Connor Danik

February 20, 2026

Section 45Z Proposed Regulations Are Out — What Changed?

On February 3, 2026, the Department of Treasury and the Internal Revenue Service (IRS) issued proposed regulations for the Clean Fuel Production Credit.

For Buyers

For Sellers

On February 3, 2026, the Department of Treasury and the Internal Revenue Service (IRS) issued proposed regulations for the Clean Fuel Production Credit (§45Z). The proposed regulations were published in the Federal Register on February 4, 2026, and are generally consistent with the prior guidance issued.

Noted below are key changes and additions, as well as clarifying or confirmatory guidance that was issued in the proposed regulations.

Jump to a section:

Sold for use in a trade or business

A taxpayer is eligible for the 45Z credit only if it produces transportation fuel and subsequently sells it to an unrelated person (i) for use by such person in the production of a fuel mixture, (ii) for use by such person in a trade or business, or (iii) such person sells such fuel at retail to another person and places such fuel in the fuel tank of such other person. The proposed regulations confirm that the term “sold for use in a trade or business” includes sales of fuel to an intermediary or reseller. The definitions in Section 3.03(7) and the "Appendix - Draft Text of Forthcoming Proposed Regulations" of Notice 2025-10 previously defined the term to mean fuel sold for “use as a fuel” in a trade or business. After stakeholders raised concerns that this language could prevent sales for resale, the proposed regulations removed the “use as a fuel” requirement from the definition of “sold for use in a trade or business.” The proposed regulations also conforms the definition for “sold for use in a trade or business” with the meaning under Internal Revenue Code Section 162.

Safe Harbor Certificates

The proposed regulations introduce two new safe harbors for substantiating the emissions rate for a transportation fuel as well as substantiation for qualified sales. For non-SAF transportation fuel, taxpayers may substantiate an emissions rate determined under the 45ZCF-GREET model by obtaining a certification in substantially the same manner required for sustainable aviation fuel (SAF) under proposed regulation §1.45Z-5. For qualified sales, taxpayers may obtain from the purchaser a certificate in substantially the same form as described in proposed regulation §1.45Z-4(g)(3)(ii). However, a key requirement is the taxpayer must obtain the certificate from the purchaser prior to or at the time of sale (or, for multiple sales, before or at the first covered sale). In addition, the proposed regulations state the Purchaser agrees to provide the person liable for tax with a new certificate if any information in the certificate changes.

Related Party Sales

The proposed regulations adopt a broader related-party “look-through” rule. Under Notice 2025-10, a taxpayer that is a member of a consolidated group is treated as selling fuel to an unrelated person if another member of the group (the related person) ultimately sells the fuel to an unrelated person. Under the broader related-party rules, a taxpayer that is not a member of a consolidated group is also treated as selling fuel to an unrelated person if and when a related person sells the fuel to the unrelated person.

Energy Attribute Certificates & Incrementality

Certain taxpayers may purchase energy attribute certificates (EACs) such as renewable energy certificates (RECs) to reduce their carbon intensity score and resulting emissions rate. The proposed regulations confirm that when incorporating EACs into the 45ZCF-GREET model, rules similar to final regulation §1.45V-4(d) apply. When applying the rules for purposes of the 45ZCF-GREET-Model, the facility is considered placed in service in the first taxable year it produces transportation fuel. The proposed regulations require the EAC-generating facility (or if the EAC facility uses carbon capture and sequestration technology) to have a commercial operations or placed in service date no more than 36 months prior to the first day of the taxable year in which the 45Z facility first produced transportation fuel.

Emissions Rate Table

The proposed regulations clarify that the applicable emissions rate table establishes the emissions rate for a fuel if the emissions rate table includes both the type and category of that fuel. The applicable emissions rate table for a taxpayer is the first publicly available emissions rate table that is in effect during the taxpayer's taxable year of production. However, if an allowed methodology is updated with respect to an included type or category of fuel and is publicly available after the first day of the taxable year of production (but still within such taxable year), then the taxpayer could choose to treat such updated version as the most recent version of such methodology. If an emissions rate table does not initially include a type or category of fuel but an allowed methodology is updated to add such type or category during the calendar year, then that fuel type or category will be considered included in such emissions rate table, and an impacted taxpayer must use this version as its the first publicly available version that includes its type and category of fuel.

Facility Ownership

The proposed regulations confirm the taxpayer is not required to own the qualified facility and credit eligibility is tied to the production of transportation fuel at a qualified facility and subsequent qualified sale.

Timing of Sale

The proposed regulations confirm that production of a transportation fuel may occur in a prior taxable year than the taxable year in which the qualified sale of the fuel occurs, but that a qualified sale may not occur before the date the fuel is produced.

Double Crediting

Code §45Z(d)(5)(A)(iv) states transportation fuel means a fuel which “is not produced from a fuel for which a credit under this section is allowable.” The proposed regulations clarify that the first transportation fuel in the production chain qualifies for the §45Z credit. However, a fuel could still qualify for the §45Z credit if its production process uses a transportation fuel solely as a process fuel or other non-primary-feedstock input.

Feedstock

The proposed regulations confirm that transportation fuel produced after December 31, 2025, must be exclusively derived from a feedstock that was produced or grown in the United States, Mexico, or Canada.

Negative Emissions Rate

Except for transportation fuel in which its primary feedstock is derived from animal manure, the proposed regulations confirm that the emissions rate may not be less than zero for any transportation fuel produced after December 31, 2025.

Indirect Land Use

The proposed regulations confirm that the emissions rate should exclude any emissions attributed to indirect land use change for transportation fuel produced after December 31, 2025.

Production

The proposed regulations clarify that the term production must involve substantial processing by the producer and does not include instances in which a person engages in minimal processing such as creating a fuel mixture or otherwise engaging in activities that do not result in a chemical transformation. For example, this definition of production would exclude any person that removes conventional or alternative natural gas (CANG) from a pipeline, compresses it further after removal, and then sells such further compressed CANG; compression of CANG that is already interchangeable with fossil natural gas would also not meet the proposed definition of production.

Carbon Capture Equipment

The proposed regulations confirm carbon capture equipment will be considered a part of the qualified facility if the equipment contributes to the lifecycle GHG emissions rate of the transportation fuel, which includes emissions from all stages of the fuel’s production and use, including feedstock production and transportation, fuel production and distribution, and use ofthe finished fuel.

Undenatured Ethanol

There was an open question if undenatured ethanol would qualify as transportation fuel as the previous guidance only referenced denatured ethanol. The proposed regulations clarify that undenatured fuel ethanol that meets the qualifications of ASTM D8651 for blending with gasoline and that has an emissions rate that is not greater than 50 kilograms of CO2e per mmBTU meets the definition of non-SAF transportation fuel.

Suitable Use

Code §45Z(d)(5)(A)(i) specifies transportation fuel means a fuel which “is suitable for use as a fuel in a highway vehicle or aircraft.” The proposed regulations clarify that actual use as a fuel in a highway vehicle or aircraft is not required.

Written or electronic comments must be received by April 6, 2026 and a public hearing will be held on May 28, 2026. Taxpayers may rely on the proposed regulations as long as they rely on them in their entirety and in a consistent manner.

Katherine Westcott

February 19, 2026

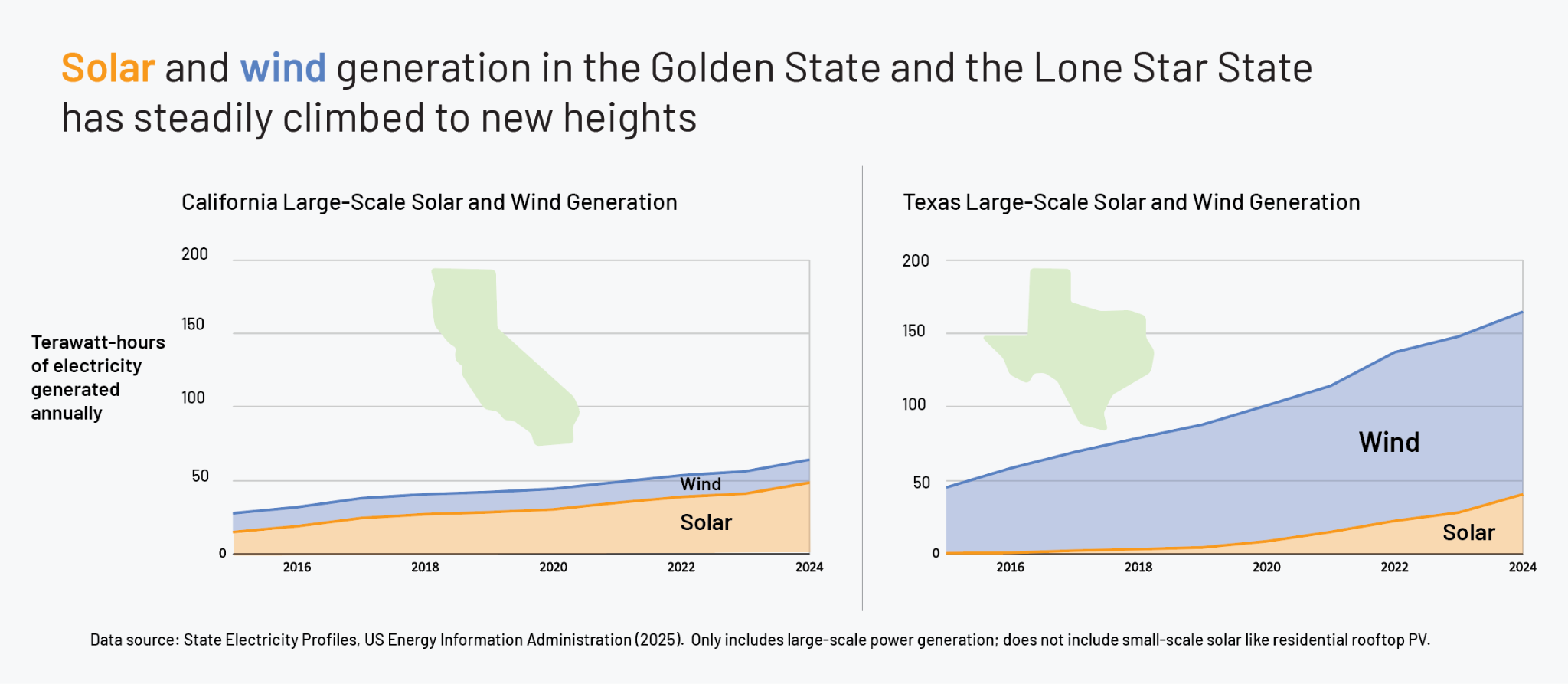

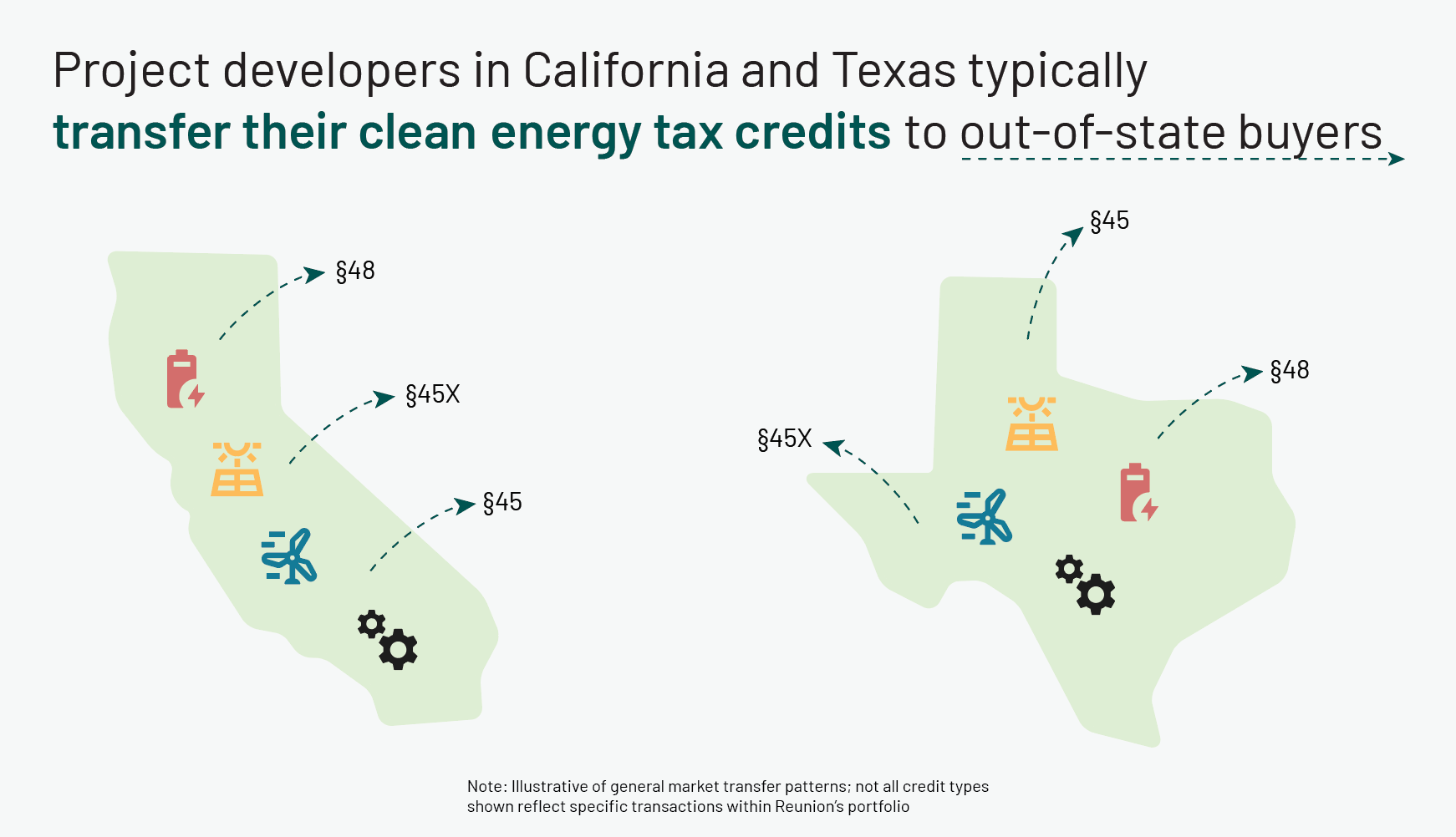

Footnote of the Week: California and Texas have a Common Export — Transferable Energy Tax Credits

We calculate that in more than 90% of cases, project developers and manufacturers in California and Texas ultimately transferred their tax credits to out-of-state buyers.

For Buyers

For Sellers

When it comes to clean energy in America, California and Texas are a central part of the story. The Golden State leads the nation in installed solar power, while the Lone Star State claims second place. Meanwhile, Texas produces far more wind power than any other state. The charts below track the remarkable year-on-year growth in electricity production from large-scale solar and wind in the nation’s two most populous states. (California’s vast adoption of rooftop solar isn’t presented here, but tells a similar growth story.)

This expansion of renewable power has occurred alongside the rise of other innovations in these states – including energy storage and manufacturing of clean energy components (e.g., solar modules and battery cells).

Reunion’s portfolio of work has included numerous clean energy deals in California and Texas – ranging from wind turbines to fuel cells to batteries. Since these projects generate transferable tax credits, we were curious to what degree these credits have been transferred to in-state entities versus out-of-state entities.

We calculate that in more than 90% of cases – across many technology types and deal types (§45 production credit, §45X manufacturing credit, and §48 investment credit) – project developers and manufacturers in California and Texas ultimately transferred their tax credits to out-of-state buyers. We inferred buyers’ location from the address of their corporate headquarters. (Note: Our assessment makes an allowance for the reality that a portion of Californian and Texan buyers acquire in-state credits in a manner that is neither visible to nor transacted via Reunion’s platform.)

The frequent export of tax credits may seem surprising at first glance for California and Texas, given that many Fortune 1000 companies are headquartered in those states and likely have the tax appetite to purchase transferable credits. However, the interstate movement of these tax credits is a positive validation of their transferable nature – which was designed to accelerate the deployment of clean energy nationwide, and is making good on that promise through a geographically flexible framework.

Katherine Westcott

February 5, 2026

Footnote of the Week: Among Insured Tax Credit Deals, Many Have Coverage Levels of 110% or Higher

For transactions that include insurance, our data reveals that the Limit of Liability often exceeds the face value of the tax credit.

For Buyers

For Sellers

In discussions of energy tax credit transfers, much of the focus goes to headline numbers like pricing, deal sizes, and types of credits. A less discussed element that can make or break a deal is tax credit insurance. The demand for tax credit insurance, which is designed to protect the value of tax credits in the event of an IRS challenge, has grown significantly since the start of transferability.

Since Reunion began facilitating tax credit transfers in 2023, about 40 percent of our transactions have included tax credit insurance coverage. As shown in the colored bars below, most of this insurance coverage has had a Limit of Liability equal to or greater than 100%. Conversely, the black bar represents the roughly 60 percent of deals that did not include insurance, suggesting cases in which the tax credit seller could provide a sufficiently strong indemnification, or the parties were comfortable with the risk-reward of the credits being transferred.

The pattern of Limits of Liability commonly exceeding 100% is noteworthy, and implies that many tax credit buyers want protection from second-order risks such as penalties and legal fees that could arise from a disallowance or recapture. To gauge the upper range of these Limits of Liability, we dug into the tax credit type that we’ve seen insured most frequently: §48 investment tax credits.

For §48 transfers, the Limits of Liability have pushed markedly higher than face value – with a little over half of insured deals hitting 110% or higher, and multiple deals establishing Limits of Liability greater than 130%. (The small share of deals with a liability limit below 100% are primarily distributed or residential energy assets; this coverage is designed to support a partial loss, rather than a less likely portfolio-wide loss event.)

While tax credit insurance isn’t warranted on every deal, it plays an important role in enabling tax credit transfers among risk-sensitive buyers, especially when the seller is not investment grade. Our analysis suggests that relatively high Limits of Liability are supported by the market, and may give buyers access to a wider range of tax credit opportunities.

Denis Cook

January 8, 2026

ASU 2023-09 should highlight adoption of IRA clean energy tax credits

ASU 2023-09, Improvements to Income Tax Disclosures, requires public and private companies to provide a more detailed tax rate reconciliation in their financial statements. Participation in the transferable clean energy tax credit market should become more clear.

For Buyers

For Sellers

Overview of ASU 2023-09

Accounting Standards Update (ASU) 2023-09, Improvements to Income Tax Disclosures, represents the FASB’s latest effort to modernize and enhance income tax disclosures under ASC 740, with a clear emphasis on improving transparency around effective tax rate drivers and cash taxes paid.

For corporate tax professionals, the update is less about changing tax accounting and more about significantly expanding what must be explained – and supported – in the tax footnote.

At its core, 2023-09 requires companies, public and private, to provide a more robust and structured explanation of why their effective tax rate differs from the statutory federal rate. The rate reconciliation must now be presented in a tabular format that includes both dollar amounts and percentages, and reconciling items must be categorized using prescribed groupings such as state and local taxes, foreign tax effects, tax credits, valuation allowance changes, and changes in tax laws.

When reconciling items exceed a quantitative threshold – generally 5.0% of the tax at the statutory rate – further disaggregation is required, often by nature or jurisdiction. The result is a more decision-useful, but also more data-intensive, reconciliation.

When do the disclosure updates go into effect?

ASU 2023-09 applies to public business entities (PBEs) and non-PBEs. Simplistically, a PBE is a public company, while a non-PBE is a private company.

The new requirements within ASU 2023-09 go into effect at different dates, depending on the type of entity:

- PBEs: Annual periods beginning after December 15, 2024 – generally, calendar year 2025

- Non-PBEs: Annual periods beginning after December 15, 2025 – generally, calendar year 2026

Impacts on transferable tax credit investments

ASU 2023-09 does not change the accounting for transferable tax credits, but it will make their financial statement impact more visible through enhanced income tax disclosures.

Most notably, tax credits that materially reduce tax expense will need to be more clearly reflected in the effective tax rate reconciliation. Under the new standardized categories and quantitative thresholds, significant transferable credits are likely to be disclosed as a separate reconciling item rather than being aggregated within broader “credits” or “other” categories, increasing transparency around their role in lowering the effective tax rate.

The new income taxes paid disclosure also affects companies that utilize transferable credits. Because these credits often reduce cash taxes owed, companies may report low or minimal taxes paid in certain jurisdictions. ASU 2023-09 requires income taxes paid, net of refunds, to be disaggregated by federal, state, and foreign jurisdictions, with separate disclosure for significant jurisdictions, making the disconnect between tax expense and cash taxes paid more apparent.

Finally, while the ASU is disclosure-focused, it may drive additional documentation and controls around transferable credits. Companies should expect greater scrutiny of the nature, materiality, and sustainability of tax credit investments, as well as more robust explanations in the tax footnote regarding how those credits affect both the effective tax rate and cash tax profile.

Sample income tax disclosure

ASU 2023-09 includes a “sample rate reconciliation between income tax expense (or benefit) and statutory expectations.”

Companies that have disclosed a transferable tax credit purchase

Reunion maintains a list of public companies that have disclosed a transferable tax credit purchase through an SEC filing. We invite you to request access to the evolving list.

Alex Melehy

December 29, 2025

What Are the Prevailing Wage and Apprenticeship (PWA) Requirements for Clean Energy Tax Credits?

The IRA's Prevailing Wage & Apprenticeship (PWA) requirements are the gateway to the full 5x clean energy tax credit multiplier. Projects that comply unlock credits worth five times the base rate; those that don't forfeit up to 80% of their potential value.

For Sellers

To create a robust market for well-paying clean energy jobs, the Inflation Reduction Act (IRA) radically transformed the economics of clean energy project development by introducing Prevailing Wage and Apprenticeship (PWA) requirements.

For developers, EPCs, and tax equity investors, PWA compliance is not just an administrative checklist—it is the key to unlocking project viability. Projects that comply with PWA requirements receive a tax credit that is five times greater than the base rate. Conversely, failing to meet PWA standards means forfeiting up to 80% of a project's total potential credit value.

Here is the definitive breakdown of what PWA compliance entails, which tax credits are impacted, and the specific thresholds developers must navigate.

The Two Pillars of PWA

PWA is divided into two distinct components: prevailing wage requirements and apprenticeship requirements.

1. Prevailing Wage Rules

All laborers and mechanics employed by the developer, contractors, or subcontractors must be paid a minimum prevailing wage specified by the U.S. Department of Labor (DOL). Prevailing wages must be paid during the construction of the facility, as well as during any alteration or repair work for a set number of years after the project is Placed in Service (PIS) (the number of years depends on the credit type**)**. It is important to note that workers do not have to be paid prevailing wages for basic maintenance work, which is “routinely scheduled and continuous or recurring.” Examples of basic maintenance are regular inspections of the facility, regular cleaning and janitorial work, regular replacement of materials with limited lifespans such as filters and light bulbs, and the calibration of any equipment.

2. Apprenticeship Requirements

The apprenticeship rules fall into three strict categories:

- Labor Hours: A specific percentage of total construction labor hours must be performed by qualified apprentices. For projects beginning construction in 2024 or later, this requirement is 15% (compared to 12.5% for projects started in 2023).

- Ratio Requirement: Contractors must adhere to daily apprentice-to-journeyworker ratios as prescribed by the associated registered apprenticeship program (the program that apprentices are sourced from).

- Participation: Any contractor or subcontractor employing four or more laborers or mechanics must hire at least one qualified apprentice.

Crucially, apprenticeship requirements do not apply after a facility has been placed in service. Post-PIS compliance applies only to prevailing wages for alterations and repairs.

Which Credits Are Subject to PWA?

Of the 11 clean energy tax credits eligible for transfer, 10 are subject to PWA requirements. The sole exception is the §45X Advanced Manufacturing Production Credit, which is entirely exempt from PWA rules.

PWA Exemptions: The BoC and 1 MW Thresholds

There are two primary ways a project might be exempt from PWA requirements entirely:

- Beginning of Construction (BoC): Projects that successfully established beginning of construction before January 29, 2023, are strictly exempt from PWA rules, except for §48C and §45Z credits.

- The 1 Megawatt (MW) Threshold: Under §45 and §48 (and their tech-neutral replacements, §45Y and §48E), projects with a maximum net output of less than 1 MW (measured in alternating current) are automatically exempt from PWA.

Quick Reference: PWA Duration by Tax Credit Type

Depending on the tax credit, prevailing wage requirements extend well into the operational life of the asset.

Because retroactive PWA compliance is exceptionally difficult and expensive, clean energy developers and EPCs must implement structured tracking from day one. By utilizing purpose-built compliance software and subject matter experts, developers can automatically flag noncompliance, cure underpayments, and secure bankable compliance reports that protect their 5x credit multiplier.

Denis Cook

December 10, 2025

Reunion's Q3 2025 Transferable Tax Credit Pricing and Markets Update

Reunion’s Q3 Market Monitor print highlights moderate tax credit pricing declines, but continued market maturation

For Buyers

For Sellers

Reunion recently released our Q3 Market Monitor update, including forward-looking pricing estimates through Q4 of this year.

Overall, our data highlights two seemingly divergent trends: (1) softened demand for 2025 tax credits alongside (2) increased market maturity and liquidity.

To better understand this dynamic, this note examines six key trends from our data:

- Pricing: 2025 tax credit prices have declined compared to 2024 levels, primarily due to the OBBBA

- Market dynamics: Sections 45U and 45Z are becoming increasingly popular production credits

- Transaction timing: 10% of 2024 tax credit transfers closed in Q3 2025

- Prevailing wage and apprenticeship (“PWA”): Credits that are PWA exempt because of beginning of construction (“BoC”) exemption are vanishingly rare

- FEOC: FEOC will become a key purchase consideration, with upward pricing for credits with low FEOC risk

- Credit adders: Adoption of bonus credit adders continues to expand for ITCs, but remains muted for PTCs

Pricing

2025 tax credit prices have declined compared to 2024 levels

Across virtually all credit types and deal sizes, 2025 pricing declined relative to 2024 levels. This trend has been particularly pronounced in Q3 and Q4. In 2024, prices rose from Q3 to Q4 as buyers competed for increasingly limited supply. In 2025, the trend reversed, with pricing generally softening over the same period.

Investment-grade (“IG”) supply continues to command a premium – ITCs from IG sellers, for example, continued to trade one to three cents above these median levels in late 2025.

*Section 48 ITC pricing is exclusive of residential solar and biogas. Reunion maintains separate pricing series for these technologies.

The following chart compares estimated Q4 2025 to actual Q4 2024 data. This year’s Q4 data is based on deals closed through November and terms sheets executed through the publication date of this note.

*Section 48 ITC pricing is exclusive of residential solar and biogas. Reunion maintains separate pricing series for these technologies.

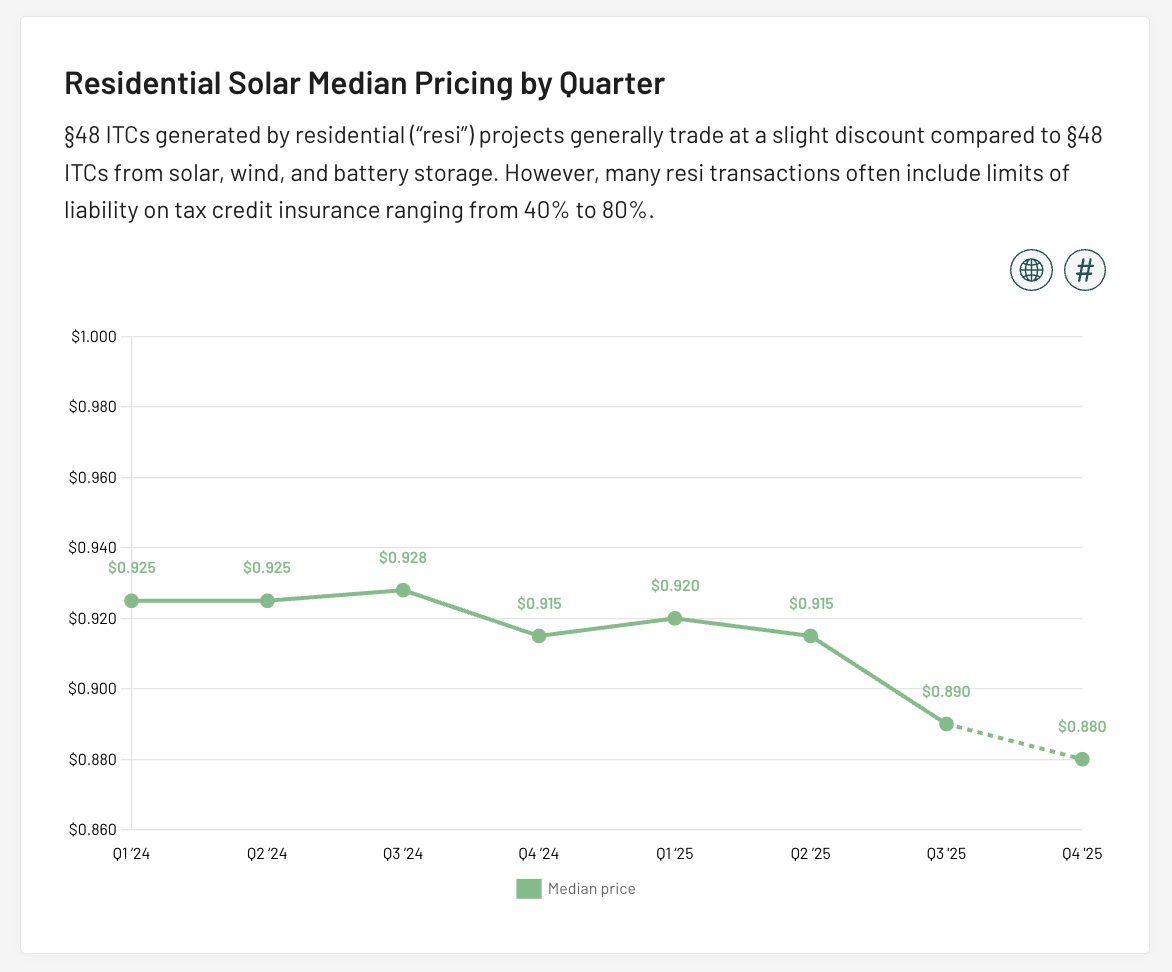

Residential, or “resi,” solar experienced marked price declines throughout 2025 as well. (Reunion maintains separate pricing series for ITCs from resi solar and biogas. We do not include resi and biogas deals in our market-wide Section 48 ITC pricing above.) Looking across 2024 and 2025 vintages, median prices fell from $0.928 in Q3 2024 to an estimated $0.88 in Q4 2025.

When understanding resi prices, it's important to recall that buyers and sellers often negotiate the limit of liability ("LOL") on resi tax credit insurance policies, which flows through to headline pricing. A major resi solar developer, for example, offered a further discount of two cents for an LOL of 40% versus 100%.

While “headline” declines in prices have been modest on a percentage basis, the flow through to cash tax savings has been significant

A corporate taxpayer who purchased a $50M tranche of Section 48 ITCs Q3 2024 and am equivalent $50M tranche of Section 48 ITCs in Q3 2025 would have benefited from an additional $500,000 in cash tax savings – a 14.3% increase.

Tax credit pricing declines in 2025 have largely been driven by impacts of the OBBBA

In the months leading up to the Bill’s passage on July 4, the tax credit market slowed as buyers hesitated to make meaningful commitments without clarity on the final legislation. Many feared that 2025 tax credits might be retroactively repealed and chose to wait for assurance that existing credits would be respected before proceeding with transactions.

The Bill provided clarity that both current- and future-year tax credits will be respected, but the OBBBA itself had a significant downward impact on corporate tax liabilities. Dozens of corporations that were expecting $50M or $100M+ in tax liability no longer had the appetite to purchase 2025 credits.

Today, many companies are still working to understand how OBBBA will affect their final 2025 tax liability – and have delayed purchasing credits as a result.

We expect lingering OBBBA-related impacts on 2026 tax liabilities. As of the publication of this note, Reunion is conducting our year-end tax credit buyer survey, and early feedback suggests that corporations are anticipating reduced 2026 tax liabilities of 10% to 30% against an assumed “non-OBBBA” baseline. Varying degrees of impact tend to cluster in sectors that are particularly sensitive to tax law changes. We’ll publish our year-end buyer report in early 2026.

Although 2026 aggregate demand may be down compared to this non-OBBBA baseline, we are seeing a significant number of taxpayers moving early on 2026 credits. These taxpayers generally fall into two camps:

- Strategic: Companies proactively seeking investments over $50M

- Opportunistic: Companies seeking investments with outsized discounts

We will incorporate pricing for 2026 tax credits in our Q1 2026 Market Monitor release.

Market dynamics

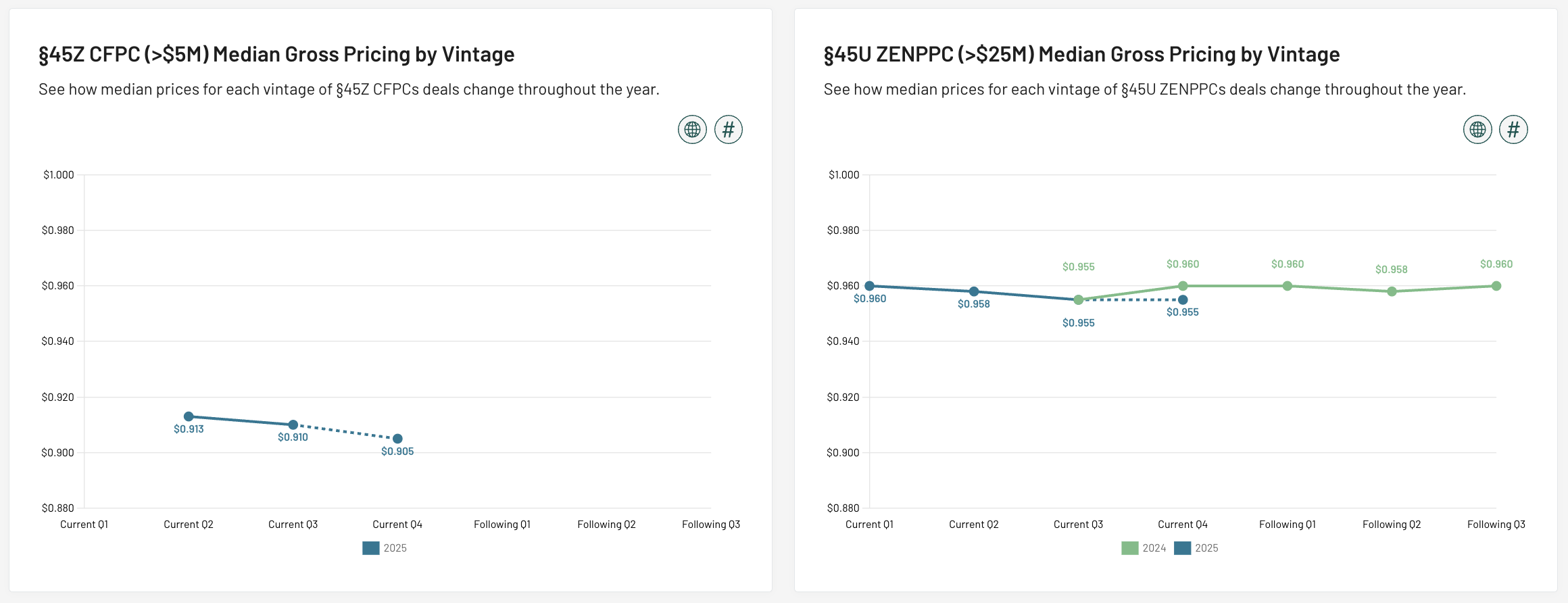

Section 45U nuclear and Section 45Z clean fuels are becoming increasingly popular production credits

In the second half of 2024, a handful of Reunion’s corporate clients explicitly prioritized Section 45U zero-emission nuclear power production credits (“ZENPPCs”). However, the majority of production credit-focused buyers focused on Section 45 PTCs.

As we approach the end of 2025, we have observed that many production credit-focused companies now view 45U ZENPPCs and 45 PTCs with roughly equivalent interest. From a pricing perspective, 45U nuclear credits are among the most stable.

A similar pattern is emerging around Section 45Z clean fuel production credits (“CFPCs”). An increasing number of corporate buyers are actively targeting 45Z credits due to two key factors:

- Risk/return: Section 45Z clean fuel credits are trading in the high $0.80s to low $0.90s, depending largely on the purchase size, presence of tax credit insurance, and the seller’s financial strength. Although this pricing generally aligns with Section 48 ITCs, Section 45Z CFPCs are not subject to recapture.

- General business credit (“GBC”) ordering: Tax credit carrybacks have become more popular, and an effective carryback strategy must account for the credit-ordering rules reflected in IRS Form 3800. Compared to Section 48 ITCs, Section 45Z CFPCs are more advantageous for a carryback from a credit ordering perspective.

To reflect this growing interest, we are now publishing pricing series for both 45U and 45Z credits. Our 45U pricing goes back to 2024, while 45Z begins in 2025 (when the credit first became available).

Although demand for 45Z credits is growing, prices have moderated slightly throughout 2025. We believe this reflects supply dynamics: since the 45Z credit only became available this year, a preponderance of sellers entered the market in the latter half of this year, generally offering full-year tranches of 2025 credits.

Looking ahead to 2026, we expect, and have already begun to see, 45Z deals structured around quarterly payments, akin to many Section 45 PTC transactions. Strips should become increasingly common, too.

The Treasury and the IRS have not yet issued final guidance for either of these credits, though this has not been a gating factor for most buyers. 45Z, in fact, is among the credits that received favorable treatment under the OBBBA.

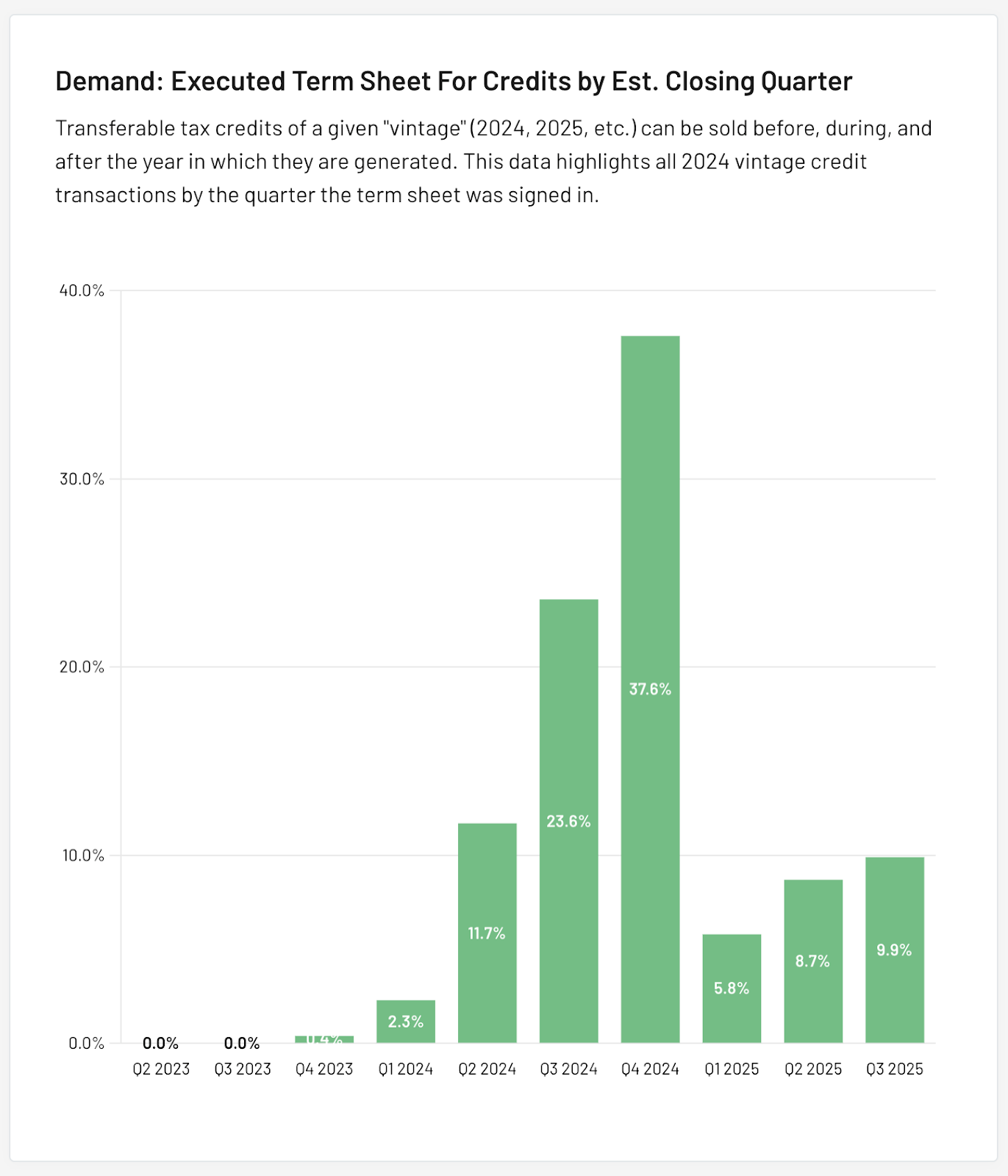

10% of 2024 tax credit transfers closed in Q3 2025

Nearly 10% of all transfers involving 2024 credits took place in Q3 2025 – concentrated heavily in September and the first half of October, just ahead of the extended filing deadlines for both partnerships and C-corporations, respectively. This is measured by notional deal volume.

For many buyers, these “before-the-buzzer” transactions were structured around a carryback strategy, allowing them to request a refund simultaneously with the filing of their 2024 return.

Other deals were driven by the desire to fully utilize remaining tax capacity under the 75% statutory credit offset cap.

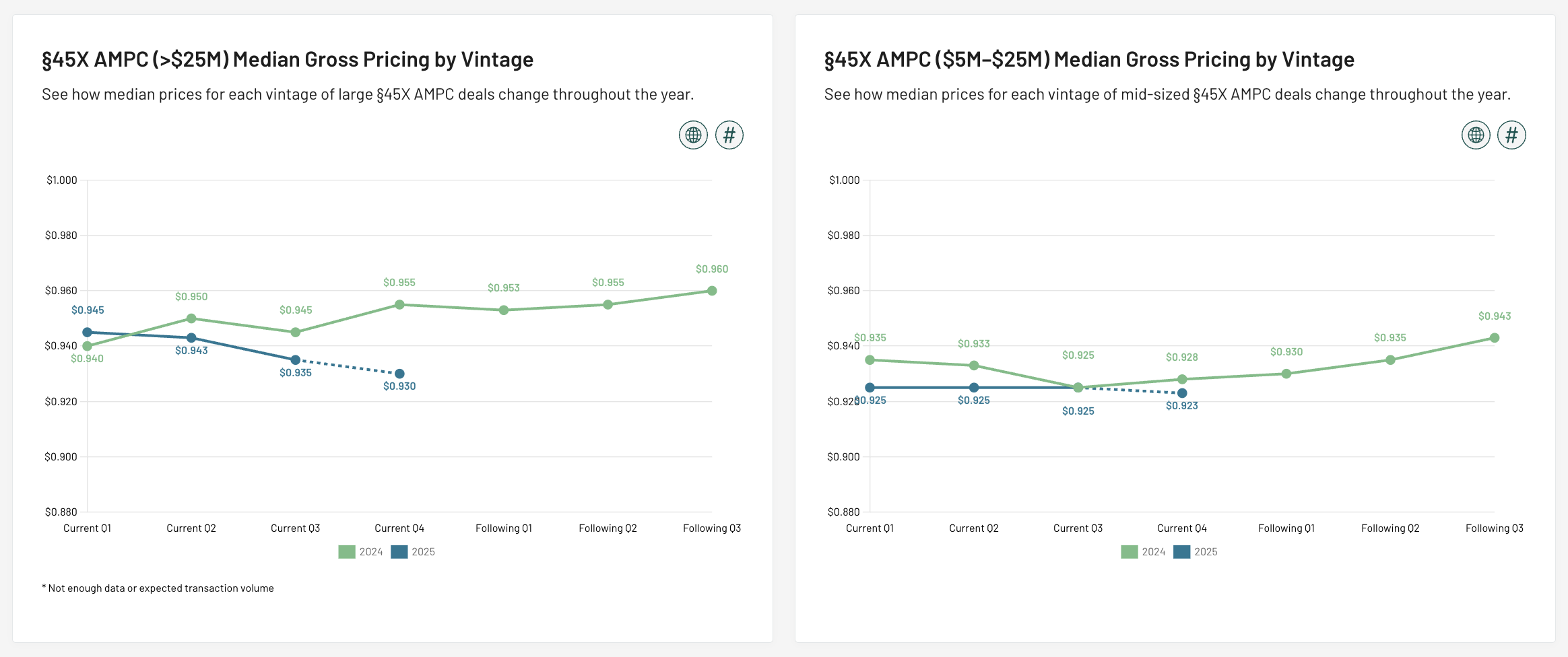

Regardless of the buyer’s underlying motivation, sellers generally benefited from premium pricing. Section 45X transactions for the 2024 vintage, for example, traded at the top of their range in Q3 2025 – "Following Q3" for the 2024 trend line – for both large and small deals.

PWA

Credits that are PWA exempt because of beginning of construction (BoC) dates are vanishingly rare

In the early days of the transfer market, buyers often sought tax credits that were exempt from prevailing wage and apprenticeship (PWA) requirements in an effort to avoid an incremental due diligence burden. Projects that either began construction before January 29, 2023 or have a capacity of less than 1 megawatt are generally exempt from PWA rules.

In 2023, nearly all available credits on Reunion’s platform fit that profile: by credit value, 95% of Section 48 ITCs and 100% of Section 45 PTCs were PWA-exempt due to BoC timing. Fast-forward to the 2026 credit vintage, and the landscape has essentially reversed.

Projects with a capacity under 1 MW, such as residential solar, remain exempt from PWA requirements, as do certain other credit types (e.g., 45X credits).

Only 1% of 2026 Section 48 ITCs and 29% of Section 45 PTCs remain PWA-exempt due to BoC timing.

The 29% exemption figure for 2026 Section 45 PTCs may give buyers an overly optimistic impression. Much of this volume is already committed through multi-year strips or tied up by existing buyers holding rights of first refusal. As a result, PWA-exempt PTCs that are broadly available may carry a pricing premium and clear the market quickly.

FEOC

FEOC is becoming a key purchase consideration, resulting in premium pricing for credits with low FEOC risk

In 2024, buyers specifically requested credits that were exempt from PWA requirements. We are starting to see a similar trend emerging with respect to Foreign Entity of Concern (FEOC); buyers are prioritizing “legacy” Section 48 ITCs and Section 45 PTCs that qualify as FEOC-exempt. We expect legacy credits to trade at a premium price compared to similar credits (e.g., 48E and 45Y) that require compliance with FEOC rules.

We expect demand for increasingly scarce "legacy,” FEOC-exempt Section 48 and Section 45 tax credits to drive pricing higher.

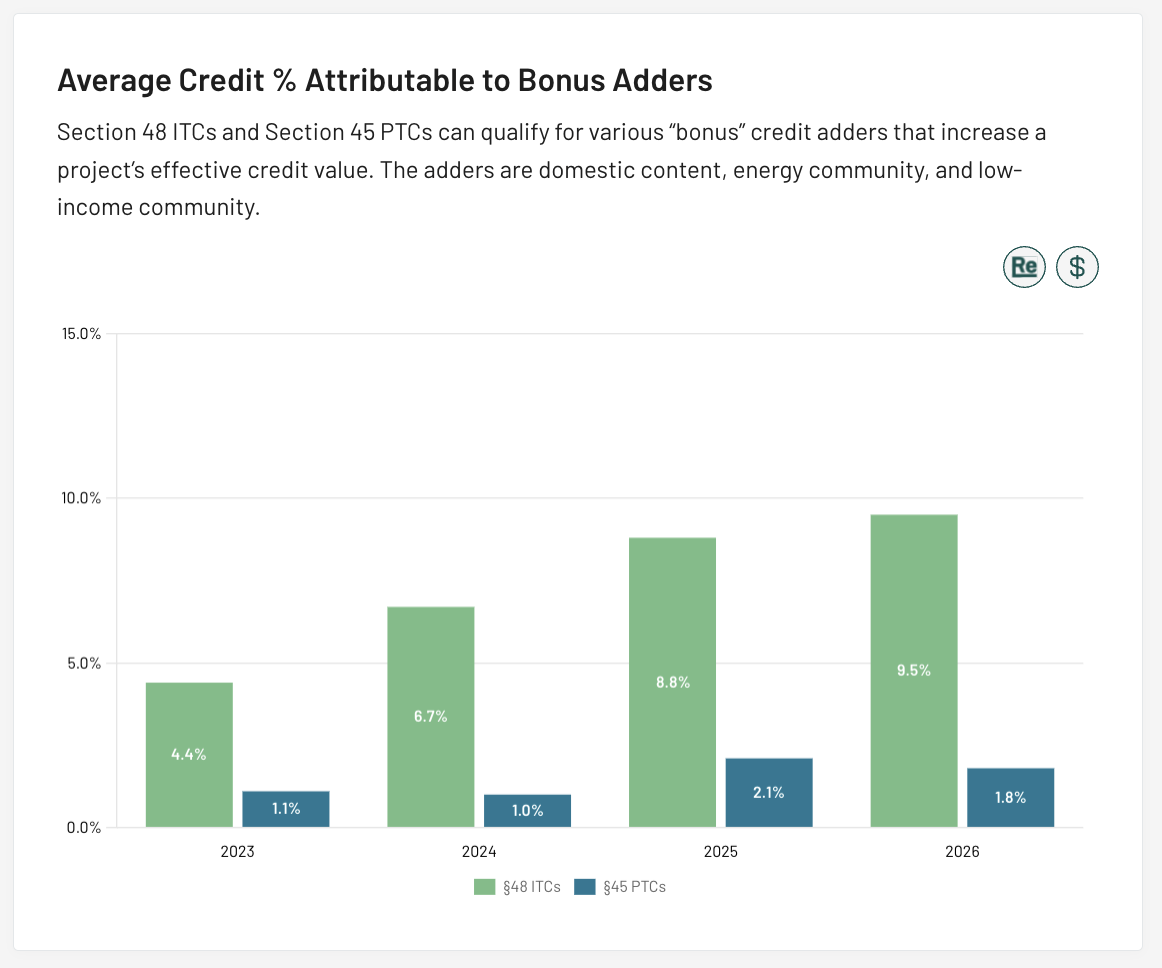

Credit adders

Adoption of bonus credit adders continues to expand for ITCs, but remains muted for PTCs

Section 48 ITCs and Section 45 PTCs can qualify for various “bonus” credit adders that increase a project’s effective credit value.

Since 2023, average ITC credit amount above the 30% baseline (assuming PWA compliance), have risen from 4.4% to 9.5%, indicating that most developers are now effectively incorporating at least one credit adder.

From a buyer’s perspective, Section 48-eligible projects without a bonus credit adder have become relatively scarce.

Section 45 PTCs, by contrast, show a different pattern. Average PTC rates above the base credit amount have remained relatively flat from 1.1% in 2023 to 1.8% in 2026. This stability is expected, however, because many Section 45 PTCs originate from projects that pre-date the Inflation Reduction Act’s introduction of bonus credit adders.

Access Reunion's Q3 Update to Market Monitor

Explore the latest pricing trends, transaction data, and market dynamics shaping the transferable tax credit market.

Alex Melehy

December 8, 2025

What Happens If You Fail PWA Compliance? Penalties, Recapture, and the Real Cost of Non-Compliance

Failing to meet PWA requirements under the IRA can cost developers up to 80% of their tax credit value, with cure penalties ranging from $5,000–$10,000 per worker for wage shortfalls to $50–$500 per hour for apprenticeship gaps.

For Sellers

Under the Inflation Reduction Act (IRA), PWA compliance isn't just a regulatory checkbox—it's the mechanism that lets you claim 5x your project's base tax credit amount. Most developers know this in theory, but few appreciate just how costly non-compliance actually is in practice. Below, we break down the penalties, recapture risks, and deal friction that come with falling short.

The 80% Cliff: Losing the 5x Multiplier

Projects that meet both prevailing wage and apprenticeship requirements qualify for a 5x credit multiplier. Miss either one, and you forfeit up to 80% of the credit you planned on. On a $100 million project claiming the §48 ITC, that's $24 million in lost credit value. And if the failure surfaces during the recapture period, the IRS can potentially claw that amount back from the tax credit buyer.

The IRS Correction and Penalty Framework

The good news: if a prevailing wage underpayment or apprenticeship gap comes to light, the IRS doesn't automatically knock your credit down to the base rate. You get a 180-day window after a final IRS determination to make corrections. The bad news: those cure provisions are steep.

- Prevailing Wage Shortfalls: You must pay affected workers the back-wages owed, plus interest at the federal short-term rate (per §6621) plus 6%, along with a $5,000 penalty to the IRS per worker for each year of underpayment. If the IRS finds the failure was due to "intentional disregard," the back-wage obligation triples and the penalty jumps to $10,000 per worker.

- Apprentice Labor Hours Gaps: Every hour short of the apprentice labor hours requirement costs $50—or $500 per hour if the IRS deems it intentional disregard. To put that in perspective: on a 100,000-hour project requiring 15% apprentice labor, a complete apprenticeship labor hour failure could mean $750,000 in penalties.

- Apprentice Participation Shortfalls: Any contractor or subcontractor with four or more laborers or mechanics on the project must employ at least one qualified apprentice. If they don't, the penalty is calculated by dividing that contractor's total labor hours by the number of laborers and mechanics they had on the project, then multiplying by $50 per hour ($500 for intentional disregard). This one is assessed at the contractor level—so a single large sub that never brings on an apprentice can rack up serious exposure even if the project-wide apprentice labor hour percentage looks fine.

Real-World Deal Friction: The Cost of Incomplete Reports

IRS penalties aside, poor PWA tracking creates real deal friction. In Reunion's transaction database, deals with a PWA diligence requirement close more than two weeks slower on average than those without one.

The usual culprit? Incomplete certified payroll reports. In one recent transaction Reunion facilitated, buyer's counsel spent weeks picking apart gaps in the PWA data, eventually pushing the compliance report to a post-closing obligation—resulting in lost leverage for the seller that could have been avoided entirely.

Why "We'll Figure It Out Later" Doesn't Work

A lot of developers assume they can piece together their records after construction wraps. In practice, retroactive compliance is far harder and far more expensive. Forensic reconstruction of wage data from messy records can run $150,000–$200,000 in accounting fees, compared to roughly $40,000 when tracked from the start (depending on project size and contractor count).

The takeaway: treat certified payroll data as a hard dependency, not a nice-to-have. A purpose-built PWA compliance provider can flag issues in real time, get ahead of back-pay or penalty exposure, and keep your 5x multiplier intact from day one.

Mahon Walsh

December 5, 2025

A guide to quick refunds for tax credit buyers

Form 4466 quick refunds help tax credit buyers recoup their investment months sooner

For Buyers

In brief

A quick refund under IRC §6425 allows a corporation that has overpaid its estimated income taxes – perhaps due to buying tax credits – to get cash back before filing its full tax return. By filing IRS Form 4466 shortly after year-end (and before the regular return due date), eligible corporations can recover overpayments – so long as the excess exceeds both $500 and 10% of expected tax liability. For tax credit buyers in particular, quick refunds are a powerful cashflow tool, accelerating the economic benefit of credits by months compared to the standard refund process.

Quick refunds allow corporations to recover overpaid estimated taxes early

Under IRC §6425, a “quick refund” allows a corporation that has overpaid its estimated federal income tax to request an “adjustment” of its estimated income tax prior to filing its full annual return.

Corporations may request a quick refund by filing IRS Form 4466 (see the full Instructions for Form 4466).

Quick refunds have become a common mechanism for corporations purchasing tax credits to more quickly realize the benefit of their investment in the event that they overpaid their estimated tax.

Quick refunds accelerate cash recovery from tax credit purchases

If a corporation has overpaid estimated tax due to a tax credit transaction in their current tax year, the quick refund returns the overpayment much faster than the conventional refund process. This allows the corporation to more quickly realize the benefit of their investment.

Benefits are particularly pronounced for corporations who purchase credits in the months immediately preceding or following the close of their tax year. As a quick refund can only be requested after the end of a given tax year (see §6425(a)(1)), corporations purchasing tax credits in the months surrounding the end of their tax year may more quickly request and receive a quick refund.

A quick refund, however, yields benefits for any corporation that has overpaid their estimated tax, regardless of the timing of their tax credit purchase.

Eligibility depends on the size of the estimated tax overpayment

Corporations that have overpaid their estimated income tax in the current tax year are eligible for a quick refund under Form 4466. Take a company that has an estimated 2025 tax liability of $100M, which it pays in quarterly estimated tax payments of $25M each. Let’s assume that the company purchases $40M of tax credits, reducing their estimated tax liability to $60M.

- After their Q3 estimated payment date, they will have paid $75M in estimated taxes, which is an overpayment of $15M

- After their Q4 estimated payment date, they will have paid $100M in estimated taxes, which is an overpayment of $40M

If the corporation is in an overpayment position, they can file for a quick refund using Form 4466. To qualify, the overpayment must be:

- Greater than 10% of expected tax liability for the year AND

- Greater than $500

Form 4466 must be filed shortly after year-end

Corporations must apply for a quick refund after the end of their tax year (e.g., December 31 for calendar-year tax filers) but before the 15th day of the fourth month thereafter and their income tax return filing (Form 1120) for that year. Thus, a calendar-year filer would submit Form 4466 between January 1st and April 15th.

Form 4466 instructions state, “An extension of time to file the corporation’s tax return will not extend the time for filing Form 4466”, so corporations must file Form 4466 before their non-extended tax filing deadline, even if they extend. In other words, a corporation with a December year-end that extends their tax return filing date must still submit Form 4466 before April 15th. Practically speaking, corporations should file a quick refund request as soon as possible after their tax year-end to maximize cashflow benefit.

The corporation must also file a copy of the previously filed Form 4466 with its income tax return.

Refunds are typically issued within 45 days

The IRS is required to process a Form 4466 request within 45 days. The IRS may review elements of the filing, so corporations should be prepared to provide any requested information promptly to avoid delays in receiving the refund.

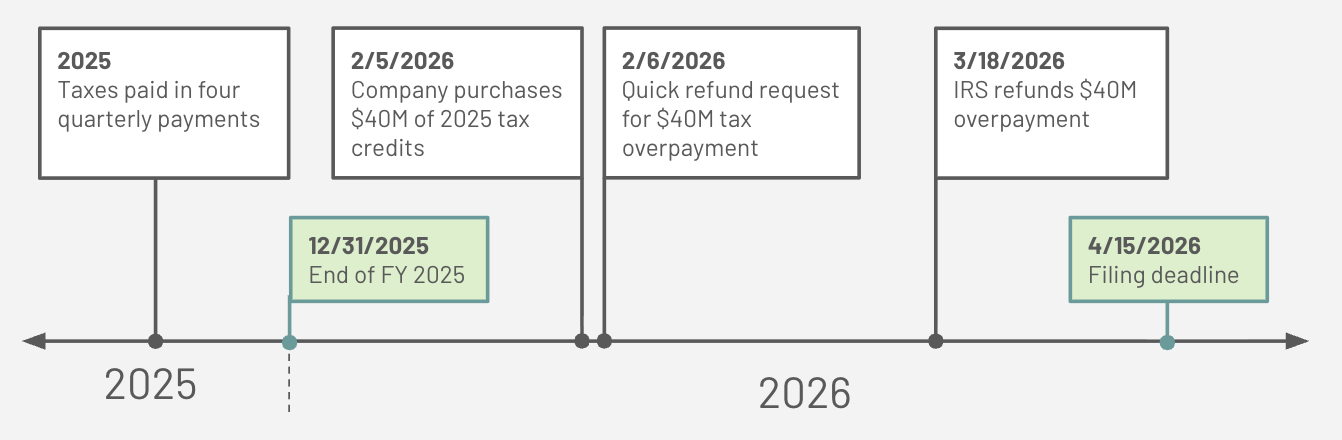

Here is a sample quick refund timeline for a calendar-year filer with a filing deadline of 4/15/26:

- The company has a 2025 estimated tax liability of $100M, which it already paid in four quarterly payments of $25M

- The corporation purchases $40M of Section 48 ITCs on 2/5/2026 for $36M. The corporation has now overpaid their 2024 taxes by $40M.

- The corporation submits Form 4466 on 2/6/2026, requesting a quick refund of their $40M overpayment

- The corporation receives $40M from the IRS on 3/18/2026, realizing their cash savings of $4M

Alex Melehy

November 26, 2025

A Comprehensive Guide to Complying with Prevailing Wage and Apprenticeship Requirements

Ensure compliance with the final regulations on prevailing wage and apprenticeship requirements for energy tax credits. Mitigate risks & avoid penalties.

For Buyers

For Sellers

The Inflation Reduction Act (IRA) aims to create a robust market for well-paying clean energy jobs. To achieve this goal, the IRA significantly increases the tax benefits for projects that meet Prevailing Wage and Apprenticeship (PWA) requirements. The IRA introduced transferable tax credits, codified under §6418 of the Internal Revenue Code (IRC), allowing "eligible taxpayers" to sell certain energy tax credits to unrelated third parties for cash. Transferability intends to broaden the pool of investors participating in clean energy financing by simplifying complex structures like traditional tax equity arrangements.

Projects that comply with PWA requirements generally receive a tax credit that is five times greater than the base rate. Of the 12 tax credits eligible for transfer, only the §45X credit is not subject to PWA requirements.

The IRS and Treasury published final PWA regulations on June 18, 2024, which went into effect on August 26, 2024. Alongside the final regulations, the IRS published a fact sheet and updated its PWA FAQs.

For more information about Reunion’s PWA compliance product, please contact us here.

Prevailing wage rules

Overview of prevailing wage

Prevailing wage rules require that laborers and mechanics who are employed by the project developer, or by construction contractors or subcontractors working on the project, are paid a minimum prevailing wage specified by the U.S. Department of Labor (DOL). Prevailing wages must be paid during the construction of a facility or property, and during alteration or repair of a facility or property for a certain number of years after the project is placed in service (see Duration of PWA requirements section).

Prevailing wages apply not only to laborers and mechanics at the site of construction, but also to secondary sites where a significant portion of the construction, alteration, or repair of the facility occurs, provided that the secondary site either was established specifically for, or dedicated exclusively for a specific period of time to, the relevant project. Secondary sites include any adjacent or virtually adjacent dedicated support sites, such as job headquarters, tool yards, batch plants, or borrow pits.

Workers do not have to be paid prevailing wages for basic maintenance work, which is “routinely scheduled and continuous or recurring.” Examples of basic maintenance are regular inspections of the facility, regular cleaning and janitorial work, regular replacement of materials with limited lifespans such as filters and light bulbs, and the calibration of any equipment.

When to start paying prevailing wages

Prevailing wages must be paid from the time at which construction, alteration, or repair begins; the definition of construction, alteration, or repair is expansive and includes all types of work done on a particular building or work site, as defined in 29 CFR 5.2. This aligns with the Davis-Bacon Act (DBA) definition administered by the DOL, rather than the physical work and 5% tests the IRS has used to determine when construction starts for tax purposes (as discussed in the Beginning of construction section). For example, prevailing wages must be paid during certain demolition or removal activities, which would not be considered the start of physical work on the project for purposes of qualifying for tax benefits.

Determining the prevailing wage rate

Prevailing wage rates are published on the SAM website. The appropriate job type, location, and wage determination must be selected to comply with prevailing wage requirements. Occasionally, a job type for a given location will not be published. In this case, the taxpayer must contact the DOL at IRAprevailingwage@dol.gov to request a wage determination for the unlisted job type. The request to the DOL must include specific pieces of information such as form SF-1444, project name and location, contractor name, contract number (if applicable), name and description of the job classification needed, proposed wage rate and fringe benefits, the duties performed by workers in the proposed classification, explanation of why no current classification in the wage determination matches these duties, and an agreement or disagreement of the contracting officer and contractor with the proposed rate. The department has indicated that it will try to respond to wage determination requests within 30 days. For more information, please consult our PWA Help Center.

The prevailing wage rates that must be paid are locked in at the time the contract for the construction, alteration, or repair of the facility is executed by the project developer and the contractor. This is consistent with the timing of wage determinations in Davis-Bacon compliant projects. If a project developer enters into a contract for alteration or repair work over an indefinite period of time that is not tied to the completion of any specific work, the applicable prevailing wage rates must be updated on an annual basis on the anniversary date of such contract.

If the project developer executes separate contracts with more than one prime contractor, then for each such contract, the applicable prevailing wage rates are determined at the time the contract is executed with each prime contractor. The prevailing wage rates apply to all subcontractors under each prime contractor. Prevailing wage rates must be reset to current wage rates if the contract is later amended to add substantially to the scope of work or extend the contract period.

If work on a project straddles locations with different wage rates, then the project developer should pay the wages for each location based on where the work is done. Offshore wind projects should use the prevailing wages for the closest location on shore.

Reunion PWA automatically scrapes the SAM website for all wage determinations across all states and counties regularly. Reunion makes this data available and searchable via Reunion PWA so that developers and contractors can easily select the appropriate wage determinations for their projects.

Apprenticeship rules

The IRA’s apprenticeship rules fall into three main categories.

Labor hours requirement

The apprenticeship rules require a certain percentage of labor hours during construction, alteration, or repair for a project prior to the facility being placed in service to be performed by a qualified apprentice. The minimum percentage of hours that must be performed by qualified apprentices is:

- 12.5% for projects that began construction after December 31, 2022, and before January 1, 2024

- 15.0% for projects that begin construction after December 31, 2023

Hours worked by foremen, superintendents, owners, or persons employed in a bona fide executive, administrative, or professional capacity are excluded from the labor hours calculation, unless these persons devote more than 20% of their time during a workweek to manual or physical labor. In this case, the hours worked must be included in the denominator (total labor hours) of the apprentice labor hours calculation.

Ratio requirement

Any apprentices performing work on a project are subject to the applicable apprentice-to-journeyworker ratio as prescribed by the associated registered apprenticeship program. Apprentice-to-journeyworker ratios must be met daily and vary depending on the applicable apprentice program’s requirements.

Participation requirement

Any contractor, subcontractor, or taxpayer who employs four or more mechanics or laborers on the project must employ one or more qualified apprentices. The journeyworkers and apprentices, however, do not have to be employed at the same time, provided that the applicable apprentice-to-journeyworker ratio as prescribed by the associated apprenticeship program is met on days when the apprentice is working.

Duration of PWA requirements

The duration of the PWA compliance requirement depends on the tax credit type. The IRS clarified in the final regulations that apprentices are not required for work after a project is placed in service; therefore, compliance during the post-construction period applies only to prevailing wages.

As previously noted, §45X advanced manufacturing production credits are not subject to PWA requirements.

Impact of PWA Compliance on Tax Credits

Overview

The Prevailing Wage and Apprenticeship (PWA) requirements are a critical component of the Inflation Reduction Act of 2022 (IRA), and compliance with these rules has a direct and substantial financial impact on the value of most clean energy tax credits.

PWA compliance determines whether a project qualifies for an enhanced, significantly larger tax credit amount, which is generally five times greater than the base tax credit rate.

Financial Impact: The 5x Multiplier

For most transferable tax credits, meeting the PWA requirements results in a credit rate that is five times higher than the base rate.

The IRS updates §45 and §45Y PTC rates on an annual basis, generally in Q2. Rates are determined using an inflation adjustment factor (IAF) and published in the Federal Register. The inflation adjustment factor for 2025 is 1.9971. Specific examples of this financial enhancement include:

- Investment Tax Credits (§48 and §48E ITCs):

- If PWA requirements are met (or exempted from), the credit is 30% of a project’s qualified basis.

- If PWA requirements are not met, the credit is reduced to the base rate of 6% of the qualified basis.

- Furthermore, achieving PWA compliance is necessary to receive the full value of certain bonus credits. For example, the Energy Community bonus or Domestic Content bonus is typically 10% of the qualified basis if PWA requirements are met, but only 2% if they are not met.

- Production Tax Credits (§45 and §45Y PTCs):

- The §45Y PTC has one base rate, irrespective of when a qualifying project is placed in service. The base rate is $3 per megawatt-hour (MWh) of qualifying electricity produced and sold. With PWA compliance (or exemption), the rate increases to $15 per MWh. There is also an annual, calendar year inflation adjustment for the rates, in which the rates are multiplied by the inflation adjustment factor described above and rounded. The $3 base rate is rounded to the nearest multiple of $0.50, and the $15 PWA rate is rounded to the nearest multiple of $1. As such, using the 2025 inflation adjustment factor of 1.9971, the 2025 base rate and PWA rate (after rounding) are $6 and $30 per MWh of qualifying electricity produced and sold, respectively.

- For projects placed in service after December 31, 2021, the §45 PTC rate calculation is $3 per MWh of qualifying energy, multiplied by the inflation adjustment factor, and rounded to the nearest $0.50. For projects meeting PWA requirements, this product is multiplied by five. There is no separate PWA rate of $15 per MWh of qualifying energy for these projects, and as such, the resulting rate for PWA-compliant projects may have small differences from the PWA rates discussed above, as was the case in 2024. The same technology-specific rate adjustments apply for open-loop biomass, small irrigation power, landfill gas, and trash facilities, so the resulting rate is reduced by one-half. There is no phaseout adjustment for wind projects placed in service after December 31, 2021. The 2025 rate, assuming prevailing wage and apprenticeship compliance, is $30.00 per MWh for wind, closed-loop biomass, geothermal, and solar; and $15.00 per MWh for open-loop biomass, landfill gas, trash, qualified hydropower, and marine and hydrokinetic renewable energy. For qualified hydropower and marine and hydrokinetic renewable energy facilities placed in service after December 31, 2022, the 2024 rate is $15.00 per MWh, assuming prevailing wage and apprenticeship compliance.

- Similar to the ITC case, the Energy Community bonus and Domestic Content bonus add a 10% increase to the applicable rate (Base or PWA-compliant).

Impact on Risk and Due Diligence

For tax credit purchasers, PWA compliance is a major risk factor. If the requirements are not met and the project claimed the enhanced rate, the credit amount can be dramatically reduced (e.g., from 30% to 6% for an ITC), resulting in an "excessive credit transfer". The buyer is liable for this excessive credit amount plus a 20% penalty.

Therefore, PWA compliance heavily influences the due diligence process for transferable tax credit transactions:

- Buyers must ensure sellers maintain extensive records, including payroll records for all laborers and mechanics (including apprentices).

- Documentation must substantiate proper labor classifications, applicable wage rates, and comprehensive apprenticeship records (requests, hours worked, ratios).

- For §48 ITCs, the seller must provide an annual prevailing wage compliance report during the five-year recapture period.

- Buyers should validate if a seller claims an exception, such as verifying the BoC date or the project's output capacity.

- Due to the complexity, Reunion offers a PWA compliance software product to reduce the time and expense of complying with PWA requirements and generate a standardized report for due diligence purposes.

Records and documentation

If PWA requirements are not fulfilled, tax credit buyers who were expecting the full tax credit amount could face a credit disallowance and be subject to underpayment penalties. However, when PWA compliance is well-documented, a careful due diligence process can help buyers get comfortable that the tax credits are properly accounted for.

Prevailing wage records

PWA documentation must include “payroll records for each laborer and mechanic (including each qualified apprentice) employed by the taxpayer, contractor, or subcontractor employed in the construction, alteration, or repair of the qualified facility.”

The guidance also lists further information that the taxpayer “may include” in their records for prevailing wage compliance:

- Identifying information for each laborer and mechanic who worked on the construction, alteration, or repair of the qualified facility, including the name, the last four digits of a social security or tax identification number, address, telephone number, and email address

- The location and type of construction of the qualified facility

- The labor classification(s) the taxpayer applied to each laborer and mechanic for determining the prevailing wage rate and documentation supporting the applicable classification, including the applicable wage determination and copies of executed contracts for construction, alteration, or repair of the qualified facility with any contractor or subcontractor

- The hourly rate(s) of wages paid (including rates of contributions or costs for bona fide fringe benefits or cash equivalents thereof) for each applicable labor classification

- Records to support any contribution irrevocably made on behalf of a laborer or mechanic to a trustee or other third person pursuant to a bona fide fringe benefit program, and the rate of costs that were reasonably anticipated in providing bona fide fringe benefits to laborers and mechanics pursuant to an enforceable commitment to carry out a plan or program described in 40 U.S.C. 3141(2)(B), including records demonstrating that the enforceable commitment was provided in writing to the laborers and mechanics affected

- The total number of hours worked by each laborer and mechanic per pay period.

- The total wages paid for each pay period (including identifying any deductions from wages)

- Records to support wages paid to any qualified apprentices at less than the applicable prevailing wage rates, including records reflecting an individual’s participation in a registered apprenticeship program and the applicable wage rates and apprentice-to-journeyworker ratios prescribed by the registered apprenticeship program

- The amount and timing of any correction and penalty payments and documentation reflecting the calculation of the correction and penalty payments, including records to demonstrate eligibility for the penalty waiver in §1.45-7(c)(6)

- Records to document any failures to pay prevailing wages and the actions taken to prevent, mitigate, or remedy the failure (for example, records demonstrating that the taxpayer (or an independent third party engaged by the taxpayer) regularly reviewed payroll practices, included requirements to pay prevailing wages in contracts with contractors, and posted prevailing wage rates in a prominent place on the job site)

- Records related to any complaints received by the taxpayer, contractor, or subcontractor that the taxpayer, contractor, or subcontractor was paying wages less than the applicable prevailing wage rate for work performed by laborers and mechanics with respect to the qualified facility

Apprenticeship records

For apprentices, the developer should capture:

- Any written requests for the employment of apprentices from registered apprenticeship programs, including any contacts with the DOL’s Office of Apprenticeship or a state apprenticeship agency regarding requests for apprentices from registered apprenticeship programs

- Any agreements entered into with registered apprenticeship programs with respect to the construction, alteration, or repair of the facility

- Documents reflecting the standards and requirements of any registered apprenticeship program, including the applicable ratio requirement prescribed by each registered apprenticeship program from which taxpayers, contractors, or subcontractors employ apprentices

- The total number of labor hours worked with respect to the construction, alteration, or repair of the qualified facility, including and identifying hours worked by each qualified apprentice

- Records reflecting the daily ratio of apprentices to journeyworkers

- Records demonstrating compliance with the Good Faith Effort Exception in §1.45-8(f)(1) (including requests for qualified apprentices, correspondence with registered apprenticeship programs, and denials of requests)

- The amount and timing of any penalty payments and documentation reflecting the calculation of the penalty payments

- Records to document any failures to satisfy the apprenticeship requirements under §45(b)(8) and §1.45-8 and the actions taken to prevent, mitigate, or remedy the failure

- Records related to any complaints received by the taxpayer, contractor, or subcontractor that the taxpayer, contractor, or subcontractor was not satisfying the apprenticeship requirements

Annual prevailing wage compliance report

For §48 ITCs, tax credit sellers must submit an annual prevailing wage compliance report to the IRS during the five-year recapture period. The report should adequately document the payment of prevailing wages with respect to any alteration or repairs of the project.

Tax credit sellers submit the report to the IRS with their tax returns. To ensure compliance with the reporting requirement, tax credit buyers should receive confirmation of the seller’s annual submission.

Compliance

The IRS encourages tax credit sellers to take the following actions to ensure ongoing compliance:

- Regularly reviewing payroll records

- Ensuring that any contracts entered into with contractors require that the contractors and their subcontractors adhere to prevailing wage and apprenticeship requirements

- Regularly reviewing compliance with the prevailing wage and apprenticeship requirements (including the proper worker classifications of laborers and mechanics, the applicable prevailing wage rates, and the percentage of labor hours performed by qualified apprentices)

- Posting information about paying prevailing wages in a prominent and accessible location, or otherwise providing written notice regarding the payment of prevailing wage rates

- Establishing procedures for individuals to report suspected failures to comply with the prevailing wage and apprenticeship requirements without retaliation or adverse action

- Investigating reports of suspected failures to comply with the prevailing wage and apprenticeship requirements

- Contacting the DOL’s Office of Apprenticeship or the relevant state apprenticeship agency for assistance in locating registered apprenticeship programs

Exceptions

Beginning of construction

Projects that began construction before Jan. 29, 2023, are exempt from the prevailing wage and apprenticeship rules, except for credits under §48C and §45Z. To learn more, please refer to the Beginning of construction section.

For the avoidance of doubt, the beginning of the construction test to determine exemption from prevailing wage and apprenticeship requirements is a different test than determining when construction, alteration, or repair of a project began for purposes of starting compliance with prevailing wage rates (as discussed in the When to start paging prevailing wages section).

One megawatt

Projects under §45 and §48 (and their replacements under §45Y and §48E) are exempt from PWA if the maximum net output is less than one megawatt (as measured in alternating current) or the capacity of electrical or equivalent thermal storage is less than one megawatt. The net output will be determined by “nameplate capacity,” defined in 40 CFR 96.202, as the maximum output on a steady-state basis during continuous operation under standard conditions when not restricted by seasonal or other deratings.

In the case of thermal equipment, like geothermal heat pumps and solar process heating, a developer must use the equivalent of 3.4 million British thermal units per hour (mmBTU/hour) to determine maximum capacity. For hydrogen storage and clean hydrogen production facilities, 3.4 mmBTU/hour is equivalent to 10,500 standard cubic feet per hour. Finally, for qualified biogas, developers can convert 3.4 mmBTU/hour into a maximum net volume flow rate of 10,500 standard cubic feet/hour, after converting the gas output into a maximum net volume flow using the appropriate high heat value conversion factors found in an EPA table.

Electrochromic glass, fiber-optic solar, and microgrid controllers are not eligible for the one-megawatt exception because they do not generate electricity or thermal energy.

Remedies

Prevailing wages

If a developer does not meet the PWA requirements, the tax credit does not automatically get reduced to the base rate. A developer can cure any deficiencies and will be deemed to satisfy the PWA requirements if, within 180 days from when the IRS makes a final determination (which occurs on the date the IRS sends a notice to the developer stating that the developer has failed to satisfy the PWA requirements), they:

- Pay back-wages with interest: Pay the affected laborers or mechanics the difference between what they were paid and the amount they were required to have been paid (multiplied by three for intentional disregard), plus interest at the federal short-term rate (as defined in §6621) plus 6%; and

- Pay a penalty: Pay a penalty to the IRS of $5,000 ($10,000 for intentional disregard) for each laborer or mechanic who was not paid at the prevailing wage rate in the year. This penalty applies to each calendar year of the project. If, for example, a laborer is not paid the correct prevailing wage in two calendar years, the penalty is $10,000

The taxpayer can waive the penalty if they make a corrective payment with interest by the last day of the first month after the calendar quarter in which the wage shortfall occurred, and either of two conditions is true:

- The worker was not paid less than the prevailing wage for more than 10% of all pay periods of the calendar year during which the worker was employed on the project

- The shortfall in payment was not greater than 5% of what the worker should have been paid during the year

The penalty is waived if the laborer or mechanic was employed under a “qualifying project labor agreement” and if any correction payment owed to the laborer or mechanic is paid on or before a return is filed claiming an increased credit amount. A qualifying project labor agreement must meet six requirements, which can be found at 26 CFR §1.45-7(c)(6)(ii).

To avoid increased penalties due to intentional disregard, the taxpayer should undertake a quarterly (or more frequent) review of wages paid to mechanics and laborers to ensure that wages not less than the applicable prevailing wage rate were paid.

Apprentices

Apprenticeship cures are unique to the failure that occurred. To cure a failure of a particular requirement, the following processes apply:

- Apprentice labor hours requirement: Any shortfall in apprentice labor hours is calculated (see Labor hours requirement section above and reclassification of apprentices to journeyworkers in the Apprentice ratio requirement below) and multiplied by $50 (or $500 for intentional disregard) to determine the amount of cure payment owed.

- Apprentice ratio requirement: The required apprentice-to-journeyworker ratio is calculated daily (see Ratio requirement section above), and apprentices in excess of the ratio are required to be paid a journeyworker wage. Labor hours from apprentices in excess of the ratio are also accounted for as journeyworker labor hours in the apprentice labor hours requirement above. Any shortfall in prevailing wage payments resulting from this reclassification of apprentices to journeyworkers must be remedied to maintain compliance.

- Apprentice participation hours requirement: If the participation requirement is not met (see Participation requirement section above), the shortfall in participation hours is the total labor hours divided by the number of laborers or mechanics (for the laborers or mechanics that failed to meet the participation requirement). This shortfall in participation hours is then multiplied by $50 (or $500 for intentional disregard) to determine the amount of cure payment owed.

Good-faith effort exception

The apprenticeship requirement can be satisfied if the developer or contractor made a good-faith effort to comply. The developer or contractor must have requested qualified apprentices from a registered apprenticeship program and either:

- The request was denied for reasons other than the developer’s refusal to comply with the program’s standards and requirements

- The apprenticeship program failed to respond within five business days of receiving a request

- The apprentice program provided apprentices, but there were fewer than requested

To satisfy the good faith effort exception, the developer or contractor must make a written request to at least one registered apprenticeship program that has a geographic area of operation that includes the location of the facility, or that can reasonably be expected to provide apprentices to the location of the facility; trains apprentices in the occupation(s) needed by the developer performing construction, alteration, or repair with respect to the facility; and has a usual and customary business practice of entering into agreements with employers for the placement of apprentices in the occupation for which they are training, pursuant to its standards and requirements.

An apprenticeship request must be made at least 45 days before the qualified apprentice is requested to begin work on the facility, so that registered apprenticeship programs have adequate time to plan for the anticipated need. Subsequent requests to the same registered apprenticeship program must be made no later than 14 days before qualified apprentices are requested to begin work on the facility.

If no apprentice program covers the project location, trains apprentices in the occupations needed, and supplies apprentices to employers, then the project is deemed to have made a good-faith effort without the need to file a request for apprentices. In this case, however, developers or contractors must contact the DOL and/or a state apprentice agency to help find apprentices.

A good-faith effort exception can be applied as an exemption from a portion of the apprentice labor hours requirement for a period of 365 days (or 366 during a leap year). The good faith effort exception excuses a developer or contractor from the amount of labor hours that were requested from the applicable apprentice program by applying the requested block of labor hours towards the numerator (apprentice labor hours) of the apprentice labor hours calculation. Developers or contractors must submit a subsequent request within the 365-day (or 366-day) window to continue to satisfy the good-faith exception for an additional block of apprentice labor hours. The annual duration also applies if a developer or contractor is not able to locate a registered apprenticeship program with an area of operation that includes the location of the facility.

Due diligence

Under the IRS regulations, it is the seller’s obligation to maintain and preserve sufficient records demonstrating compliance with PWA requirements. But the liability for non-compliance is on the buyer in the form of an excessive credit transfer.

If the tax credit claims to be exempt from PWA requirements, the tax credit buyer should substantiate the exemption under one of two scenarios:

- Beginning of construction exemption: Validate and substantiate that construction began before January 29, 2023

- One megawatt exemption: Validate the size of the eligible project through an audit of relevant contracts

If the tax credit requires compliance with PWA requirements, the tax credit buyer should validate that proper documentation was collected by the seller and that compliance was substantiated by a third party. At a minimum, the IRS requires “payroll records for each laborer and mechanic (including each qualified apprentice) employed by the taxpayer, contractor, or subcontractor.” The IRS also lists several other items the taxpayer may include in their records for PWA compliance, including nine related to wages and five related to apprentices; the list is available at 26 CFR §1.45-12(c) and (d).

Tax credit buyers should ensure sellers (or a contracted third party) have properly collected, maintained, and reviewed payroll records to ensure that prevailing wages were paid and sufficient apprentice labor was utilized. Tax credit sellers often engage third parties to provide additional analysis with respect to PWA compliance. Furthermore, buyers should also review the covenants, representations, and warranties in contracts with the primary EPC (and potentially with their subcontractors) to validate that all parties have agreed to comply with PWA requirements.

In the case of the §48 ITC, the seller should also provide an annual compliance report to the IRS during the recapture period.

Guidance and resources

Guidance

- November 30, 2022: IRS Notice 2022-61, Prevailing Wage and Apprenticeship Initial Guidance Under §45(b)(6)(B)(ii) and Other Substantially Similar Provisions

- August 30, 2023: Notice of Proposed Rulemaking, Increased Credit or Deduction Amounts for Satisfying Certain Prevailing Wage and Registered Apprenticeship Requirements

- November 17, 2023: Notice of Proposed Rulemaking, Definition of Energy Property and Rules Applicable to the [§48] Energy Credit

- June 24, 2024: Final regulations, Increased Amounts of Credit or Deduction for Satisfying Certain Prevailing Wage and Registered Apprenticeship Requirements

Resources

- The IRS maintains a prevailing wage and apprenticeship requirements FAQ

- The Department of Labor determines and maintains prevailing wages

- To request a wage determination, developers can email iraprevailingwage@dol.gov with project and labor information

- Apprenticeship.gov provides resources for finding qualified apprentices

- Reunion maintains a Reunion PWA Help Center for Reunion PWA customers that includes information about various regulations and instructions for submitting information to the DOL

Frequently Asked Questions about Prevailing Wage & Apprenticeship

- How can developers structure contracts to ensure continuous compliance with prevailing wage requirements across multi-phase projects?

- Ensure that contracts with EPCs (or primary contractors) contain provisions obligating the EPC and all subcontractors to abide by prevailing wage and apprenticeship requirements. Additionally, ensure that the EPC is obligated to provide certified payroll records and other relevant information to the developer (or a third party) such that PWA compliance can be certified.

- What mechanisms exist to verify and document apprenticeship utilization to satisfy the IRA’s PWA requirements?

- Developers (and contractors) should ensure that apprentices are hired from a registered apprentice program (listed on apprenticeship.gov) and that all apprentices have a certificate of registration with the applicable apprenticeship program.

- How do project timelines and change orders affect prevailing wage determinations?

- Wage determinations are “locked in” on the execution date of the construction contract with the EPC for a facility. However, wage determinations must be updated in one of the following situations:

- A new contract for alterations or repairs is executed after the facility is placed in service. In this case, use the wage determinations that are in effect when that alteration/repair contract is signed.

- There is a material contract change to the initial EPC contract. If the EPC contract is amended to substantially add scope or extend the contract period, wage determinations must be reset to the then-current modifications.

- Indefinite-term contracts are not tied to specific work. In this case, wage determinations must be reset each new contract year.

- Wage determinations are “locked in” on the execution date of the construction contract with the EPC for a facility. However, wage determinations must be updated in one of the following situations:

- What are the financial and tax credit implications of partial non-compliance with PWA provisions?

- For the purposes of determining compliance with the PWA requirements for the eligibility of the 5X rate multiplier, there is no partial compliance. Either a project is PWA compliant or it is not. That said, there are cure methods for any shortfall with respect to the PWA compliance requirements, such that projects are able to remedy issues and maintain compliance even if mistakes are uncovered later.

- How can digital compliance systems or third-party verification tools be integrated to simplify PWA tracking and reporting?