Reunion

August 14, 2025

Tax Credit Buyer Webinar: Post OBBBA Analysis with Wesco and Mercantile Bank

Domenic Macioce, SVP of Tax at Wesco, and Pete Scudder, FVP and Financial Reporting Manager at Mercantile Bank, share practical insights on approaching tax credit transfers in a post "One Big Beautiful Bill Act" (OBBBA) landscape.

For Buyers

Joined by: Domenic Macioce, SVP of Tax at Wesco, and Pete Scudder, FVP and Financial Reporting Manager at Mercantile Bank

Reunion hosted a buyer-focused webinar with Domenic and Pete as they share practical insights on approaching tax credit transfers in a post "One Big Beautiful Bill Act" (OBBBA) landscape.

Recording: Transferable Tax Credits with Wesco and Mercantile Bank

Key topics

- 0:00 - 1:40 Introduction and Agenda:

- 1:41 - 5:25 Meeting the Speakers

- 5:26 - 13:38 New Tax Law's Impac

- 13:39 - 25:48 Company Approval Process

- 25:49 - 33:40 Finding the Right Credits

- 33:41 - 38:16 Negotiation Challenges

- 38:17 - 43:38 Pricing Strategies

- 43:39 - 49:24 The Role of Intermediaries

- 49:25 - 57:00 Future Market Predictions

- 57:01 - 59:36 Q&A

Insights from your peers:

1. Impact of Tax Legislation: New tax laws like OBBBA significantly impact the market by forcing companies to re-evaluate their tax capacity. This leads to a temporary slowdown as buyers adjust their financial models, highlighting the critical need for companies to monitor and respond to policy changes.

2. The Acquisition Process: The process for buying tax credits is formal and requires approval from top executives and a cross-functional team. Companies meticulously review each deal, often using a detailed package that outlines economics and risks, and they've learned that despite a structured approach, the timeline can be unpredictable due to administrative hurdles.

3. Economic and Risk Evaluation: Buyers now look beyond a simple price discount, focusing on the overall Return on Investment (ROI) and the net value after considering payment terms and the time value of money. They mitigate risk by diversifying their portfolio, carefully vetting counterparties, and ensuring strong legal protections like indemnification and insurance.

4. The Role of Intermediaries: Intermediaries like Reunion are crucial for managing the complex due diligence process, particularly by ensuring sellers are prepared with the necessary documentation. This helps streamline the transaction and build trust, which is highly valued by buyers.

Billy Lee

August 6, 2025

An overview of trends in clean energy tax credit transfers - August 2025

A look at market trends and insights, along with some highlights from recent Reunion transactions.

For Sellers

Below is our first Monthly Market Digest, which provides a look at market trends and insights, along with some highlights from recent Reunion transactions. To recieve this monthly, or add any friends or colleagues, subscribe here.

What we’re seeing in the market

Some buyers have lower tax liability due to the OBBBA, impacting their ability to purchase credits

Several corporate clients are expecting to have lower tax liability in 2025 due to provisions in the OBBBA, including 100% bonus depreciation, domestic research & experimental expensing, and higher interest deductibility. We have particularly noted this trend with capital-intensive (e.g., oil and gas, datacenter) and research-heavy companies (e.g., pharmaceutical). While some anticipated this liability decrease early in the year, many taxpayers are only now coming to this determination. On the other hand, taxpayers who were holding off on making purchases due to legislative uncertainty are now actively seeking 2025 credits, given that the OBBBA has provided clarity on tax planning.

Insurance costs have been on the rise

While sellers have been modeling insurance costs between 2 to 3% based on pricing in 2024, we have seen costs increase to a range of 3% to 4.5% or even more. Checks with insurance brokers suggest there is growing demand but limited capacity for insurance coverage, and requests for specific covered tax positions can add incremental premiums to a policy.

Tax credit sellers have had success selling 2024 vintage credits in 2025

We have regularly seen new 2024 credit opportunities emerge in Q1 and Q2 of 2025. Given the relative scarcity of prior year credits, tax credits sellers have been able to quickly find buyers and sell credits near the top of the tax credit price range in Reunion's Market Monitor. Many of these buyers are fiscal year tax filers, who require credits that were placed in service in 2024 from calendar year sellers to offset taxes in their fiscal years that end in 2025.

A majority of Reunion’s transactions are coming in under the capped reimbursement amount

Typically, sellers will negotiate a capped reimbursement for the buyer’s third-party legal and diligence costs, with the expectation that they will need to pay the full amount. In nearly a dozen of Reunion's recently closed transactions, the actual costs have come in less than the negotiated cap. This is largely due to Reunion’s due diligence and execution effort, where we provide a comprehensive diligence memo to both parties typically within 10 days of a term sheet being executed, to identify and tackle any issues upfront and avoid 11th-hour surprises.

Other initiatives: Forward commitment facility

We have partnered with a large, investment-grade taxpayer to enter into forward commitments for ITCs ($50+ million) that will be generated in 2026, 2027, and 2028. Our forward commitment facility will allow developers to maximize proceeds under their transfer bridge loans, as lenders will advance much higher amounts at lower costs when sponsors have executed a creditworthy tax credit agreement. The tax credit purchase commitment will ultimately be substituted with another purchaser upon closing, in a way that does not expose the lender to a less creditworthy balance sheet.

Highlights from recently closed transactions

Project Sequoia

$35M in 2025 ITCs, Utility-Scale Solar

A tax equity investor approached Reunion for assistance in selling $35 million in §48 investment tax credits from a tax equity partnership. The seller provided a guaranty from the parent company of the class B member, along with tax credit insurance. Reunion introduced the seller to a large corporate buyer with whom we have completed multiple transactions.

What was interesting about this transaction

- The transaction moved from term sheet to close in under 45 days, with funding occurring six months after close when the project is placed in service.

- Negotiations included the developer, the tax equity investor, the lender, and the tax credit purchaser. Despite the number of counterparties, Reunion was able to facilitate an efficient process, due largely to our rigorous due diligence and transaction support.

Project Olympic

$45M in 2025 AMPCs, Critical Minerals Production

A critical minerals producer worked with Reunion to execute a tax credit transfer agreement with a Fortune 500 taxpayer for $45 million of 2025 credits. Reunion was deeply involved in helping the buyer navigate contract negotiation, understand tax credit insurance, and gain internal approvals.

What was interesting about this transaction

- This transaction represented the fourth transaction that Reunion has facilitated with this particular seller, across three large taxpayers for the 2023, 2024, and 2025 tax years.

- By negotiating quarterly payments in arrears, the seller can benefit from ongoing cash flows throughout the year, supporting their corporate expansion plans.

Denis Cook

July 16, 2025

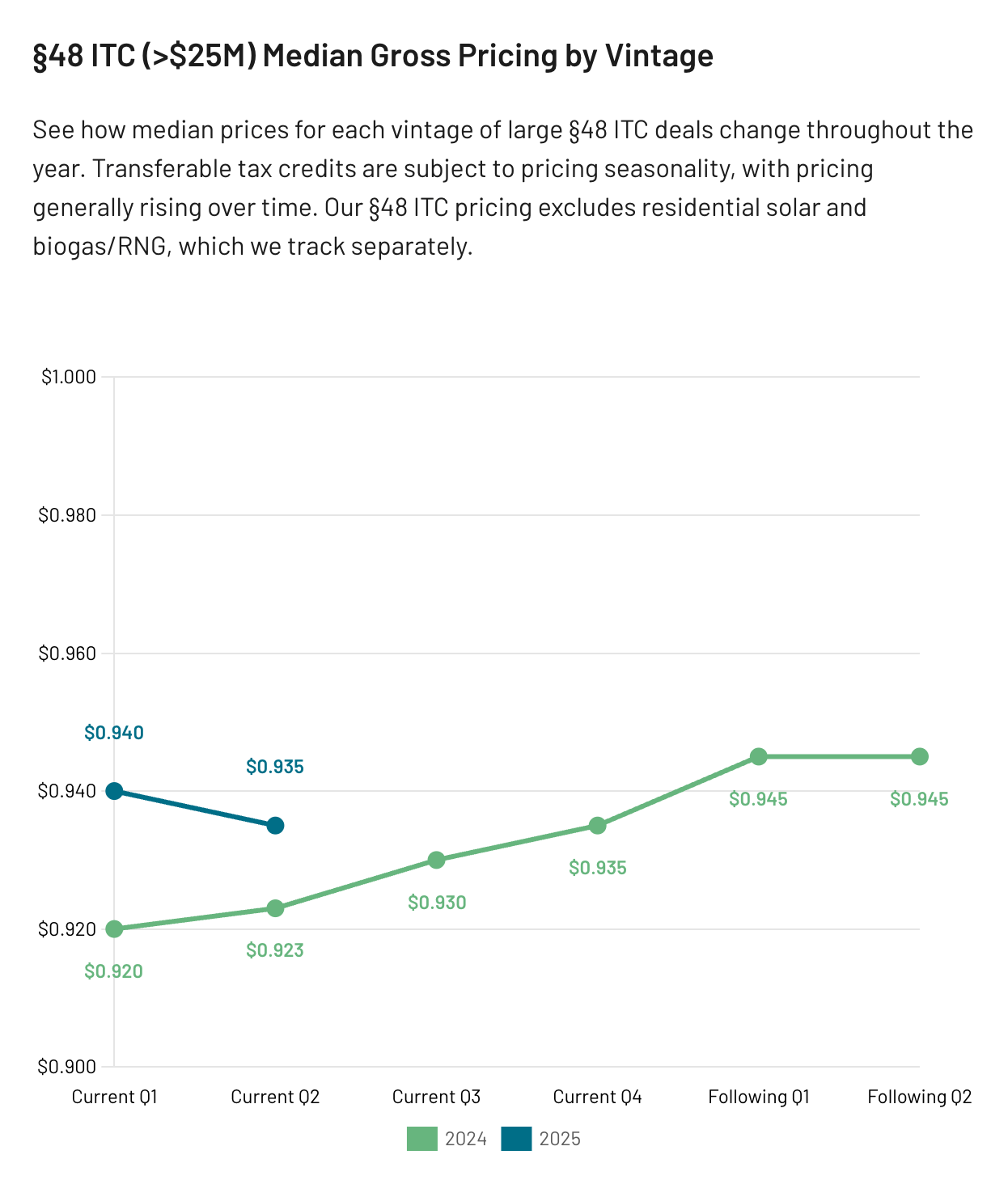

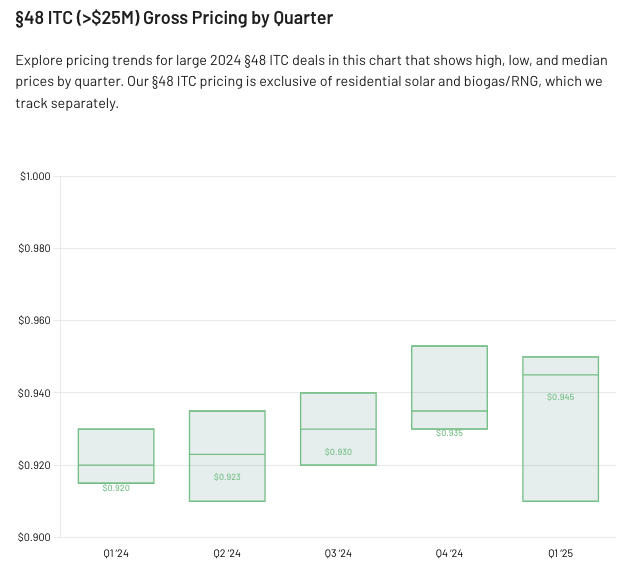

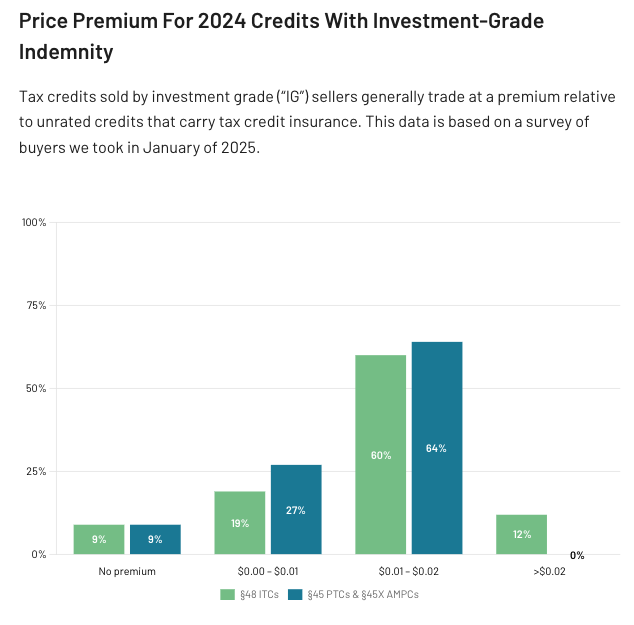

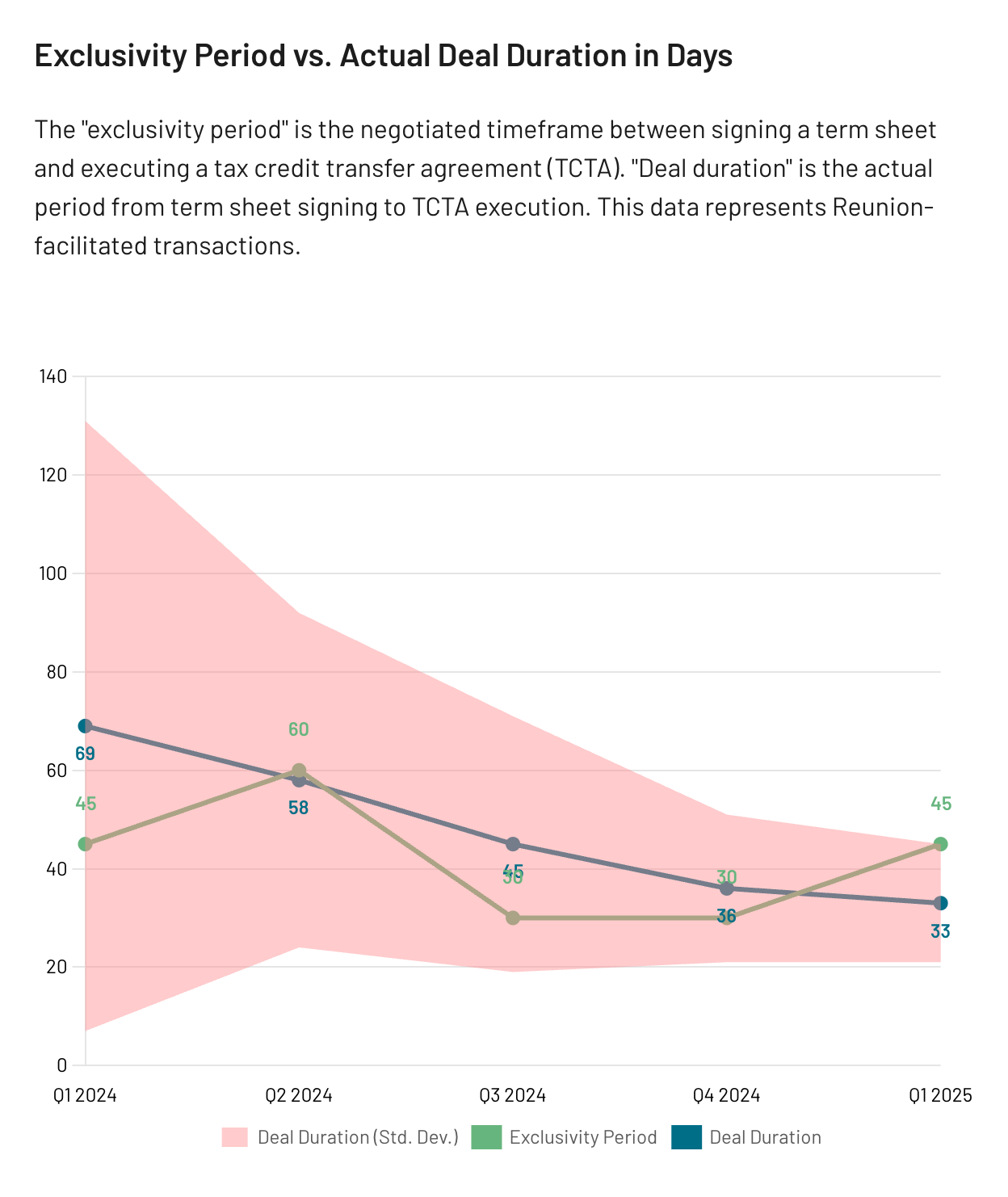

Reunion's Market Monitor Q2 2025 Report

A Q2 2025 review of Reunion's Market Monitor, a market intelligence dashboard built on over 300 verified tax credit transfers.

For Buyers

For Sellers

This is a snapshot of Q2 2025 data. For a real time look at transaction data, access the full dashboard here.

In June, Reunion released Market Monitor, a comprehensive view of transferable tax credit pricing, deal terms, and market dynamics. Based on over 300 transactions and $25B of deal volume, Market Monitor represents a 360-degree view of the clean energy tax credit market. You can watch our release webinar.

Alongside the platform, we are also publishing a quarterly analysis to bring key trends and observations to life.

Key trends

- In the first half of 2025, pricing has softened for 2025 credits relative to last-minute 2024 credits

- Seasonality of tax credit pricing has persisted into 2025

- Pricing dispersion reflects deal- and counterparty-specific nuances

- Premium on Investment Grade Tax Credit Sellers amounts to 1 to 2 cents more per credit

- Increased standardization among key commercial terms

- Buyers of all stripes are in the market

- Nearly 20% of 2024 vintage credits closed in early 2025, driven by fiscal-year filers

- Most Section 48 ITC transactions now include at least one bonus adder

- Domestic content remains limited for Section 45 PTCs

- A growing share of credits, 62% of 2025 ITCs, require PWA compliance

Pricing

Pricing for 2025 credits, relative to 2024 credits, has softened

Pricing for 2024 vintage credits generally trended up and remained elevated through Q1 and Q2 of 2025, reflecting a large number of buyers chasing a relatively small number of opportunities (especially for larger Section 48 ITCs). Conversely, 2025 vintage credits saw some softening in price in early 2025.

Seasonality of tax credit pricing has persisted into 2025

The market exhibits annual seasonality driven by supply-demand imbalances. A relatively small share of buyers were ready to purchase credits earlier in the year without knowing their tax liability; this was exacerbated in 2025 due to early-year uncertainty on how tax laws would change as a result of the reconciliation bill (now known as the OBBBA). In general, buyers willing to enter the market earlier in the year may find more deals to choose from and more advantageous terms and pricing.

Pricing dispersion reflects deal- and counterparty-specific nuances

Median pricing doesn't tell the whole story. Reunion's data shows pricing dispersion, where factors such as delayed payment timing or indemnities from investment-grade entities can lead to higher prices. Section 48 ITCs tend to have greater dispersion due to a broader mix of technologies and counterparties, while Section 45 PTCs trade in narrower bands.

The Premium on Investment Grade Tax Credit Sellers amounts to 1 to 2 cents more per credit

A selection of corporate buyers, many of whom tend to be larger, require an investment-grade counterparty. This translates into higher pricing for tax credits from investment-grade sellers, with tax credits trading for 1 to 2 cents more per credit compared to similar projects that might carry tax credit insurance.

With a finite supply of credits from investment grade sellers. Essentially, these credits are "priced to perfection" due to their scarcity and the perceived lower risk associated with the seller.

Commercial terms

Increased standardization among key commercial terms

Reunion continues to see standardization around key commercial terms — in particular, the buyer fee reimbursement (often $50K-$150K) and exclusivity period (commonly 30-60 days). We believe this is emblematic of a maturing market with increasing efficiency in deal closing.

Markets

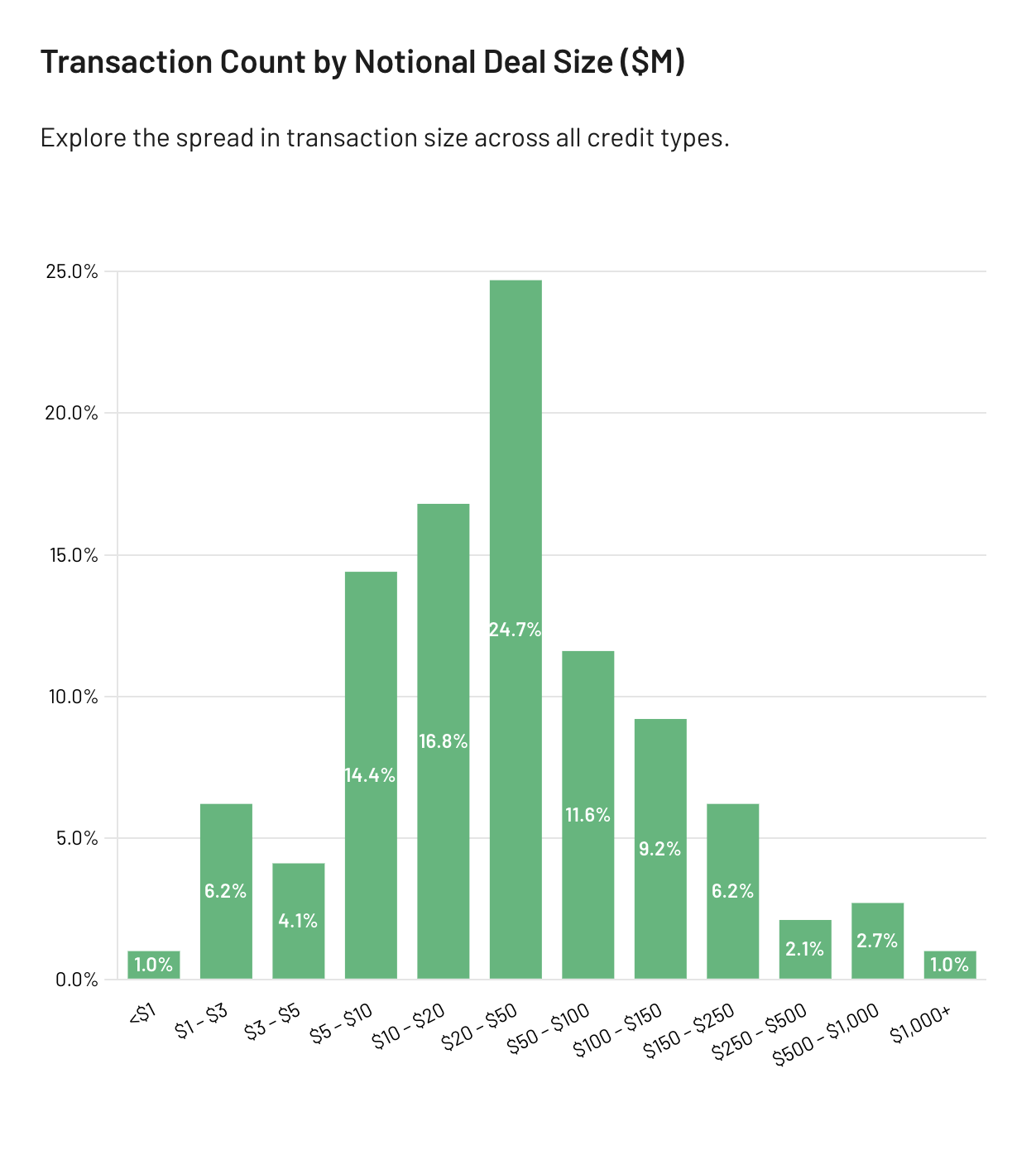

Buyers of all stripes are in the market

The transferable tax credit market demonstrates wide adoption across various buyer industries and supports a diverse range of deal sizes, from a concentration of $20 to $50M transactions, to a notable volume of $250 million+ deals.

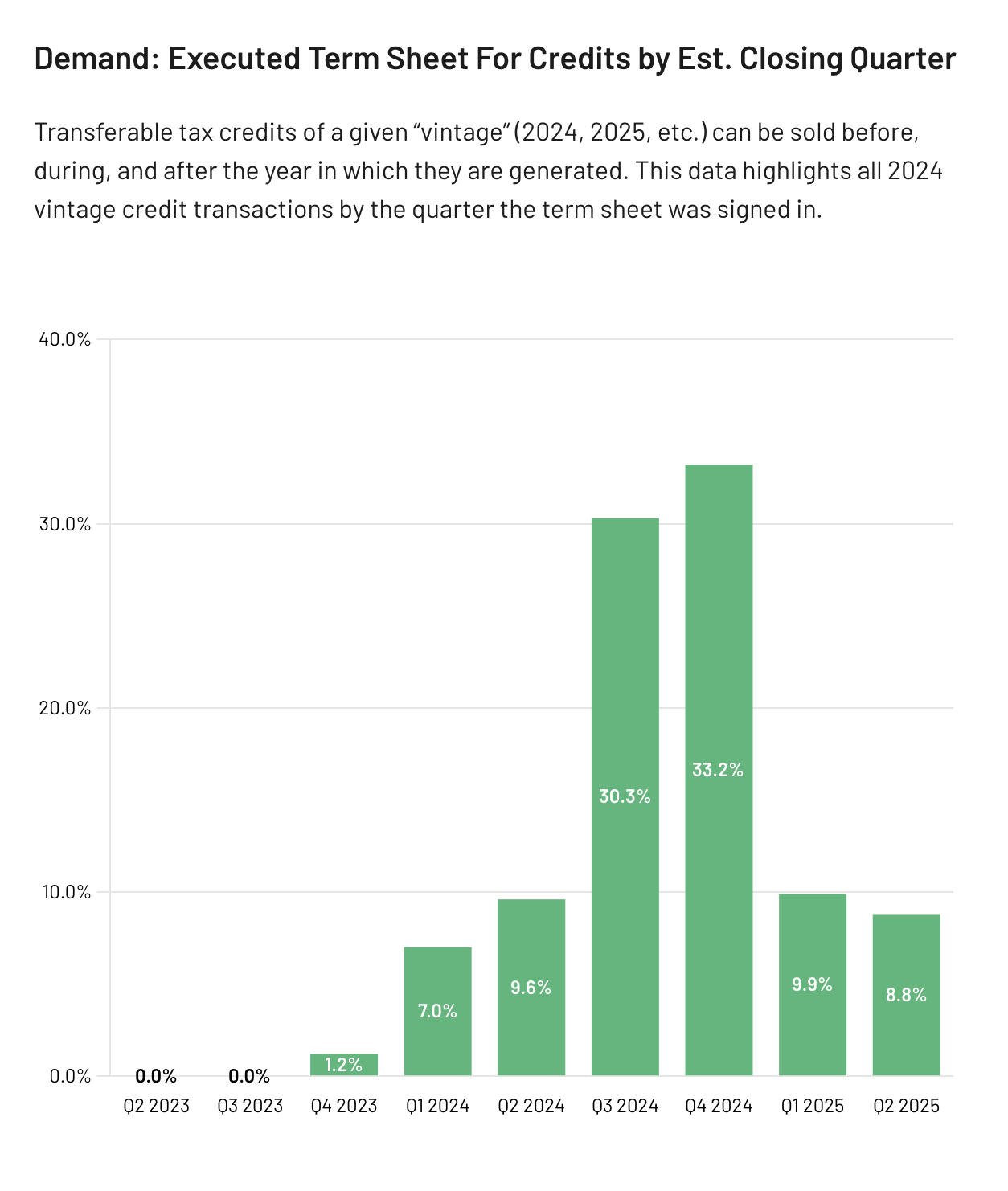

Nearly 20% of 2024 vintage credits closed in early 2025

A significant portion of 2024 vintage credits (nearly 20%) and their associated term sheets closed in early 2025, largely driven by fiscal year-end buyers. This sustained demand, even for prior-year credits, reinforces the importance to buyers of entering the market early.

Credit values

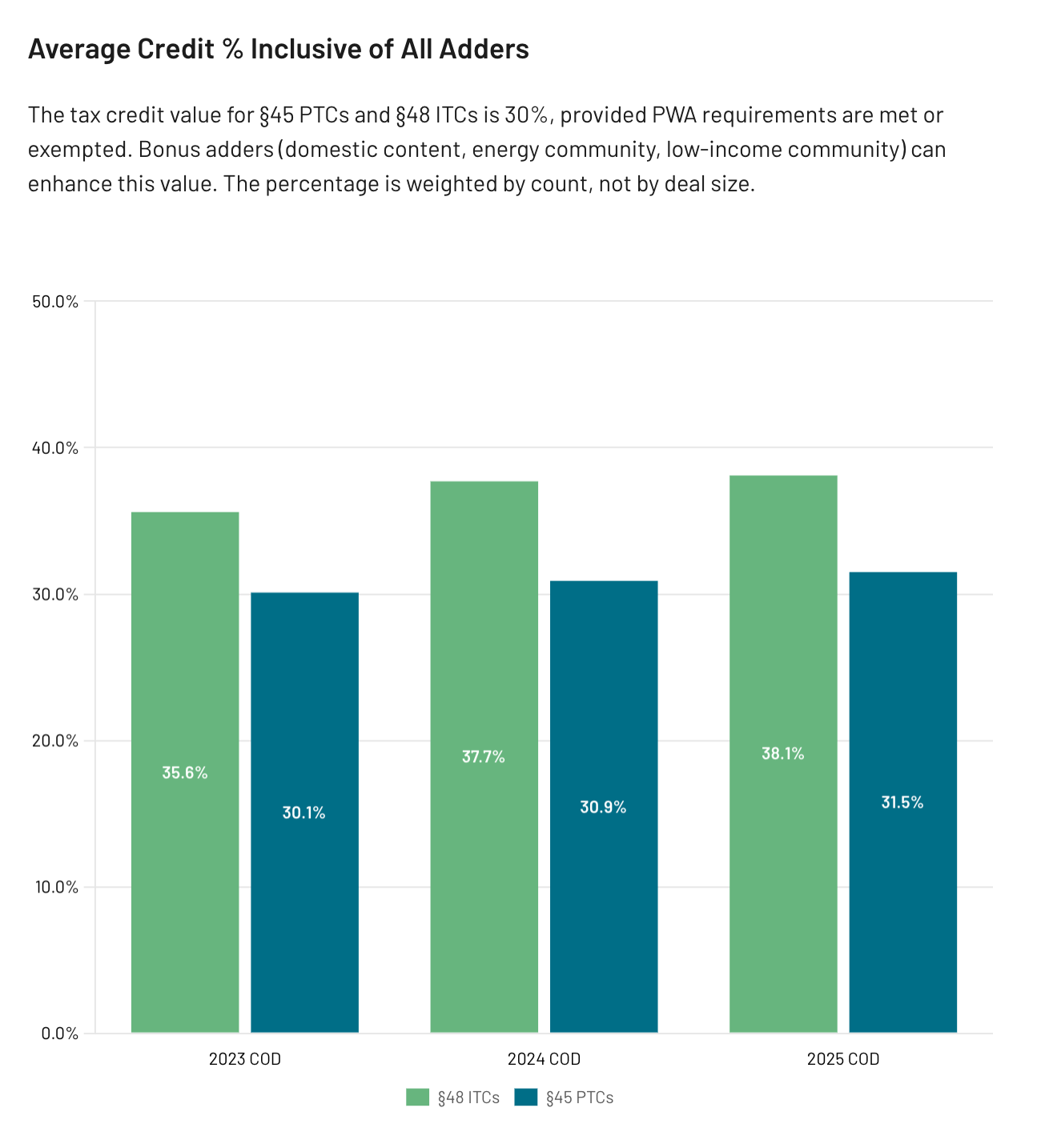

Most Section 48 ITC transactions now include at least one bonus adder

When weighed by dollar value, the average credit value for 2025 Section 48 ITCs is 38.1%. At nearly 40%, the increasing average credit percentage for ITCs implies that most opportunities include at least one bonus credit adder — most commonly energy community, followed by domestic content.

Domestic content remains limited for Section 45 PTCs

Only 2.9% of 2025 Section 45 PTCs — when weighted by dollar value — are claiming the domestic content bonus credit.

Although the elective safe harbor meaningfully increased domestic content adoption for Section 48 ITCs, we have not observed the same flow-through to Section 45 PTCs. This largely stems from “legacy” PTCs that were placed in service before the IRA.

PWA compliance

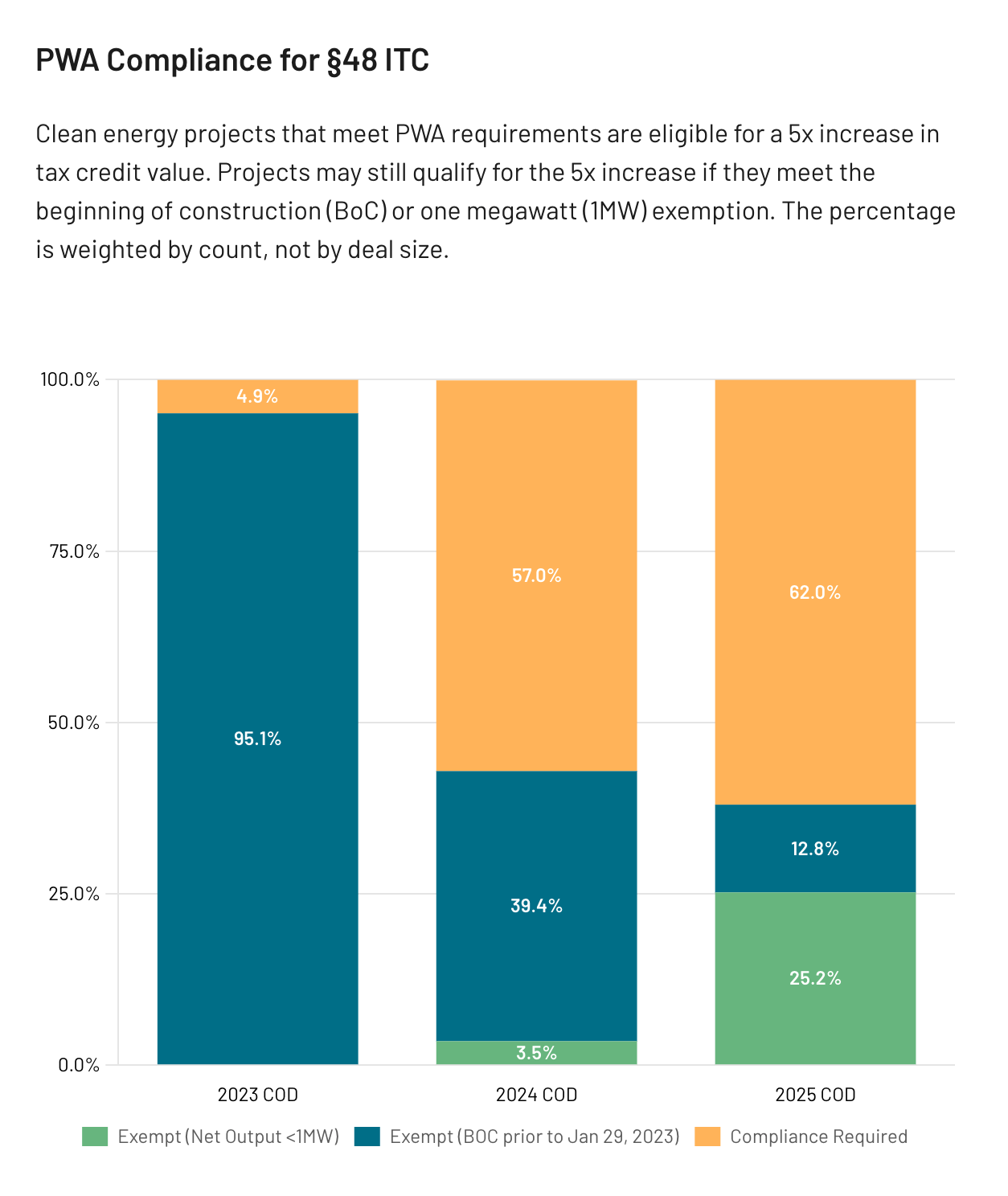

A growing share of credits, 62% of 2025 ITCs, require PWA compliance

PWA compliance is becoming increasingly commonplace for 2025 Section 48 ITCs. However, 25% of 2025 ITCs — Sections 48 and 48E — are exempt from prevailing wage and apprenticeship requirements because of the 1MW exemption. The overwhelming majority of exempt projects are rooftop solar, whether residential (”resi”) or commercial and industrial (”C&I”).

29% of 2025 Section 45 PTCs are PWA exempt — although these credits tend to trade at an “IG-like” premium and clear the market quickly

Approximately 30% of 2025 PTCs by dollar volume are exempt from PWA requirements per the beginning of construction exemption — that is, the projects began construction before January 29, 2023.

Reunion

June 11, 2025

10 terms to negotiate in your next tax credit purchase

No two tax credit transfer agreements are identical - considering these commonly negotiated 10 terms in advance will help deals move quickly once negotiations begin.

For Buyers

For Sellers

Reunion’s breadth of experience includes working with both new and seasoned tax credit market participants. Since the ability to transfer tax credits was only enacted through the Inflation Reduction Act in 2022, some buyers are still getting introduced to the advantages of transferable tax credits as it is written in the Internal Revenue Code §6418 (the Code). Therefore, it is essential for buyers to be aware of the negotiable terms in the transaction, as no two tax credit transfers are the same. Each party (and the underlying asset) involved in the transaction may require bespoke terms and conditions to make the deal close, as is exemplified in this case study of a $200m PTC transfer that met the “audit-ready” diligence requirements of the buyer.

Below are 10 terms that Reunion helps buyers consider when negotiating a tax credit transfer agreement (TCTA). These are not ordered by importance since each buyer’s priorities are particular to them, however, each of the following should be considered when negotiating a transaction:

Payment Terms

The payment terms are primarily composed of the purchase price and payment timing.

- Purchase Price: The purchase price is calculated as a dollar value for every $1.00 tax credit transferred – for instance, $0.935. Buyers and sellers negotiate this term based on the economics of the transaction and key risk factors, such as whether the counterparty is investment grade, what kinds of tax credits are involved, and the total expected volume of the transaction. Read more about the buyer’s perspective for these transactions and how to set the appropriate price.

- Payment Timing: When a transaction closes can significantly influence the negotiated purchase price. Transactions with earlier payments, such as a simultaneous sign and close, are often favored by the seller due to the time value of money. Therefore, the seller may be more open to a lower purchase price. Sometimes the buyer is inelastic on this term and requires that transfer payments align with their quarterly estimated tax payment dates to minimize out-of-pocket spend.

Transaction Cost Reimbursement

Most buyers opt to include a transaction cost reimbursement provision in their tax credit bids. It is common for buyers to ask sellers to reimburse some or all of the transaction costs they incur. This request is often driven by accounting considerations, as most buyers do not want to incur an “above the line” expense to generate a “below the line” tax benefit.

Buyers should first identify the expenses they will incur, such as legal fees for outside counsel or costs for accounting firms providing third-party diligence support. For transfers with subsequent funding milestones (e.g. multiple closing dates), buyers should consider the timing of expenses as well as the amount needed to support subsequent fundings.Buyers must weigh what other impacts this provision could have on the transaction. A reimbursement provision will ultimately decrease the amount of proceeds to the seller, so it could impact the overall economics of the transaction (e.g., smaller tax credit transfers may not support large transaction cost reimbursements) or make the bid less competitive when a seller considers their net proceeds.

Exclusivity

Most of Reunion’s tax credit transfers move from term sheet execution to TCTA signing in under 45 calendar days. During the exclusivity period, both parties are generally incurring costs related to definitive documentation and due diligence. To protect their investment of time, effort, and money, buyers typically request an exclusive right to purchase the credits.

Buyers can negotiate for a fixed exclusivity period when drafting the term sheet and will typically request an extension if the exclusivity period has expired and all parties are working in good faith to close the transaction. Reunion has seen exclusivity periods range from zero to 60 days following execution of the term sheet. A period beyond 60 days is not typical and could signal to the seller that the buyer is not able to close the transaction in a timely manner.

Indemnity Scope

In every tax credit transfer agreement, a buyer will require the seller to indemnify them for the disallowance or recapture of tax credits. Indemnities can be structured in two ways:

- Breach-Based Indemnity: Indemnification for a loss is triggered by a specific breach of a representation, warranty, or covenant.

- No-Fault Indemnity: Indemnification for a loss occurs regardless of whether a contractual breach has happened.

Most indemnities will cover any tax gross-up, interest, penalties, and fees incurred in connection with the loss. For ITC transactions, as further described in the Section 48 ITC Due Diligence Guide, buyers negotiate for indemnity in the case of a recapture event.

Indemnity Seller Cap

Sellers may negotiate for a cap to the amount recoverable through the indemnity clause. Stipulated limitations of liability are often required by larger, institutional sellers. If the seller makes this request, buyers should analyze whether the indemnity limit is sufficient enough to recoup any losses incurred on an after-tax basis (including anticipated damages such as interest, penalties, taxes, and additional expenses needed to enforce the claim).

Reunion has supported transactions with no caps, as well as transactions with caps expressed as a percentage of the face value of the credits or the purchase price of the credits. The former is more common.

IRS Contest Process

In the case of an IRS contest, Reunion sees most transactions include language in the TCTA that dictates which party will be responsible for working through, and leading, the process with the IRS and what rights each party will hold. Buyers should consider how they want this to be managed while reviewing the TCTA. In most cases, the party that is directly involved in the contest with the IRS controls the process at that party’s expense and notifies the other party as needed.

Buyers and sellers may also be required to adhere to any requirements under the insurance policy (where applicable) to preserve and pursue a claim to minimize the amount of tax credits lost.

Change in Law

Due to the uncertain political climate, most buyers have asked for provisions to be included in the TCTA that protect them from any future changes in the Code, or regulations that could impact their ability to utilize any purchased tax credits. A recent focus for buyers has been on language that specifically indemnifies the buyer against changes in law that are retroactive in effect (e.g., tax credits for projects placed in service on or before a retroactive change in law). Buyers may also seek the ability to terminate an agreement if there are changes in law that have a material adverse effect between signing and closing.

Credit Enhancements

When the seller is not investment grade or there are other unique risks in the transaction, the buyer can negotiate for further credit support.

- Guarantor: The primary option is a guarantee from the seller's parent company or another affiliated party. Securing protection from an investment-grade guarantor may result in a higher net credit price if the seller does not have to obtain tax credit insurance.

- Tax Credit Insurance: If the seller cannot provide a suitable guarantor, tax credit insurance is an alternative. The policy limit of liability is typically based on a negotiated percentage of the tax credits' face value. However, all policies have specific exclusions to coverage, including material misrepresentations, inaccuracies or omissions, breaches of transaction documents, recapture that is caused by the seller, fraudulent or criminal conduct, any position taken in tax returns that is materially inconsistent with the covered tax position, and change in law. Additional exclusions may also apply depending on specific circumstances relating to the underwriting of the tax credit.

Step-up Limit

For investment tax credit transactions, project developers commonly sell a project into a partnership where the purchase price is “stepped up” to a fair market value (FMV) that exceeds the developer’s total capital expenditure. These FMVs should be supported by underlying documentation and assessed by a third-party appraiser. Some buyers and insurers have requested a limit to the step-up percentage as a higher step-up may have additional risk in the event of an IRS contest if the step-up is partially or fully disallowed. Recent transactions have allowed for at least a 20% step-up when supported by the facts and circumstances of the applicable transaction.

Diligence Requirements

After the buyer and seller have executed a term sheet, they work alongside their respective counsel and any other third-party assistance, to mitigate concerns around the transaction and underlying tax credits. Most transactions require a standard set of diligence items, which typically extends beyond the minimum documentation requirements under Treas. Reg. Section 1.6418-2(b)(5)(iv). Diligence may include, but is not limited to, third party reports, legal memoranda, and original project documents.

Standard diligence items include:

- Third Party Consultant Reports: Examples include a cost segregation report, fair market value appraisal, independent engineer report, 80/20 analysis, and tax memo, depending on the type of tax credit.

- Legal Memoranda: In some instances, a third-party legal analysis may be required to address specific risks in a transaction, including qualification as eligible technology or qualification for credit adders.

- Original Project Documents: Sellers should anticipate requests to substantiate the tax credits and analyze any potential for recapture. For §48 ITCs and §45 PTCs, this may include executed site control and interconnection documents, as well as offtake, EPC, asset management, and O&M agreements. Photographs or satellite imagery is often used in diligence as well. In instances where a portfolio of distributed generation assets is involved, buyers can request a sampling size that is reasonable given the terms of the transaction. For §45X AMPCs, the documentation involves proof of sales contracts and underlying costs for the eligible technology.

Buyers should consider which diligence items are non-negotiable given the details of the transaction and parties involved. We have seen in recent transactions, buyers and sellers collaborating on mandatory diligence requests and finding a path to resolution. On items that are not imperative, flexibility from buyers has helped transactions be executed within the exclusivity period.

More details can be found in the Transferable Tax Credit Handbook.

Summary

Reunion has seen many recent transactions accommodate the pain points of both the buyer and the seller - especially when backed with well-reasoned requirements. Ultimately, both parties benefit from these transactions moving forward de-risked and well positioned in the market.

If you are interested in buying credits, thinking through which of these terms is important to you will help get ahead of negotiations in your tax credit transfer deal. Then as an informed and prepared buyer, you can move quickly and take advantage of quality tax credits as they become available in the market.

Reunion

June 4, 2025

Hear from Your Peers: Transferable Tax Credits with Hormel & Gallup

Jim Fleming of Hormel and Adam Fritz of Gallup join Reunion's CEO, Andy Moon, for a candid conversation about their experiences as buyers in the transferable tax credit market.

For Buyers

Joined by: Jim Fleming of Hormel and Adam Fritz of Gallup

Reunion hosted a buyer-focused webinar with Jim and Adam, who shared important lessons they've learned in the transfer process, including getting internal buy-in, origination and sourcing investments, deal structure negotiations, and due diligence.

Recording: Transferable Tax Credits With Hormel & Gallup

Key topics

- 0:00 Agenda Overview

- 01:41 Introductions

- 07:45 Impact of House Tax Bill

- 14:35 Gaining Internal Buy-in

- 25:53 Origination and Sourcing Investments

- 31:35 Structuring and Negotiations

- 45:00 Due Diligence and Closing

- 52:00 Final Questions and Advice

Insights from your peers:

- Secure Internal Buy-In Up Front: Align with relevant stakeholders (which often include the CFO, legal, and treasury teams) early on to establish your company's goals and risk tolerance. This internal alignment is crucial for moving quickly and decisively on potential deals.

- Negotiate Beyond Price: While price is top of mind for most buyers, other terms such as a strong seller indemnity and favorable payment timing can be equally important. Buyers also often negotiate for sellers to cover a capped amount of legal and diligence fees.

- Key Buyer Metrics Include Cash Savings, Timing of Payment and Strength of Seller: Buyers noted that the amount of cash savings and resulting impact on ETR was their primary consideration. Timing of payment is also significant to ensure there isn't too large of a "prepayment" on taxes. Finally, partnering with a strong seller is critical in the event there is an IRS challenge down the road.

- Conduct Thorough Due Diligence: Even with a strong seller guarantee, buyers must conduct comprehensive due diligence. Experienced legal counsel, and the right broker / advisor can help streamline the due diligence process and ensure proper risk mitigation.

- Monitor Legislative Changes: Tax credit transfer activity has picked up since the proposed reconciliation bill passed in the House, which gave the market confidence that there will not be a retroactive repeal of credits. However, the proposed bill will also lower tax liability for many buyers, which will impact the volume of credits a buyer can purchase.

Andy Moon

May 19, 2025

The “One, Big, Beautiful Bill” and the implications for corporate taxpayers and the clean energy industry

This new draft tax bill provides short-term stability for clean energy through clearer 2025 tax credit guidance, but creates long-term uncertainty due to accelerated credit phase-outs and complex FEOC restrictions.

For Buyers

For Sellers

NOTE TO READERS: This content is current as of Friday, June 20, 2025. Given current discussions in the Senate, we will post updates here as they become available.

On June 16, the Senate Finance Committee released its much-anticipated draft of the budget reconciliation bill. The proposed Senate bill extends tax cuts from the Tax Cuts and Jobs Act of 2017, while rolling back parts of the Inflation Reduction Act to help cover the cost. This comes on the heels of the House’s version of the bill that passed the floor on May 22, 2025, by a vote of 215-214. After the Senate votes, it will return to the House, which may lead to further changes.

Short-term stability

The proposed Senate bill provides short-term stability, which will result in a meaningful uptick in clean energy transactions throughout the rest of the 2025 and for the next several years.

Since the House bill was passed, we have observed a significant uptick in interest from tax credit buyers. We expect increased activity through the rest of 2025 and for the next 3-5 years, given the proposed Senate bill provides clear guidance that near-term tax credits eligible under the IRA (and associated transfers) will be respected. Most notably:

- Tax credits will not be retroactively repealed for the 2025 tax year.

- Transferability is preserved for all credit types, with the caveat that tax credits cannot be sold to Specified Foreign Entities (SFEs).

- Legacy §45 Production Tax Credits (PTCs) and §48 Investment Tax Credits (ITCs), which began construction before 2025, are not changed.

- Many technology-neutral credits (§45Y or §48E), including energy storage, geothermal, hydropower, and nuclear, remain eligible for the full credit value, as long as construction begins by 2033.

- Wind and solar projects specifically are subject to an accelerated phasedown schedule for projects that begin construction starting in 2026. Credits will be eliminated for projects that begin construction in 2028 and beyond.

- The phasedown is based on the beginning of construction date. Wind and solar developers are rushing to start construction on projects in 2025, which should create a steady pipeline of projects for the next several years (projects have four years from beginning of construction to be placed into service for tax purposes).

- The §45X Advanced Manufacturing Production Credits (AMPCs) phase-down schedule is largely unchanged from the IRA. Components produced and sold through 2029 are eligible for the full credit, with a phase-down starting in 2030. Components produced and sold after 2032 are not eligible for credits. There are several meaningful exceptions:

- The provision relating to the sale of integrated components that are produced and sold after 2026 is repealed, which may impact certain solar component manufacturers.

- Wind components are not eligible for credits if produced and sold after 2027. Critical minerals have a longer eligibility period, with a phasedown in credits starting in 2031.

- Critical minerals produced and sold after 2033 are not eligible.

- There are no changes in the phasedown schedule for the §45Q Credit for Carbon Oxide Sequestration and the §45U Zero-Emission Nuclear Power Production Credit.

- Complex Foreign Entity of Concern (FEOC) restrictions were introduced, which will add significant risks and compliance burdens. However, there are short-term exemptions (e.g., at the project level, FEOC restrictions are intended to apply to projects that begin construction after December 31, 2025).

Assume that the bill becomes law in September 2025, and a project begins construction by December 2025. A project that generates a tech-neutral credit (§45Y or §48E) will qualify for the full credit value, which can be transferred to a third party. We are already seeing a wave of projects rushing to establish start of construction before the end of 2025.

Unrelated to the adjustments in tax credit eligibility, many corporate taxpayers have held off on purchasing 2025 credits due to a lack of certainty regarding their 2025 tax liability. In particular, three outstanding tax policies have disrupted tax planning. The Senate bill proposes the following changes:

- §174 R&D Expenses: Reinstate immediate expensing of R&D costs for tax years from 2025 to 2029

- Bonus depreciation: Reinstate 100% bonus depreciation for property acquired after January 19, 2025, and before January 1, 2029 (a shift from the proposed House bill, which applied to property acquired through January 1, 2030)

- §163(j): Reinstate the more favorable calculation of the limit on the interest deduction under §163(j) for tax years beginning after December 31, 2024, and before January 1, 2030

The proposed changes will lower corporate tax liabilities, which will reduce the volume of credits that certain buyers can purchase. However, increased certainty on tax liabilities will have the overall impact of giving buyers confidence to move forward on tax credit purchases. In 2024, we saw a wave of buyers enter the market in the 3rd quarter of the year when they had clarity on their tax liabilities. We anticipate a similar dynamic this year, with many buyers coming into the market later in the year and competing for a dwindling number of tax credit opportunities.

Medium- to long-term uncertainty

However, the Senate bill creates medium to long-term uncertainty for the clean energy market, due to proposals such as FEOC restrictions and accelerated tax credit phasedowns.

Major changes in the proposed bill include:

- Accelerated phasedown or reduced eligibility of clean energy tax credits, particularly tech-neutral credits (§45Y or §48E) for solar and wind

- Elimination of the credit for wind and solar leased property that would otherwise qualify for the residential credit under §25D

- The clean hydrogen production credit (§45V) is not available for facilities that begin construction after December 31, 2025

- FEOC restrictions, which will be difficult to comply with as currently written and may slow project development due to increased risk.

Summary of proposed tax credit phasedown

Accelerated phasedown for solar and wind

Solar and wind-related credits are subject to an accelerated phasedown, which will impact upcoming project development.

Tech-neutral credits (§45Y and §48E) generally phase down in 2034 and are eliminated by 2036 based on when the project begins construction. However, the proposed Senate bill phases down tax credits for solar and wind on a significantly shorter timeline:

- Projects that begin construction in 2025 receive 100% of credit value

- Projects that begin construction in 2026 receive 60% of credit value

- Projects that begin construction in 2027 receive 20% of credit value

- Projects that begin construction in 2028 or later receive 0% of credit value

As a result, wind and solar developers are rushing to begin construction this year. Projects can establish start of construction through two well-established methods: the physical work test or the 5% safe harbor, after which they have four years to be placed in service. If developers don't start construction by the end of 2025, they will receive a significantly lower (or no) tax credits, which will have the impact of slowing new development from 2026 onward. Segue Sustainable Infrastructure forecasts 122 GW of project cancellations, resulting in $211 billion less investment in the grid as a result of the proposed bill.

There are several other important ways that wind and solar developer manufacturers are impacted by the proposed Senate bill:

- The credit for wind and solar leased property that would otherwise qualify for the residential credit under §25D is eliminated, which will cause developers to shift away from leases

- For §45X credits, wind components are not eligible for credits if produced and sold after 2027. Certain solar component manufacturers will also be impacted by the repeal of the provision regarding integrated components that are produced and sold after 2026, which potentially will limit the ability for manufacturers to stack credits from components that are integrated into larger products

Transferability preserved in most cases

Transferability is preserved, so long as the transferee is not a Specified Foreign Entity.

There was no mention of transferability in the proposed Senate bill, meaning that tax credit transfers will be available for the same duration as tax credits. However, tax credits cannot be sold to Specified Foreign Entities (SFE), which is defined below:

- Meets any of the criteria outlined in Section 9901(6) of the William Thornberry National Defense Authorization Act (NDAA) for Fiscal Year 2021:

- Is designated as a foreign terrorist organization by the U.S. Secretary of State under Section 219 of the Immigration and Nationality Act (8 U.S.C. § 1189)

- Appears on the Treasury Department’s Office of Foreign Assets Control (OFAC) list of Specially Designated Nationals and Blocked Persons

- Has been linked to criminal activity resulting in a conviction, as alleged by the U.S. Attorney General

- Is identified as a Chinese military company

- Is listed due to the Uyghur Forced Labor Prevention Act

- Is named under Section 154(b) of the NDAA for FY 2024 (specifically, paragraphs 1–7 on page 47 of Public Law 118-31)

- Is a foreign-controlled entity, meaning it is owned or influenced (directly or indirectly) by:

- The government of a covered nation (specifically China, Iran, Russia, or North Korea)

- Its agencies or instrumentalities

- Citizens or nationals of a covered nation

- Entities organized or headquartered in a covered nation

- Or any entity controlled by the above (with “control” defined as owning 50% or more of voting shares, capital, or beneficial interest)

Foreign Entities of Concern

The bill includes complex restrictions to avoid benefiting Foreign Entities of Concern. The current draft will be difficult to comply with, potentially causing a slowdown in future clean energy projects. However, we don’t expect significant market disruption in 2025.

Complex Foreign Entity of Concern (FEOC) restrictions will apply to §48E, §45Y, §45Q, §45U, §45X, and §45Z credits to ensure that the benefit of tax credits does not accrue to China, Russia, Iran, or North Korea.

We do not expect significant disruption to the market in 2025. Most PTCs and ITCs currently in the transfer market began construction before 2025 and therefore qualify for the legacy §45 and §48 credits, which are not subject to FEOC rules.

For the newer §45Y and §48E credits, there is a transition period for complying with FEOC rules (e.g., projects that begin construction by the end of 2025 are not subject to FEOC at the project level. Rules to ensure FEOC compliance at the taxpayer level begin in 2026 and become stricter in 2028).

Most concerning for clean energy developers is the annual compliance requirement to ensure that “specified foreign entities” do not benefit from tax credits. There are also payment restrictions to ensure that prohibited foreign entities do not earn a certain amount of dividends, interest, compensation for services, rents, royalties, or similar payments. For §48E credits, these compliance requirements must be tested for 10 years, and any breach results in a full recapture of the §48E credits. A recapture period this long and this challenging to comply with will make it harder to raise financing or sell tax credits from projects that require FEOC compliance. As a result, we expect the clean energy industry to lobby for clarifications and adjustments to the FEOC restrictions.

Conclusion

We expect a strong, continued mobilization from developers, banks, utilities, and corporations to advocate against the early phasedown of tax credits, particularly related to solar and wind, and to create a workable and simplified version of FEOC regulations.

Andy Moon

May 16, 2025

Impact of the “Big, Beautiful Bill” on Clean Energy and Corporate Tax with Keith Martin

A discussion about the proposed impact on clean energy tax credits, transferability, and corporate tax liability. We also outline how the process will unfold as the "Big Beautiful Bill" winds its way through Congress.

For Buyers

For Sellers

Key takeaways from the session:

- Short-term clarity on the ability to transfer tax credits: Repeals were not retroactive, and will give the market stability to move forward on near-term transactions. We expect an uptick in buyer activity for 2025.

- The Senate historically moderates changes proposed by the House: However, four House Republicans declined to support the bill on May 16, and have demanded additional IRA rollbacks.

- The clean energy industry will be focused on clarifying FEOC (Foreign Entity of Concern) restrictions, and extending transferability:

- The proposed FEOC restrictions will be almost impossible to administer, and their complexity will slow clean energy deployment. The Senate is expected to simplify the rules.

- Clean energy developers will rush to start construction to secure FEOC exemption, and preserve ability to transfer credits.

Andy Moon

March 17, 2025

The Road Ahead for Clean Energy Finance with Keith Martin and Jigar Shah

Reunion's Andy Moon hosts a wide-ranging conversation, covering an inside look at the current policy environment and market sentiment, and a big-picture discussion on what’s next.

For Buyers

For Sellers

Reunion's Andy Moon spoke with two of the most insightful voices in clean energy — Keith Martin (Norton Rose Fulbright) and Jigar Shah (formerly of the DOE Loan Programs Office) — for an inside look at the current policy environment and market sentiment, and a big-picture discussion on what’s next.

Recording: The road ahead for clean energy finance

Key topics

- Introductions to Keith Martin and Jigar Shah [00:58]

- Reunion’s report on transferable tax credits in 2025, drawing from in-depth interviews with buyers [03:36]

- Policy and tax updates by Keith Martin [05:40]

- Trends in the clean energy sector, based on Jigar Shah’s experience at the DOE Loan Programs Office [14:23]

- Discussion of trends in nuclear energy [20:00]

- Impact of tariffs on the clean energy industry [22:43]

- Impact of potential changes to the IRA, with a focus on tax credits [26:00]

- Discussion of letter from 21 Republican members of Congress in support of the IRA, and legislative strategies for the clean energy industry [29:58]

- Importance of making voices heard in-district, rather than in DC [31:41]

- How stakeholders can prepare in case IRA tax credits are repealed [36:15]

- How federal agencies including DOE and IRS will be able to operate in the face of cuts from DOGE [37:58]

- Over 90% of new energy capacity in 2024 was clean; why doesn’t the clean energy industry act more dominant? [44:00]

- Most counterintuitive predictions for the next four years in clean energy [47:46]

- Wishlist requests for the Trump administration [52:36]

Denis Cook

February 12, 2025

30C Tax Credit For Alternative Fuel Vehicle Refueling Property

Discover the IRS’s regulations for the 30C tax credit on EV charging infrastructure. Learn about per-item definitions, eligible locations & calculation methods.

For Buyers

For Sellers

On January 16, the Treasury and IRS published Notice 2025-08, which provides additional guidance on the Inflation Reduction Act’s domestic content bonus credit elective safe harbor. The Treasury and IRS introduced the elective safe harbor in May 2024 in Notice 2024-41.

According to the Treasury’s press release, the latest guidance “updates and builds upon the domestic content safe harbor that Treasury and the IRS published in May of 2024 that provides clean energy developers the option to rely on default cost percentages provided by [the] Department of Energy (in lieu of obtaining direct cost information from suppliers) to determine eligibility for the domestic content bonus.”

Notice 2025-08 “reflects improved default values that more closely align with the characteristics and costs of applicable project components and manufactured product components in the marketplace, as analyzed by the Department of Energy.”

Definitions and percentages updated for solar, battery storage, and onshore wind

Solar

Definitions

Notice 2025-08 split the solar PV table into two separate tables:

- PV ground-mount (tracking and fixed)

- PV rooftop (module level power electronics (MLPE) and string)

The guidance also renamed, redefined, and reclassified several applicable project components (APCs) and manufactured product components (MPCs).

Percentages

In addition to updating several existing assigned cost percentages, the guidance added updated assigned cost percentages for PV modules that “incorporate c-Si [crystalline silicon] PV cells and wafers manufactured in the United States.”

These additional cost percentages were added to reflect “the significant cost premium” associated with domestic cells. Depending on the system, the premium for domestic cells can exceed 40%.

Although the applicable percentages for domestic cells increased, the applicable percentages for other manufactured product components MPCs decreased (to keep the total at 100).

Battery storage

Definitions

The guidance made certain adjustments to the characterizations of applicable project components and manufactured product components. For example, a “battery pack” is now a “battery pack/module,” and an “inverter” is now “inverter/converter.” It also provided a number of clarifying definitions.

Cost percentages

The guidance updated assigned cost percentages for manufactured products and manufactured product components for BESS. The updated cost percentages apply to “grid-scale BESS and distributed BESS” projects.

The DOE made the change after collecting data from three different national laboratories instead of a single national laboratory survey, as well as “comprehensive interviews of manufacturers, installers, developers, and owners” of BESS technologies.”

Onshore, or “land-based,” wind

Definitions

The updated table for onshore, or “land-based,” wind includes minor adjustments to the characterizations of applicable project components and manufactured product components. “Steel or iron rebar in foundation,” for instance, has been renamed “steel or iron reinforcing products in foundation.”

Cost percentages

Notice 2025-08 did not change any associated cost percentages for onshore wind. The DOE, “using analysis from the national laboratories, found only minor changes in the component cost data” from Notice 2024-41.

Offshore wind, hydropower, and other technologies remain out of scope

Offshore wind, hydropower, biomass, geothermal, fuel cell, and other technologies remained outside the scope of the elective safe harbor. Therefore, to qualify for the domestic content bonus, these project sponsors must rely on extensive calculations based on actual component costs.

Retrofits qualify for domestic content safe harbor

Section 4 of Notice 2025-08 allows qualifying retrofits to use the updated classifications and cost percentages to qualify for the domestic content bonus credit amount. Wind repowers are a prime example of a retrofit.

Projects must meet the the 80/20 rule and qualify for at least one of four credits, depending on the placed-in-service date:

- PIS after December 31, 2022: §48 ITC or §45 PTC

- PIS after December 31, 2024: §48E ITC or §45Y PTC. These are the IRA’s “technology-neutral credits”

Importantly, any used components retained from an existing facility – the 20 in the 80/20 rule – are assigned a 0% value for calculating domestic content.

Clarity on parking canopy, carport, and floating solar projects

The guidance expanded the definition of ground-mounted solar to include parking canopies and carports (“canopy steel racking structures”) and floating solar (“floating on a body of water”).

Parking canopies and carports are considered fixed-tilt systems, while floating solar can be fixed-tilt or tracker systems.

Relationship to elective, or “direct,” pay

As our team highlighted in a prior update, taxpayers who choose to monetize their tax credits – like the Section 45X advanced manufacturing production credit (AMPC) – through direct pay, may be subject to a “haircut” if they do not meet certain domestic content requirements. These taxpayers may utilize the domestic content safe harbor.

Record-keeping

Taxpayers, including transferable tax credit buyers, who claim the domestic content bonus credit must meet the general recordkeeping requirements under Section 6001 to substantiate that the domestic content requirement has been met.

Timing and future guidance

The updated domestic content tables apply to calculations made on or after January 16, 2025, and the Treasury signaled that they intend to update the safe harbor annually. Taxpayers may utilize the safe harbor tables included in Notice 2025-08 for projects beginning construction up to 90 days after the release of further guidance or after any future modification, update, or withdrawal of the updated elective safe harbor. For a comprehensive assessment of eligibility and compliance, refer to our 45X Due Diligence Checklist, designed to help navigate key regulatory and documentation requirements.

Reunion Accelerates Investment Into Clean Energy

Reunion’s team has been at the forefront of clean energy financing for the last twenty years. We help CFOs and corporate tax teams purchase clean energy tax credits through a detailed and comprehensive transaction process.