The Road Ahead for Renewable Energy is Paved With Tax Credit Financing

How Reunion is positioned to help connect corporate buyers with discounted tax credits to fund clean energy growth.

.webp)

The Inflation Reduction Act of 2022 (IRA) was a sweeping bill with many implications for the energy transition–particularly the financing of new projects. In the IRA, Congress specifically sought to incentivize private sector investment into the energy transition. One of the most prominent ways they did this was through tax credits, to incentivize corporate taxpayers to redirect capital into the clean energy and sustainable technology industry.

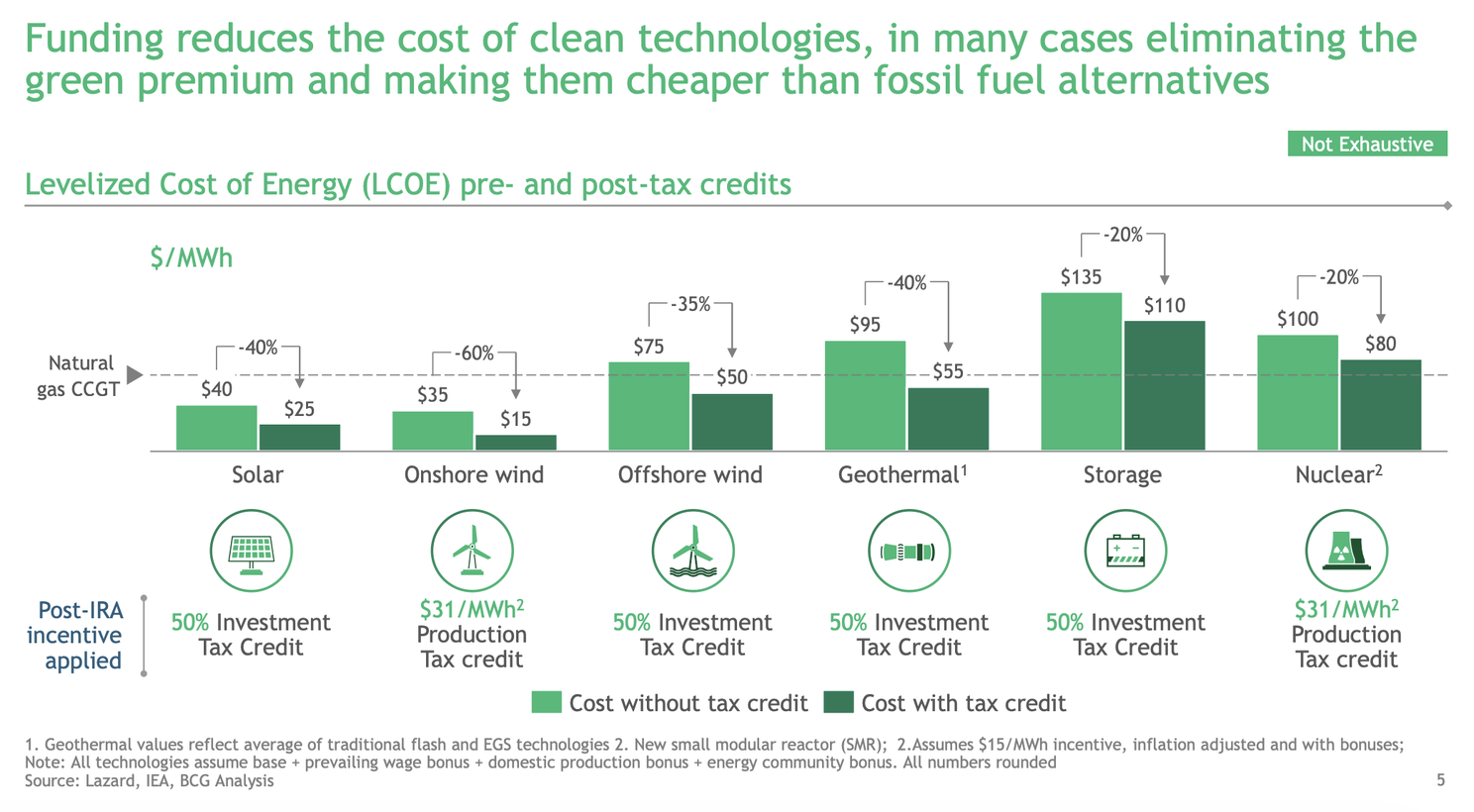

A recent assessment of the IRA from Boston Consulting Group (BCG) and Breakthrough Energy puts a fine point on the value of tax credits in switching to low carbon energy, by demonstrating the impact of tax credits on levelized cost of energy (LCOE).

Per BCG’s analysis, tax credits from the IRA and other major energy-related legislation can drive between 20% and 60% reductions in LCOE across six technology types. But a low LCOE and actual steel-in-the-ground are not the same thing. To physically deploy these less expensive technologies, project developers will require many billions of dollars of project finance capital.

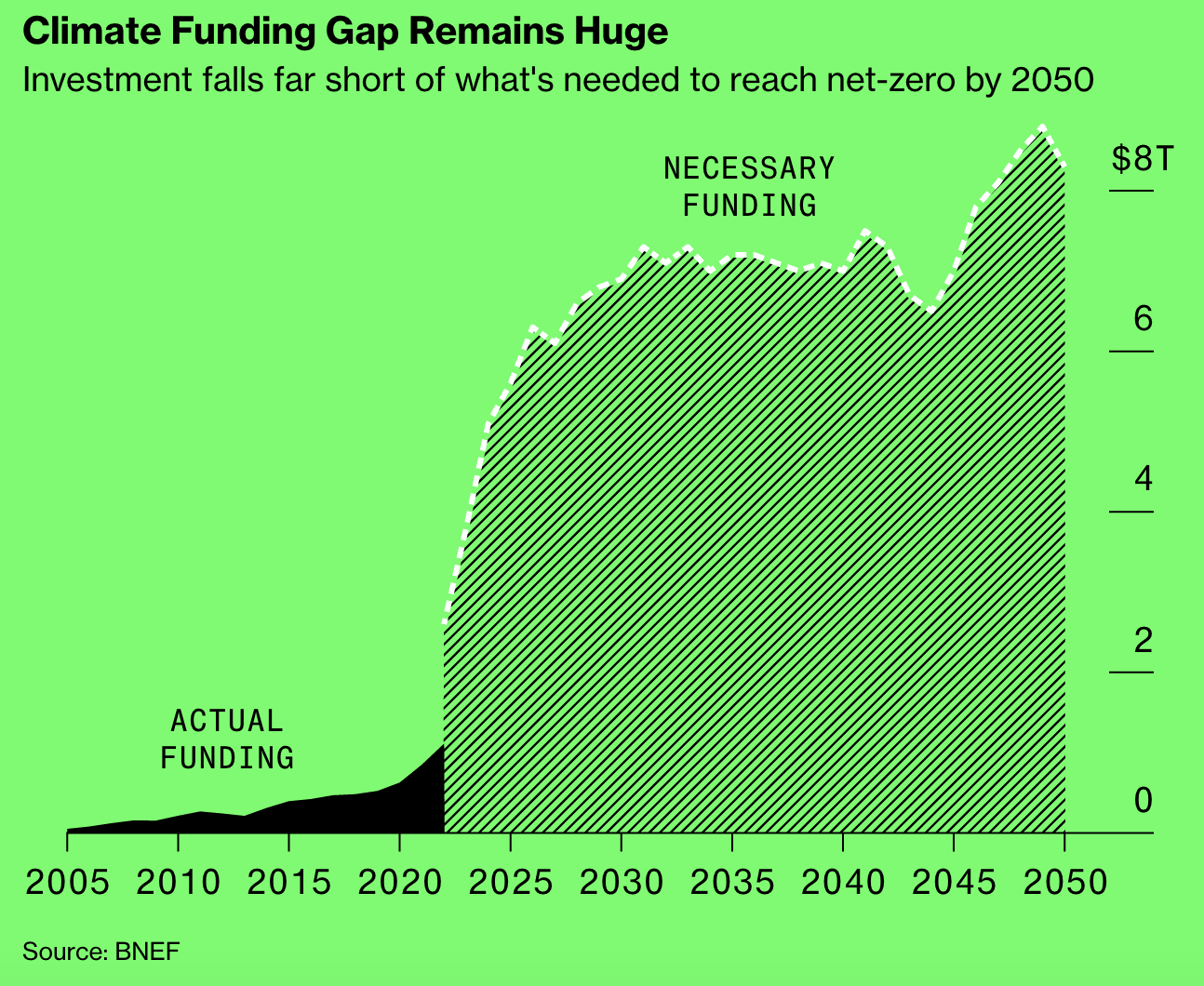

Bloomberg illustrates just how significant the demand for investment dollars may be over the next 25-30 years. This demand is a powerful function of government policies, decarbonization goals of Fortune 500 companies that increasingly extend down into global supply chains, and the aforementioned plummeting LCOE that allows low carbon energy technologies to displace incumbent coal, gas and oil-based power generation. That’s a very difficult demand-pull force to derail once it gets going.

The opportunity and challenge of tax credits for project finance

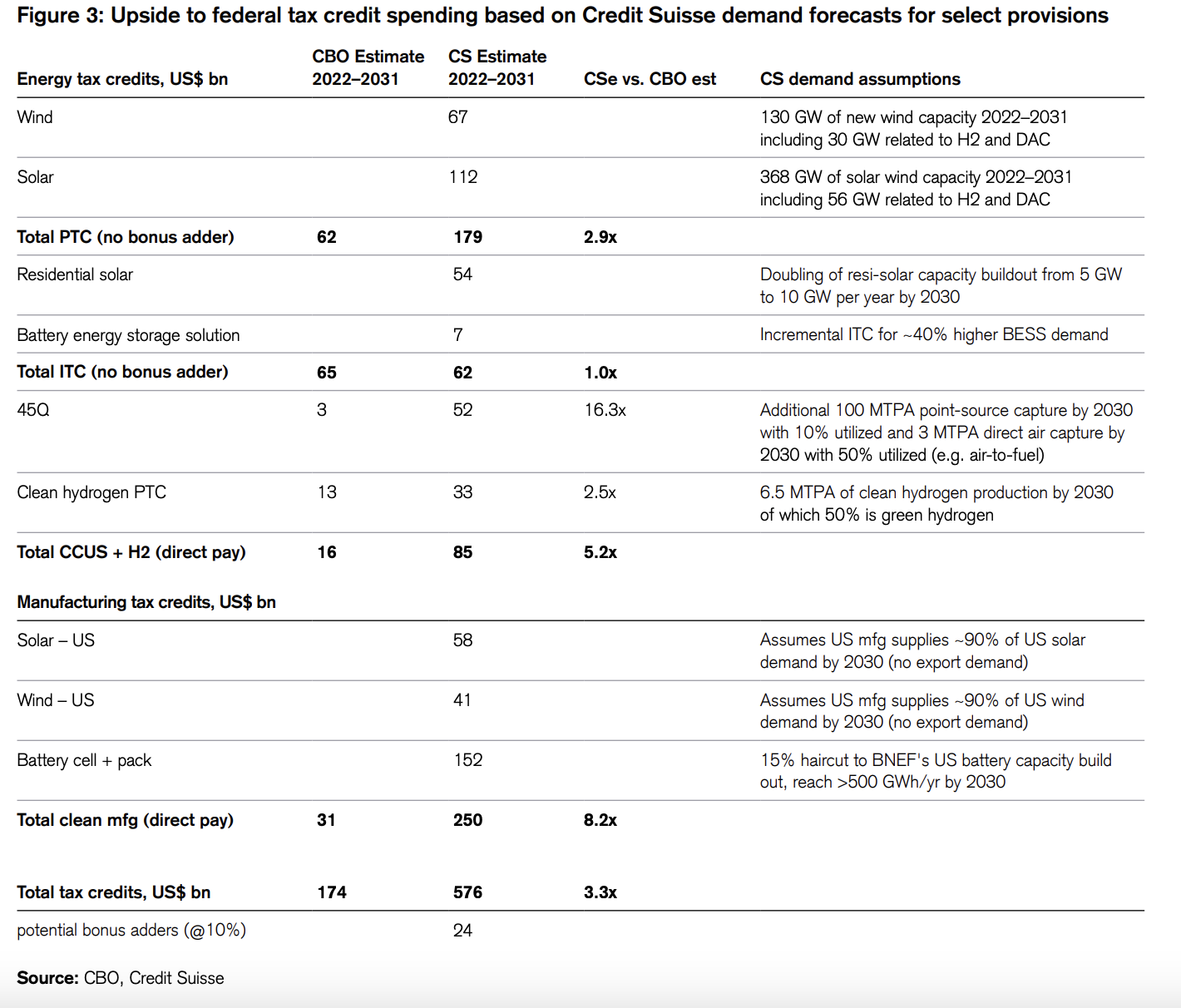

So where will all this capital come from? In the U.S. the IRA’s tax credit regime significantly enhances project capital stacks with upwards of $500 billion of tax credits over the next 10-20 years, depending on various estimates and factors. Here’s one such estimate from Credit Suisse, which projects $576B in tax credits over a 10-year period.

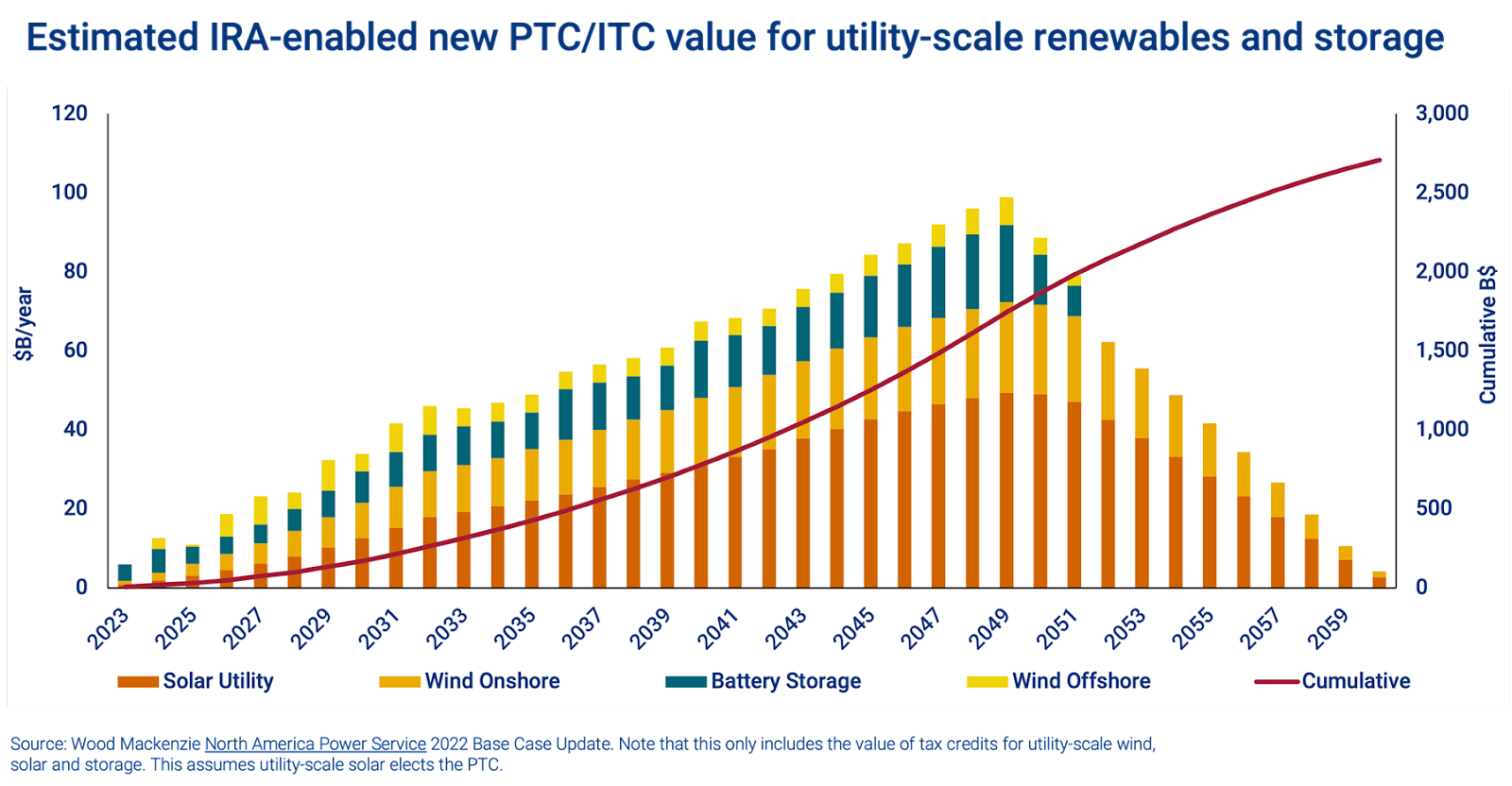

The IRA also enhanced the value of tax credits on a project-by-project basis. For example, developers can now monetize up to 70% of a solar project’s costs with the addition of bonus credits. Project developers typically are not able to absorb the tax benefits from their projects, and traditionally would tap into a $15B-20B tax equity market to finance the tax credit portion of any given project. With the enhancements from the IRA, the renewable energy sector could require up to 3.5x market growth by 2030 and possibly ~5x growth by 2049 according to demand projections by Wood Mackenzie. And that doesn’t even include fuels, CCUS, hydrogen, manufacturing or any of the other tax credits created by the IRA. That's a lot of external tax appetite being put to work that did not previously participate in this market.

Monetizing tax credits for project development will be one of the primary barriers to clean energy deployment, particularly in the initial years following the IRA legislation as corporate tax groups are educated on the opportunity to redirect their tax payments into renewable energy tax credit investments.

Recruiting capital into sustainable technology tax credits with transferability

Following the IRA, the question developers now face is how quickly and to what extent they'll be able to monetize these benefits as they execute on their development pipeline.

Tax credit-related capital has traditionally come from large banks such as JP Morgan Chase, Bank of America, Wells Fargo, and US Bank; a handful of banks account for the majority of tax equity investment capital in recent years.

The IRA legislation seeks to broaden this pool of capital to meet the anticipated demand represented above in the WoodMac chart. To do this, they created a transaction mechanism called Transferability which allows project developers to monetize their credits with a simple purchase-and-sale agreement, rather than the traditional equity partnership investment structure.

Here is a detailed description of transferability.

Transferability as a promising solution

Transferability isn't intended to replace traditional tax equity; instead, it gives corporate tax and treasury teams an alternative pathway to:

- Easily secure tax benefits to offset their federal income tax liability, and

- Participate in financing new, renewable energy and sustainability infrastructure that aligns with their corporate ESG goals

The value proposition for corporate taxpayers is simple: redirect your tax payments into clean energy projects and receive a discount on your federal tax liability. The reality is a little more complicated – tax credit purchases do carry some risks and reporting requirements, so partnering with third parties on transactions can often streamline the process. But earning an estimated 8%-10% discount on federal tax with controllable risks will be an attractive proposition to corporate taxpayers who may have chosen not to pursue traditional tax equity investments.

If the IRA is successful in its goal to scale more established technologies while kickstarting newer technologies like hydrogen and CCUS, a deep market for transferable tax credits could develop by 2030 with wider pricing spreads and creative structures used to pull more capital in from corporate taxpayers.

In conclusion, while it’s early days in the post-IRA renewable energy project finance market, the outlook is bright for both sustainable technology growth broadly speaking and for transferable tax credits sales specifically.

About Reunion

Reunion Infrastructure is leading the market on transferability as a service by packaging market expertise with core services needed to execute rapid, de-risked, and repeatable transferable tax credit transactions. Through its marketplace platform, Reunion provides:

- Access to a best-in-class range of project and tax credit types

- The ability to bundle different project or credit types into risk-adjusted portfolios

- Comprehensive due diligence and legal documentation to project buyers

- Access to tax credit insurance products

- Reporting services to ensure credit transactions are properly recorded

To learn more about Reunion, please contact Kevin Haley at kevin@reunioninfra.com.