guide, please visit our resources page.

Jump to a due diligence category

- Transaction overview

- Major deal participants

- Seller diligence

- Qualification

- Structure

- Recapture (qualified energy facility, change in ownership)

- Prevailing wage and apprenticeship requirements (compliance, exemption)

- Bonus credits (domestic content, energy community, low-income community)

- Tax credit insurance

Transaction overview

The transaction overview should include an overall description of the transaction, including:

- Brief description of sponsor

- Technology

- Project size in MW AC, location, and description

- Placed in service (PIS) date

- Eligible cost basis

- Resulting ITC credit amount

- Description of tax credit percentage, including bonus credit adders and compliance with, or exemption from, prevailing wage and apprenticeship requirements

- Details on how the project is financed

Major deal participants

Tax credit transfers involve a range of stakeholders on the buy- and sell-sides, all of whom should be memorialized for reference during the five-year recapture period.

Seller diligence

Qualification

Buyer should validate that the Project qualifies for the Section 48 ITC. Buyer should ensure that the Project qualifies as energy property, the proper cost basis is used, and that the Project was placed in service in the appropriate tax year.

Structure

Buyer should validate that Seller is an eligible transferor, and that the Seller’s underlying legal structure will be respected by the IRS.

Recapture

To avoid recapture, a Section 48 ITC requires that (1) the property remains qualified energy property for five years and (2) there is no change in ownership of the property for five years. If a project fails to meet these requirements, the IRS will recapture the unvested portion of the ITC.

The ITC vests equally over a five-year period, meaning 20% of the total ITCs claimed will vest on each anniversary of Project’s placed in service date.

Qualified energy facility

A property can cease to be qualified energy property when an asset is disposed of, or otherwise ceases to be investment credit property to the eligible taxpayer during the recapture period. For example, the asset is:

- Destroyed and not rebuilt and placed back in service

- Abandoned

- Repurposed to sell something other than electricity derived from the qualified generation asset

Key risk mitigation measures include sufficient property and casualty insurance, adequate site control and interconnection rights, and identification of alternatives in the event of an Offtaker default.

Change in ownership

A change in ownership can occur if the project owner transfers its ownership of the facility during the five-year recapture period. If a lender has a collateral interest in the project company, a foreclosure can trigger recapture due to change in ownership.

Key risk mitigation measures include a forbearance agreement with lenders, structuring the debt in a way that foreclosure will not trigger a recapture, and indemnification from the seller.

Prevailing wage and apprenticeship requirements

Buyer should validate that the Project is exempt from, or compliant with, prevailing wage and apprenticeship requirements. Prevailing wage rules require that certain workers are paid a minimum prevailing wages specified by the U.S. Department of Labor during the construction of a facility or property, and during alteration or repair of a facility or property for a certain number of years after the project is placed in service.

Buyers should require proper documentation that the correct wage was paid.

Exempt from PWA

Compliant with PWA

Bonus credits

If a Project claims a bonus credit adder (domestic content, low-income community, or energy community), the Buyer should substantiate that the Project qualifies for the relevant bonus credit adder.

Domestic content

Energy community

Low-income community

Tax credit insurance

If a Seller is unable to offer an indemnity from a creditworthy guarantor, tax credit insurance is commonly purchased to provide additional risk mitigation in the event of a disallowance or recapture of credits.

There is a robust market for tax credit insurance, which has been utilized on tax equity transactions for over a decade. Tax Credit Insurance Brokers can help place insurance with a wide selection of investment-grade insurance carriers.

Download Reunion's Section 48 Investment Tax Credit Due Diligence Guide

To download Reunion's Section 48 due diligence guide in PDF format, please visit our resources page.

Denis Cook

August 16, 2024

The transferable tax credit market continues to evolve, and Reunion is seeing several key trends emerge

The transferable tax credit market continues to evolve, and Reunion is seeing several key trends emerge

For Sellers

For Buyers

Reunion recently surpassed $1.5B in clean energy tax credit sales in 2024. Our transactions have spanned solar, wind, battery storage, fuel cells, biomass, and advanced manufacturing components.

Our team works directly with dozens of Fortune 500 tax credit buyers and leading clean energy companies, and we have observed several emerging trends in 2024.

Emerging 2024 trends

Speed of execution is a critical factor in winning deals

An increasing number of deals are competitive bidding situations. Buyers should have a clear sense from relevant stakeholders — e.g., CFO, legal, board of directors — on what deal terms are acceptable and what specific approvals are required prior to starting the negotiation process, as delays can be the difference between winning and losing a deal.

We have seen several companies proactively establish investment thresholds that allow them to move quickly for the right credit.

Very large credits carry premium pricing

There has been increased interest in tax credit purchases from major corporations that pay $500M to $1B or more in annual taxes, resulting in more competition for large credit opportunities.

These opportunities tend to trade at a premium — upwards of $0.01 to $0.02, depending on the credit type.

Buyers are increasingly interested in ITCs

Many buyers were reluctant to pay for ITCs early in the year because doing so required them to “pre-pay” their taxes. Buyers, consequently, willing to purchase ITCs in Q1 or Q2 were rewarded with deeper discounts.

Now that we are in Q3 and payments for ITCs will not occur until later in the year, buyer interest has increased.

Pricing on ITCs, PTCs, and AMPCs trended upward in Q3

Buyers, particularly ones that have bid and lost on tax credit opportunities, want to make sure that they lock in credits in time to offset Q3 and/or Q4 estimated tax payments.

There is a price ceiling on ITC transactions

ITCs are still expected to trade at a wider discount compared to production credits. Although sellers often ask for mid-$0.90s pricing for ITCs, buyers typically push back since lower-risk PTCs or AMPCs would be available at similar pricing.

Scope and coverage of insurance is a focus of deal negotiation

Initially, tax credit buyers demanded tax credit insurance to cover 100% or more of the tax credit value. We are seeing more flexibility in structures, whereby insurance may not cover the full tax credit amount due to presence of other risk mitigants such as portfolio diversification, creditworthy seller indemnities or parent guaranties.

Buyer fee reimbursement becoming standard

Over the past few months, virtually every transaction we’ve executed has included a capped fee reimbursement for the buyer. The size of the reimbursement is largely dependent on the deal size.

Billy Lee

August 12, 2024

Reunion and Summit Ridge Energy host webinar on Tuesday, August 20th for tax credit sellers

Phil Schapiro, VP of Project Finance at Summit Ridge Energy, joins our Q3 seller office hours on Tuesday, August 20th at 2:00pm ET.

For Sellers

Reunion recently announced our collaboration with Summit Ridge to sell $40M in tax credits to fund community solar projects.

Phil Schapiro, VP of Project Finance at Summit Ridge Energy, will join Reunion's transactions team on Tuesday, August 20th for a 60-minute workshop covering recent market developments and a discussion about their experience working through a tax credit transaction.

Topics

The workshop will include three 15-minute modules, with about five minutes of Q&A per module.

Speakers

Phil Schapiro – Summit Ridge Energy

Phil Schapiro is VP of Project Finance at Summit Ridge Energy, where he leads fundraising efforts across the capital stack including debt, equity, and monetization of tax credits.

Andy Moon and Billy Lee – Reunion

Andy Moon and Billy Lee are the co-founders of Reunion and work closely with Fortune 500 corporations and clean energy companies to buy and sell clean energy tax credits.

Andy and Billy have led hundreds of clean energy financings since 2006, including some of the first solar transactions with institutions such as US Bank, JP Morgan, Wells Fargo, Bank of America, D.E. Shaw, and others.

Questions welcome

We want our office hours to be interactive, so please bring any questions you have, whether related to current market conditions, pricing, or commercial terms.

You're welcome to ask questions beforehand.

Reunion

August 11, 2024

What Is the Production Tax Credit (PTC) and How Does It Work?

What is the Production Tax Credit and how does it impact your project economics? Explore eligibility, credit values, and key compliance requirements. Learn more today.

For Buyers

For Sellers

Introduction to Production Tax Credits (PTCs)

Production Tax Credits (PTCs) are performance-based federal financial incentives that reward the volume of clean energy generated or specific components manufactured and sold to unrelated parties. The current landscape includes legacy renewables under §45, technology-neutral electricity under §45Y, and specialized credits for nuclear energy (§45U), clean hydrogen (§45V), and transportation fuels (§45Z). Additionally, §45X supports the domestic production of advanced manufacturing components. These credits typically accrue over a ten-year period following a project’s service date. While most require Prevailing Wage and Apprenticeship (PWA) compliance for maximum value, §45X is a notable exception.

What Is the Production Tax Credit (PTC)?

A Production Tax Credit (PTC) is a federal income tax benefit calculated based on the precise amount of electricity or specific components produced and sold to unrelated parties. Essential IRC sections include §45, §45Y, §45X, §45U, §45V, and §45Z. Through transferability, eligible taxpayers can sell these credits to third parties for cash, simplifying clean energy financing. Unlike investment credits, PTCs do not face recapture risk but instead rely on rigorous production accounting to substantiate claims. To receive the full 5x credit multiplier, most projects must meet PWA standards, though advanced manufacturing under §45X is exempt.

How does the Production Tax Credit work?

The Production Tax Credit (PTC) provides a federal benefit based on the volume of energy produced or components manufactured and sold to unrelated third parties. For electricity projects (§45 and §45Y), the credit is calculated per megawatt-hour (MWh) generated over ten years, verified by revenue-grade meter reports or system operator settlement data. Advanced manufacturing under §45X uses specific rates tied to weight, capacity, or production cost. Credits are transferable for cash, and unlike investment credits, they carry no recapture risk. Buyers often pay for PTCs quarterly in arrears, aligning with estimated tax payment dates.

Which Energy Projects Qualify for the Production Tax Credit?

The Production Tax Credit (PTC) incentivizes investment in clean energy by offering tax benefits to a range of qualifying facilities — from traditional renewables to advanced manufacturing and emerging clean fuel technologies.

Advanced manufacturing: solar and wind components, batteries, inverters, and critical minerals produced in the United States

Eligibility often depends on either the beginning of construction date or the date the project is placed in service, making early planning and documentation critical for developers seeking to claim these credits.

How Much Is the Production Tax Credit Worth?

Credit values vary significantly by technology and labor compliance. The amount a project can claim depends on the applicable credit section, technology type, whether prevailing wage and apprenticeship standards are met, and any qualifying bonus adders. For 2025, the base credit rate for legacy renewable technologies and some newer tech-neutral projects is $6/MWh, while projects meeting PWA requirements qualify for a significantly higher full rate of $30/MWh. Certain technologies, such as open-loop biomass, receive a reduced rate of half these amounts, and 45V and 45Z rates are on different unit scales. Additionally, qualifying for energy community or domestic content bonus adders can increase these rates by another 10%.

PTC rates for electricity are generally inflation-adjusted annually, so the credit values a project can access may shift from year to year — understanding which rate applies to your placed-in-service year is an important part of project planning.

Production Tax Credit vs Investment Tax Credit

The Production Tax Credit (PTC) and Investment Tax Credit (ITC) differ in how the credit is calculated and when the financial benefit is realized. Developers often evaluate both incentives based on project economics and expected performance.

The key differences between these two credits are summarized below.

Because the PTC is based on electricity production rather than project cost, it can provide greater long-term value for projects with strong generation performance.

Compliance Requirements for Claiming the Production Tax Credit

To claim the maximum credit value, developers must comply with Prevailing Wage and Apprenticeship (PWA) rules during construction and the credit period. Projects must also navigate Foreign Entity of Concern (FEOC) restrictions, which prohibit "prohibited foreign entities" from claiming or receiving "material assistance" for credits like §45Y and §45X. Substantiation requires maintaining payroll records, production reports from revenue-grade meters, and evidence of sales to unrelated parties. Furthermore, projects must be placed in service within specific windows to qualify for intended rates and tech-neutral transitions.

Transferability and Monetization of Production Tax Credits

Under §6418, "eligible taxpayers" can transfer PTCs to unrelated third parties for cash consideration. This monetization process is a one-time transfer; buyers cannot resell purchased credits. To effectuate a transfer, sellers must complete IRS pre-filing registration to obtain a unique registration number for each facility. Both parties must then execute a Transfer Election Statement and attach it to their respective tax returns. Cash payments received by the seller are federal tax-exempt, while the buyer recognizes no federal gross income from the purchase discount.

How the Inflation Reduction Act Changed the Production Tax Credit

The Inflation Reduction Act (IRA) transformed the PTC landscape by introducing transferability, allowing developers to monetize credits without complex tax equity structures. It established a two-tiered rate system, linking maximum credit value to PWA compliance. The IRA also created the §45X credit to incentivize domestic manufacturing and introduced tech-neutral PTCs (§45Y) to replace resource-specific credits after 2024. Furthermore, it introduced bonus adders for projects in Energy Communities or those meeting Domestic Content requirements, significantly increasing the potential financial return for clean energy investments.

Key Takeaways for Developers Claiming the Production Tax Credit

Developers should prioritize production accounting and ensure all output is sold to unrelated parties to secure §45 and §45Y credits. Maintaining rigorous PWA documentation for both construction and ongoing alterations is essential to avoid credit reduction. To attract corporate buyers, developers can leverage quarterly-in-arrears payment structures, which allow buyers to offset estimated taxes without upfront cash outlays. Finally, securing tax credit insurance and offering strong indemnities can mitigate qualification risks and maximize the sale price of transferred credits.

Andy Moon

August 8, 2024

Unlocking the Economic Benefits of Tax Credits Before Cash Payment

Corporate taxpayers can buy tax credits in a way that preserves the timing of existing tax-related cashflows, or even improves corporate cash availability relative to the status quo.

For Buyers

Treasury’s June 2023 guidance made clear that corporate taxpayers can offset their quarterly estimated tax payments using tax credits they “intend to purchase,” opening the door for tax credit buyers to realize most or all of the benefit of a tax credit prior to paying the tax credit seller.

An increasing number of corporate tax directors and treasurers are focused on these types of opportunities, which do not require the buyers to go “out of pocket” to invest in a tax credit. Instead, the buyer pays a clean energy company a discounted amount compared to what they would have paid the IRS; the payment is concurrent with, or in some cases even after their scheduled tax payment date.

In this article, we outline four scenarios where buyers can realize tax benefits prior to cash outlay. We assume the buyer is a corporation that pays $200M each year in federal tax, and is looking to purchase $50 to $100M in tax credits.

Structures that enable buyers to realize full tax benefit prior to cash outlay

Structure 1: §45 PTCs, paid quarterly in arrears

The buyer commits to purchasing $100M in tax credits in Q1, which allows the buyer to offset $25M in tax payments each quarter. Note that if the buyer commits to purchase $100M in Q2 instead of Q1, there is a similarly strong benefit; the buyer can offset $50M in tax payments in Q2, and $25M in both Q3 and Q4.

§45 PTC transactions are typically paid quarterly in arrears. Often, the payment schedule is organized such that the buyer pays concurrently or shortly after each quarterly estimated tax payment date, based on actual tax credits generated during the preceding period. In this example, the buyer pays a clean energy developer $23.75M on each estimated tax payment date, instead of paying the IRS $25M. This results in a $1.25M net benefit each quarter, without any out-of-pocket investment.

For a real-world illustration of how this structure delivers value, see our Section 45 PTC transfer case study, which details transaction mechanics, cash flow timing, and buyer benefits.

Both §45 PTCs, from electricity generated by qualified renewable energy resources such as solar or wind, and §45X AMPCs from advanced manufacturing facilities, can be structured in this way.

Structure 2: §48 ITC portfolio, paid quarterly in arrears

A portfolio of ITCs can be structured similarly to the previous example, where the buyer pays quarterly in arrears (and is therefore able to utilize the full tax benefit prior to cash outlay).

In this example, the seller has a portfolio of rooftop solar projects that will be placed in service throughout the year, generating a total of $100M in tax credits. The seller is offering an 8% discount for the credits. The buyer commits to the tax credit purchase in Q1, and reduces their estimated tax payments by $25M each quarter.

The buyer will pay for the actual credits generated at the end of each preceding quarter. In this example, we assume that $20M in credits are generated in Q1 and Q2, while $30M is generated in Q3 and Q4. As a result, a relatively lower volume of credits need to be paid for in Q1 and Q2 (while the reduction in estimated tax payments remains fixed at $25M each quarter), resulting in a strong net benefit in Q1 and Q2. Overall, the buyer saves $8M in taxes over the course of the year, without any out of pocket investment.

There is a risk that the seller does not generate as many credits as anticipated in a given tax year; if so, a make-whole provision can be negotiated, which obligates the seller to make the buyer whole for any difference between what they agreed to pay for the credits and what they would have to reasonably pay for any replacement credits. In the event of a shortfall of credits, Reunion will also work with the buyer to source replacement credits.

Structure 3: Commit to ITC early in the year, but pay late in the year

In this scenario, a buyer commits to purchasing ITCs that a developer will generate later in the year. While the IRS was clear that buyers can offset quarterly tax payments with tax credits they intend to purchase, it is up to buyers and their legal and tax advisors to decide what documentation is needed to establish intent.

Assume that the buyer and seller execute a tax credit transfer agreement in Q1, and the buyer uses this as a basis to start offsetting quarterly estimated tax payments. If the project is placed in service around or after the Q3 estimated tax payment date, the buyer will be able to offset taxes in Q1, Q2, and Q3 before having to pay the seller for the credits (see example below). This will free up $25M of additional cash each quarter for other corporate purposes, with the understanding that a lump sum will need to be paid to the tax credit seller at a later date.

Sellers typically prefer to receive payment as soon as the credits are generated, but it is possible to negotiate a delayed payment date. For example, if the payment date can be delayed to on or after the Q4 estimated payment date, the buyer will be able to take the full benefit of the tax credit before any cash outlay.

This strategy also applies if the buyer commits to the ITC in Q2 or Q3, and does not have to pay for the credit until later in the year.

Scenario 3 carries the risk that the project is not placed in service in 2024 tax year, which would require the buyer to source replacement credits. It is possible for the buyers to negotiate a make-whole provision, in the event that credits are not delivered as promised.

Structure 4: Buy tax credits to top up at the end of the year, resulting in a lower Q4 or final tax payment

The final scenario is a variation of Scenario 3. A company purchases tax credits at the end of the year, once they have a more concrete understanding of their total annual tax liability, and delays payment until their Q4 or final tax payment date.

Assume the buyer has paid $150M in taxes through the first 3 quarters, and has $50M due in taxes in Q4. The buyer can fully offset their remaining taxes due by committing to purchase $50M in credits in Q4. In this example, the buyer receives an 8% discount, paying $46M for the credits and achieving tax savings of $4M. The buyer can achieve the full benefit of the credit prior to cash outlay by arranging to pay the seller of the tax credit on or after the Q4 estimated tax payment date.

The same logic applies for credits purchased in time for the final tax filing (e.g., on April 15 for the prior tax year, for a calendar year filer). If a buyer has $20M in remaining payments due at final tax filing, they could offset the entire tax payment through purchase of a tax credit. Assuming they could identify and purchase a tax credit with an 8% discount, they would pay $18.4M to a tax credit seller, achieving $1.6M in tax savings. It is worth noting that if the buyer procures more than they end up owing in their final tax payment, the overpayment can be applied to the first estimated tax payment of the following year.

How Reunion works with corporate finance teams to purchase tax credits

Reunion partners with corporate tax and treasury teams to identify and purchase tax credits in a five-step process.

Download an Excel model with the four structures

To download the Excel model featured in this article, please visit our resources page.

Customize these scenarios to your company

Tax credit buyers have a variety of objectives when choosing to purchase a tax credit. Some are focused on maximizing the amount they can save on taxes by looking for the largest discount, while others want to minimize complexity and risk.

We have observed an increasing number of corporate tax and treasury professionals who are focused on transactions that preserve the timing of existing tax-related cashflows, or even improve corporate cash availability relative to the status quo.

Please reach out to the Reunion team if you’d like to examine the cash flow impact of tax credit purchases in further detail, and hear about specific project opportunities that can be structured to maximize economic benefits prior to cash payment.

Reunion

June 30, 2024

What Is Section 48 Investment Tax Credit (ITC) & How Does It Work?

What is Section 48 ITC and how does it impact your project economics? Explore eligibility, transfer rules, and compliance requirements. Learn more today.

For Buyers

What Is Section 48 Investment Tax Credit (ITC)?

The Section 48 Investment Tax Credit (ITC) is a federal credit calculated as a percentage of a project’s qualified cost basis. It is realized during the tax year in which the eligible energy property is officially placed in service. The scope of §48 includes various technologies such as solar, geothermal, fuel cells, and energy storage systems. This credit generally applies to projects that began construction prior to 2025, before technology-neutral frameworks take over.

How the Section 48 Investment Tax Credit (ITC) Works

The Section 48 Investment Tax Credit (ITC) is a federal tax incentive for investment in qualified energy properties, facilities or energy storage technologies, under Section 48, determined by a project's qualified cost basis and providing a financial benefit when the property is placed in service. Most projects qualify for a 30% credit if they satisfy prevailing wage and apprenticeship (PWA) requirements; otherwise, the rate is reduced to 6%. The total value can grow through bonus adders related to domestic content or energy communities. A critical characteristic of ITCs is the five-year recapture period, during which the credit vests at 20% annually. If ownership changes or the facility ceases operations prematurely, the IRS may recapture the unvested portion. These mechanics form the foundation of how Section 48 ITCs are calculated, claimed, and evaluated during project diligence.

Eligibility for Section 48 Investment Tax Credit

Eligibility for Section 48 Investment Tax Credits (ITCs) depends on technology, timing, and labor standards. Section 48 applies to projects like solar, energy storage, and geothermal that begin construction before 2025 (with the exception of geothermal heat pumps which remain eligible if construction begins prior to January 1, 2035). Section 48E replaces this for zero-emission facilities and energy storage technologies placed in service after 2024; wind and solar projects have additional OBBBA restrictions around beginning of construction and placed in service dates compared to other technologies. To secure the full 30% credit rate, projects must satisfy prevailing wage and apprenticeship (PWA) requirements. Additionally, under the OBBBA, eligibility for §48E is restricted to entities that are not Foreign Entities of Concern (FEOC), ensuring benefits remain with compliant domestic stakeholders.

Projects Eligible Under Section 48 Investment Tax Credit

Section 48 Investment Tax Credits apply to a diverse range of energy properties. Under Section 48, qualifying investments include solar, fuel cells, geothermal, energy storage, and microgrid controllers. Section 48E extends eligibility to technology-neutral facilities generating zero-emission electricity.

In addition to the base credit rate, projects may qualify for the following bonus adders:

How to Transfer Section 48 Investment Tax Credits

Transferring a Section 48 Investment Tax Credit (ITC) involves a structured process, beginning with negotiating a tax credit transfer agreement. Sellers must complete IRS pre-filing registration for each Section 48 project to obtain a unique registration number for each facility. Finally, both parties must execute a transfer election statement and attach it to their respective tax returns to finalize the transfer.

The following documentation is typically required to substantiate and transfer the credit:

Common Mistakes to Avoid When Transferring Investment Tax Credits

When transferring Section 48 Investment Tax Credits (ITCs), taxpayers must avoid technical pitfalls like inflating the qualified cost basis under Section 48 with ineligible affiliate fees. Neglecting Prevailing Wage and Apprenticeship (PWA) compliance can drastically reduce credit rates from 30% to 6%. Additionally, failing to mitigate five-year recapture risks, such as lacking lender forbearance agreements to prevent ownership changes via foreclosure, is a critical oversight. Finally, late IRS pre-filing registration may invalidate intended credit transfers.

The IRS may recapture previously claimed Section 48 ITCs under the following circumstances:

Benefits of Transferring Investment Tax Credits

A Section 48 Investment Tax Credit (ITC) transfer offers significant financial and structural benefits for clean energy developers and corporate investors. By selling credits at a discount to face value, developers can reduce the cost and complexity of financing projects. For corporate buyers, transferability simplifies participation by eliminating the need for high-cost, multi-year tax equity co-ownership structures. Buyers enjoy a narrower set of risks because they are not directly subject to asset performance issues. Furthermore, ITCs provide straightforward accounting treatment and can be used to offset quarterly estimated tax payments or CAMT liabilities.

Recent Changes to Section 48 ITC (IRA & OBBBA)

The Inflation Reduction Act (IRA) expanded the Section 48 Investment Tax Credit (ITC) and introduced transferability, enabling credits to be sold for cash. Recently, the One Big Beautiful Bill Act (OBBBA) implemented an accelerated phasedown for wind and solar projects under §48E. The OBBBA also introduced strict Foreign Entity of Concern (FEOC) restrictions and eliminated the permanent 10% minimum ITC under Section 48. Furthermore, 2025 Treasury guidance modified Beginning of Construction standards for solar and wind projects.

Section 48 ITC: Key Takeaways

The Section 48 Investment Tax Credit (ITC) remains a transformative tool for clean energy financing, offering significant federal tax savings while lowering overall project costs. However, technical complexities introduced by the OBBBA necessitate a disciplined approach to risk management. To maximize value and avoid recapture or excessive credit transfer penalties, stakeholders must prioritize rigorous due diligence, substantiate qualification and cost basis, and ensure strict PWA compliance. Ultimately, a proactive strategy involving tax credit insurance and meticulous recordkeeping will ensure these incentives remain a secure investment.

Denis Cook

May 20, 2024

How Do Differences in Fiscal Year-End Dates Affect Tax Credit Transfers?

A review of how tax year-end affects transferability for buyers and sellers.

For Sellers

For Buyers

Transferable tax credits are a powerful tool for profitable companies looking to manage their federal tax liability. When buying transferable tax credits, however, companies must consider their tax year-end in conjunction with that of the seller in order to claim the credits correctly and to the greatest extent possible.

IRC §6418(d) dictates tax credit purchase timing between buyers and sellers

Internal Revenue Code §6418(d) explains the specific rule relating to the relationship between a buyer’s (transferee taxpayer) and seller’s (eligible taxpayer) tax year-ends.

"In the case of any credit (or portion thereof) with respect to which an election is made under subsection (a), such credit shall be taken into account in the first taxable year of the transferee taxpayer ending with, or after, the taxable year of the eligible taxpayer with respect to which the credit was determined."

Corporate taxpayers will face one of three scenarios when engaging tax credit sellers

Scenario 1: Buyer and seller both have a calendar year-end

For transactions where both the buyer and seller have a 12/31 tax year-end date, the credits simply apply to the tax year in which they were generated.

Scenario 2: Buyer's tax year ends before that of the seller

For a transaction where the buyer tax year ends before that of the seller – for example, the buyer has a 9/30 tax year, and the seller has a 12/31 tax year – any credits generated in the same calendar year are pushed into the next tax year for the buyer.

Scenario 3: Buyer's tax year ends after that of the seller

Lastly, for a transaction where the seller's tax year ends before that of the buyer, credits generated prior to the end of the seller tax year will apply to the current calendar year, but credits generated after the end of the seller tax year will push into the next calendar year.

Most eligible corporate taxpayers are calendar-year filers

There are approximately 600 publicly traded companies in the U.S. with a trailing 12-month income tax liability over $100M (as of May 2024).

Of these companies, 78% are calendar-year filers, while another 8.0% close out their fiscal year in February or September.

If we increase the threshold to $500M of trailing 12-month income tax liability, the numbers remain consistent: 78.2% of companies are calendar-year filers.

Find credits that complement your company's tax year-end

To find clean energy tax credits that complement your company's tax year-end, please contact Reunion's transactions team. In addition to providing access to our tax credit marketplace, we can curate a list of projects that most closely align with your needs.

Reunion Accelerates Investment Into Clean Energy

Reunion’s team has been at the forefront of clean energy financing for the last twenty years. We help CFOs and corporate tax teams purchase clean energy tax credits through a detailed and comprehensive transaction process.