Managing Corporate Alternative Minimum Tax (CAMT) with Transferable Tax Credits

With many companies facing the new corporate alternative minimum tax, clean energy tax credits are available to ease the burden.

.webp)

The new corporate alternative minimum tax (CAMT) is nothing if not complex. Created by the Inflation Reduction Act (IRA), the CAMT seeks to place a 15% “floor” under corporate taxpayers in order to raise revenues and force certain companies to bring their tax rate up to a uniform level. The number of companies affected is still unknown; the Joint Committee on Taxation estimated 150, but one estimate from KPMG exceeded 300 companies.

Implementation of the CAMT will take some time, as the specifics of the law are developed through IRS guidance and as corporate taxpayers calculate their exposure. In fact, the IRS has already granted penalty relief to companies who have not made estimated tax payments related to the new CAMT. But this relief is, of course, temporary and most companies affected by the CAMT will quickly start to look for viable ways to manage their exposure.

Fortunately, we already know that companies facing the CAMT may still utilize general business tax credits to reduce this tax liability back below the 15% threshold. And while the IRA created this burden, the IRA also created a possible solution in transferable clean energy tax credits that can be obtained with a simple purchase and sale agreement.

As tax teams figure out the CAMT and potential solutions, transferable tax credits are worth some analysis.

CAMT basics

In creating the CAMT, Congress is attempting to do at least two things. First, the CAMT is designed to ensure that profitable corporations pay at least some federal income tax, regardless of the deductions and credits they may claim under the regular tax system. Second, the CAMT is also intended to reduce the gap between the book income and taxable income of corporations, which has been a source of public criticism and scrutiny.

The CAMT applies to large corporations (other than an S-corp, regulated investment company, or real estate investment trust) that report more than $1 billion in profits to shareholders on their financial statements. The CAMT imposes a 15% minimum tax on the adjusted financial statement income (AFSI) of these corporations, which is their income before taxes as reported on their financial statements, with certain adjustments.

KPMG points out that, “Because AFSI diverges in significant ways from taxable income, corporations with a higher than 15 percent effective tax rate cannot assume they have no CAMT liability.” This also means that corporations which are already paying above a 15% effective tax rate may still be subject to CAMT liability.

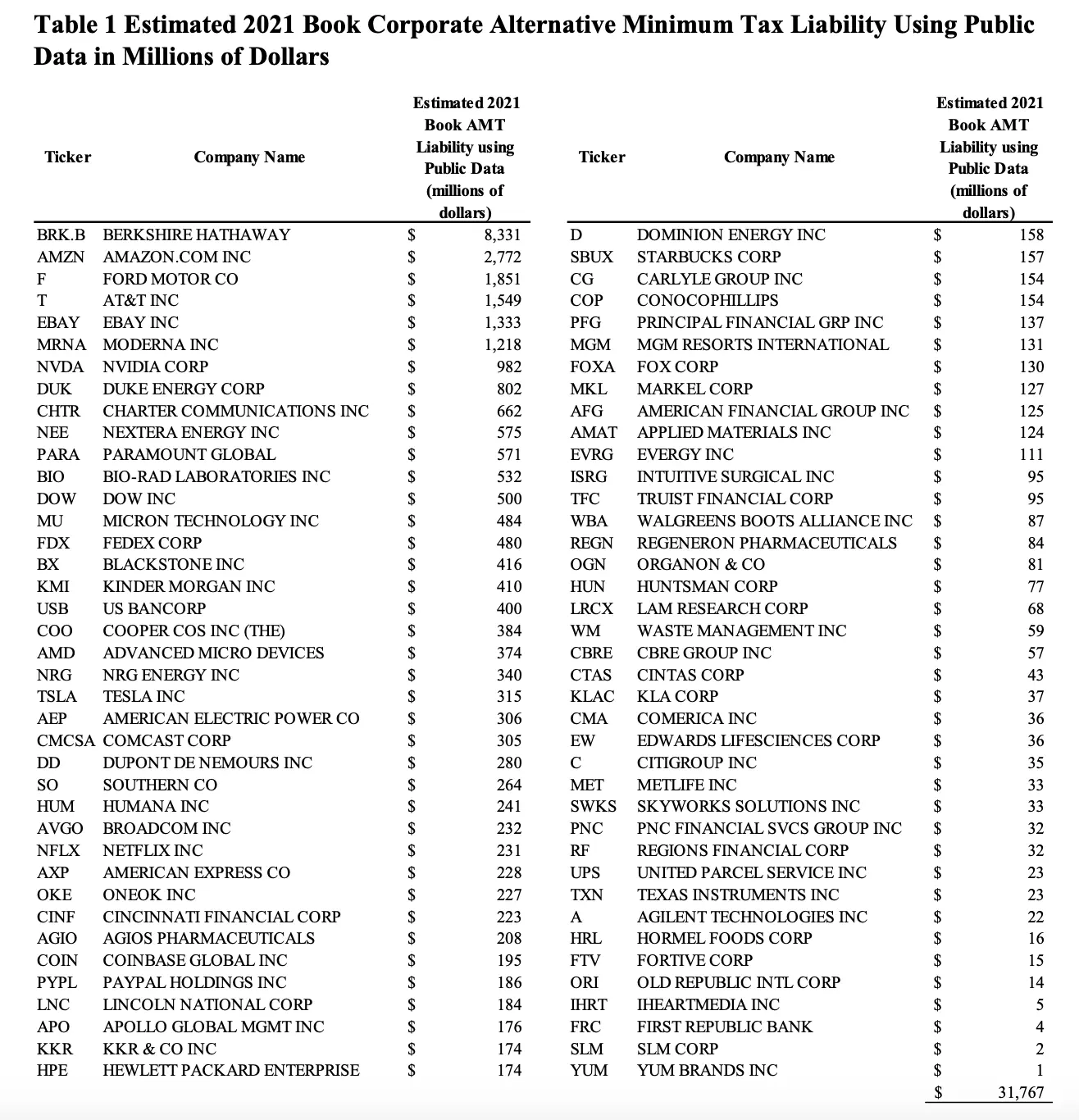

For example, here is a hypothetical review of what the CAMT’s impact could have been in 2021, from researchers at the University of North Carolina.

Transferable tax credits as a solution

One of the most important adjustments for the CAMT is the allowance of certain tax credits to reduce the CAMT liability–up to 75% of the combined regular and minimum tax. These credits include the same clean energy tax credits–Section 45 production tax credits and Section 48 investment tax credits, among others–that are enhanced by the IRA.

Practically speaking, this means that corporates facing CAMT liabilities can procure renewable energy tax credits via tax equity partnerships or the simpler transferability purchase and sale process to reduce any cash tax burden created or extended by the CAMT.

In addition, once companies are designated as “in-scope” for CAMT–meaning the minimum tax is applicable–that status is “hard to shake, even if income falls below the $1 billion threshold in future years,” per KPMG. So unless future guidance changes this fact, companies facing the CAMT may feel more comfortable structuring multi-year tax credit purchases.

Novogradac suggests that, on balance, this will drive greater appetite for tax credits: “The IRA created a 15% minimum tax on corporate book earnings, which could boost demand for tax credits since some public companies will have larger income tax bills due to the corporate minimum tax and may seek to offset a portion of that tax liability with federal income tax credits.”

In a separate article, however, Novogradac also flags some potential challenges for CAMT-affected companies exploring the tax equity route (as opposed to transferability, for example):

- “...partnerships would be required to report to their partners the allocable share of the partnership’s AFSI. This will likely mean that accountants for those partnerships will need to perform a new analysis that includes certain adjustments, such as for accelerated tax depreciation, to calculate each partner’s share of the partnership’s AFSI as defined by the new law…

- This language also appears to require the corporation to record the flow-through AFSI income and/or losses of the partnership to determine its own AFSI. For tax credit investments that are recorded using the proportional amortization method or other similar methods that account for income or losses “below the line,” this adjustment for investments in partnerships appears to require that income or loss be recorded “above the line” for purposes of determining the corporation’s AFSI.”

Given the preexisting complexities around tax equity investing, transferability appears to be a best-of-both-worlds solution for companies facing CAMT liability. By purchasing renewable energy tax credits, any of the companies in this camp can easily reduce their tax burden without introducing new layers of accounting complexity.

For an overview of transferability, download our transferable tax credit handbook.

Next steps for CAMT and transferability

The Treasury Department released transferability guidance in mid-June, 2023 to clarify the rules behind how these credits are bought, sold, and utilized. There were no major surprises and the guidance was generally friendly to credit buyers. Several key points of clarification include:

- Application to quarterly payments: Treasury formally blessed the application of credits to estimated quarterly payments. While this practice was common for tax equity investors already, receiving formal approval only helps streamline the application of transferable tax credits.

- Credit value is not taxable income: Treasury clarified that the value of the credit to the buyer–that is, the difference between a discounted price paid for the credit and the full dollar of tax savings–is not considered taxable income to the credit buyer.

- Recapture risk to the buyer is partially limited: The risk of credit recapture due to a change in project ownership sits with the developer, not the buyer. The buyer is still responsible for other types of recapture risk, but can secure protection against that with indemnification and insurance.

More clarity around CAMT will undoubtedly develop as companies calculate their exposure and Treasury offers additional guidance. But transferable tax credits will continue to be an attractive solution. Learn more about the Buyer Perspective on Transferable Tax Credits in 2025, where strategic purchasing and risk management remain key to maximizing value.